1.1. INTRODUCTION

On 26 June 2008 the Liechtenstein Parliament passed the new foundation law. The new Foundation Act (hereafter referred to as the StiG), together with the amendments to the Law on Persons and Companies (PGR), was published on 26 August 2008 in the Liechtenstein Law Gazette No. 220/2008. It comes into force on 1 April 2009 subject to transitional periods (see under Point 8).

It has long been one of the intentions of the Liechtenstein Government and the legislature to introduce statutory amendments which reflect the various rulings passed by the country's high court which had brought about changes in the foundation law, a law which had been in existence for 70 years. In addition, the aim was not only to put a stop to what were in some cases rather questionable developments that had been adopted into practice by the foundation law on the basis of a wide-ranging reference norm to the Law on Trust Enterprises (TrUG), but also to create clarity with regard to the legal form of the foundation. Yet, it was not the subject of taxation that provided the impetus for the reform of the foundation law and therefore, media reports to this effect are based on a lack of subject knowledge.

The aim of the legislature was to create a modern, self-contained foundation law that retained its competitive nature. The founder's level of responsibility has been increased, new rules have been drawn up for the procedure in respect of the establishment or amendment of foundations, with no requirement in the future for the copies of the statutes to be physically deposited with the competent authorities. The aspects of modern foundation governance were taken into account through clear regulations on the rights of the beneficiaries with a view to disclosure and information. The foundation supervisory authority, primarily responsible for the supervision of common-benefit foundations (in practice known as "charitable foundations") as well as the procedure for the establishment and amendment of foundations, has now been attached to the Office of Land and Public Registration as an independent department.

Finally, the transitional provisions stipulate which aspects of the new foundation law will also apply to existing foundations. Particular reference should be made in this context to the provisions on foundation governance, specifically the rights of the beneficiaries to disclosure and information.

2. DEFINITIONS

2.1. Purposes And Types Of Foundation

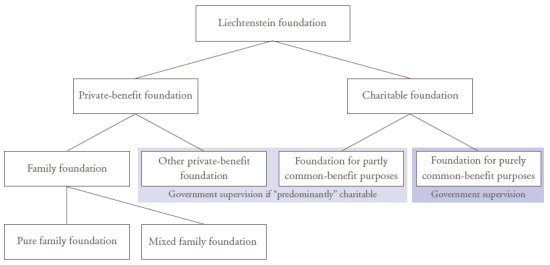

The new foundation law creates clarity with regard to the subject of definitions. The legislature draws a distinction between private-benefit and charitable foundations. It is also laying down a rule as to when mixed foundations, which continue to be permitted in future, are to be regarded as established predominantly for common-benefit or private-benefit purposes.

Mixed foundations are accordingly categorised as serving predominantly common-benefit purposes either if the charitable proportion is predominant or if it is not possible to weight common-benefit and private-benefit purposes as a result of open provisions. It is therefore recommended that in the future the foundation documents should clearly specify whether the intended purpose is predominantly of a charitable nature or whether despite its mixed character the foundation is to be regarded as established predominantly for private-benefit purposes. This will clearly define whether or not the foundation will be subject to Government supervision.

In the case of mixed family foundations attention must be paid to ensuring that the proportion with a family purpose exceeds the other purposes since the latter may only be of a supplementary nature. If a family foundation is to pursue predominantly common-benefit or non family-related private-benefit purposes, then it may be regarded as falling into the category of "other private-benefit foundation", may lose its family foundation character and may be subject to Government supervision if the charitable proportion is predominant or has not been clearly defined.

The provision in § 7 StiG has also allowed for a more precise description of the discretionary type of foundation by outlining the associated nature of beneficial interest and the rights of such beneficiaries.

2.2. Foundation Documents

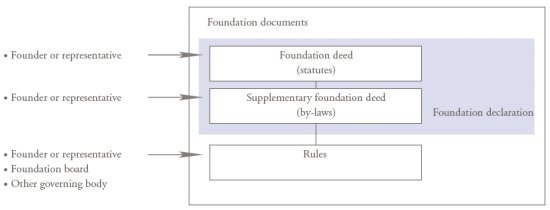

A clear document hierarchy has been created in the new foundation law. Amongst other things, the question has now been defined as to who is permitted to issue which documents and which mandatory and optional contents these documents may contain. In this context, all the relevant documents taken together represent the so-called "foundation documents" in accordance with the heading of No. II StiG.

2.2.1. Foundation Deed (Statutes)

The central document to be drawn up on a mandatory basis is the foundation deed, commonly known as the statutes. These simultaneously constitute the so-called foundation declaration in accordance with § 14 StiG (lit. B).

The foundation deed must contain:

- the founder's declaration of intent regarding his/her wish to form the foundation

- name respectively company name and domicile of the foundation

- asset endowment, at least CHF, USD or EUR 30'000 (minimum capital)

- purpose of the foundation, including appointment of beneficiaries (this can, however, also be included in the by-laws)

- date of formation

- duration, if the foundation is established for a limited period

- organisational provisions regarding the foundation board

- rules on the allocation of assets in the event of the foundation being liquidated

- address of the founder or the indirect representative (the representation must be expressly stated)

If the founder harbours the following intentions then the details relating to these must also be included in the statutes as a mandatory requirement:

- Existence or possibility to issue a supplementary foundation deed (by-laws)

- Existence or possibility to issue regulations

- Reference to any other existing governing bodies or the option to establish these (details in respect of these bodies can be defined in by-laws or regulations)

- Any right of revocation reserved for the founder or authority of the founder to make amendments

- Any powers of the foundation board or other governing bodies to make amendments

- Exclusion from enforcement Conversion provison

- Voluntary agreement to submit a private-benefit foundation to

- Government supervision

The statutes must be drawn up in writing and signed by the founder or his/ her indirect representative (i.e. trustee). The signatures of the founder or indirect representative must be authenticated.

2.2.2. Supplementary Foundation Deed (By-Laws)

Insofar as the founder has made corresponding provisions in the statutes he/ she can issue a supplementary foundation deed, also known as the by-laws. The by-laws can contain those elements of the foundation declaration/statutes whose inclusion in the statutes is not a mandatory legal requirement. In practice these are normally the specific regulations on beneficial interests.

The by-laws must also be issued and signed by the founder or his/her indirect representative. Here again the signatures must be authenticated since the by-laws form part of the foundation declaration.

Despite the abolition of the mandatory requirement for the statutes to be deposited, it remains good sense to issue statutes and by-laws separately. The reason for this is that in practice copies of the statutes frequently need to be presented or submitted to third parties for purposes of evidence. In this case separation into statutes and by-laws continues to provide additional protection in respect of the privacy of the beneficiaries nominated by the founder.

2.2.3. Regulations

Whilst statutes and by-laws are issued by the founder or, as the case may be, his/ her indirect representative, the foundation board or other governing bodies whose appointment is optional can, in addition to the founder, also issue regulations which contain the provisions on the execution of and/or internal instructions on the management of the foundation. However, the statutes must contain a provision which allows regulation to be drawn up.

The legislature has also stipulated that in the event of contradictions those regulations which have been issued by the founder him/herself shall have precedence over the regulations which have been issued by the foundation board or other governing bodies.

3. THE FOUNDER AND HIS/HER REPRESENTATIVE

It was the declared aim of the Government to increase the level of responsibility on the part of the founder. The reform has removed existing legal uncertainties with regard to the formation of foundations by trustees, foundations with undefined purpose as well as the legal quality of the founder's rights.

A representative will still be able to form the foundation, also in order to protect the founder's privacy with regard to the external relationships of the foundation. Representation has now been categorised as an indirect one, but having the effect of direct representation. This shall clearly state that all rights and obligations apply directly to the effective founder and that this person alone is seen as the founder. Direct representation is also permitted but requires a power of attorney to be issued by the founder for the establishment of the foundation. On the other hand, under § 4 Para. 3 StiG, the indirect representative has a mandatory requirement to disclose the name of the founder to the foundation board in any case.

The rights of the founder are neither transferable nor can they be inherited. Moreover, these can only be reserved if the founder is a natural person.

In contrast to the original intention, Government and Parliament have decided to allow enforcement in reserved founder rights (right of revocation or power of amendment). This is intended to put a stop to potential abuse of the foundation in connection with any detriment to creditors.

The founder has now been accorded a central and exclusive role in forming the foundation and drawing up the foundation declaration, if necessary represented by his/her indirect representative. This has relegated the previous option of wide-ranging powers being granted to the foundation board in favour of the founder's position with the principle of rigidity in mind. Protectors, collators and curators too will in future only be able to perform their role in accordance with the verifiable wishes of the founder. In the case of foundations under the new law it will no longer be possible in the future that amendments be readily made by the foundation board to by-laws in respect of the regulations on beneficiaries, either solely or in consultation with and the agreement of the first beneficiaries. Nevertheless, corresponding rules for foundations established under the old law may continue to be valid and permitted on the grounds of preserving trust under the constitution. However, no information is provided by law or substantive facts.

4. THE FORMATION AND SUBSEQUENT AMENDMENTS

4.1. Deposit Of The Notification Of Formation Or Registration

Under the new foundation law a distinction will continue to be drawn between registered and deposited foundations. As in the past, registered foundations will only acquire the right of personality upon registration whilst deposited foundations on the other hand will acquire the same right on the date of the formal signing of the foundation declaration.

All foundations established for common-benefit or predominantly common-benefit purposes are required to be registered in accordance with § 14 Para. 3 StiG. In addition, all private-benefit foundations which pursue a commercial business on a special statutory basis must be registered. There is also the option for other private-benefit foundations to be voluntarily recorded in the Public Register. However, if that should entail Government supervision then explicit provision must be made for this in the statutes.

Whereas in the case of registered foundations an authenticated transcript/ copy of the foundation deed must be enclosed with the application for registration, in the case of deposited foundations there is now no requirement for the submission of a copy of the foundation deed. Instead, a so-called notification of formation must now be drawn up and submitted within 30 days by a member of the foundation board or the representative.

The notification of formation must contain the following details:

- Name, domicile and purpose of the foundation

- Date of formation and duration of the foundation, if the latter is established for a limited period

- Details on the foundation board

- Details on the statutory representative

- Confirmation that the tangible beneficiaries, or beneficiaries identifiable on the basis of objective criteria, or the category of beneficiaries have been designated by the founder, unless this is already evident in the purpose of the foundation

- Confirmation that the foundation is not intended entirely or predominantly for common-benefit purposes

- Details as to whether the foundation is to be subject to supervision in accordance with the foundation deed

- Confirmation that the statutory minimum capital is freely available to the foundation

In accordance with § 24 Para. 2 StiG the foundation board of foundations established under the new law must comprise at least two members, whereby legal entities are also permitted to act as a member of the foundation board. This provision applies only to foundations established after 1 April 2009, i.e. existing foundations with only a single foundation board member do not have to appoint additional members. In the absence of any provision in the statutes to the contrary, the period of office for members of the foundation board is limited to three years, although they can be re-elected.

In addition, an attorney, trustee or holder of an authorisation under Art. 180a PGR, licensed to practise in Liechtenstein, must confirm that the notification of formation is correct. Details of this requirement, particularly regarding the need for independence on the part of the confirming party, will be defined through an ordinance.

Provision has been made for criminal sanctions to be applied for false details being given in the notice of formation through negligence or wilful intent.

4.2. Notification Of Amendment

Any subsequent amendments to facts contained in the notification of formation submitted to the Public Register must be notified to the authorities within 30 days by way of a notification of amendment. Likewise, should grounds for liquidation arise in accordance with § 39 Para. 1 StiG, these must be notified within 30 days by way of a notification of amendment. These grounds include e.g. the resolution passed by the foundation board to wind up the foundation as a result of it having fulfilled its purpose or if bankruptcy proceedings have been initiated against the assets of the foundation.

If relevant amendments in existing foundations established under the old law occur after 1 April 2009, these must also be communicated to the authorities via the new notification of amendment system. According to Art. 1 Para. 3 of the transitional provisions in respect of the StiG, a request may be made that the copies of the statutes of foundations established under the old law which have been deposited with the Office of Land and Public Registration be returned as soon as a notification of amendment for these has been submitted for the first time to the new foundation supervisory authority.

The notification of amendment must also be confirmed as correct by an attorney, trustee or holder of an authorisation under Art. 180a PGR, licensed to practise in Liechtenstein.

5. CHARITABLE FOUNDATIONS

5.1. Definition Of Charitable

With the introduction of Art. 107 Para. 4a PGR the legislature has created a standardised definition of the term charitable which applies over and beyond foundation law to other areas of Liechtenstein company law. The core of the terms charitable and charitable activity is to be understood to include purposes whose pursuit enhances the common good. Under Art. 107 Para. 4a PGR this applies in particular if the activity "serves the common good in a charitable, religious, humanitarian, scientific, cultural, moral, sporting or ecological sense, even if only a specific category of persons benefits from the activity".

5.2. Mandatory Registration And Supervision

The new foundation law introduced the creation of an independent foundation supervisory authority which is attached to the Office of Land and Public Registration in accordance with § 29 Para. 2 StiG.

Under § 14 Para. 4 StiG all foundations with entirely or predominantly common-benefit purposes as well as those private-benefit foundations which pursue a commercial business on a special statutory basis, are required to register and only come into existence after they have been recorded in the Register.

Charitable foundations as well as foundations which voluntarily agree to supervision are subject to regulation by the foundation supervisory authority in accordance with § 29 StiG and require auditors appointed by the court. For foundations with minimal assets or for other reasons, the foundation supervisory authority may, by way of exception, dispense with the need for auditors to be appointed and conduct the corresponding audit activities itself. Further details on this will be set out in an ordinance by the Government.

As part of its supervisory functions the authority will verify whether the foundation assets are being managed and used in accordance with the designated purpose or not. If breaches are identified, the foundation supervisory authority must, as part of its notification obligation, contact the judge who can take the necessary measures by way of non-contentious proceedings. The authority does not itself possess any powers with regard to reorganisation or sanctions.

In addition, based on the notification of formation, the authority will examine whether the relevant details have been provided for the deposit of private-benefit foundations and whether there is any need for supervision because an allegedly private-benefit foundation is to be regarded as entirely or predominantly for common-benefit purposes. Furthermore, based on the purpose of a foundation stated in the notification of formation, the foundation supervisory authority will verify whether the purpose may have to be categorised as being unlawful or immoral and if necessary will order the corresponding foundation to be wound up

5.3. Discretionary And Mixed Foundations With Charitable Elements

The question as to whether a foundation is subject to Government supervision is not an easy one to answer in the case of mixed or discretionary foundations. In § 2 Para. 2 StiG the legislature has chosen a relatively strict approach. In this context two basic statements are of significant importance: on the one hand, in the case of mixed foundations, the question as to the predominance of the proportion of private-benefit or commonbenefit purposes "is to be assessed according to the relationship between services provided to serve private-benefit purposes and those serving commonbenefit purposes" (wording of § 2 Para. 3 StiG). In the future particular attention will therefore have to be paid both to the percentage allocation of the beneficial interest as well as to the proportional number of beneficiaries of a charitable nature if the intention is to prevent private-benefit foundations from being categorised as a "predominantly charitable foundation".

On the other hand, the legislature passed the new rule that, in the case of foundations for which it is unclear whether they are at a specific point in time predominantly for private-benefit purposes, it will be assumed that they are for common-benefit purposes. This applies in particular to the so-called discretionary foundations which in practice very frequently only nominate classes of beneficiaries on a general basis (e.g. non-specified issue within a family) and often list not only potential beneficiaries for private-benefit but also commonbenefit purposes (e.g. for the purpose of achieving the complex status under US tax law). If no weighting of interests has been applied here then there is the possibility of the new foundation law to assume a common-benefit purpose and consequently that Government supervision should apply. This can be countered by clearly setting out in the statutes or by-laws that the foundation is to be regarded in any event as predominantly for private-benefit purposes and that the foundation board must take this accordingly into account at its discretion.

Additional importance is attached to the above-mentioned issue by the fact that this re-assessment and the resulting consequences will also apply to all active foundations established under the old law. Consideration will have to be given to corresponding adjustments, particularly in the case of discretionary foundations.

6. BENEFICIARIES AND THEIR RIGHTS

6.1. Types Of Beneficiaries

Under § 3 StiG it is the beneficiaries, in addition to the governing bodies and the founder, who are the key participants in the foundation. In this context the new foundation law draws a distinction between the following types of beneficiaries:

- Entitled beneficiaries

- Prospective beneficiaries

- Discretionary beneficiaries

- Ultimate beneficiaries

Beneficiaries can be natural persons or legal entities who enjoy or can enjoy an economic benefit derived from the foundation. The beneficial interest can be granted either with or without consideration, conditions or specific prerequisites, it can be for a limited or unlimited period, conditional or unconditional as well as revocable or irrevocable.

6.2. Beneficiaries With A Legal Claim

6.2.1. Entitled Beneficiaries

Entitled beneficiaries are in the strongest legal position. They have a legal claim to a benefit, to a specified or determinable extent, arising from the foundation assets or foundation proceeds, based on the statutes, by-laws or regulations. Unlike discretionary beneficiaries or prospective beneficiaries, their claim is neither subject to a time-related or other type of condition, nor is their benefit at the discretion of the foundation board or another appointed governing body. Their claim is clearly defined and unconditional.

6.2.2. Prospective Beneficiaries

Prospective beneficiaries take the position of an entitled beneficiary after the occurence of a condition precedent or once a specific date has been reached. It is only from this point in time onwards that they have a legal claim to a benefit arising from the foundation.

A classic example of this is second beneficiaries who succeed the first beneficiary in his/her absence. Their claim to succession as entitled beneficiaries is based on statutes, by-laws or regulations.

6.3. Discretionary Beneficiaries (Beneficiaries With No Legal Claim)

The discretionary foundation, inspired by the discretionary trust and the concept of asset protection, has increased massively in importance over recent years. It is therefore only right and fair that the legislature has taken this situation into account by giving it corresponding consideration within the new foundation law.

A discretionary beneficiary under § 7 StiG is someone "who belongs to the category of beneficiaries specified by the founder and whose possible beneficial interest is placed within the discretion of the foundation council or another body appointed for this purpose". The two criteria therefore are the requirement for an individual to be listed as a potential beneficiary and simultaneously the decision on the timing or extent of an actual distribution has been assigned to the foundation board or a protector, collator or other governing body.

Under § 7 Para. 2 StiG the legal claim of the discretionary beneficiary to a specific benefit arising from the foundation assets or foundation income proceeds shall "in any event not come into being until there is a valid resolution by the foundation council, or another executive body vested with this responsibility (§ 28), on an actual distribution to the relevant discretionary beneficiaries and such claim shall lapse on receipt of this distribution".

The prospective beneficiary entitled to a discretionary beneficial interest is explicitly excluded from the class of discretionary beneficiaries in § 7 Para. 1 StiG and consequently from the participants in the foundation in general. These would be e.g. persons who, according to the founder, are intended to be included only within the class of discretionary beneficiaries after reaching the age of 30, or charitable institutions which have been put forward to the foundation board for selection as potential beneficiaries following the death of the first beneficiary. The new foundation law clearly sets out that the prospective beneficiary who is entitled to a discretionary beneficial interest shall not be included among the actual beneficiaries. This has particular consequences for the right to disclosure and information for this type of participant in the foundation: these "future discretionary beneficiaries" have no entitlement to disclosure or information by the foundation board.

6.4. Ultimate Beneficiary

The term "ultimate beneficiary" has now also been included in the foundation law. The provisions relating to the ultimate beneficiary detail in precise terms the situation in the event of the foundation being terminated through liquidation. The possibility to nominate an ultimate beneficiary should provide the founder with an alternative to the provision of § 8 Para. 2 StiG under which any assets remaining after liquidation will pass to the Liechtenstein state in the absence of any rule to the contrary. If the founder decides against exercising this option then under § 8 Para. 2 StiG the assets will pass to the Liechtenstein state. It should be noted at this point that under the statutes or by-laws the ultimate beneficiary in the event of a regular termination of the foundation through the passing of a winding-up resolution, in other words e.g. a third beneficiary, is not per se the ultimate beneficiary as understood by § 8 StiG.

6.5. Rights Of The Beneficiaries To Disclosure And Information

The prevailing subject of discussion worldwide on matters relating to company law is that of corporate governance. In recent years this has also led to the development of basic principles of foundation governance. It was the aim of the legislature to also adopt these contemporary basic principles of foundation governance into the new foundation law. This applies in particular to the monitoring of the foundation management by the beneficiaries. Within the new foundation law, the legislature decided to conclusively standardise the rights of the beneficiaries to disclosure and information, which had previously existed on the basis of the cross reference to the Law on Trust Enterprises in accordance with the previous Art. 552 Para. 4 PGR in conjunction with § 39 TrUG, by abolishing the reference to the TrUG and taking into account the established practice of the country's highest court over recent years.

Under the new foundation law all participants in the foundation designated in § 5 Para. 2 StiG as "beneficiaries" have the rights to disclosure and information in accordance with §§ 9 ff. StiG. Under § 9 Para. 1 StiG these rights encompass the entitlement "to inspect the foundation deed, the supplementary foundation deed and possible regulations". Moreover, under § 9 Para. 2 StiG the beneficiary "is entitled to the disclosure of information, reports and accounts".

The new foundation law also contains no obligation on the part of the foundation board to automatically inform the beneficiaries of their beneficial interest. This in itself represents a certain relativisation of the rights to disclosure and information which leaves it to the discretion of the founder to decide whether he/she wishes to inform the beneficiaries on their position.

6.6. Restriction Of The Beneficiary Rights

6.6.1. To The Legal Claim Of The Respective Beneficiary

The main restriction affecting the rights of beneficiaries to disclosure and information is first of all the wording in § 9 StiG, repeatedly used, under which these rights only have to be granted to a beneficiary "insofar as his rights are concerned".

Supplemented by the provision contained in § 9 Para. 2 StiG under which a beneficiary may only exercise his/her rights in such a way that does not contravene the interests of the foundation or those of other beneficiaries, this means that the information provided to a beneficiary can be restricted by the foundation board if there are indications that the beneficiary would use the information received to the detriment of all or individual other beneficiaries or intends to cause harm to the foundation.

6.6.2. For Important Grounds

In § 9 Para. 2 StiG the new foundation law, by way of exception, also provides for a restriction in the above-mentioned beneficiary rights, "for important reasons to protect the beneficiary". This is intended to counter e.g. a so-called "spoiling effect". In some cases, where beneficiaries of minor or young age are aware of the existence of foundation assets and their position as beneficiaries, there is danger that in the knowledge of and through exercising their rights they slacken in their endeavours to acquire an adequate education and live an independent life. A founder should therefore be permitted to deliberately refuse the rights of disclosure and information for such beneficiaries until they reach a certain age. There are other conceivable cases of serious due cause.

6.6.3. In The Event Of Reservation Of The Right Of Revocation And An Ultimate Beneficiary Position Of The Founder

If the founder has reserved for himself the right to revoke the foundation and simultaneously appointed him/herself as ultimate beneficiary then under § 10 StiG the beneficiaries have no entitlement to rights. If a foundation is formed by multiple founders, each of the founders for whom a right of revocation has been reserved is entitled to the beneficiary rights.

6.6.4. Through Appointment Of A Controlling Body

One key change compared with the old foundation law is represented by the introduction of a new optional governing body, the so-called controlling body under § 11 StiG. The founder can make provision for this governing body in order to limit the beneficiary rights to an irrevocable core area and at the same time to have the management of the foundation monitored by the controlling body. If a controlling body is set up the beneficiary only retains the entitlement to information relating to the purpose and organisation of the foundation as well as to his/her own rights towards the foundation. In order to verify the accuracy of the information the beneficiary can inspect the foundation documents; however, information which extends beyond this requirement may be blanked out. Where a controlling body has been established the beneficiary has no further entitlement e.g. to information on the foundation's total assets or of the names of other beneficiaries.

Provision for the controlling body must be made by the founder in the statutes. For foundations established under the old law, despite the fact that the statutes contain no provisions for this purpose, a controlling body can also be introduced subsequently and by way of exception by the foundation board up to 30 September 2009, albeit with restrictive conditions.

Under § 11 StiG the founder has three options available for appointing as controlling body: auditors, a confidant or the founder him/herself. Independence from the foundation must be guaranteed in all three cases. For both the confidant as well as the founder the same stringent requirements for independence apply as to the appointment of auditors as the controlling body. No family or other close ties with the foundation board or the foundation itself are permitted (position as beneficiary, relative of the family, employment relationship etc.).

Whilst auditors may only be appointed as the controlling body by the competent court based on two proposals, with the founder indicating his/her preferred choice, the nomination of a confidant or of the founder him/herself is made directly by the founder.

The new law demands certain qualifications of a controlling body. Whilst auditors are automatically qualified by the requirements of the profession, the confidant must also possess "sufficient specialist knowledge in the sphere of law and business" to be appointed as a controlling body. By contrast, the founder him/herself is not required to possess any qualifications other than independence.

The controlling body must conduct an annual review of the foundation's management and draw up a report for the attention of the foundation board. If the annual review does not give rise to any objections/complaints, this report can be limited to a brief certificate. If by contrast there are indications that the foundation assets are being managed or used by the foundation board in a way which is contrary to the purpose of the foundation, the controlling body must notify the beneficiaries whose details are known to it as well as the competent court. The court must then initiate the next steps in the process, e.g. revocation of resolutions passed by the foundation board or even dismissal of the foundation board and appointment of a new one.

On the basis of the above-mentioned formal regulations on the controlling body, the role of the protector, a familiar function in existing practice, cannot automatically be equated with that of a controlling body under § 11 StiG. Under the new law the classic protector is "another governing body" under § 28 StiG, which can undoubtedly carry out the monitoring of the foundation's management but has often also been assigned other organisational or co-determination rights.

It is for this reason that the appointment of a classic protector will also not effectively restrict the beneficiary rights. In contrast, it is certainly conceivable for the controlling body under § 11 StiG to be accorded additional duties over and beyond those required as a statutory minimum and for the controlling body to be nominated protector, provided the associated confusion of terminology is taken into account.

6.7. Non-Contentious Proceedings

In every case the beneficiaries have the right to initiate non-contentious proceedings in order to safeguard their rights. Provision had already been made for these proceedings in the previous law.

In the case of foundations which are subject to Government supervision the competent judge has the option, giving due regard to the presumed wishes of the founder, to amend the purpose of the foundation at the request of the foundation supervisory authority or the participants in the foundation. Other contents of the foundation documents, in particular that relating to the organisation of the foundation (i.e. foundation board), can be amended by the judge in the case of foundations subject to regulation at the request of the foundation supervisory authority or the participants in the foundation. This is first of all subject to the condition that the purpose of the foundation is maintained and secondly that the statutes do not grant a governing body of the foundation the power to make amendments.

In the case of foundations which are established for private-benefit purposes and not subject to supervision, under § 35 StiG the judge likewise has the power to carry out the necessary amendments to purposes or other contents at the request of the participants of the foundation or ex officio. In this context the same conditions apply as apply to foundations subject to supervision.

6.8. Need For Adaptation In Existing Foundations

If only the statutory provisions were to be taken into account when comparing the old with the new foundation law this could give the impression that the foundation reform has led to an extension of the rights of the beneficiary. However, if the established practice of the country's highest court over recent years is also taken into consideration then it is clear to see that this is not actually the case.

The legislature has only incorporated into the new law the existing beneficiary rights as defined by the practice of the court albeit a practice that frequently changes. The previous law itself had accordingly already viewed as unlawful the restrictions to the beneficiary rights as frequently allowed for in the existing by-laws, and in specific disputes granted the beneficiaries more far-reaching rights in spite of the attempted restriction in the by-laws.

The new clarity with regard to the definition of beneficiary rights under the new foundation law may prompt the need for an amendment of the regulations on beneficial interests in some foundations established under the old law. This must be examined on a case by case basis. For foundations whose allocations of beneficial interest are fixed in the by-laws and consequently where the foundation board is granted no discretion either with regard to the timing or extent of the distribution, it is virtually impossible to limit the rights of the beneficiary. The situation differs in those foundations where, although there are clearly specified first beneficiaries, the timing and extent of the distribution are left to the foundation board, if necessary in conjunction with a protector. These foundations are to be categorised as discretionary foundations, whose discretionary beneficiaries, defined under § 7 StiG as beneficiaries with no legal claim, have only limited rights to disclosure and information. In such foundations any second beneficiaries are to be regarded as prospective beneficiaries entitled to a discretionary beneficial interest and, as explained, have no beneficiary status nor any rights to disclosure and information under § 7 Para. 1 StiG. The situation is even clearer for pure discretionary foundations in which the foundation board can choose from a number of different, potential beneficiaries and grant the latter restricted rights only. Here again, other potential, lower ranking beneficiaries have no legal status based on the provision of § 7 Para. 1 StiG.

7. PRINCIPLE OF RIGIDITY

The aim of the new foundation law is to increase the founder's level of responsibility; this is also reflected in the consolidation of the principle of rigidity. This is expressed amongst other things in the provision under which only the founder him/herself can define the purpose as set forth by the foundation declaration in the statutes and additionally in the by-laws. Under § 30 StiG he/she can also amend the purpose in the event of the existence of corresponding reservations. Although under § 31 StiG the power can be reserved for the foundation board or another governing body of the foundation to make amendments in respect of the purpose – and hence also in respect of the regulations on beneficiaries as a key element of the purpose – § 31 StiG simultaneously makes it clear that this far-reaching power to make amendments can only be exercised by the designated governing body of the foundation if the purpose "has become unachievable, impermissible or irrational or if circumstances have changed to the extent that the purpose has acquired a quite different significance or effect, so that the foundation is estranged from the intention of the founder". In the future a general power of the foundation board or a protector to make amendments to the regulations on the beneficiaries, will no longer be permissible.

Even where amendments to contents unrelated to the purpose of the foundation are made, the foundation board or another governing body entrusted with this task is required to fulfil the condition that there must be a "substantially justified reason".

For subsequent amendments to be linked with the corresponding wishes of the founder, it is recommended that in future, particularly in the case of discretionary foundations, greater use be made of the instrument of a "letter of wishes" from the founder which will be enclosed with the foundation declaration and can make the foundation board aware of the founder's intentions at a later date.

8. TRANSITIONAL PROVISIONS

8.1 Effective Date And Periods

The new foundation law and accordingly the Foundation Act (StiG) will come into force as Art. 552 §§ 1–41 PGR with effect from 1 April 2009. Art. 553–570 PGR, i.e. the previous foundation law, will simultaneously be revoked.

All existing foundations which have been established under the previous law and are subject to supervision by the foundation supervisory authority under the new legal status, e.g. based on their charitable nature, must be registered with the authorities by the members of the respective foundation board within six months of the new law coming into force. This means that for all charitable foundations – under the new definition accordingly also for mixed foundations with predominantly common-benefit purposes or an unspecified ratio between common-benefit and private-benefit purposes – as well as for all foundations which voluntarily agree to be subject to government supervision, a corresponding notification must be sent to the relevant authorities by 30 September 2009.

For all foundations which are regarded as being of a charitable nature under the new law or which pursue a commercial business on a special statutory basis and have not yet been recorded in the Public Register, the foundation board must effect the registration within six months after the new foundation law comes into force, i.e. by no later than 30 September 2009.

All existing foundations which wish to exercise the new option to set up a controlling body and in this way limit the rights of the beneficiaries, despite there being no corresponding provision in their statutes, also have a six month period in which to do this. In the case of foundations established under the old law it is therefore permitted for a controlling body to be set up by the actual founder, or the foundation board if the founder has died or no longer has the capacity to transact business, by 30 September 2009. However, if it is the intention of the foundation board to exercise this right, the choice of the controlling body is restricted to auditors, whereas the founder by contrast can choose from all three options provided by law. If a controlling body is set up for foundations established under the old law, then under the transitional provisions the first audit to verify the correct and proper management of the foundation and use of the foundation's assets must be conducted by 30 June 2010.

8.2. Reorganisation Of Foundations Established Under The Old Law With An Insufficiently Specified Purpose

8.2.1. Periods

In order to finally resolve the issue of foundations which have been established under the old law and whose purpose is insufficiently specified, a long-standing subject of discussion and one for which a comprehensive ruling was issued by the State Court in 2003, the legislature has issued clear provisions in the new foundation law, in implementation of the above-mentioned ruling by the State Court.

All foundations which were formed prior to 31 December 2003 and whose purpose is still insufficiently specified, have time until 31 December 2009 to bring about the legal status as described in the new law. For foundations which have been formed under the old law but after 31 December 2003, the legislature assumes conversely that the founder or his/her legal adviser has already correctly applied the legal situation created by the ruling of the State Court and that there can be no requirement for reorganisation.

Under § 16 Para. 1 No. 4 StiG the task of defining a foundation's purpose involves in particular "the designation of tangible beneficiaries, or beneficiaries identifiable on the basis of objective criteria, or of the category of beneficiaries". This can continue to be carried out in the by-laws. If the purpose of a foundation is defined insufficiently in respect of the beneficiaries then the foundation is suffering from a lack of essential aspects and under the formal legal requirements has therefore not been established to legally valid effect. In order to avoid this the necessary attention would have had to be devoted to the sufficiently specified purpose at the latest since 31 December 2003.

Even if a founder has not reserved the power to make amendments in the case of foundations established under the old law, which were formed prior to 31 December 2003 and have an insufficiently specified purpose, the transitional provisions of the new law permit the actual founder to effect the corresponding reorganisational measures. If the founder is deceased or no longer has the capacity to transact then the foundation declaration can also be amended accordingly by the foundation board, provided the wishes of the actual founder can still be determined. It is only permitted to use documents which emanate from the founder, a representative who/which acted directly or indirectly at the time the foundation was formed, or a governing body of the foundation.

This rule is further tightened by the fact that, under Art. 2 Para. 3 of the transitional provisions, documents dated after the qualifying date of 1 December 2006 must emanate from the actual founder him/herself.

8.2.2. Mandatory Declaration Of The Legal Status Regarding Specified Purpose

In Art. 2 Para. 4 of the transitional provisions the legislature imposes a mandatory requirement on all foundations not recorded in the Public Register to issue an explicit declaration confirming the legal status of the specified purpose or that this status has been achieved. This declaration must be issued by 1 August 2010, otherwise the judge will be notified of the situation upon expiry of a six month grace period granted. The judge is required to liquidate the defaulting foundation in non-contentious proceedings.

8.3. Applicability And Consequences For Existing Foundations Under The Old Law

The transitional provisions expressly define which provisions of the new law are to be applied to foundations established under the old law. Moreover, the government has issued explanations which define additional provisions as law to be indirectly applied.

Essentially, the following are therefore to be applied directly or indirectly:

- the new definition of common-benefit purpose and the definition on the distinction between private-benefit and charitable foundations (Art. 107 Para. 4a PGR, § 2 StiG, § 29 StiG, ordinance to the StiG)

- the definition of the participants in the foundation (§ 3 StiG)

- the categorisation of the beneficiaries (§§ 5–8 StiG)

- the provisions on the rights of the beneficiaries to disclosure and information (§§ 9–12 StiG)

- tasks and characteristic features of the controlling body (§ 11 StiG)

- the new system of notifications of formation and amendments (§§ 20–21 StiG)

- the provisions on auditors (§ 27 StiG)

- the supervision by the new foundation supervisory authority (§ 29 StiG and ordinance to the StiG)

- the powers of the governing bodies of the foundation in particular with regard to amendment of purpose and other content (§§ 31–32 StiG)

- the rights of the judge in non-contentious proceedings (§§ 33–35 StiG)

In practice this raises various questions relating to the application of the new law to foundations established under the old law. Whilst the aspect of the rights of the beneficiary purely represents a stipulation of the existing legal practice of the Supreme Court and therefore does not constitute any fundamental changes on a substantive basis, the strengthening of the principle of rigidity gives rise to a number of more difficult questions.

A rigid application of the principle of § 31 StiG, under which now only the actual founder can make amendments to the purpose and consequently to the regulations on beneficiaries, would conflict with many by-laws of existing foundations where the foundation board is certainly permitted to amend the by-laws and consequently the regulations on beneficiaries, in most cases with the consent of the first beneficiaries.

In the spirit of the principle of trust which is protected under constitutional law, as also laid down by the State Court in the above-mentioned ruling in 2003 on the lack of a specified purpose, one should be able to assume that the powers to make amendments which have been granted for existing foundations, will be retained.

9. ADAPTATION OF THE IPR IN RESPECT OF THE PROTECTION OF THE STATUTORY SHARE

The legislature took the reform of the foundation law as an opportunity to deregulate the act on international private law by making the protection of the statutory share subject not only to the statute on foreign personnel but also to the law applicable to the process of acquisition, i.e. in the case of the formation of foundations §§ 785 and 951 in conjunction with § 1487 ABGB. The grace period for the opportunity to contest the formation of a foundation or endowment on the grounds of curtailment of the mandatory inheritance or statutory share will therefore be reduced in each case to two years from the date on which the foundation is formed or the endowment occurred. Significantly longer periods, as provided for e.g. under the French inheritance law (30 years), are therefore reduced by the supplementary application of Liechtenstein law.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.