On 1 January 2022, the Regional Comprehensive Economic Partnership Agreement (RCEP) officially came into force for Vietnam. RCEP is the world's largest free trade area among the ASEAN countries, China, South Korea, Japan, Australia, and New Zealand. It accounts for approximately 30% of the world population with a total gross domestic product of approximately USD 25.527 trillion. The RCEP not only promises to eliminate approximately 90% of the trade tariff between the contracting parties within 20 years but also requires businesses in the contracting parties to increase their competitive capacities in the challenging free trade market. It is expected to bring many opportunities for the contracting parties to strengthen the value chain. In that context, efficient tools for the contracting parties to protect their domestic manufacturing businesses are the trade remedies, which are permitted by the World Trade Organisation (WTO) and commonly recognised within the regime of free trade agreements (FTAs). Trade remedies such as anti-dumping, countervailing, and transitional safeguard measures are prescribed in Chapter 7 of the RCEP. Circular No. 07/2022/TT-BCT (Circular 7) was promulgated by the Ministry of Industry and Trade (MOIT) and provides further guidance on implementing the trade remedies as stipulated in the RCEP.

This update highlights several remarkable points under Circular 7 about the transitional safeguard measures and the antidumping measures.

1. Transitional Safeguard Measures

1.1. Application of Transitional Safeguard Measures

1.1.1. The Transitional Period

Under the RCEP, the transitional safeguard measures are applied within the transitional period commencing from the date of Vietnam's entry into force. Given that each product to be imported into Vietnam shall be subject to different timelines for elimination or reduction of the customs duty according to Vietnam's Schedule of Tariff Commitments under the RCEP, the transitional period varies subject to the aforesaid timeline applied to each particular product.

It shall not last more than eight years after the date on which the elimination or reduction of the customs duty on that good is completed.

1.1.2. Principles of Application

As defined in Circular 7, the transitional safeguard measures under the RCEP are defined as the special safeguard measures prescribed in the 2017 Law on Foreign Trade Management. Accordingly, MOIT shall decide if these special safeguard measures shall be imposed on imports into Vietnam deemed detrimental to domestic manufacturing. Because the special safeguard measures, which can only be applied within the transitional period, are separate from the general safeguard measures prescribed in the 2017 Law on Foreign Trade Management, Circular 7 explicitly provides that the transitional safeguard measures and the safeguard measures cannot be applied at the same time for the same imported goods.

1.2. Grounds for Application of the Transitional Safeguard Measures

According to Circular 7, any organisation or individual in Vietnam manufacturing similar goods or goods deemed competitive with the imported goods of other member states of the RCEP is entitled to submit an application to MOIT for the imposition of the transitional safeguard measures on such goods. Accordingly, as prescribed in Circular 7, MOT shall investigate the concerned imported goods and then decide whether the transitional safeguard measures should be applied based on all the following grounds:

- There is an absolute or relative increase in quantities of imported goods benefiting from the special incentive rates of customs duty under the RCEP, compared to those of 'like goods' and directly competitive goods domestically produced in Vietnam;

- The domestic manufacturing industry will be or threatens to be impaired seriously; and

- There is a causal relationship between the abovementioned increased imports and the seriously or potential serious impairment caused to the domestic manufacturing industry.

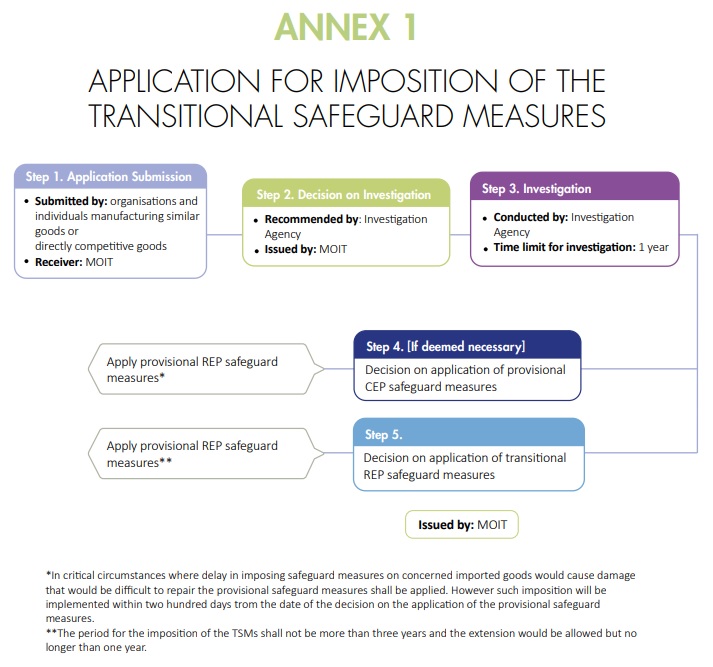

The process of handling an application for the imposition of transitional safeguard measures is demonstrated in the chart in Annex 1 of this update.

1.3. Remedy Measures if the Transitional Safeguard Measures are Applied

As per Circular 7, the following measures may be imposed:

- Suspend the further reduction of any rate of customs duty provided for in the RCEP on the good originating from an RECP party; or

- Impose the safeguard duty in the form of an additional

customs duty on the originating good, provided that the sum of the

customs duty under Vietnam's schedule of tariff commitments and

the safeguard duty shall not exceed the lower amount of the

most-favoured-nation applied rate of customs duty in effect on the

day:

- when the transitional safeguard measures are applied; or

- immediately preceding the date of entry into force of the RCEP for Vietnam, 1 January 2022.

2. Methods of Calculation of Dumping Margin

Dumping margin is a method of trade protection aimed at preventing exporting countries from dumping goods cheaply on a domestic market. The dumping margin needs to be calculated to evaluate whether the antidumping measure should be applied. For example, if the dumping margin exceeds de minimis, e.g. 2%, the anti-dumping duty may be applied.

As aligned with the Agreement on Implementation of the 1994 General Agreement on Tariffs and Trade (GATT 1994) (Antidumping Agreement), and Decree No. 10/2018/ND-CP that guides the implementation of the 2017 Law on Foreign Trade Management provides for the following methods of calculating the dumping margin:

- Comparison of weighted average normal value with a weighted average of export prices (WA-WA); or

- Comparison of normal value and export prices on a transaction-to-transaction basis (T-T).

(Dumping Margin Calculation Methods)

Under the Dumping Margin Calculation Methods, all the individual dumping margins shall keep their original value, whether positive or negative. In the practice of zeroing, all export transactions which include negative results of calculation between domestic market prices and export prices shall not be considered. This prevents negative results are offset against the positive ones. As stipulated by the RCEP and reiterated in Circular 7, zeroing cannot be applied to the abovementioned Dumping Calculation Methods.

3. Conclusion

For those who are doing business in Vietnam and having manufactured products in competition with products from other exporting countries, it is worth paying more attention to trade remedies provided under the treaties and utilise these protection measures in a more effective way to protect its domestic production in the context of the global competition and economic integration.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.