- within Wealth Management topic(s)

- in United States

- within Wealth Management topic(s)

- in United States

- within Wealth Management, Litigation, Mediation & Arbitration and Law Practice Management topic(s)

- with readers working within the Banking & Credit industries

Impairment is often viewed as a point-in-time accounting conclusion rather than a reflection of how capital decisions play out over time. That perspective is becoming harder to sustain as investment models grow more complex and assumption-driven.

For many CFOs and controllers, accounting for impairment has long been treated as a technical assessment performed after capital decisions are made, budgets finalized, and strategies set. If the analysis clears the accounting threshold, teams usually move on, relieved to avoid impairment for another year. In today's environment, that framing is increasingly insufficient—a shift that has meaningful implications for those responsible for capital allocation, forecasting, and audit readiness.

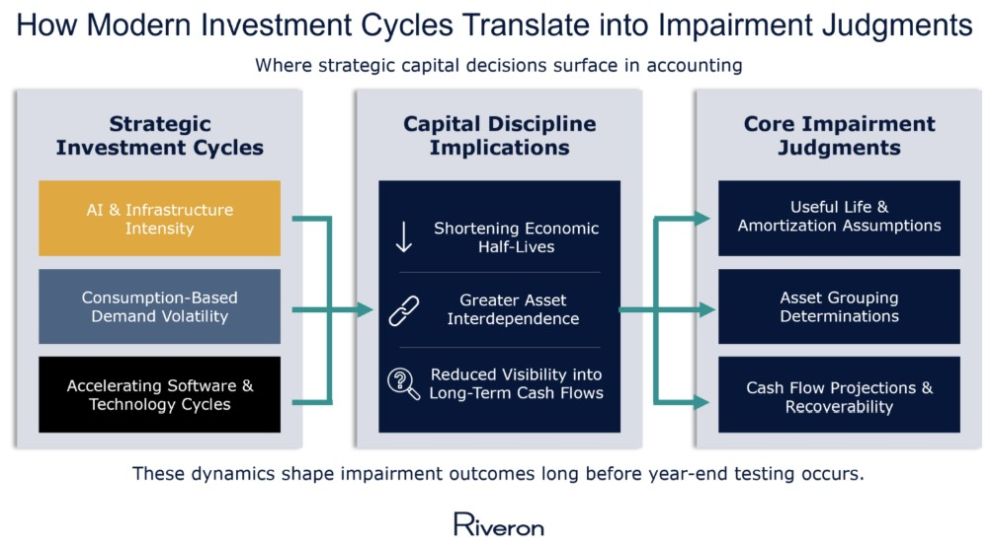

Capital deployment has changed materially. Investments in AI infrastructure, specialized hardware, internal-use software, and technology-enabled operations have accelerated, often with shorter economic half-lives, greater interdependencies, and more volatile demand assumptions than traditional assets. Business models have also become more dynamic, shaped by faster pivots, evolving pricing structures, and heavier reliance on forward-looking forecasts.

Viewed through the right lens, accounting for impairment is less about avoiding write-downs and more about reinforcing capital discipline.

What hasn't kept pace is how impairment is typically approached across finance and accounting functions. Even for companies that completed year-end impairment assessments without issue, the more relevant question is no longer whether an impairment was required at a point in time, but whether the impairment framework itself reflects how capital is being deployed, monitored, and reallocated.

Viewed this way, accounting for impairment is less about avoiding write-downs and more about capital discipline. When designed thoughtfully, it becomes a forward-looking signal that clarifies which investments are performing as expected, which assumptions are weakening, and where optionality still exists. When treated as a compliance exercise, impairment tends to surface later as audit friction, investor confusion, or reactive adjustments at inopportune moments.

AI and Infrastructure Spend: When Capital Cycles Outpace Feedback Loops

Few areas illustrate this shift more clearly than AI and infrastructure investment.

Companies across industries are committing meaningful capital to data centers, high-density computers, specialized hardware, power and cooling infrastructure, and the software required to operate them. These investments are no longer limited to hyperscalers; many mid-cap and private companies now manage capital profiles that are far more infrastructure-intensive than in the past.

The economic half-life of many modern assets is shortening, even when accounting lives remain long, placing greater pressure on impairment judgements made by finance and accounting leaders.

Technology refresh cycles are accelerating, and demand assumptions tied to AI workloads or usage growth remain highly dynamic. In many cases, these assets generate value only as part of a broader ecosystem of hardware, facilities, software, and operating models working together.

A robust impairment framework forces management to confront questions central to capital allocation:

- How quickly will we know if utilization assumptions are breaking down?

- Which components of this investment are recoverable on their own versus only in combination?

- When does reinvestment preserve value, and when does it compound risk?

While impairment ultimately surfaces through accounting mechanics such as asset grouping, cash-flow modeling, useful-life assumptions, those mechanics are simply expressions of underlying strategic judgments. When impairment models rely on static groupings or assumptions that no longer reflect operating reality, the issue is rarely technical noncompliance. It is a signal to CFOs and accounting leaders that feedback loops between capital deployment and performance have weakened.

Companies that treat impairment as an ongoing discipline tend to surface issues earlier, preserving flexibility and decision-making clarity rather than reacting after the fact.

Internal-Use Software: When Strategic Optionality Quietly Erodes

Internal-use software has historically been one of the least controversial impairment areas. Once capitalized and placed into service, these assets were often assumed to deliver steady economic benefit over their accounting lives.

But for effective accounting and financial reporting professionals, that assumption no longer holds.

As companies modernize technology stacks, adopt AI capabilities, and pivot operating models, software investments increasingly resemble strategic options rather than long-duration assets. They deliver value only as long as the underlying business case remains intact. Systems may remain operational, development may continue, and amortization schedules may still appear reasonable even as the strategic rationale weakens.

In this context, impairment is not a failure but a signal that an option has expired.

A forward-looking impairment framework aligns technology strategy with financial reality by asking:

- Has the intended functionality changed?

- Are projected benefits still achievable?

- Is the system still core to value creation, or transitional?

When impairment is treated as a year-end accounting exercise, write-downs tend to arrive late and feel reactive. When embedded into capital discipline, impairment becomes a governance tool, helping CFOs manage innovation velocity without accumulating stranded capital.

Demand Volatility: Stress-Testing Forecast Credibility

The shift toward usage-based pricing, consumption-driven demand, and variable customer behavior has altered the reliability of long-term forecasts. Revenue no longer scales predictably, and capacity decisions are often made in advance of confirmed demand.

The strategic issue is not whether forecasts will be wrong; they will be. The question is whether management has designed a framework that recognizes uncertainty early and responds decisively.

This volatility places greater weight on judgment embedded in impairment models and cash-flow assumptions. Impairment plays a unique role here, acting as a structured stress test of the assumptions embedded in capital decisions:

- How resilient are projected cash flows under downside scenarios?

- When does underutilization become economically meaningful?

- Are investments sized for sustainable demand or peak optimism?

Organizations that integrate impairment thinking into ongoing planning tend to identify pressure points earlier, while choices still exist. In that sense, accounting for impairment becomes a mechanism for improving future forecasts, rather than a judgment on past forecasts.

Asset Grouping: Where Capital Discipline Meets Economic Reality

While often treated as a technical determination, asset grouping is fundamentally a statement of how management believes value is created and sustained. In practice, this is where impairment frameworks most often lag operating reality.

Common breakdowns include:

- Grouping legacy and next-generation assets despite diverging economics

- Evaluating infrastructure, software, and facilities in silos even though none generate cash flows independently

- Maintaining enterprise-level groupings after management has effectively segmented the business waly

The consequence is not merely accounting imprecision. Overly broad groupings can delay recognition of underperforming investments, while overly narrow groupings can obscure genuine interdependencies.

A well-designed impairment framework treats grouping as a living judgment, reassessed as strategies evolve and assets become more or less integrated. When finance and accounting leaders ensure that asset groupings align with how management actually evaluates performance and allocates capital, impairment becomes less about defending conclusions. The team can make better decisions with clearer visibility.

Audit Readiness as a Byproduct, Not the Objective

Impairment issues often surface during audit not because auditors uncover new problems, but because misalignments already exist between strategy and assumptions, operating reality and documentation, or capital decisions and impairment conclusions.

Organizations that treat impairment as a strategic discipline experience fewer audit surprises. Their assumptions are clearer, documentation more coherent, and narratives more consistent with how the business is run. In contrast, reactive impairment approaches tend to surface tensions late, when flexibility is limited.

Audit friction, in this sense, is a lagging indicator, not the root cause.

Preserving Strategic Optionality

The ultimate value of impairment discipline lies in what it enables:

- Clearer capital allocation decisions

- Greater investor and board confidence

- Reduced risk of value leakage in transactions or strategic shifts

Impairment done well enhances strategy and preserves optionality by surfacing economic realities early, while choices still exist.

Designing Forward

The companies that navigate impairment most effectively will look beyond year-end tests and integrate impairment into their operating infrastructure alongside planning, forecasting, and capital deployment.

In an environment defined by AI adoption, infrastructure intensity, and rapid change, impairment is no longer a retrospective accounting exercise. It is a discipline that helps CFOs see more clearly, decide more quickly, and allocate capital more confidently.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]