- within Wealth Management topic(s)

- in North America

- within Wealth Management topic(s)

- in North America

- in North America

- in North America

- with readers working within the Media & Information, Metals & Mining and Retail & Leisure industries

- within Wealth Management, Corporate/Commercial Law, Media, Telecoms, IT and Entertainment topic(s)

- with Senior Company Executives and HR

In today's interconnected world, managing wealth across borders has become increasingly complex. Yet, many individuals with substantial offshore assets leave critical aspects of their wealth unstructured or, worse, risk it falling into uncertain hands by passing away intestate. According to wealth management sources, a substantial percentage of ultra-high-net-worth individuals worldwide face complex estate challenges. Approximately 30-40% of wealthy individuals either lack a structured estate plan or die intestate, leading to family disputes and substantial legal fees. This lack of planning can lead to prolonged legal battles, unforeseen tax consequences, and unintended beneficiaries gaining control over hard-earned wealth. Mauritius, with its robust trust laws and favorable tax environment, presents an appealing solution for individuals seeking a secure and flexible framework to safeguard their assets.

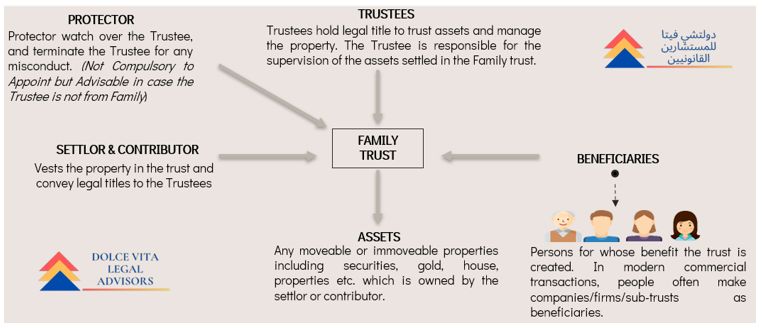

Understanding the Mechanics of Private Trusts

A Trust is a legal arrangement where a settlor transfers assets to a trustee to manage for the benefit of beneficiaries. The trustee holds and manages the Trust assets, while the beneficiaries receive the income or assets generated by the Trust. A Trust protector may be appointed to oversee the trustee and ensure they are acting in the best interests of the beneficiaries. Trusts can be used for various purposes, such as wealth preservation, estate planning, and asset protection. The typical trust structure is given below:

Several jurisdictions globally can be used for the administration and running of Trusts, but an important aspect is the tax treatment which applies in the jurisdiction chosen for the Trust. As a rule, Offshore Trusts are set up in jurisdictions such as the British Virgin Islands, the Cayman Islands, Mauritius, and the Channel Islands – Jersey, Guernsey. Depending on the jurisdiction chosen, the Trust is governed by the legislation of the place where it is registered.

For example, consider a high-net-worth individual seeking to shield assets from high inheritance taxes or to protect wealth from creditors—offshore trusts can be instrumental here. A trust structured in jurisdictions like the Cayman Islands or Mauritius often benefits from flexible tax policies and strong asset protection laws, helping avoid local inheritance taxes or forced heirship rules that may not align with the settlor's intentions.

Why Mauritius is an Ideal Jurisdiction for Trusts?

Mauritius stands out as a jurisdiction with a contemporary "Trust Law", renowned for its political and economic stability. Its democratic system, modelled after the British parliamentary system, ensures a clear separation of powers. Additionally, Mauritius boasts a highly-skilled, multilingual workforce with a literacy rate exceeding 90% (ninety percent).

The country offers a cost-effective operating environment and a range of attractive fiscal incentives, including exemption from taxes on dividends, interest, royalties, and estate duties. Foreign-sourced income also benefits from favourable tax treatment.

Recent reforms have significantly enhanced Mauritius' business and investment climate, making it a prime destination for entrepreneurship. The government has streamlined processes, by reducing the time required to start a new business to just three days and implementing measures to attract investors and professionals.

Key Advantages of Establishing a Trust in Mauritius

Mauritius Trust offers a compelling combination of legal protection, tax advantages, and privacy, making it an ideal jurisdiction for establishing Trusts:

- Tax Efficiency: Benefits from a favorable tax environment with various exemptions and incentives for significant wealth accumulation.

- Asset Protection: Robust legal framework safeguards trust assets from personal liabilities, creditors, and legal challenges.

- Succession Planning: Offers control over asset distribution post-death, allowing flexibility and reducing potential disputes among beneficiaries.

- Confidentiality: No mandatory registration requirements enhance privacy for settlers and beneficiaries, ideal for discreet wealth management.

- Flexibility: Versatile legal framework allows for the creation of various trust types (discretionary, fixed interest, purpose, and charitable) tailored to evolving needs.

Legal Framework Governing Trusts in Mauritius

The governing legislation for trusts in Mauritius is the Trusts Act, 2001 ("Act"). This Act regulates the creation and administration of trusts and outlines the responsibilities of trustees. A trust in Mauritius must be manifested via a written document, ensuring transparency and clarity in the Trust's operation. The Act does not require Mauritius Trusts to be registered, which offers privacy to the settlors and beneficiaries. It also provides for the appointment of a 'Protector,' who has fiduciary responsibilities towards the beneficiaries.

To be valid, a trust must be established through a written instrument that encompasses the following essential elements: the name of the trustee, a clear expression of the settlor's intent to create a trust, the specific purpose or objective of the trust, the names of the beneficiaries or a defined class of beneficiaries (unless the trust permits discretionary beneficiaries), the assets transferred to or held in trust, and the duration or timeframe of the trust. A trust is deemed fully constituted only when all property settled within the Mauritius trust is vested entirely in the trustee. Notably, the duration of a Mauritian trust is capped at a maximum of 99 years.

Qualification of parties: In the context of a Mauritius Trust, the settlor must be an individual of sound mind and possess the legal capacity to contract. Any person can serve as a settlor; however, they may also act as a beneficiary, protector, or enforcer of the trust, provided they are not the sole beneficiary of the trust they establish. Furthermore, when a non-citizen transfers or disposes of assets into a trust, such actions cannot be challenged, invalidated, or deemed void due to any violation of local laws related to inheritance or succession in the settlor's domicile or nationality.

Beneficiaries of the trust must be expressly identified by name or be ascertainable through reference to a defined class or their relationship to another individual. It is essential that a trust maintains, at all times, at least one qualified trustee, which must be a management company licensed by the Financial Services Commission.

Functions of a protector: The terms of the trust may provide for the office of protector of a trust whose function shall be to advise the trustee. The protector may also be a settlor or beneficiary of the trust. Subject to the terms of the trust, the protector may exercise the following specific powers:

- Remove a trustee and appoint a new or additional trustee

- Determine which jurisdiction's law shall be the proper law of the trust

- Change the forum of administration of the trust

- Withhold consent of specific actions of the trustee either conditionally or unconditionally.

Trustee Appointment & Responsibilities: The trust may provide for the appointment of a Trustee, who can be either an individual of full age with the legal capacity to contract or a corporate entity authorized under its statute to act as a Trustee. The trust instrument may designate a Custodian Trustee or a Managing Trustee, but the total number of Trustees must not exceed four. At least one Trustee must be a qualified Trustee, defined as a management company licensed by the Financial Services Commission.

The Trustee has a duty to disclose details regarding the trust property and the administration of the trust to the Settlor, the Enforcer, or the Protector, unless there is reasonable cause to believe that such a request is made under duress. The Trustee may only disclose confidential information to a court or a judge in chambers when ordered to do so. This disclosure may occur upon application by the Director of Public Prosecutions, provided that there is proof beyond a reasonable doubt that the confidential information is genuinely required for the purposes of an inquiry or trial involving:

- Drug trafficking

- Economic crime and money laundering

- Any acts deemed offenses related to trafficking, economic crime, or money laundering in Mauritius or elsewhere.

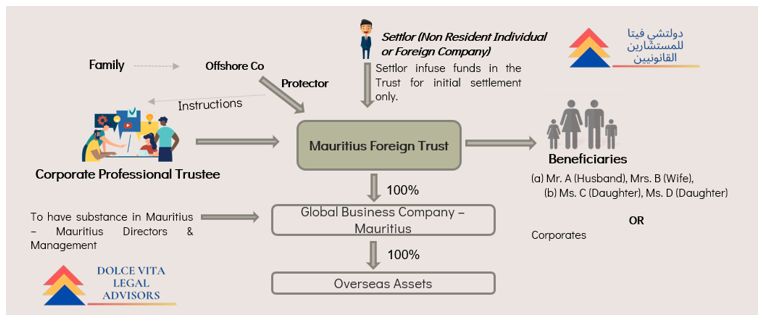

The following outlines the typical structure of a Mauritius trust:

Understanding the Tax Landscape for Trusts in Mauritius

In Mauritius, trusts and foundations are treated as companies for tax purposes through a legal fiction, which differs from the treatment in many other jurisdictions. They are subject to a chargeable income tax rate of 15 percent.

Before 1 July 2021, a trust could file a declaration of non-residence with the Mauritius Revenue Authority (MRA) within three months after the end of the income year, provided that: (i) the settlor was a non-resident or held a 'global business licence' under the 2007 Financial Services Act (FSA); (ii) all beneficiaries appointed under the trust were non-residents or held a global business licence under the FSA for the entire income year; and (iii) it was a purpose trust under the Trusts Act, with its purpose executed outside Mauritius. If these conditions were met, the trust would be exempt from income tax for that year.

However, following the amendments introduced by the Finance Act 2021, trusts and foundations can no longer submit a declaration of non-residence. Instead, they will be classified as non-resident if they are centrally managed and controlled outside of Mauritius, in accordance with Section 73A of the Income Tax Act, 1995 ("ITA").

Controlled outside of Mauritius: According to subsection (1) of Section 73A of the ITA, a company, which includes a trust, incorporated in Mauritius will be considered non-resident if its central management and control occur outside the country. This condition is pivotal in determining the tax residency status of the entity, regardless of its place of incorporation, ensuring that substantive decision-making authority is exercised beyond the borders of Mauritius.

The Statement of Practice (SP 24/21) issued by the Mauritius Revenue Authority (MRA) offers guidance on defining "central management and control" for trusts under Section 73A. Issued on August 24, 2021, this statement outlines the criteria for determining whether a trust is considered centrally managed and controlled in Mauritius.

A trust will be deemed to have its central management and control in Mauritius if:

- The trust is administered in Mauritius, with a majority of the trustees being residents of Mauritius; and

- The settlor of the trust is a resident of Mauritius at the time the trust instrument is executed or when new property is added to the trust; and

- The majority of the beneficiaries, or the class of beneficiaries specified in the trust, are residents of Mauritius.

These criteria establish a framework for assessing the tax residency of trusts and emphasize the importance of management location and beneficiary residency in determining tax obligations in Mauritius.

Once a trust or foundation qualifies as a resident entity, it becomes liable for tax on its worldwide income at a rate of 15%. However, it may be eligible for an 80% partial exemption on specific types of income, such as foreign dividend income and interest income, provided it meets the substance requirements outlined in the Income Tax Act (ITA). Notably, there is no capital gains tax in Mauritius, so any capital gains realized by a trust or foundation will not incur taxation. Furthermore, foundations or trusts that exist solely for charitable purposes are exempt from taxation in Mauritius.

Distributions made by a trust or foundation to its beneficiaries are classified as dividends. In Mauritius, these dividends are not subject to withholding tax. Resident individual beneficiaries can receive dividends exempt from tax up to MUR 3 million, with any amount exceeding this threshold liable for solidarity tax at a rate of 25%, capped at 10% of leviable income. Non-resident beneficiaries may be taxed on such distributions according to the tax regulations in their country of residence.

For non-resident trusts and foundations, income tax is applied at a rate of 15% only on income sourced from Mauritius.

In summary, resident trusts and foundations are taxed on their worldwide income, whereas non-resident trusts and foundations are taxed solely on Mauritian-sourced income.

Tax Implications of Mauritius GBC Company

Global Business Companies (GBCs) in Mauritius enjoy significant tax advantages, including a 15% tax rate on certain types of income, along with exemptions from capital gains and withholding taxes. An 80% exemption regime is available for specific income streams, contingent on meeting certain substance requirements. The eligible categories for exemption include:

- Foreign Dividends: Exempt unless tax is withheld in the source country.

- Interest Income.

- Profits from a Permanent Establishment (PE) in a foreign jurisdiction.

- Foreign-Source Income earned by Collective Investment Schemes (CIS), funds, or asset managers licensed by the Financial Services Commission (FSC).

- Income from Ship and Aircraft Leasing.

- Interest from Peer-to-Peer Lending, subject to a five-year tax holiday.

- Income from Leasing International Fibre Capacity.

- Income from Reinsurance and Brokering.

- Aircraft-Related Income, which encompasses sales, financing, asset management, and advisory services.

With these exemptions in place, the effective tax rate for GBCs can be reduced to approximately 3%.

Leveraging Mauritius for Effective Trust Structures: Conclusion

In conclusion, Mauritius emerges as a premier jurisdiction for establishing offshore trusts, offering a unique blend of legal protection, tax efficiency, and confidentiality. Its modern trust laws and favorable regulatory environment empower high-net-worth individuals and families to effectively manage their wealth while safeguarding their assets from potential liabilities. With the absence of capital gains tax and the opportunity for significant tax exemptions, Mauritius presents an attractive option for optimizing financial strategies.

However, while there are substantial benefits, it is crucial to acknowledge the associated risks. Navigating the complexities of international tax laws and compliance requirements can be challenging. Regulatory changes, both in Mauritius and the settlor's home country, may impact the efficacy and benefits of the trust structure. Additionally, potential challenges regarding asset protection could arise, especially if the trust is perceived as a vehicle for tax avoidance or if local laws change unexpectedly.

Despite these risks, the flexibility of trust structures in Mauritius allows for tailored solutions that can adapt to the evolving needs of settlers and beneficiaries. Whether implementing robust succession planning or seeking asset protection against unforeseen circumstances, Mauritius provides essential tools for achieving these goals. By carefully weighing the advantages and risks associated with establishing an offshore trust, individuals and entities can effectively navigate the complexities of wealth management.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.