- with readers working within the Law Firm industries

- within Accounting and Audit, International Law and Law Department Performance topic(s)

AFRICAN UNION: African Continental Free Trade Area Agreement developments

The African Continental Free Trade Area Agreement ("ACFTA"), signed on 21 March 2018 by 44 countries and on 1 July 2018 by Burundi, Lesotho, Namibia, Sierra Leone and South Africa, will enter into force 30 days after the 22nd country has deposited its instrument of ratification.

The National Assembly of Mauritania approved the ACFTA on 19 December, the National Assembly of Togo on 6 December and the National Assembly of Namibia earlier the same month, while the cabinet of Senegal approved the agreement on 28 November 2018 and the National Assembly of the Ivory Coast on 31 October 2018.

Guinea deposited its instrument of ratification for the ACFTA on 16 October 2018 and Uganda on 28 November 2018.

BOTSWANA: Double tax agreement with Malta enters into force

The Botswana - Malta Income Tax Treaty (2017) entered into force on 13 November 2018 and generally applies in Botswana from 13 December 2018 for withholding taxes and 1 July 2019 for other taxes. In Malta, the treaty applies from 1 January 2019.

CAMEROON: 2019 Finance Law promulgated

The Finance Law 2019 was promulgated on 11 December 2018 and is effective from 1 January 2019 unless stated otherwise. Significant amendments include:

Corporate taxes

- the introduction of a 30% tax credit of the amount invested (capped at F.CFA100-million) in the renewal or reconstitution of machinery by taxpayers in economically affected areas;

- an exemption from withholding tax on the local purchase of petroleum products by distributors registered with the Large Taxpayers' Department (Direction des Grandes Entreprises);

- amendments to the requirements for benefiting from tax incentives pertaining to the rehabilitation of economic disaster areas to include utilising raw materials produced in the relevant area;

- extending the ambit of tourists' tax to furnished apartments and other bed-and-breakfast owners, which are required to withhold and remit F.CFA 2 000 per night spent in their establishments;

- extending the scope of the special tax on income. The super-reduced rate of 2% will be applicable to payments made by resident companies to foreign companies for vessel rentals and charter, space rentals in foreign vessels and commissions to foreign port agents;

- an increase in the rate of forestry felling taxes from 2.5% to 4%;

Individual taxation

- fixing the income tax on commissions paid to sales agents, including those of the insurance sector, at 10% to be withheld at source by the payer, after deducting business expenses of 30%;

- an exemption from withholding tax on the local purchase of petroleum products by distributors registered with the Large Taxpayers' Department (Direction des Grandes Entreprises);

- introducing a flat rate capital gains withholding tax rate of 5% on "property" as defined;

- clarifying that employers in the specialised management unit industry managing multiple branches must pay income tax withheld from salaries of their employees only in their respective tax offices;

Value-added tax ("VAT")

- clarifying that funding agreements, including foreign and joint grants for the funding of public contracts signed as from 1 January 2019 must be concluded VAT inclusive as VAT on such contracts will no longer be borne by the government of Cameroon. However, VAT on pending contracts will continue to be borne in accordance with applicable laws upon their signature;

- introducing being subject to the payment of registration fees as a prerequisite for the exemption from VAT available to real estate operations carried on by non-professionals and transfers of real estate and goodwill (fond de commerce);

- repealing the exemption from VAT applicable to, inter alia, life and sickness insurance;

- increasing the threshold for VAT exemption on water and electricity utility services for low-income earners to 20 m3/month for water and 120 kW/month for electricity;

- allowing general traders to carry forward VAT credits, irrespective of the amount, upon validation by the tax administration. VAT credits accrued to industrialists and petroleum distribution and leasing companies are reimbursable after three months, provided that such persons waive their right to carry forward the said credit;

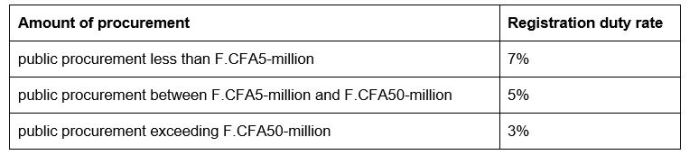

Registration duty

repealing the reduced registration duty of 2% on public

procurements of less than F.CFA5-million paid by the state, local

councils and public companies and replacing it with the following

rates applicable depending on the amount of procurement:

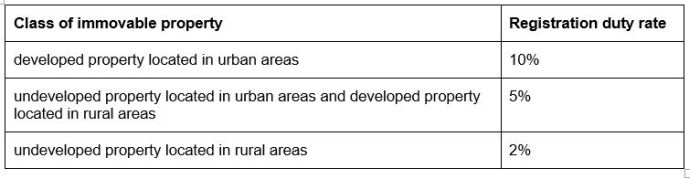

- amending the registration duty rates on the transfer of immovable property to the following:

Tax procedures and administration

- introducing the requirement that taxpayers of the specialised units (Medium Size, Large Taxpayers' Offices and Tax Offices for Liberal Professions) must file their annual returns electronically;

- clarifying that the tax administration may only send pre-filled returns to taxpayers if they have not yet filed returns for the relevant taxes;

- specifying that charges payable to banks and other financial institutions wiring taxes on behalf of taxpayers, as well as issuing proof thereof, must be between F.CFA500 and F.CFA10 000 and under no circumstances may such charges exceed 10% of the taxes wired;

- allowing tax correspondence to be sent to taxpayers via email following certain modalities yet to be determined by law;

- requiring taxpayers who keep computerised accounts to hand over soft copies of required information at the commencement of tax audits;

- allowing taxpayers undergoing desk audits, partial audits or spot checks a response time of 30 calendar days (previously 30 working days) upon receipt of a notification of tax adjustments;

- requiring all entities (public or private) engaged to carry out periodic tax reviews and audits of the accounts of public and private entities to forward the results of the audits to the tax administration;

- extending the deadline for payment of taxes already contained in the Tax Collection Notice (Avis de Mise en Recouvrement) from 15 to 30 days;

- extending the limitation period to request VAT refunds from two to three years;

- requiring a valid tax clearance certificate as condition for the transfer of funds out of the country; and

- providing an online facility for requesting stay of payment of outstanding tax pending determination of a tax dispute.

DEMOCRATIC REPUBLIC OF CONGO (DRC): New social security contribution rates introduced

In terms of Decree no. 18/041 of 24 November 2018 promulgated on the said date, the new social security contribution rates to be paid to the National Social Security Fund (Caisse nationale de sécurité sociale), with effect from 1 January 2019 are as follows:

- 6.5% for family contributions;

- 10% (to be divided equally between the employer and the employee) for retirement contributions; and

- 1.5% for professional risks contributions (unchanged and to be borne by the employer).

DRC: Draft Finance Law 2019 promulgated

The 2019 Draft Finance Law 2019 was adopted by the National Assembly and Senate on 5 November 2018 and 16 November 2018 respectively, and promulgated by the President on 13 December 2019. Unless otherwise stated, it applies with effect from 1 January 2019. Significant amendments include:

Corporate taxes

- reducing the corporate income tax rate from 35% to 30%;

- allowing a deduction of the minimum corporate income tax paid in loss-making years from taxable profits of subsequent tax years;

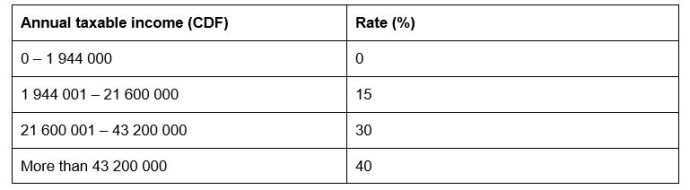

- introducing new employment income tax rates as follows:

Value-added tax

- exempting the importation and purchases of equipment and chemical products used for mining or petroleum production from VAT;

- considering exporting mining and petroleum companies and companies having made heavy investments during their establishment phase subject to VAT for the purchase of their goods and services;

- disallowing VAT charged by a person required to use the VAT electronic system per invoice issued outside that system as an input;

- introducing provisions relating to the VAT electronic system with effect from 1 January 2020;

Tax administration

- requiring transfer pricing documentation to be submitted by no later than two months after the corporate tax return filing deadline; and

- amending the assessment penalties applicable to the principal amount of tax (pénalités d'assiette).

DRC: Strategic mineral products decree published

On 24 November 2018, the prime minister promulgated Decree No. 18/042 establishing a list of strategic mineral products subject to a 10% royalty rate in terms of Law No. 18/001 of 9 March 2018, amending the Mining Code.

The strategic mineral products listed under the decree are germanium, colombo-tantalite and cobalt.

GHANA: Excise Tax Stamp (Amendment) Act 2018 passed

Parliament passed the Excise Tax Stamp (Amendment) Act 2018 (Act 981) and the president assented to the Act 981 on 28 December 2018.

Act 981 amends the Excise Stamp Act 2013 (Act 873) to include textiles in the list of goods on which an excise stamp must be affixed (section 2 of Act 873).

GHANA: Income Tax (Amendment) (No. 2) Act 2018 enters into force

On 28 December 2018, parliament passed Income Tax (Amendment) (No. 2) Act 2018 into law and was assented by the president on the same day. Significant amendments, which, unless otherwise stated, become effective from 1 January 2019, including:

- confirming the withholding tax rate for the supply of services by non-residents to be 20%;

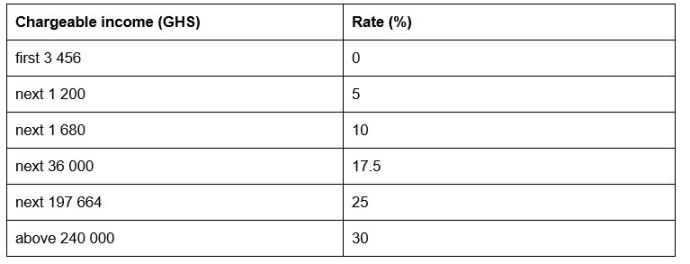

- amendments to the income tax bands

applicable to resident individuals as follows:

The 2019 Budget presented to parliament by the Minister of Finance

on 15 November 2018, include, inter alia, the following

proposed tax measures:

- VAT zero rate on the supply of locally made textiles for a period of three years;

- broadening the tax base through thorough enforcement of the requirements for a tax identification number; and

- putting together property data to enhance the collection of property tax.

GHANA: Protocol to treaty between Ghana and Switzerland enters into force

The amending protocol to the Ghana - Switzerland Income and Capital Tax Treaty (2008), signed on 22 May 2014, entered into force on 29 October 2018 and generally applies from 1 January 2019.

KENYA: Draft Housing Fund Regulations 2018 issued for public comment

In order to facilitate the task of the State Department for Housing and Urban Development under the Ministry of Transport, Infrastructure, Housing and Urban Development to deliver at least 500 000 affordable homes, it has published draft Housing Fund Regulations 2018 (the Regulations) for public comment.

The draft Regulations intend to provide clarity on the operation of the contribution to the National Housing Development Fund introduced by the Finance Act 2018 and which is charged at the rate of 1.5% of the employee's earnings.

MAURITANIA: Finance Law for 2019 approved by parliament

The draft Finance Law for 2019 was approved by parliament in 28 December 2018 and generally applies as from 1 January 2019.

MAURITIUS: "Place of effective management" concept clarified

The Mauritius Revenue Authority published a statement of practice clarifying the concept of "place of effective management" used for corporate tax purposes on 28 November 2018.

As per the statement, all relevant facts and circumstances must be examined when determining the "place of effective management", including elements relating to the business activities of the company and the use of information and communication technologies in the decision-making process. In general, a company will be deemed to have its place of effective management in Mauritius, and therefore be tax resident in Mauritius if:

- the strategic decisions relating to the company's core income generating activities are taken in, or from, Mauritius; and

- the majority of the board of directors' meetings are held in Mauritius or the executive management of the company is regularly exercised in Mauritius.

MOZAMBIQUE: Tax amnesty announced

The President of the Mozambique Tax Authorities ("MTA") announced a tax amnesty program at a press conference on 4 January 2019. In terms of the program the MTA will forgive fines, interest and tax foreclosures for companies under the Tax Enforcement (Execuções Fiscais) process, provided that the companies settle the net amount of outstanding tax in 2019. Further details on the programme are awaited.

MOZAMBIQUE: Potential reduction in VAT rate announced

At the same press conference, the President of the MTA announced that the VAT rate may be reduced from 17% to 15% in 2019. The MTA is currently working on the proposed amendments to the VAT Code, which may include, in addition to the rate reduction, significant changes to zero-rated exemptions.

ZAMBIA: Amendment Acts gazetted

On 26 December 2018, the Income Tax (Amendment) Act 2018, the Mines and Minerals Development (Amendment) Act 2018 and the Customs and Excise (Amendment) Act 2018 were gazetted, implementing measures proposed in the 2019 Budget with effect from 1 January 2019. However:

- although the 2019 Budget proposed to replace VAT by sales tax with effect from 1 April 2019, there has been no development on the proposal, as the relevant Bill has not yet been presented to the parliament; and

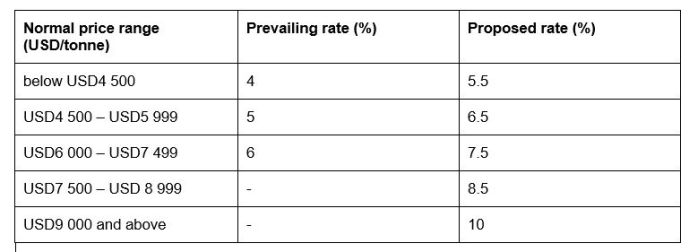

- the copper mineral royalty tax have

been revised as follows:

ZIMBABWE: 2019 Budget presented to parliament

The Minister of Finance and Economic Development presented the 2019 Budget to parliament on 22 November 2018. Significant proposals include, inter alia:

Corporate taxes

- taxing income accruing to foreign domiciled broadcasting and satellite services and foreign based persons who sell goods and services through electronic commerce platforms with defined minimum prescribed amounts and requiring such persons to be registered with the Zimbabwe Revenue Authority, appoint agents to act for them and have a tax clearance certificate to facilitate the remittance of funds;

- allowing expenditure from separate mining locations held by the same taxpayer and forming part of an integrated process of beneficiation under the control of the taxpayer;

- holding liable directors who liquidate or dissolve a company with a tax liability to avoid payment of tax but subsequently form a new company to pursue the same business for the tax of the old company;

- scrapping the 10% withholding tax on tenders for persons whose income is subject to non-residents tax on fees, remittances or royalties;

- exempting the Reserve Bank of Zimbabwe from withholding the 10% tax on interest from Treasury Bills where tax clearance certificates were not furnished;

- exempting financial institutions' income from treasury bills specifically stated as tax free;

- formalising into law Statutory Instrument SI 205 of 13 October 2018, which brought into effect the 2% intermediated money transfer tax;

- requiring taxpayers to disclose

details of transactions with related parties on the self-assessment

return and subjecting them to the following potential penalties:

- 100% of the shortfall when there is evidence a scheme was designed to avoid payment of tax;

- 30% of the shortfall where there are no or inadequate transfer pricing documents supportive of arm`s length pricing;

- 10%, where the related party transactions do not meet the arm's length principle;

Personal taxation

- increasing the employee tax free threshold is by USD600 to USD4 200 per annum;

- reducing the tax rate on annual amounts exceeding USD240 000 from 50% to 45%;

Value-added tax

- allowing the payment of outstanding VAT in the order of principal, penalty and interest;

- amending the definition of "supply" to include the supply of imported services; and

- deeming a supply to take place on the

earlier of:

- the time an invoice is raised by the supplier or the recipient in respect of that supply; or

- the time any payment of consideration is received by the supplier in respect of that supply; or

- the time of removal from the place of sale of movable goods; or

- the time the recipient takes possession of immovable goods; or

- the time a service is performed.

Sources include IBFD's Tax Research Platform;

www.allafrica.com; http://tax-news.com

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]