- in United States

- with readers working within the Aerospace & Defence industries

- within Compliance topic(s)

A lot has been written about the importance of indices.

Index providers, whether the large providers responsible for benchmark indices or smaller index providers, regularly develop and maintain a myriad of indices. These indices may be designed to reflect an investment thesis; the performance of a sector, a region, an asset class or a particular market measure; or any other of a variety of objectives. In any event, index providers and indices have become indispensable. Index providers have well-defined rules-based methodologies that define their indices. These generally are published. These methodologies outline, among other things, the index selection criteria, the weighting of index constituents, the effect of corporate events on the index (such as the effect on the index of a stock split or a spin-off), and index rebalancings. For large benchmark indices, providers conduct consultations from time to time relating to potential changes to their index methodologies. An index provider may remove an index constituent that no longer meets the criteria for inclusion in the index. Similarly, an index provider may consider the inclusion of a new constituent. From time to time, there are exceptional events.

In this newsletter, we have reported on exceptional events in the life of indices. For example, some index providers considered whether or how to address dual class or multi-share class stocks. Some index providers were compelled to address the exclusion of securities issued by companies that were based in the PRC or in Russia. And so on. Now, we come upon another exceptional event, though likely not the last such exceptional event—whether indices will modify their rules for early inclusion of certain IPO stocks

A lot turns on this given that many funds track indices, including many funds that invest on behalf of retail investors. Similarly, exchange-traded products, like ETFs, track indices. Changes to benchmark indices affect the portfolios and retirement accounts of millions of retail investors who are likely not paying close attention to index providers’ press releases.

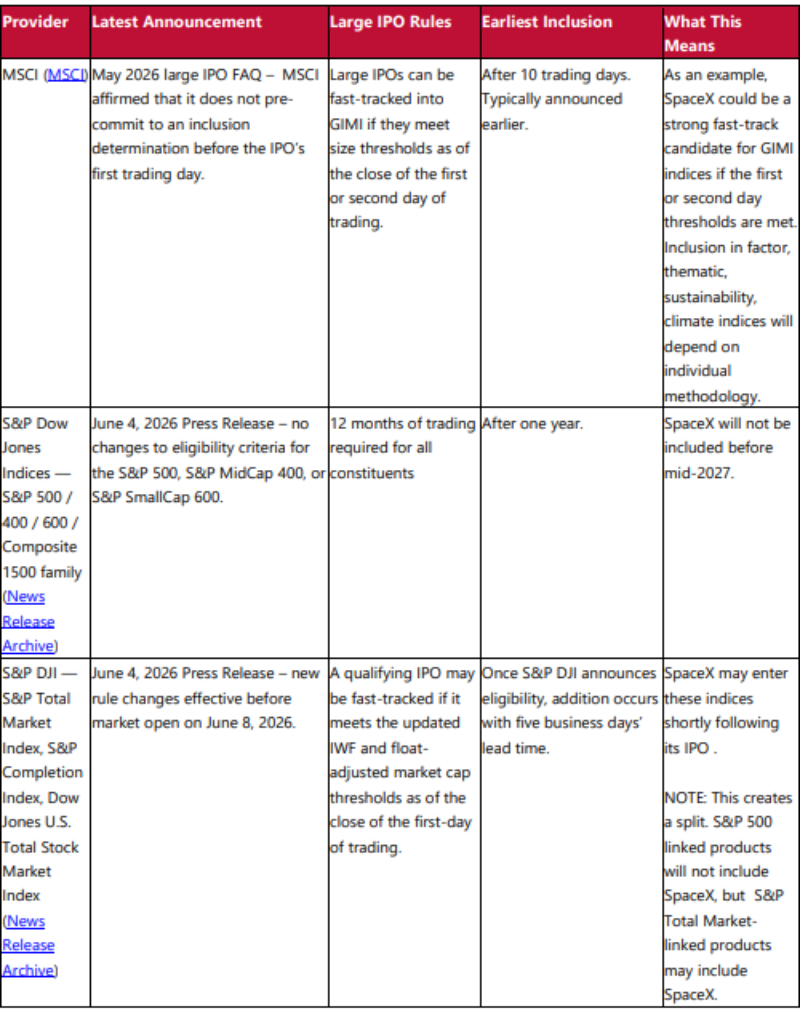

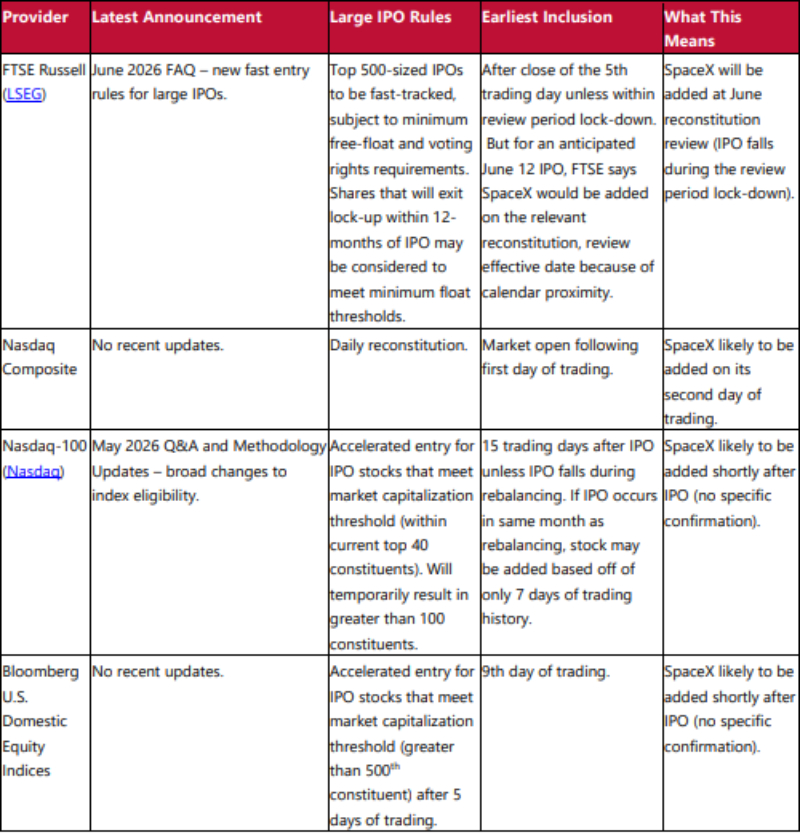

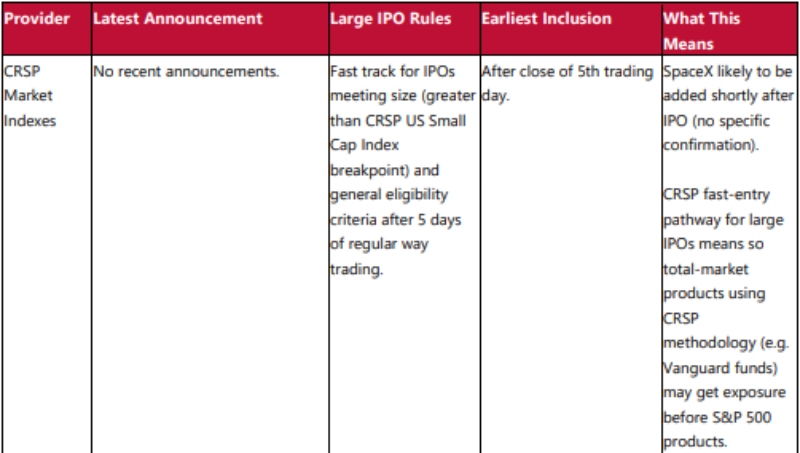

While this is an area that has been changing by the day, we report on the current state. Below, for illustration, we use one particular IPO stock as an example.

Originally published in REVERSEinquiries: Volume 7, Issue 3.

Click here to read the articles in this latest edition.

Visit us at mayerbrown.com

Mayer Brown is a global services provider comprising associated legal practices that are separate entities, including Mayer Brown LLP (Illinois, USA), Mayer Brown International LLP (England & Wales), Mayer Brown (a Hong Kong partnership) and Tauil & Chequer Advogados (a Brazilian law partnership) and non-legal service providers, which provide consultancy services (collectively, the "Mayer Brown Practices"). The Mayer Brown Practices are established in various jurisdictions and may be a legal person or a partnership. PK Wong & Nair LLC ("PKWN") is the constituent Singapore law practice of our licensed joint law venture in Singapore, Mayer Brown PK Wong & Nair Pte. Ltd. Details of the individual Mayer Brown Practices and PKWN can be found in the Legal Notices section of our website. "Mayer Brown" and the Mayer Brown logo are the trademarks of Mayer Brown.

© Copyright 2026. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.

[View Source]