- with readers working within the Aerospace & Defence industries

- within Criminal Law, Privacy and Law Department Performance topic(s)

- with Finance and Tax Executives

Key Takeaways:

- Forfeiture accounts are common in retirement plans, but inconsistent application and shifting guidance are driving increased regulatory scrutiny.

- Plan sponsors must understand permitted uses, follow required timelines, and document decisions to stay compliant and reduce fiduciary risk.

- A proactive governance approach — including regular monitoring and clear processes — helps protect plan qualification and build participant trust.

Forfeiture accounts are a routine part of many retirement plans — but they're also getting more attention from regulators. These accounts accumulate funds when employees leave a company before becoming fully vested in employer contributions. And while they may seem straightforward, forfeitures can create real compliance issues for plan sponsors if they aren't handled correctly.

Most plan documents include forfeiture provisions that often align with the IRS' proposed regulations from February 2023. But in practice, those rules aren't always applied consistently. For plan fiduciaries, understanding both the requires AND the practical steps for using forfeitures on time is essential.

Regulatory Context: IRS, ERISA, and DOL Guidance

Several regulatory authorities influence how forfeiture accounts must be handled:

- ERISA requires fiduciaries to act in the best interest of plan participants and beneficiaries, including when deciding how forfeitures are used.

- IRS guidance generally allows three

uses for forfeiture funds:

- Paying reasonable plan expenses

- Reducing future employer contributions (i.e., lowering what the employer is required to contribute)

- Allocating funds to participant accounts to increase benefits

Even with these clear categories, applying the rules can still be tricky, particularly as regulatory positions evolve. Recent litigation has questioned whether using forfeitures to offset employer contributions is appropriate, although a recent Department of Labor brief supported this practice in a specific case.

Because of this evolving landscape, plan sponsors need to stay aware of not only the formal guidance, but also how interpretations may shift due to new cases or regulatory updates.

Risks of Inaction or Mismanagement

Forfeiture balances typically must be used either by the end of the plan year in which they arise or by the end of the following year depending on plan terms. Missing that window can jeopardize the plan's tax-qualified status (meaning it could lose its favorable tax treatment).

There's also the risk of participant challenges. In the last few years, more than 70 federal lawsuits have been filed over to forfeiture usage, often claiming that using forfeitures to reduce employer contributions violates fiduciary duties. Beyond litigation costs and regulatory scrutiny, these disputes can create uncertainty for both fiduciaries and participants.

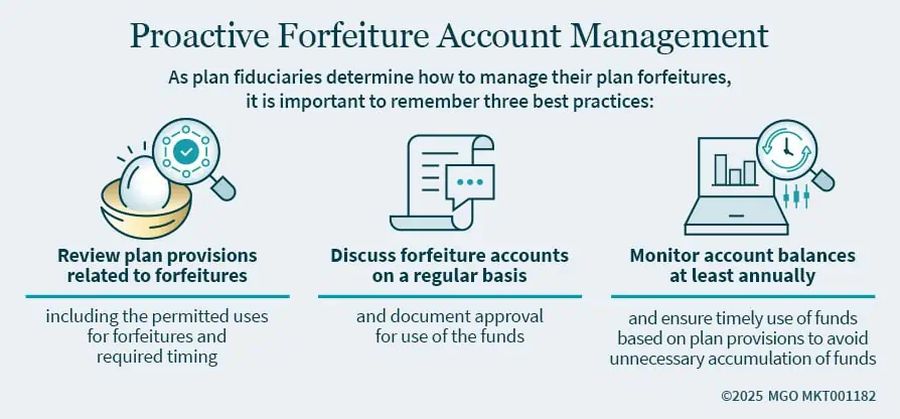

Practical Steps for Oversight

To manage forfeiture accounts effectively and mitigate associated risks, plan sponsors should consider these governance practices:

- Review the plan document's forfeiture

provisions

Confirm permitted uses and required timelines for using forfeiture balances. - Incorporate forfeiture discussions into regular

oversight routines

Document decisions about how and when funds are applied. - Monitor forfeiture balances at least

annually

Use available funds within required timeframes to prevent unnecessary accumulation or inaction.

Forfeitures are a normal component of qualified retirement plans, but they require consistent attention. A proactive governance approach can support both compliance and participant trust.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]