- within Criminal Law, Tax and Employment and HR topic(s)

- with readers working within the Aerospace & Defence and Banking & Credit industries

One year from the signature of the Multilateral Convention, the deadline of the first exchange of information based on the OECD agreements is approaching. In September 2018, Lebanon has started to operate the Automatic Exchange of Information (AEOI) since the signature of the Convention in 2016.

It is not clear yet how the correct implementation of the Common Reporting Standards (CRS) procedures will effectively impact on the banking secrecy still in force in the country and one of the pillar of the financial sector.

I. A brief recap

In May 2016, Lebanon formally adhered to the Global Forum on Transparency and Exchange of Information for Tax Purposes, committing to implementing a series of reforms that would lead to the integration of domestic legislation with OECD standards in the tax area.

The standards impose the obligation, on the part of the financial administrations of the acceding States, to exchange reciprocally and automatically the data related to the financial accounts held by non-residents and collected by financial institutions (banks, mutual funds, insurance companies, trusts, foundations, etc.) located in their territory.

Also known as CRS, the international rules provide for the introduction of common rules on reporting, analysis of accounts (due diligence) and exchange of information, to allow a smoother communication between all the member countries. The failure to apply the CRS may be the violation of laws for local actors (banks, companies and individuals), and the potential inclusion in the blacklists for Lebanon, with the consequence of no longer being considered a key player in the international economic community.

According to the agreements, starting from next September, Lebanon will automatically exchange information on non-residents (tax), and will have access to information on residents, who hold assets abroad.

II. Current situation according to the OECD report

Adhesion and commitment did not, however, amount to preparation. At the time, the country did not have an adequate organization in terms of classification of information nor a regulatory and administrative framework to promptly introduce what is required by the OECD.

Looking at the reports published on the OECD's website, the latest updated on March 22, 2018, it is possible to have a specific overview of the steps taken and choices made by Lebanon in the context of implementing the Standard.

Since 2016, the Lebanese Government has approved (a) primary and secondary legislation and (b) used a wider approach to the CRS.

a. More specifically, Law n. 55 of 27 October 2016 is the main act of primary legislation. It provides the procedures for the implementation of the Convention on Mutual Administrative Assistance in Tax Matters and the Multilateral Competent Authority Agreement (the "MCAA"), and identifies the authorities responsible for the exchange of information both on request and automatically.

In addition, other legislative acts were approved to flank the current fiscal discipline:

- Pursuant to Law No. 44/2015, tax evasion is currently considered a predicate offense for the configuration of money laundering and terrorist financing crimes;

- Law No. 75/2016 effectively deletes bearer shares from Lebanese company law;

- Law No. 74/2016 imposes tax obligations on subjects carrying out activities as a trustee;

- Finally, Law No. 60/2016 introduces into the legal system the definition of "residence" for both corporations and individuals, a concept that has not yet found space in the codes and which is mandatory under the CRS.

These acts were issued shortly after the issue of the additional report of the Global Forum on Lebanon and demonstrate the strong will of the country to comply with the OECD criteria.

With regard to the secondary legislation, the Ministry of Finance issued the Decree No. 1022 of 7 July 2017, pursuant to art. 6 of law no 55 of 27 October 2016 – to implement the obligations of Lebanon under the terms of the MCAA. Few days later, the Lebanese Central Bank (Banque du Liban1) published Basic Decision No. 12625 of 21 July 2017 relating to the Common Reporting Standard.

The Lebanese Tax Authority will exchange the information to its counterparts of the reportable jurisdictions on or before 30 September of the year following the calendar year to which the return relates.

For the purposes of the AEOI, the following are currently2 the reportable jurisdictions: Argentina, Australia, Bahamas, Belgium, Brazil, Bulgaria, Canada, Cayman Islands, Chile, China, Colombia, Costa Rica, Curaçao, Czech Republic, Estonia, Faroe Islands, Finland, France, Gibraltar, Greece, Greenland, Grenada, Guernsey, Hong Kong (China), Iceland, India, Indonesia, Ireland, Isle of Man, Italy, Japan, Jersey, Korea, Kuwait, Latvia, Malaysia.

b. As we understood from the Decree and the Decision in 2017, Lebanon decided to adopt a wider approach to review their procedures for existing and new clients of financial institutions (FIs). In other words, FIs capture and maintain information on the tax residence of account holders regardless of whether or not that account holder is a reportable person.

The rationale behind the approach is to set common best practices once for all, to avoid additional review and changes each time a new country is added to the list of reportable jurisdictions.

Furthermore, for the purposes of the CRS, Lebanese authorities have not excluded any account from the collection and due diligence, nor listed any "non-reporting financial institution" that will be exempted from the procedures.

III. The Lebanese challenge

In the report issued by OECD in November 20173, the monitoring results in relation to the early adopters4 essentially show the full delivery of each aspect of the commitments made, including collecting the data domestically and ensuring its widespread exchange internationally.

OECD acknowledged in the same report that Lebanon, after a slow beginning, was on track with the domestic laws in place and the collection of data by the FIs, which started in July 2017 after the secondary legislation entered into force.

Although Lebanese FIs are requiring all information about tax residence and assets detained abroad before providing any services, there is another matter that the country needs to address, especially in the view of the above-mentioned wider approach: the banking secrecy.

In fact, the OECD model abolishes banking, financial and fiduciary secrecy when a state financial administration asks another administration of a Contracting State for financial information about a taxpayer resident. Nonetheless, decades of banking secrecy cannot be buried without warning and protection for the beneficiaries.

The banking secrecy law has had an important role at raising the confidence in the local banking sector and boosting the flow of foreign capitals. The current challenge of Lebanon is therefore to balance the banking secrecy, established in 1956 and still in force, with the introduction of the laws that comply with international standards.

To allow effective compliance with the law n. 55 in conjunction with the law of 1956, the recent provisions specify that if the information to disclose is protected by the banking secrecy, the request shall be forwarded to the SIC (Special Investigation Commission) with a review opinion by the Ministry of Finance, before it can be released to the foreign tax administration on the basis of a AEOI agreement.

The SIC is a body established within the Central Bank of Lebanon with law n. 318 of 20 April 2001 - following the first report of the FATF (Financial Action Task Force) of June 2000 - to protect banking secrecy and to defend the identity and sensitive data of customers.

According to the Decision No. 12625/2017, the SIC could be also involved in the control and review of books and records of FIs, for the purpose of controlling the proper implementation of the laws, and in the imposition of administrative sanctions and financial penalties pursuant to the anti-money laundering and terrorism financing legislation.

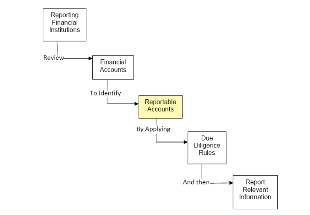

The following figure5 describes the steps to be followed by FIs when reporting information to the Tax Authority, according to the CRS that Lebanon applies. It would be ideal to know when the banking secrecy can be invoked along the process, and in which cases it can be lifted other than money laundering, tax evasion and other forms of criminal activity.

According to the Law of 1956, information concerning names of clients, their funds and related matters may be revealed in cases of:

- Written permission by the concerned client or heirs;

- Declaration of bankruptcy;

- Legal action between a bank and its client.

- Exchange of information about indebted accounts between banks for reason of securing their investments;

- Actions of illegal enrichment upon the request of the judicial authorities.

Moreover, the law imposes sanctions for the violation of the banking secrecy.

In light of the above, in the future it should be clarified what legislation prevails between the new AEOI laws and the banking secrecy provision, and when the sanctions are applied.

IV. A first exception to the banking secrecy...in practice

While the banking secrecy remains a solid pillar of Lebanon, we have witnessed to an exception created by the practice, after the Foreign Account Tax Compliance Act (FATCA) was approved by the US in 2010.

The FATCA has the aim of tracking the accounts of all US citizens worldwide, regardless of their residence in the American territory, to prevent tax evasion. This particular law forces all the banks and foreign financial institutions (FIs) to identify their clients (Know you client obligation) considered as "US persons" according to the requirements of the said law and to transfer automatically all the information related to the accounts detained by them in case the balance of the account exceeds certain limits reflecting the customer's profile (250,000 $ for legal entities; 50,000$ for natural persons).

The adoption of the FATCA falls into the legal framework of the intergovernmental agreements aim for making mandatory the automatic exchange of banking and fiscal information between States. When an inter-governmental agreement is not in place, the FATCA is implemented between the US Internal Revenue Service (IRS) and the financial institutions.

In Lebanon it has not been implemented through a law, but directly by banks and financial institutions. Accordingly, it does not lift the banking secrecy from US persons' accounts, but each bank requires US persons to waive their rights to banking secrecy, subject to closing their bank accounts or rejecting their application to open a new one.

In conclusion

Both FATCA and AEOI are automatic exchanges of information's mechanisms with the same purpose, which is the optimization of tax collection by the competent authorities, although only the second is based on a general principle of reciprocity. The main purpose behind these laws is to increase the international transparency in tax matters and to reduce tax evasion.

Following a different rationale, the current exception to the banking secrecy, generated by the law, is the AEOI legislation currently in force. Even if no act has been approved by the Government yet to refine the secrecy according to the international principles, the new laws waive the banking secrecy law for what concerns non-resident accounts.

The AEOI has a broader scope of application6 and any reportable person identified within the due diligence undertaken since 2017 has become reportable to the relevant tax authority in 2018.

Therefore, in case of activities carried out in multiple countries, individuals and companies need to be aware of their status, the structure of their business, financial situation, and the double tax treaties in force, in order to avoid possible sanctions or double payments.

Footnotes

1. Banque du Liban is the sole regulatory body in charge of the sound implementation of the Law, the Decree, and the Decision.

2. Update as at June 2018.

3. https://www.oecd.org/tax/transparency/reporting-on-the-implementation-of-the-AEOI-standard.pdf

4. The countries starting the implementation of CRS and data collection since 2015.

5. OECD (2018), Standard for Automatic Exchange of Financial Information in Tax Matters - Implementation Handbook - Second Edition, OECD, Paris. http://www.oecd.org/tax/exchange-of-tax-information/implementation-handbook-standard-for-automatic-exchange-of-financial-account-information-in-tax-matters.htm, p. 57

6. With this new CRS standards based on residence factor, it has become necessary for Lebanon to define what a fiscal resident is. The article 1 of N0 60 law that entered into force on the 27 October 2016, determined the fiscal resident as follows: i) in case of legal persons, the one which is registered and incorporated under Lebanese laws the one that has a place of business in Lebanon; ii) in the case of natural persons, the one that has in Lebanon a place of business or permanent place of residence or satisfies the presence rule ( present 183 days in Lebanon during a consecutive period of 12 months).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.