- in European Union

- with readers working within the Accounting & Consultancy and Insurance industries

- within Litigation and Mediation & Arbitration topic(s)

As finance leaders look to the year ahead, the tone from regulators continues to evolve and emphasize pragmatism, fundamentals, and decision-useful information without lowering the bar on financial reporting and audit quality. Effective finance and accounting teams will have to navigate a variety of critical matters as stakeholder expectations rise, regulations evolve, and transactions become more complex.

"What stood out was not one overwhelming issue, but the reality that companies are being asked to absorb multiple layers of change at the same time."

In December 2025, accounting, finance, and reporting leaders convened in Washington, DC for the AICPA and CIMA Conference on Current SEC and PCAOB Developments, a three-day forum widely regarded as a bellwether for regulatory priorities and emerging trends shaping the profession. The conference offered a timely view into the direction of US capital markets regulation, audit oversight, and accounting standard setting at a moment when preparers and auditors alike are navigating heightened complexity alongside increasing expectations for transparency, consistency, and quality.

Following the conference, Riveron hosted a debrief webinar to synthesize the most impactful insights and translate them into practical considerations for finance leaders, management teams, and accounting professionals. The discussion focused on what matters most as organizations look ahead to 2026, including evolving SEC priorities, audit quality and inspection themes, standard-setting developments, and the operational realities facing both public and private companies. The perspectives summarized below reflect the collective takeaways from that discussion, with an emphasis on actionable considerations as organizations prepare for year-end reporting, audit season, and the year ahead.

Participants were polled on their biggest anticipated financial reporting challenge in 2026, and the responses were distributed relatively evenly, including:

- Adoption of the disaggregation of income statement expenses standard

- Income tax reporting and expanded disclosure requirements

- Financial reporting implications of tariffs

- Impairment considerations

- Increasingly complex financial and M&A-related arrangements

The variety of accounting and financial reporting topics indicate that the office of the CFO will have to address many evolving priorities in the year ahead. As Patrick Garrett observed, "What stood out was not one overwhelming issue, but the reality that companies are being asked to absorb multiple layers of change at the same time."

A Shift in Tone from the SEC and PCAOB

Regulatory messaging emphasized pragmatism and a renewed focus on fundamentals, particularly the importance of delivering information that is both pertinent and material in decision-making to investors. SEC leadership openly acknowledged that disclosure overload, litigation risk, and governance complexity have become meaningful deterrents to companies considering entry into the public markets.

Lara Long summarized the shift succinctly, observing that "the message from regulators was refreshingly direct, with a clear emphasis on fundamentals and transparency rather than prescriptive enforcement."

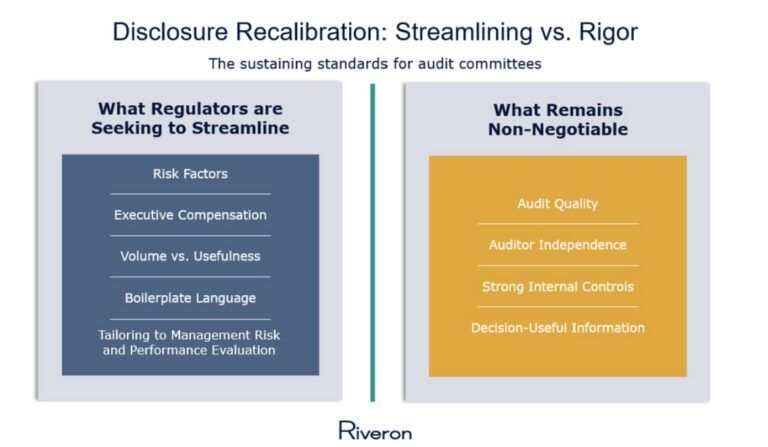

This recalibration was especially evident in discussions around disclosure effectiveness. Risk factor disclosures and executive compensation reporting were frequently cited as areas where volume has increased without a corresponding increase in usefulness. Registrants were encouraged to critically assess whether disclosures are tailored, current, and aligned with how management evaluates risk and performance. At the same time, regulators emphasized that streamlining disclosures does not equate to lowering expectations. Audit quality, auditor independence, and strong internal controls remain foundational.

As Long emphasized, "Reducing disclosure clutter does not mean reducing rigor. The bar for quality remains very high."

Audit oversight discussions reinforced this message. The PCAOB reiterated its emphasis on tone at the top, firm-wide systems of quality management, and consistent execution across engagement teams. With implementation of the new quality control standard deferred again, inspection efforts are increasingly focused on how firms design and operate quality management systems in practice rather than on isolated engagement deficiencies. From a preparer's perspective, this focus reinforces the importance of early planning, timely involvement of specialists, and proactive coordination with auditors throughout the audit cycle. Garrett highlighted that "inspection outcomes are increasingly tied to how well firms and issuers anticipate issues early, not how well they react late."

Operational realities at the SEC were also featured prominently. Ongoing staffing constraints and filing backlogs continue to influence the review process, with a first-in, first-out approach now standard and IPOs receiving priority. In this environment, early engagement with auditors and SEC staff on complex transactions is critical. Transactions such as spinoffs, predecessor or successor determinations, and multi-step combinations require advanced planning and early dialogue to avoid timing challenges during the review process. Long noted that early engagement has become less of a best practice and more of a necessity in the current environment.

Evolving Guidance, Consistent Expectations

Recent remarks from SEC leadership and standard setters point to a clear recalibration in regulatory priorities. While there is a growing effort to streamline disclosures and reduce unnecessary complexity, expectations around audit quality, transparency, and decision-useful information remain firmly in place. Below are several key takeaways to navigate evolving regulatory and standard-setting developments:

- Global convergence is gaining momentum. SEC leadership emphasized closer alignment between US and international accounting and auditing standards, including potential coordination between the PCAOB and global standard setters. For multinational organizations, this signals a possible reduction in pergence over time — while reinforcing the importance of closely monitoring global regulatory developments.

- Reporting frequency may evolve, but expectations will not. While semi-annual reporting was discussed as a potential way to reduce burden, regulators and preparers cautioned that investor and analyst demand for timely, high-quality information is unlikely to diminish. Even if reporting cadence changes, the market's expectations around transparency and responsiveness remain intact.

- Core areas of SEC focus remain unchanged. Continued emphasis was placed on non-GAAP measures, revenue recognition, and MD&A disclosures that address current macroeconomic risks, including tariffs. Strong internal controls continue to be viewed as foundational, particularly as companies provide more forward-looking information. Streamlining disclosures does not equate to lowering the bar.

- Segment reporting remains under scrutiny. Following the first year of ASU 2023-07 implementation, SEC staff observed recurring deficiencies in explaining how the chief operating decision maker uses reported measures of segment profit or loss. Overreliance on quantitative tables and income statement cross-references — especially among single-segment issuers — continues to be a concern, underscoring the need for clearer narrative context.

- Standard-setting is shifting toward practical, implementable guidance. Recent FASB updates addressed ESG-linked derivative scope exceptions, share-based noncash consideration in revenue arrangements, targeted CECL relief for certain purchased loans, and modernized guidance for internal-use software. The overarching theme is guidance that is workable for preparers while still faithfully reflecting economic reality.

Valerie Flanigan underscored this approach, noting that "the Board is clearly focused on making standards workable for preparers while still faithfully reflecting the economics of increasingly complex transactions."

Near-term adoption challenges

Expanded income tax disclosures under ASU 2023-09 and the forthcoming disaggregation of income statement expenses standard were top of mind. The income tax disclosure requirements are already effective at year end 2025 for calendar-year public companies and require more granular data, enhanced cross-functional coordination, and strengthened internal controls. Polling results indicated a wide dispersion in readiness, with many organizations still in early stages of implementation.

Flanigan emphasized that "early assessments of data availability, definitions, and system readiness are critical to avoiding compressed timelines and execution risk."

Emerging Technologies and Business Models

The accelerating use of artificial intelligence in finance underscores the need to govern AI like any other system, with appropriate controls, human oversight, and accountability. At the same time, regulators, activists, and analysts are increasingly using AI to analyze companies' reported results and management commentary provided during earnings calls, raising expectations around consistency and narrative discipline.

Kayla Mayfield observed that "AI is quickly becoming both a tool for preparers and a lens through which disclosures are evaluated, which raises the stakes for consistency and control."

Finally, renewed SPAC activity driven by more experienced sponsors reinforced the importance of technical rigor, consistent judgments, and clear investor communication in a continuous reporting environment. As Mayfield noted, "the always-on nature of reporting in these structures leaves little room for misalignment between accounting conclusions and investor messaging."

Looking Ahead: The Year of Balance

Regulators and standard setters are signaling a desire to refocus on fundamentals and reduce unnecessary complexity, while maintaining high expectations for quality, transparency, and accountability. Organizations that invest early in planning, engage proactively with auditors and regulators, and remain disciplined in execution will be best positioned to navigate the evolving financial reporting landscape this year.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.