- within International Law topic(s)

Limited liability companies ("LLCs") are used regularly in estate planning to achieve estate tax savings and to consolidate asset management.

The first of these objectives can be realized when a business entity is utilized to facilitate gifting or transfers to children and other beneficiaries, often at discounted values, thereby reducing the value of the donor's assets that ultimately are subject to gift and estate taxation. Just as meaningful are the non-tax benefits of a properly-structured LLC: insulating owners from liability and providing an organizational control mechanism.

LLC Operation and Non-Tax Benefits

An LLC is a particularly flexible form of business entity that is governed by statute and most often is organized in the estate planning context as a "manager managed" LLC. This means that management functions and authority rest in designated or duly-elected "managers," as opposed to the LLC's owners—or "members." Separating management from ownership allows a donor to transfer some of the economic benefits of the asset(s) or business while retaining (or bestowing) control over operations. If taken a step further, this concept of limiting managerial or voting rights also happens to justify valuation discounts for the ownership interests of members who lack control over the company's affairs—presenting a tax planning opportunity to be discussed later in this article.

Non-Tax benefits of an LLC can include:

- Providing a streamlined mechanism for ownership transfers;

- Creating a structure for centralized management/control and succession thereof;

- Preserving family ownership through rights of purchase and first refusal;

- Establishing procedures for resolving intra-family disputes;

- Affording protection of LLC assets from claims asserted against owners; and

- Affording protection of owners from claims asserted against the LLC.

Tax Planning Through Lifetime Gift Transfers

When an affluent individual or family business owner desires ultimately to pass wealth or business ownership on to the next generation(s), succession planning and the owner's estate planning are inextricably linked. The most difficult issues and decisions presented in that context can relate to management control and personnel— (i) identifying or choosing who will control and manage the assets or business and (ii) figuring out how to keep key employees or advisors in place. Those issues are beyond the scope of this article. Instead, this article will focus on how, after ownership and management succession decisions have been made, careful estate planning through lifetime transfers can dramatically lessen the family's estate tax burden.

As illustrated below, incredible tax savings can be achieved through lifetime gifts of LLC interests thanks to valuation discounting and the removal of future appreciation from the donor's estate.

It is important to note that intra-family business transfers and transactions are complex and this article does not purport to address all (or even most) types of transactions or the issues that require careful analysis before undertaking lifetime transfers. Instead, the discussion herein provides an abridged example of the potential federal estate tax savings associated with lifetime transfers in one hypothetical family situation. All real life business succession situations are unique. If your situation is different than the one set forth below, that is to be expected—estate tax planning for your family might be structured differently. The takeaway is that good estate planning can result in substantial estate tax savings.

A key point of this article relates to the relative uncertainty of the future of U.S. federal gift estate tax law. Generally speaking, under current federal estate tax law, a U.S. Citizen can give or bequeath up to $12,920,000.00 ($10,000,000.00, indexed to inflation at $12,920,000.00 in 2023) of assets to non-spousal beneficiaries free of federal gift or estate tax. This exclusion from estate tax is often referred to as the "Gift and Estate Tax Exclusion Amount" (the "Exclusion Amount"). However, current law also provides that, absent intervention from Congress, the Exclusion Amount will be reduced to pre-2018 levels, or $5,000,000.00 per donor (indexed to inflation), starting on January 1, 2026. This tax law provision is referred to as a "sunset clause." With current federal estate tax law being about as taxpayer-friendly as it has ever been, and in light of the impending sunset date and the divisive current political climate, business owners and affluent individuals may want to consider taking advantage of their increased Exclusion Amount before it is a thing of the past.

Here are the facts that we will use for the purposes of our hypothetical illustration:

- Wanda and Harry are married and have three children: Adam, Betsy, and Chris.

- Wanda owns and manages 100% of ABC Co., LLC (the "LLC"), a successful enterprise or holding company valued at $20,000,000.00. (Important Note: Small and mid-sized businesses often have a higher value, as determined by the IRS, than the owners anticipate. While we will use a business entity valued at $20,000,000.00 for this illustration, your assets or business needn't be valued that high in order to achieve savings from careful estate planning.)

- Wanda and Harry want their three children ultimately to become equal owners and to take over management of the LLC.

- Wanda and Harry currently own assets, other than the LLC, totaling $5,000,000.00 in value.

- Wanda and Harry will pass away 20 years from now.

Here are important legal and financial assumptions that we will make for the purposes of our illustration.

- The LLC and Wanda and Harry's other assets will appreciate at a rate of 4% annually.

- The Exclusion Amount, which currently is $10,000,000.00 (indexed to inflation at $12,920,000.00 for 2023) per donor, will revert back to pre-2018 amounts ($5,000,000.00 per person, indexed to inflation), as of January 1, 2026. (Important Note: As discussed above, this assumption is consistent with the sunset clause provision of the current law. Without action by Congress, the recently-increased Exclusion Amounts will decrease to pre-2018 levels as of January 1, 2026). We will assume that the Exclusion Amount will be $7,000,000.00 per donor when Wanda and Harry pass away in 20 years.

Below are illustrative calculations and explanations of the potential federal estate tax consequences of two different estate planning scenarios, as applied to the above facts and assumptions:

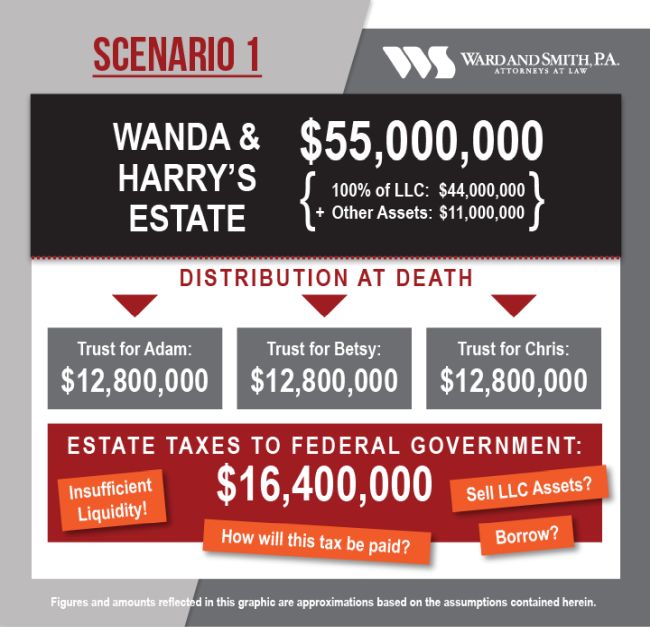

Scenario (1):

Wanda and Harry do not undertake lifetime transfers of the LLC interests to their children, and instead, when they die in 20 years, their Wills leave Wanda's ownership interest in the company to the three children, or to trusts for the three children, in equal shares.

The result under Scenario (1):

Due to the appreciation of Wanda and Harry's estate, approximately $16,400,000.00 of estate tax is owed when they pass away after 20 years. Based on the assumptions made above, Wanda and Harry's taxable estate will have appreciated to nearly $55,000,000.00 over the course of 20 years—with nearly $44,000,000.00 of that value being attributable to the LLC assets. In that case, Wanda and Harry's estate will exceed their combined available Exclusion Amounts ($14,000,000.00) by more than $40,000,000.00. Applying that figure to a 40% estate tax rate is how we arrive at an estate tax estimate of $16,400,000.00. An astute reader will note that the amount of estate tax owed under this scenario actually exceeds the value of the non-LLC assets that pass as part of Wanda and Harry's estate—creating a liquidity crisis that may be a very difficult problem for the kids to sort out.

Let us take a look at how Wanda and Harry could have planned better.

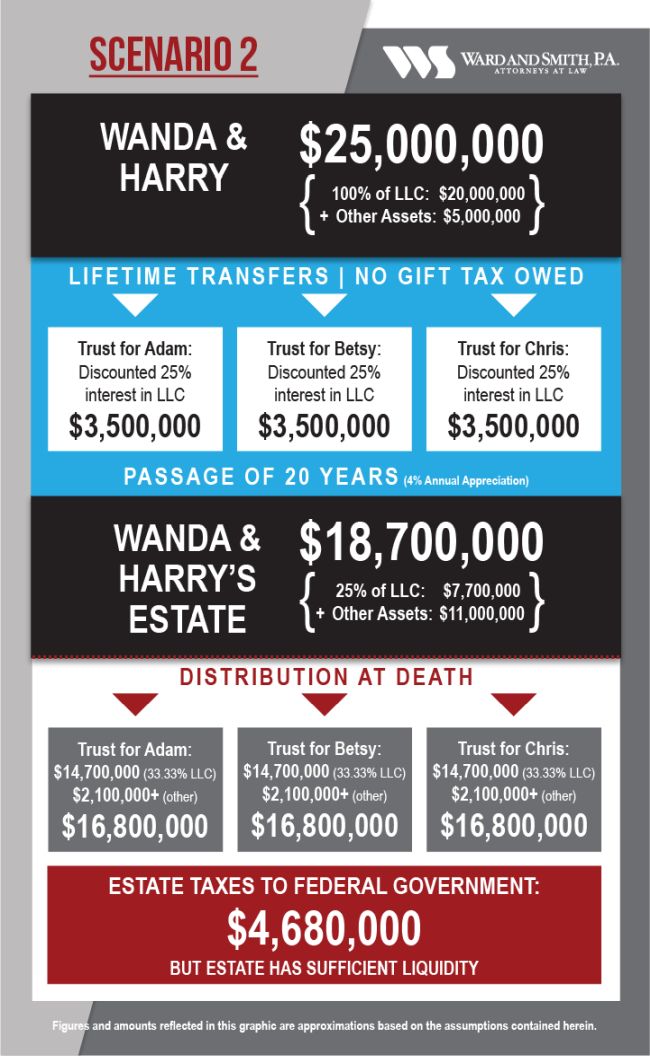

Scenario (2):

With the advice and assistance of their professional advisors, Wanda and Harry undertake carefully-planned lifetime transfers of Wanda's interests in the LLC to the children or to trusts for their benefit.

The result under Scenario (2): Due to the removal of future appreciation on the business ownership interests (and income therefrom) achieved through lifetime transfers to the three children, less than $5,000,000.00 of estate tax is owed—that's more than $11,500,000.00 in estate tax savings as compared to Scenario (1). Here's how:

Wanda works with her attorneys to structure the LLC ownership as voting and non-voting LLC interests. Wanda thoughtfully structures the entity so that all of the voting rights associated with LLC ownership are contained in 1% of the LLC ownership interests, and the other 99% of the ownership interests have economic rights to LLC earnings but no voting authority with regard to business management. As a result of this structure, the non-voting interests in the LLC are worth less, with the IRS having approved valuation discounts for non-voting interests equal to at least 30%.

Wanda then gives 25% of the LLC ownership interests to each child (or to a trust for each child) and retains 25% of the LLC—including the 1% voting interest so that she can continue to control the LLC. After applying a 30% discount, the gifts of 25% of the Company ownership interests to each child will have a discounted value for gift tax purposes equal to approximately $3,500,000.00 (or $10,500,000.00 in total, for all three gifts), but no gift tax is owed at the time of the transfers because Wanda applies her historically-high Exclusion Amount to the gifts. After the transfer of the 25% ownership interest to each child (or to his or her trust), those interests continue to appreciate outside of Wanda and Harry's Estate. So, under this scenario, Wanda and Harry's estate is valued at approximately $18,700,000.00 at the time of their deaths 20 years later (rather than $55,000,000.00, as in Scenario (1)). After applying Harry's $7,000,000.00 unused Exclusion Amount to Wanda and Harry's remaining estate, only about $4,680,000.00 of estate tax would be owed. The remainder of the estate, and the previously gifted ownership interests in LLC (as well as all appreciation thereon and income produced therefrom), pass to the children. Side note: Wanda also could structure her estate plan to stipulate that her voting interest in the LLC will pass to a specific child after her death (Betsy, probably), thereby granting control to the child that is best-suited for management.

As you can see, under the right circumstances, lifetime transfers can generate tremendous estate tax savings. In addition, if the transfers are made to trusts for the children (rather than to the child, outright) it may be possible to achieve additional benefits, including increased protection against lawsuits, dissolving marriages, and future estate taxes.

Now that we have illustrated the dramatic benefits, we must underscore that these types of transactions are not without risk and downside and must be carefully vetted by experienced tax and legal advisors. One very important downside to lifetime gifting is that, unlike assets that pass as part of a donor's estate, gifted assets do not receive a basis adjustment for income tax purposes at the time of the donor's death under current law. Another downside is that the donor generally is not able to benefit economically from the gifted assets after they are transferred. However, in cases where the donor is concerned about divesting his or herself of the transferred asset (and the income therefrom), it is possible that the transfer could be structured as a sale, rather than a gift, in order to provide increased cash flow back to the transferor.

Observing Formalities in Administrative Management of LLCs

A final point about the importance of careful administration. If an LLC is not operated consistently with the entity's non-tax business purposes, it may be vulnerable to attack by the IRS or third parties, undermining estate tax planning or limited liability protections. For this reason, the entity should be administered in a way that supports its valid business purpose as a legitimate enterprise. While not an exhaustive list, the following are examples of general principles that should be followed in this regard:

- Terms of the LLC's operating agreement should be adhered to;

- Distributions to the LLC members should be made pro rata, consistent with ownership interests;

- The LLC's assets should be clearly segregated from personal assets through titling the assets in the name of the LLC;

- The LLC should not hold "personal use" assets, such as a non-investment residence;

- Formalities of business organization should be followed, including documented meetings to discuss the entity's business operations;

- The LLC's manager should actively engage in business management, and in many cases should be compensated for such services; and

- Partnership income tax returns should be filed annually.

Conclusion

Lifetime transfers of LLC interests are not a silver bullet for all situations. However, given the uncertain future of federal estate tax law, business owners and affluent individuals should absolutely consider making lifetime gifts to take advantage of their increased Gift and Estate Tax Exclusion Amount before it becomes a thing of the past. If your circumstances may require estate tax planning, contact one of our Trusts and Estates attorneys today.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.