- within Wealth Management, Corporate/Commercial Law, Media, Telecoms, IT and Entertainment topic(s)

- in United States

- with readers working within the Basic Industries industries

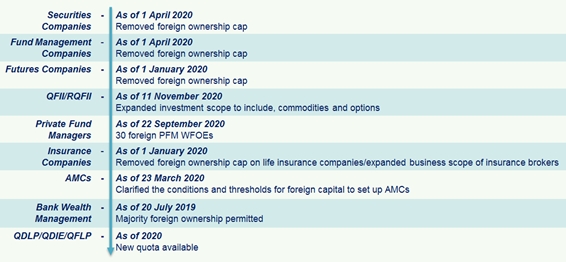

The past several years have witnessed a new round of opening-up of China's financial sectors. Since 2019 especially, with various limits on foreign investments removed, market evolvements have been speeding up which could appear bewildering to many foreign financial institutions. The table below illustrates major regulatory relaxations in the past around three years.

Due to such rapid regulatory developments, in the asset management sector particularly, offshore asset managers now have multiple new or enhanced avenues to access China's huge asset management market. Such avenues are subject to a large number of regulations issued by various authorities, the promulgation and amendments of which have been frequent in recent years.

Based on extensive experience in advising foreign financial institutions on applying for PRC licenses, Fangda Partner's Investment Management Group has summarized below certain key factors we believe must be considered when determining how to access China's asset management market. Such factors may help to lay ground for a comprehensive and thorough assessment of approaches to exploit asset management opportunities in China.

- Onshore/Offshore Products/Investments

Broadly speaking, exploiting opportunities in China's asset management market does not necessarily require launching onshore products and raising fund from onshore investors. Rather, offshore asset managers may, without setting up onshore entities/products, invest in China via cross-border investment avenues such as the Qualified Foreign Institutional Investor ("QFII") scheme, Stock Connect and Bond Connect. For QFIIs particularly, in the past around two years, the investment scope of QFIIs has been substantially expanded and also obtaining a QFII license has become less burdensome.

Even raising fund from onshore investors can be achieved without an onshore entity/product. For example, under the Mutual Fund Recognition scheme, mutual fund managers in Hong Kong can raise fund from PRC mainland investors.

Still, establishing onshore entities/products are desired by many offshore asset managers, which enables them to enjoy equal treatments as onshore managers in aspects of fundraising and investment scope.

To clarify, an onshore entity does not necessarily invest in onshore markets. Among others, the Qualified Domestic Limited Partners ("QDLP") license allows foreign asset managers to raise fund in China to invest in offshore markets.

- Available Investors/Investment Vehicles

Similar to many foreign jurisdictions, investors in China can largely be categorized to professional (institutional) investors and non-professional (retail) investors. Most types of asset management products are allowed to be distributed to professional investors only, and the criteria of professional investors may vary depending on the specific product. Currently, for foreign asset managers, other than issuing mutual funds via a fund management company ("FMC"), generally their onshore products have been allowed to raise funds from professional investors only.

Another key factor for foreign asset managers to consider the appropriate PRC license is their target investment vehicles. For example, QFIIs have become increasingly popular since 2020 as their investment scope has been expanded to cover, among others, A-shares, futures, and options generally. On the other hand, if a foreign asset manager is interested in investing in China's bond market only, it may consider the Bond Connect or CIBM Direct scheme rather than applying for a QFII license, so as to minimize potential regulatory costs.

- Investment Manager vs Investment Advisor

Under China's regulatory framework, investment management and investment advisory services are essentially differentiated. Investment managers launch their own products by raising fund from clients and may make investment decisions, whilst investment advisors generally provide investment advice only but does not raise fund or make investment decisions. One exception is the pilot mutual fund investment advisory program, under which investment advisors may determine investments in mutual fund products for clients.

Investment managers may wish to learn the rules applicable to investment advisors, which vary depending on the types of products (e.g., private funds, trust products, bank wealth management products). They may engage investment advisors, or even become investment advisors to other investment managers. For example, among the around thirty foreign wholly-owned private securities investment fund managers ("PFM") registered with the Asset Management Association of China ("AMAC"), twelve have further obtained the qualification to provide investment advisory services, such as the PFMs of Fullerton, UBS, Man Group, Winton, and Bridgewater.

- Interaction or Synergy Between Different Licenses

China's asset management regime consists of various asset management licenses which are subject to different specific regulatory rules. The regulators have long been considering how to unify regulations on asset managers to minimize regulatory arbitrage. Back in 2018, the Guiding Opinions on Regulating Asset Management Business of Financial Institutions was issued by several major regulators jointly, which aims to unify the regulatory standards applicable to asset management products of the same type. Since then, relevant detailed rules have been further promulgated by specific regulators including particularly the China Securities Regulatory Commission (the "CSRC") and the China Banking and Insurance Regulatory Commission (the "CBIRC").

The above said, currently the rules applicable to different asset management licenses still vary to a certain extent. Also, from a commercial perspective, in practice different types of PRC asset managers have different advantages. As such, foreign asset managers might consider how a license may interact with others, and whether synergy can be achieved by obtaining multiple licenses.

For example,

- we notice that some clients, parallel to obtaining an asset management license under the CSRC/AMAC regulatory regime (e.g., securities company's asset management business line, PFM, or FMC), may also consider obtaining a bank wealth management license under the CBIRC regulatory regime;

- QFIIs may engage their affiliated onshore PFM as investment advisor, and may also invest in the products launched by PFMs; and

- since the removal of foreign ownership cap in FMCs, certain renowned foreign asset managers have obtained or are applying for the FMC license on the basis of their existing PFM.

Further, multi-licensed foreign financial institutions might wish to leverage or share resources between different entities controlled by them. For example, they may consider, when establishing a new licensed entity in China, whether to set up a separate research team or leverage their existing offshore research team.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.