- within Criminal Law, Wealth Management and Intellectual Property topic(s)

It is now seven months and counting since COVID-19 was declared a pandemic, and commercial aviation faces a crisis like nothing it has seen before. With restrictions continuing across most major markets and strengthening again in some, it is now clear that a sustained downturn is ahead for the industry. A V-shaped recovery is unlikely outside of the domestic China and Russia markets.

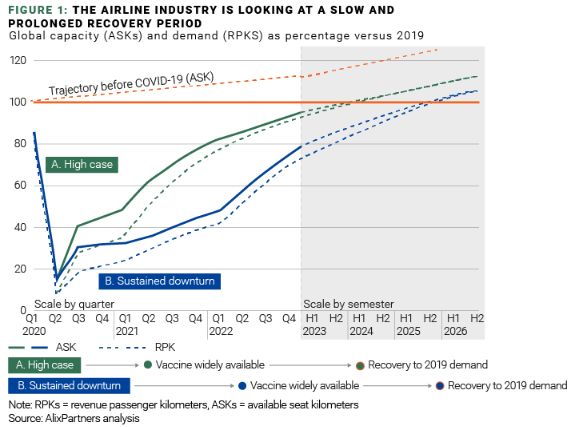

While early in the summer there were expectations of air travel demand returning and reaching 60% or higher of last year's traffic by the year's end, those hopes have dwindled fast. Business traffic, especially high-yield intercontinental travel, is not returning anytime soon. AlixPartners forecasts that passenger traffic will not return to pre-pandemic levels before 2024-2025 (figure 1).

The High Case recovery scenario reflects a COVID-19 vaccine widely available worldwide by June 2021, with GDP coming back to 2019 levels in most regions by early 2022. The Sustained Downturn scenario assumes a vaccine widely available one year later and a more prolonged global economic recession.

In both scenarios, airlines are looking at a very cold winter with anemic traffic recovery until next summer. While winter is typically the low season for airlines, this year they will be running at much lower capacity than usual—anywhere from 50% to as little as 20% of 2019 schedules.

Quarantines and entry bans have decimated global travel, hitting airlines without large domestic markets hardest. But no passenger airline business model has been spared. The loss of business and higher-yield passengers is impacting all carriers. Even leisure demand is a fraction of what it was. Both leisure and business travelers are making bookings much later because of fast-changing travel restrictions. As a result, booking curves used by airlines to understand demand and pricing are now measured in days, not weeks or months, and revenue management models and pricing systems no longer work in the current erratic demand dynamics. Excess capacity and attempts to attract passengers have also forced lower fares.

Airlines took a broad range of actions to cut costs, but initial recovery plans were built on the assumption that traffic would be at 70-80% of 2019 levels. However, load factors stayed at all-time lows (globally 59%, Middle East at 37%, US at 48%, Europe at 64%, Asia at 65% in August) even as airlines added back capacity faster than demand returned. Consequently, most airlines are continuing to burn through cash.

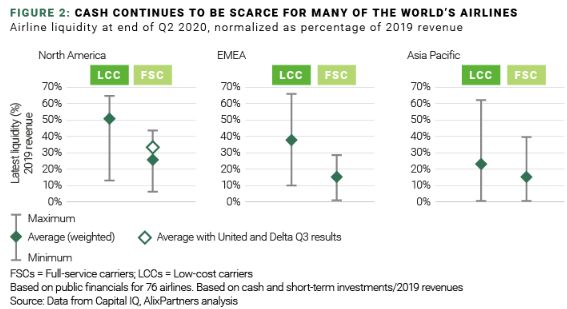

International Air Transport Association (IATA) projects that airlines will burn through $77 billion of cash during the second half of 2020 and $5 to $6 billion per month throughout 2021. At the end of Q2, airlines in North America had better liquidity than their counterparts in EMEA and Asia, thanks in part to CARES Act aid. But across all regions, a large number still only had a few months or weeks of cash left (Figure 2). Full-service carriers (FSCs) in EMEA and Asia had only 15% of 2019 revenues in cash on average. Low-cost carriers (LCCs) with more flexible operating models do sit in a better position than FSCs globally.

The first wave of public aid—$162 billion globally of payroll support, recapitalization, loans, and loan guarantees—was critical, but government help cannot sustain the industry in the longer term. Funding options for airlines are becoming more limited and more expensive as the low-hanging opportunities have already been taken and asset prices are continuing to decline. Airlines must take action now to develop robust restructuring plans leveraging creative solutions and focusing on cash preservation in an extremely uncertain current environment in order to benefit when recovery occurs. Here are some steps to do so:

- Build off conservative planning scenarios: Plan for plausible worst-case traffic outcomes and use these assumptions to define cash requirements. Set up smart indicators to detect demand down to route and market level. Focus on targeting a realistic cash breakeven point rather than trying to predict when demand will return.

- Resize the network: Resize your core network, focusing on key markets as they exist, not as they were in 2019. Redesign networks and schedules for the new demand profile. Make cash-generating flying your goal rather than taking an accounting view.

- Redesign operations and revenue planning processes for agility and link them to cash: Prioritize cash over all else—centralizing cash management and instilling a cash culture. Develop detailed and flexible cash forecasting models to simulate network plan and schedule options. Revamp obsolete demand, pricing, and inventory management models with advanced analytics, machine learning, and new data sources. Develop playbooks that allow for quick responses to changes in the market as they happen and shorten planning cycles from months to weeks.

- Restructure the fleet and review the product: Focus on cost-efficient fleet types, balancing unit cost efficiency with trip costs to allow networks to be rebuilt even with weak demand. Negotiate with equipment manufacturers to reschedule or cancel orders and with lessors to restructure leases, mark lease rates to market, or explore alternative solutions such as pay-by-the-hour arrangements. Identify ways to drive cash with cargo or alternative non-hub flying. Re-examine both hard product (seating density, cabin size) and soft product (food, lounges, in-flight entertainment) in line with the changed mix of business versus leisure travel.

- Screen all activities for outsourcing opportunities to get leaner: Securing a highly variable and efficient cost structure is critical in the current context. Review all operations and subsidiaries from ground handling to maintenance and repairs. Consider joint ventures, sales, or other alternatives for catering and flight training to raise cash.

- Relentlessly drive cost-outs: Reassess headcount in line with conservative traffic assumptions. As a next step to payment holidays from vendors, which should already have been obtained, systematically renegotiate all contracts—not just big-ticket items. Consider robotic process automation and intelligent automation to drive both internal and external cost-outs.

The airline industry has always been cyclical, but this winter is no typical downturn or shock. Airlines must get ready and thoughtfully prepare for a brutal winter if they are to reach spring 2021 in a healthy enough position to enjoy the early shoots of an eventual recovery.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.