From 2019, every company that is subject to VAT in Switzerland and has a worldwide minimum turnover of CHF 500,000 must pay a contribution for radio and TV. The basis of this contribution liability thus changes: whereas previously this depended on whether or not the company had a receiver, this new contribution in the future will generally affect every single company.

What does this mean for my company?

As soon as a company is listed in the Swiss VAT register, it generally becomes liable for this contribution. Small companies with a turnover of less than CHF 500,000 are exempt. If a com-pany is in the lowest contribution category (see table below), it can demand reimbursement of the contribution if it has achieved minimal or no profit in the year concerned. An exemption based on evidence that no devices for the reception of radio or television broadcasts are in use shall no longer apply.

Do I also have to pay as a foreign company?

Based on the partial revision of the Swiss VAT law as of 1 January 2018, more foreign companies without a registered office, domicile and operating facilities in Switzerland are liable for VAT:

All companies that are either located in Switzerland or provide services in Switzerland and whose turnover worldwide is made up of services not exempt from tax to the amount of CHF 100,000 are subject to mandatory VAT as of 1 January 2018.

From 1 January 2019, every company in Switzerland which sends small consignments exempt from import duty (i.e. the import duty would not be more than CHF 5) from abroad into Switzerland to a value of at least CHF 100,000 per year shall be liable to pay VAT.

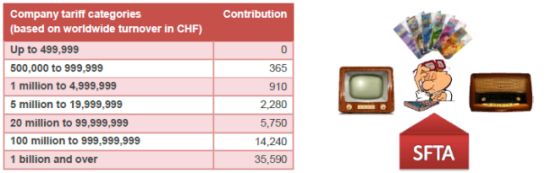

How are the contributions calculated?

The contributions are based on the worldwide overall turnover of each individual company. Turnover which qualifies as exempt or excluded in accordance with the Swiss VAT law is also included in this calculation. The basis of assessment for the first collection is the overall turn-over of the year before last, i.e. overall turnover from 2017 is decisive for contribution duty for 2019.

The basis of assessment for the subsequent years is the overall turnover for the previous year, i.e. contribution duty 2020 is based on overall turnover in 2019. How much a company has to pay depends on the tariff category.

What do I have to think about?

A company is liable for contributions from the year following that year in which it has exceeded the crucial turnover limits stated above. If a company achieved annual turnover of more than CHF 500,000 in one year, it is liable to pay the contribution in the following year. In the first year of the system switchover, i.e. in 2019, the turnover from 2017 is generally decisive. If group taxation applies, the overall turnover of the VAT group is decisive, with only one contri-bution being payable.

As soon as all VAT calculations have been received by the Swiss Federal Tax Administration (SFTA), the annual overall turnover will be calculated by the SFTA and an invoice issued (nor-mally between February and October). Payment is due 60 days after receipt of the invoice. If the company paying the contribution is in credit with the SFTA, the SFTA may offset the owed contribution against any outstanding credit.

It is our opinion that it is still not completely clear how the amount of the contributions will actually be calculated in the first year. So many new VAT registrations of foreign companies have been added in 2018. The 2017 baseline figures for all of these companies that are now subject to radio and TV contributions are completely unknown. It will be interesting to see how the SFTA calculates the amount of contribution for all these newly included companies. Of course we are happy to offer our support and assistance once the first invoices for this new contribution arrive.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.