- within Intellectual Property topic(s)

With the world continuing to experience major disruption via ongoing war and an unsettled economy, there is an opportunity for retailers to make sense of the noise and focus on significantly reducing COGS by going on an offense vs. playing defense with suppliers.

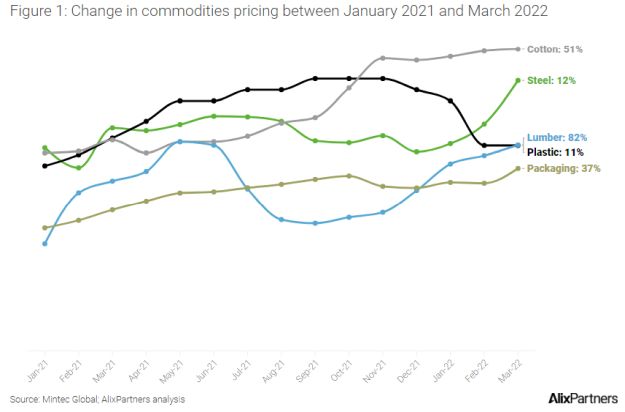

Through Q1 2022, major input commodity markets saw large increases across the board, driving COGS to previously unseen levels. The increased consumer buying power helped retailers combat these rising costs as they hiked prices to maintain margin dollars.

However, the sudden decline in consumer demand driven by record inflation is causing retailers to be squeezed from both ends. Despite significant declines in other core input commodities (e.g., freight, plastic, steel, cotton, etc.), pushing back on suppliers reactively has proven to be harder than anticipated given continued labor scarcity leading to higher input labor cost.

For retailers to be successful in the current environment, they need to transition their mindset from a reactive and defensive state to a proactive and offensive state focused on identifying and tracking underlying cost drivers and accurate should-cost models for all sets of product types. These should be used to quantify clawback opportunities based on the key movements of raw material, freight, and production input costs levied during 2020 and 2021.

Over the last few months, retailers have understandably been focused on driving a strong holiday season while managing inflated inventories. However, this is the time to pay close attention to the shifting power dynamics governing supplier relationships.

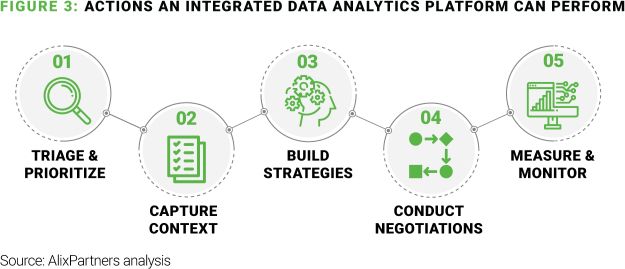

An integrated data analytics platform can help retailers analyze and highlight clawback opportunities, empowering successful negotiations with suppliers. Inputs into the platform can include historical and future cost-change data and criticality of the brand and supplier, among others. This helps tailor individual approaches for each supplier, develop custom negotiation asks and areas of leverage, assess supplier responses, finalize associated decisions, and monitor cost/price change impacts. It also allows for continued tracking of relevant indices for future opportunities.

Proactively engaging in cost reduction/claw back discussions should be at the forefront of retailers' priorities in early 2023. Here's how to get started:

Utilize the downward shift in input costs: Nearly all core commodities are down significantly from their peaks set during the pandemic and its aftershocks, with most forecast to trend further downward. While cost increase levies came fast and furious from suppliers at the time, you likely have not seen many cost concessions even as markets trend the other way. Now is the time to focus on should-cost, accounting both for raw material and freight and production inputs, and gear up for supplier negotiations.

Create a plan for supplier negotiations: Preparing for and scheduling discussions with suppliers should be at the forefront of your planning. These should occur irrespective of if the meetings fit within the normal course of business, be it line reviews or transition discussions. Remain flexible in the potential levers utilized within negotiations: with direct cost concessions remaining the primary goal, but also be open to incremental funding of all types as well as improved commercial terms. Proper communication is key, with goals and expectations for the meeting clearly outlined, along with timing for follow-up discussions and next steps.

Reduce barriers to sustaining results: Prioritize this within your organization by defining clear roles and responsibilities within both the merchandising/sourcing group as well as standing up a focused cost-control team. Transition responsibilities and align incentives as necessary to increase overall visibility and accountability to negotiation outcomes. Make the cost control team responsible for ongoing reviews of supplier product costing, tracking underlying commodity trend changes, and aligning on triggers for associated business actions.

The retail industry finds itself at yet another inflection point. Although it may be enticing to add this to-do to your merchants' already overflowing plates, there is risk that you will lose this opportunity if not done right. Retailers should be looking for 15-25% in savings driven largely by clawbacks of most of the cost increases taken over the past two years and rightsizing COGS. Those that do will put themselves in a much stronger position relative to competitors as planning continues for 2023 and beyond.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.