Individual Savings Accounts (ISAs) are attracting greater attention from investors.

Next April ISAs will reach their 25th anniversary. Over the years the appeal of ISAs has waxed and waned due largely to two main factors: the tax environment and potential investment returns.

In 2023, these factors mean ISAs may once again rise in popularity:

- Prolonged freezes to the higher rate tax threshold and personal allowance reductions to both the dividend allowance and capital gains tax annual exempt amount and a lower threshold for additional rate tax have made the UK tax shelter offered by ISAs more attractive.

- Improved share market conditions and higher yields from fixed interest securities (bonds) will improve the appeal of stocks and shares ISAs.

The government's attention meanwhile has been elsewhere – the main ISA contribution limit of £20,000 has been unchanged since April 2017.

If you have existing ISAs, it is important that you review them regularly to maximise the tax benefits and ensure continued suitability. If you have cash ISAs, that review includes considering whether switching to a stocks and shares ISA would be appropriate. Even at today's higher interest rates (not always passed on to cash ISA savers), the returns are well below the current inflation rate.

Seeking advice is important for stocks and shares ISAs, not only regarding fund selection, but also in balancing the holdings with other investments owned directly or within your pension.

✢ Investments do not offer the same level of capital security as deposit accounts. The value of your investment, and the income from it, can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit with your overall attitude to risk and financial circumstances.

The Financial Conduct Authority does not regulate tax advice. Tax treatment varies according to individual circumstances and is subject to change.

Pensions

Beyond a minimum retirement

A third of people will be unable to afford their retirement, according to a new report.

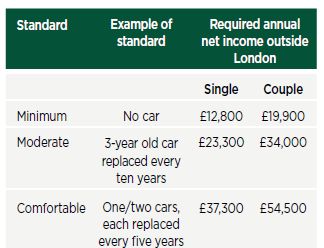

Research from major pension provider Scottish Widows has estimated individual future retirement incomes and compared them with the three living standard levels set by the Pensions and Lifetime Savings Association:

If you find yourself thinking that the comfortable standard is where you would like to be:

- Even if you and your partner each have a full state pension of £10,600 a year, there would still be a net income shortfall of over £33,000 once the state pension comes into payment (at age 67 from April 2028).

- That net income figure excludes rental or mortgage costs, which are increasingly encroaching into retirement.

- Just over a third of people are on target to reach the comfortable standard, a proportion that falls to about one in five for the self-employed.

The research also showed that 35% of people are on track to fall below the minimum retirement standard. For the self-employed, the corresponding proportion is 48%, with another 25% reaching only the minimum threshold. Working out which retirement standard – if any – that you are currently on course for is not straightforward: the launch of the government's long promised 'pensions dashboard' is not due until October 2026.

For a snapshot of your future retirement, talk to us. We can review the financial information you have already supplied, allowing us to identify your potential position and discuss possible strategies.

✢ The value of your investment, and the income from it, can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

Occupational pension schemes are regulated by The Pensions Regulator.

To view the full article please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.