- within Immigration topic(s)

Australia: Important update for partner visa holders

Australien: Wichtiges Upate für Inhaber eines Partnervisums

The Department of Home Affairs has announced that holders of certain partner visas can submit their information for the permanent residence phase if two years have passed since the visa application was submitted.

The key points are:

This announcement applies to holders of a provisional partner visa (subclass 309) or a temporary partner visa (subclass 820).

Partner visa holders can find further information at:

- For partner visas (subclass 309), you can find the relevant information on the Australian Department of Home Affairs website HERE

- For partner visas (subclass 801), you can find the relevant information on the Australian Department of Home Affairs website HERE.

If this has changed for the partner visa holder, e.g., if the relationship has ended, you can find the relevant information on the Australian Department of Home Affairs website HERE.

Das australische Innenministerium hat bekannt gegeben, dass Inhaber bestimmter Partnervisa ihre Informationen für die Daueraufenthaltsphase einreichen können, wenn seit der Beantragung des Visums zwei Jahre vergangen sind.

Die wichtigen Punkte sind:

Die Bekanntmachung gilt für Inhaber eines vorläufigen Partnervisums (Unterklasse 309) oder eines befristeten Partnervisums (Unterklasse 820).

Weitere Informationen finden Inhaber eines Partnervisums auf:

- Für Partnervisa (Unterklasse 309) finden sie aufder Homepage des australischen Department of Home Affairs die entsprechenden Informationen HIER

- Für Partnervisa (Unterklasse 801) finden sie aufder Homepage des australischen Department of Home Affairs die entsprechenden Informationen HIER.

Sollten sich die Umstände des Inhabers eines Partnervisums geändert haben, z. B. wenn die Beziehung beendet wurde, finden sie aufder Homepage des australischen Department of Home Affairs die entsprechenden Informationen HIER.

Croatia: Digital Nomad Visa now available for max. 36 months

Kroatien: Digital Nomad Visa jetzt verfügbar

This visa allows for an initial stay of 18 months and, as of this month, the possibility of an additional extension of another 18 months, bringing the total length of stay to 36 months.

Overview: Since January 1, 2021, foreign nationals have been able to apply for a temporary residence permit without sponsorship from a local business.

At the beginning of 2025, this maximum length of stay was extended to 18 months, until now in August 2025, when the possibility of an additional 18-month extension was added.

Dieses Visum ermöglicht einen ersten Aufenthalt von 18 Monaten und seit diesem Monat zusätzlich mit der Möglichkeit einer zusätzlichen Verlängerungsmöglichkeit von weiteren 18 Monate, wodurch sich die Gesamtdauer des Aufenthalts auf 36 Monate erhöht.

Übersicht: Seit dem 1. Januar 2021 konnten Ausländer ohne Sponsoring durch ein lokales Unternehmen eine befristete Aufenthaltsgenehmigung beantragen.

Anfang 2025 wurden diese maximale Aufenthaltsdauer auf 18 Monate verlängert, bis jetzt im August 2025, als die Möglichkeit einer zusätzlichen Verlängerung um 18 Monate hinzukam.

Singapore: New salary comparison table by industry now available

Singapur: Neue Gehaltsvergleichstabelle nach Branchen jetzt verfügbar

The Ministry of Labor has published the new salary comparison table for the Complementarity Assessment Framework (COMPASS), the points-based assessment system that applies to all work permit (EP) applications.

The recently published salary comparison table applies to initial work permit applications submitted on or after January 1, 2026, and to EP renewal applications expiring on July 1, 2026.

The current salary comparison table applies to initial work permit applications submitted between January 1, 2025, and December 31, 2025, and to work permit renewal applications expiring between July 1, 2025, and June 30, 2026.

To receive points under the COMPASS salary criterion (category "C1"), employers must ensure that their foreign workers meet the minimum salary requirements set out in the COMPASS comparison table. If the applicant's salary does not meet the requirements of the COMPASS comparison table, no points will be awarded under COMPASS category C1 and the applicant must earn points under other COMPASS criteria to qualify for a work permit or work permit extension.

Das Arbeitsministerium hat die neue Gehaltsvergleichstabelle für den Complementarity Assessment Framework (COMPASS) veröffentlicht, das punktebasierte Bewertungssystem, das für alle Anträge auf eine Arbeitserlaubnis (EP) gilt.

Die kürzlich veröffentlichte Gehaltsvergleichstabelle gilt für Erstanträge auf eine Arbeitserlaubnis ab dem 1. Januar 2026 und für Verlängerungsanträge für EPs, deren Gültigkeit am 1. Juli 2026 abläuft.

Die aktuelle Gehaltsvergleichstabelle gilt für Erstanträge auf Arbeitserlaubnisse, die zwischen dem 1. Januar 2025 und dem 31. Dezember 2025 eingereicht werden, sowie für Verlängerungsanträge für Arbeitserlaubnisse, deren Gültigkeit zwischen dem 1. Juli 2025 und dem 30. Juni 2026 abläuft.

Um Punkte im Rahmen des COMPASSGehaltskriteriums (Kategorie C1") zu erhalten, müssen Arbeitgeber sicherstellen, dass ihre ausländischen Arbeitnehmer die in der COMPASSVergleichstabelle festgelegten Mindestgehaltsanforderungen erfüllen. Wenn das Gehalt des Antragstellers nicht den Anforderungen der COMPASSVergleichstabelle entspricht, werden keine Punkte unter der COMPASS-Kategorie C1 vergeben und der Antragsteller muss Punkte unter anderen COMPASSKriterien sammeln, um sich für eine Arbeitserlaubnis oder Arbeitserlaubnis-Verlängerung zu qualifizieren.

Entsendungen ins Ausland

(in deutscher Sprache)

Fokus: Richtige Versicherungsunterstellung – ausreichender Versicherungsschutz & steuerliche Komplikationen vermeiden

Compliance wird immer wichtiger. In diesem Praxisseminar werden Lösungsansätze für die richtige (sozial-)versicherungsrechtliche Unterstellung aufgezeigt.

Bei Entsendungen von der Schweiz ins Ausland werden zudem verschiedene Optionen für einen ausreichenden Versicherungsschutz während eines Auslandeinsatzes besprochen. Auch die steuerrechtliche Beurteilung steht bei Entsendungen weiterhin im Mittelpunkt, sodass die gesetzlichen Regelungen anhand von Praxisbeispielen behandelt werden.

Social security and tax law challenges of working on a project abroad

FRIEDERIKEV.RUCH, CONVINUS

Working on a project abroad presents a variety of challenges that are often closely interlinked. One of the main hurdles is cultural differences, which are often underestimated. Different working styles, communication norms, and business practices can lead to misunderstandings and hinder the success of a project or, in the worst case, prevent it altogether if expectations are not clearly conveyed or communicated for these reasons. In addition, there are legal and regulatory requirements: local laws, taxes, work permits, insurance coverage, compliance requirements, and certifications must be carefully observed to avoid penalties or disadvantages. Language barriers often exacerbate this tension, as they can make communication, documentation, and internal processes more difficult.

In the following, we will look at the tax and social security aspects of a project assignment. The focus here is on the fact that the project assignment takes place in a country other than the one in which the employee has his or her employment relationship, and in which the employer has its registered office and the employee has his or her place of residence. The project assignment is therefore a type of assignment.

1. Social security

In the case of a temporary project assignment, social security coverage usually remains in the home country (this is usually the employee's country of residence or the country in which the employee was covered by social security prior to the assignment), provided this is legally possible.

The aim is also to avoid possible social security contributions in the country of destination and to obtain equivalent insurance coverage for the employee during the project assignment.

Double insurance can only be avoided if there is a corresponding agreement between the two countries and the insurance branches are specified in this agreement, and if the national law of the country of assignment provides for an exemption.

The various agreements would be:

- EU-Switzerland Agreement on the Free Movement of Persons

- EFTA Agreement

- Bilateral social security agreements

- Other multilateral agreements.

1a) Project assignment from an EU/EFTA country to Switzerland

In the case of a project assignment from Poland to Switzerland, for example, the following points would have to be taken into account:

- Verification of the employee's nationality to ensure the correct agreement is applied

- If the employee is an EU or Swiss citizen, the provisions of the Agreement on the Free Movement of Persons apply

- During the assignment, the employee remains covered by social security in their home country (in this case, Poland) in all insurance branches

- They can be exempted from social security contributions (in all insurance branches) in Switzerland

- An A1 certificate must be obtained from the competent social security institution in the home country for a period of, as a rule, a maximum of 24 months. If there is still a bilateral social security agreement between the two countries, the period can be extended to a maximum of 6 years under an exemption procedure.

In order for the employee to remain insured in their home country, the following conditions must be met:

- The employee is an EU or Swiss citizen

- The employee was subject to the social security system in Poland before working in Switzerland

- The employment relationship remains in Poland

- The assignment in Switzerland is temporary

- Social security contributions continue to be paid in Poland on the entire income from employment.

For project assignments from an EFTA country to Switzerland, the provisions of the EFTA Agreement apply, which are identical to the provisions of the Agreement on the Free Movement of Persons. The EFTA Agreement also contains a restriction regarding citizenship; it only applies to persons who are citizens of an EFTA member state or Switzerland.

1b) Project assignment from a non-EU/EFTA contracting state to Switzerland

As long as there is a social security agreement between the two countries involved, the aim is also for the employee to remain insured in their home country for the duration of the project assignment and to be exempted in the country of assignment.

However, the following must also be taken into account:

- The employee's nationality is irrelevant for the application of the social security agreement.

- The employee must have been insured under the social security system in their home country prior to the assignment (usually for at least 1 month beforehand).

- The project assignment in the other contracting state must be limited in time. As a rule, this applies for a maximum of 5 to 6 years.

- During the assignment, the employee usually remains insured in all branches of social security in their home country.

- They may be exempted from social security contributions in the country of assignment, but only for the types of insurance covered by the agreement. This may therefore lead to double insurance/double coverage

- Contributions must be calculated and paid on the entire earned income

- A certificate of secondment must be obtained in the home country, confirming social security coverage in the home country.

1c) Project assignments from a non-contracting state to Switzerland

If there is no social security agreement between the two countries, the employee is subject to social security contributions in the country of assignment in accordance with the national legal regulations.

As a rule, it is checked whether the employee can remain insured in their home country, which ultimately leads to double coverage.

In practice, this results in a number of additional challenges. For example, the employee must then actually pay social security contributions in both countries, or the question arises as to what happens if the employer pays these contributions. If the employer pays all contributions in the country of assignment and the employee has the option of having the contributions refunded, how can it be ensured that the employer will ultimately receive them?

2. Taxation

Another point to consider is the question of taxation during the project assignment, not only at the employee level, but also at the company level. Depending on the duration of the project assignment, different tax aspects must be taken into account if there is a double taxation agreement between the two countries involved:

- < 183 days in the calendar year/tax year/12-month period in the country of assignment: In most situations, tax liability remains in the home country and there is no tax liability in the country of assignment. If tax liability arises in the country of assignment, this is usually only a limited tax liability.

- ≥ 183 days in the calendar year/tax year/12-month period in the country of assignment: As a rule, the employee becomes subject to unlimited tax liability in the country of assignment.

2a) 183-day rule

All double taxation agreements (DTAs) contain a 183-day rule, which is always structured in the same way in principle. The only difference is how the 183 days are counted.

The 183-day rule contains the following three conditions, all of which must be met in order for there to be no tax liability in the country of assignment:

- Stay of less than 183 days in the country of assignment. The 183 days are counted either in a 12- month period, in a calendar year, or in a tax year.

- No salary payments from the country of assignment

- No costs are passed on to a permanent establishment or company in the country of assignment.

In addition to the 183-day rule described above, it must also be checked whether an additional regulation (economic or de facto employer) may apply in the country of assignment.

If one of these four conditions is not met, the country of assignment may tax the earned income. In Switzerland, this leads either to withholding tax or to taxation in the context of filing a tax return.

As soon as an employee registers in Switzerland, this automatically results in the person being entered in the tax register. This requires the submission of a tax return ( ), in which worldwide income and assets must be declared, but does not result in these being taxed in Switzerland. For worldwide income and assets to be taxed in Switzerland, the employee's center of life must also be relocated to Switzerland. This is usually not the case for short-term project assignments of up to 12 months.

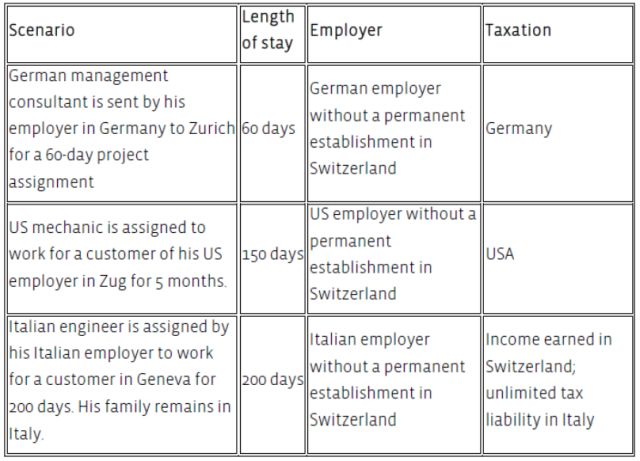

2b) Example scenarios

2c) Practical considerations for project assignments

Every cross-border project assignment should be reviewed from a tax perspective before it begins. The following points, among others, should be taken into account:

- Is there a double taxation agreement?

- For assignments lasting a maximum of 6 months: How are the 183 days counted, does the employee stay in the country of assignment for less than 183 days, are costs incurred in the country of assignment, is salary paid in the country of assignment, is there a regulation regarding economic or de facto employers?

- Tax rates can vary greatly depending on the location of the assignment (even within the same country).

- Expense regulations: Per diems and expenses are only partially tax-free

- Are there tax return obligations in the country of assignment?

- If tax liability arises in the country of assignment, what happens to tax liability in the home country?

- Does the assignment lead to additional tax costs that are reimbursed as part of a tax equalization procedure?

- Does the employee create a permanent establishment while performing their work during the project assignment?

3. Example: Project manager from England with a project assignment in Zug

Initial situation

- Employer: Engineering company based in London (England)

- Employee: Senior project manager, British citizen

- Project: Management of a construction project for a new office building in Basel-Stadt

- Duration: 85 days

- Location: Basel-Stadt, Switzerland

Employment contract / labor law

The employee will receive a supplementary agreement to his current employment contract, which regulates all aspects of the project assignment. English labor law will continue to apply to him during the assignment, but with consideration given to the relevant legal regulations in Switzerland.

Work permit

Following Brexit, England is considered a third country in Switzerland and English citizens are considered third-country nationals. Transitional provisions are currently still in force, which will generally expire on December 31, 2026, meaning that the registration procedure can still be carried out at present.

For this assignment, either the registration procedure could be carried out for the employee or a 120-day permit could be obtained.

As part of the registration procedure, the days of employment must be reported individually, which involves a great deal of administrative effort. In addition, registration via the "EasyGov" registration portal must be completed at least 8 days before the first day of employment. To make matters more difficult, employers only have a quota of 90 calendar days in a calendar year for using the registration procedure.

The 120-day permit would certainly be the simpler option, as it would allow the employee to stay and work in Switzerland for a maximum of 120 days within a 12-month period. The employee can come to Switzerland on their own, without prior notification to the authorities. However, it usually takes between 3 and 4 weeks on average from the time of application to the receipt of this permit.

To view the full article, click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.