An absolute assignment of rents conceptually, if not by its very name, provides a mortgagee on an income producing property with the "absolute" right to rental income generated by the mortgaged property in the event of a default by the borrower. However, Tennessee's Bankruptcy Courts have given disparate treatment to the absolute assignment of rents in mortgage loan transactions. In order to create clear law and predictable outcomes, lenders should call upon the Tennessee legislature to craft a solution to the uncertainty caused by the conflicting court decisions.

The economic incentives on which an assignment of rents is based is nicely summarized as follows:

When a loan is secured by a mortgage or deed of trust on an income-producing property, such as an office building, shopping center, or apartment complex, rents are a significant part of the security of the loan, in addition to the land and improvements. Rents provide the funds necessary to pay for operating and maintaining the mortgaged property, and to make payments on the mortgage loan. After a default on the mortgage loan, a borrower, facing the possibility of losing the property to foreclosure, may apply rents to purposes unrelated to the property or the mortgage loan. The lender, on the other hand, wants rents collected after a default to be applied to operation and maintenance of the property or to the mortgage debt. Therefore, a lender wants the ability to control rents from the mortgaged property in the event of a default, and to this end will require the borrower to execute an assignment of rents at the loan closing.1

Given the status of the law today, a lender can no longer be certain that an assignment of rents will provide it with the ability to control rents from the mortgaged property after an event of default. Bankruptcy cases highlight this uncertainty.

When a borrower files bankruptcy the principal issue the lender faces is whether the post-petition rents generated by the debtor's business constitute "cash collateral" within the meaning of § 363 of the Bankruptcy Code. The lender expects that as a result having obtained an assignment of rents, the cash is not cash collateral because all rights to the rents generated by the debtor's business were "absolutely" assigned to the lender. The debtor, however, asserts that it retained some rights in the rents even after the assignment and thus the cash is simply cash collateral that the debtor can use in its bankruptcy case so long as the lender's interest is adequately protected. The determination of this issue depends on whether the assignment of rents at issue effectively transferred the rents absolutely to the lender or was merely a grant of a security interest in the rents. A lender with a separate loan document titled "Absolute Assignment of Rents" may believe this is a non-issue and that it will be permitted to control the rents. However, the Tennessee bankruptcy courts do not agree.

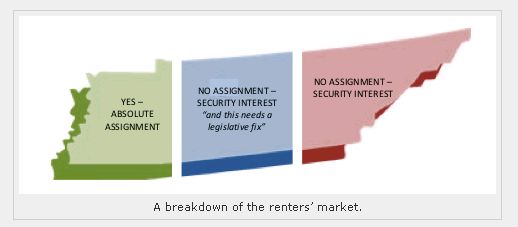

In 2010, the United States Bankruptcy Court for the Western District of Tennessee held that an assignment of rents was an absolute assignment rather than the grant of a security interest. The decision was affirmed by the District Court2. However, in 2011, on the other side of the State, the United States Bankruptcy Court for the Eastern District of Tennessee found that: "an assignment of rents absolute on its face will nevertheless be viewed as a security interest3." Exemplified by these decisions, Tennessee courts have for years ruled inconsistently as to whether an assignment of rents is absolute or for security.

A September 2012 hearing in the United States Bankruptcy Court for the Middle District of Tennessee was the impetus for writing on this topic. The Middle District found that an absolute assignment of rents was a grant of security and found the rents constituted property of the estate4. As a result, the post-petition rents generated by the debtor's business were determined to be cash collateral, and the debtor was permitted to use the rents after providing the lender adequate protection. After announcing his decision from the bench, the bankruptcy judge noted the existence of conflicting decisions interpreting absolute assignment of rents. The judge also acknowledged the difficulty lawyers faced in advising their clients on how an assignment of rents would be interpreted by the Bankruptcy Court. The judge further suggested that a legislative fix might be needed to give stakeholders more clarity and certainty on what rights parties have when they enter into an absolute assignment of rents.

As it exists today, the law interpreting absolute assignment of rents is uncertain and inconsistent. This will result in further litigation and expense for all parties. Eventually a trend will develop from court decisions that answers this question, but a judicial solution may result in a determination that an absolute assignment of rents is merely a security interest. A legislative fix will be more certain and can establish the parties' rights under an assignment of rents. A legislative fix could also save the parties and the court's expense and time by limiting future litigation on this issue. If lenders want certainty that they will be able to control a debtor's rents in a bankruptcy proceeding by virtue of obtaining an absolute assignment of rents then it is time to seek a legislative fix.

Footnotes

1 Still Crazy After All These Years: The Absolute Assignment of Rents In Mortgage Loan Transactions, 59 Fla. L. Rev. 487, 488-89 (July, 2007) (This article relies heavily on this law review article and its in depth discussion of this issue. A reader interested in a more in depth discussion of this issue will find this article informative.)

2 460 Tennessee Street, LLC v. Telesis Community Credit Union, 437 B.R. 306 (W.D. Tenn 2010).

3 In re Senior Housing Alternatives, Inc., 444 B.R. 386, 396 (Bankr. E.D. Tenn. 2011). (Noting at footnote 7, the existence of differing decisions).

4 In re Shreibman (Protective Life Ins. Co. v. Shreibman), Case No.: 12-05272 pending in the United States District Court for the Middle District of Tennessee

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.