- within Finance and Banking topic(s)

- within Strategy, Transport and Antitrust/Competition Law topic(s)

The 2026 regulatory landscape for fund managers is dominated by initiatives arising out of the renewed focus on EU competitiveness following the 2024 Draghi and Letta reports and in the context of a challenging, volatile economic outlook.

EU initiatives targeting market integration, competitiveness, and simplification and harmonisation of the EU rulebook, are scheduled to be progressed, adopted or enter into force over the course of the year including AIFMD 2, the Sustainable Finance Simplification Omnibus Package and the follow-on amendments to SFDR, the EU Market Integration and Supervision Package, the Retail Investment Framework/Strategy, EU venture and growth capital funds reform and the rationalisation of the Benchmarks Regulation.

Similarly-focussed domestic initiatives are also planned as per the Central Bank of Ireland's (CBI) December 2025 roadmap 'Regulating and Supervising well – a more effective and efficient framework' which includes a H1 2026 commitment to a comprehensive review of the fund service provider framework and H2 2026 commitment to further standardisation and clarification of regulatory processes.

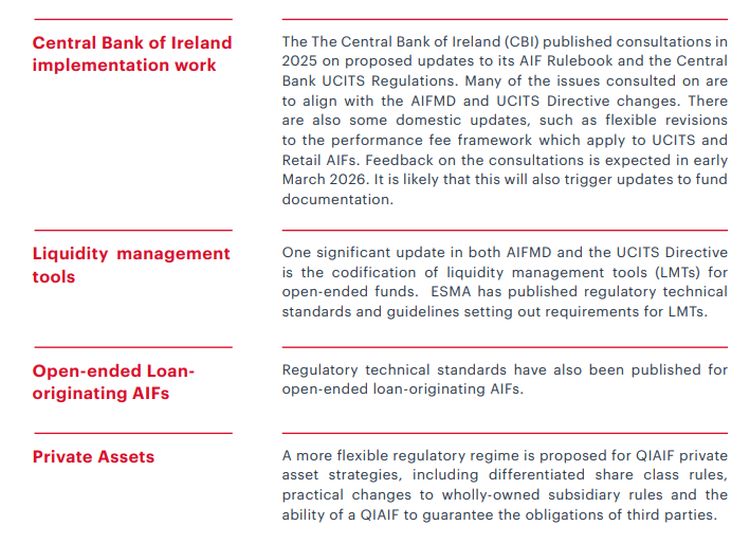

Domestic UCITS and AIF/AIFM regimes are also being updated, and final proposals are expected in the coming weeks following consultations in 2025 on revisions to the Central Bank UCITS Regulations and the AIF Rulebook.

In the near-term however, focus is on the 16 April 2026 deadline for updates to documentation, policies, procedures and controls necessitated by AIFMD 2 Level 1 amendments.

The following is a summary of expected developments in 2026. If you require support in relation to any of the topics outlined in this briefing, please contact a member of the William Fry Asset Management & Investment Funds department.

AIFMD 2

AIFMD and UCITS Directive Level 1 amendments are effective from 16 April 2026. Key changes to AIFMD include new requirements for loan-originating funds, enhanced liquidity management tools, more detailed delegation oversight, expanded reporting and disclosure obligations, and new rules on marketing by non-EU managers.

The UCITS Directive updates introduce harmonised liquidity management tools, enhanced reporting requirements and new rules on delegation.

Not every update to AIFMD / the UCITS Directive will be applicable to every fund management company and fund, however it is likely that every fund management company will need to make some updates to prospectuses, supplements, possibly constitutions and material contracts, and policies and procedures by 16 April 2026.

The expanded regulatory reporting obligations will not become effective until 16 April 2027. However, it is prudent to engage early in compliance preparations, particularly where input will be required from delegates or third parties.

Benchmarks Regulation

Amendments to the EU Benchmarks Regulation (amended BMR), effective 1 January 2026, reduce compliance obligations for funds referen cing or using benchmarks within the EU.

Under the amended BMR, use of non-significant non-climate benchmarks is no longer regulated as the scope of these rules is now limited to "critical" or "significant" benchmarks and certain climate-related and commodity benchmarks.

Where a UCITS has disclosure in its prospectus about benchmarks, these changes may result in updates to UCITS prospectus disclosure for benchmarks depending on the benchmarks used by the UCITS.

From 1 January 2026 onwards, fund management companies are required to regularly check the public register maintained by ESMA (or the European Single Access Point, when available) to verify the regulatory status of administrators for any benchmarks they plan to use.

CBI Standards for Business

The Central Bank Reform Act 2010 (Section 17A) (Standards for Business) Regulations 2025 were published in March 2025 (the BSR) and apply to regulated financial services providers from 24 March 2026. The definition of regulated entities in scope of the BSR is broad and therefore Irish authorised fund management companies and funds should carefully assess the extent of their obligations under the BSR.

The BSR set out mandatory principles for these firms under the Individual Accountability Framework. They are linked to the Central Bank's updates to its Consumer Protection Code and therefore the key objective is the protection of Irish retail investors.

These standards require firms to act honestly, fairly, and professionally, prioritising customers' interests and market integrity. They cover conduct, governance, risk management, transparency and mandate that firms operate with due skill, care, and diligence and avoid conflicts of interest. Some principles apply only in the case of consumers. Exemptions apply for certain activities, including MiFID services.

Funds Sector 2030 implementation plan

The Funds Sector 2030 Implementation Plan was published by Ireland's Department of Finance on 7 October 2025. The Implementation Plan operationalises the strategic recommendations from the Funds Sector 2030 Review, aiming to future-proof Ireland's investment funds industry and maintain its global competitiveness.

The implementation plan categorised the most substantive recommendations in 4 key areas: (1) to grow Exchange Traded Funds; (2) to grow private assets, including tax changes and measures to improve limited partnership offering; (3) to grow retail investment; and (4) to address risks and enhance transparency in structured finance, including progressing the implementation of the new EU AML package into Irish law.

A Roadmap is being developed, for publication in early 2026, which will set out a proposed approach to simplify and adapt the tax framework to encourage retail investment.

Central Bank of Ireland regulatory framework proposals

The CBI published "Regulating and Supervising well – a more effective and efficient framework" in December 2025. The proposals are to align with the European simplification framework and include cross-sectoral and funds specific proposals. The CBI will consult publicly on a new Regulatory Impact Assessment framework in 2026.

- Review the rules governing management companies and service providers, ensuring they reflect the structures and risk profiles of today's funds industry.

- Update delegation and outsourcing provisions, where necessary, to reflect AIFMD II and EU guidance

- Streamline and consolidate domestic regulations, guidance, and Q&As, reducing duplication and improving consistency across the funds sector (H1 2028).

The CBI has also committed to further standardising and clarifying its authorisation processes for funds, intermediaries, prospectuses, and market participants, including more consistent templates, clearer expectations upfront, and improved guidance, to enhance transparency, predictability and timeliness (H2 2026).

EU ESG Ratings Regulation

From 2 July 2026 any fund management company which issues a proprietary ESG rating and discloses that rating in marketing communications must include a link to a website where certain prescribed information on the ESG rating can be accessed by investors. Fund management companies using proprietary ESG ratings should conduct a review of their marketing materials to determine whether any reference to an ESG rating is included. For in scope entities, the required information will need to be disclosed on the fund management company website or ESG rating references removed from the marketing material.

Preparation for T+1 Settlement

Europe's transition to T+1 settlement is scheduled for 11 October 2027. It will apply to securities traded on EU venues and settled through CSDs. Asset managers, custodians, and central securities depositories (CSDs) must overhaul operational models to handle accelerated workflows. Europe is co-ordinating with the UK and Switzerland on the transition. The legislative proposal to shorten the settlement cycle was published in the EU Official Journal on 14 October 2025 for application on 11 October 2027. Level 2 measures have been proposed by ESMA to support implementation and enhance settlement efficiency across the EU. An Industry Committee has been established to support the move, producing a roadmap and proposing an operating timetable. Asset managers should begin to review and analyse existing trading processes during 2026 to identify any issues to be resolved in advance of moving to T+1 and give time for implementation and testing.

ESMA proposals for re-bundling research and execution payments under MIFID II

Upon its application on 3 January 2018, MIFID II only allowed payments for research by an investment firm (1) out of its own resources or (2) payments from a separate research account. In 2021, this was changed allowing joint payments for execution services and research covering issuers with a market cap of €1billion or less. Changes to the Listing Act Directive EU 2024/2811 approved in late 2024 have removed that market cap restriction.

Once the changes come into effect, an investment firm will have 3 payment options for research (1) out of its own resources (2) payment from a separate research account or (3) joint payments for research and execution services PROVIDED in each case that specific conditions are satisfied. The conditions are imposed and must be satisfied so that the provision of research is not regarded as an inducement.

Member States have until 5 June 2026 to introduce implementing measures and legislation to transpose the Listing Act Directive changes related to research and must apply the provisions from 6 June 2026.

Alongside this, a Delegated Directive supplementing MIFID (commission Delegated Directive EU 2017/593) is being amended to clarify the rules and conditions that investment firms must follow in using these 3 payment options for research. ESMA has issued a Final Report proposing these changes.

This is a welcome development for asset managers who wish to avail of bundled research, brokerage and other investment-related services. For asset managers of investment funds currently applying the "research unbundling" provisions in the context of Irish regulated funds and planning to move to joint payments, they will need to consider the provisions of the implementing legislation when it is published and examine existing fee and payment arrangements, contracts and disclosures.

SFDR 2.0

The European Commission's (EC) published its long-awaited SFDR 2.0 proposal on 20 November 2025. The proposed changes are radical, with a focus on simplification and introduction of 3 core product categories to replace the existing A8 / A9 disclosures. The European Commission opened a feedback period on 15 December 2025. The current deadline for feedback is 1 April 2026.

Feedback provided to the European Commission by this deadline will be summarised by the European Commission and transmitted to the European Parliament and the Council with a view to informing legislative discussions on its SFDR 2.0 proposal.

It is unlikely that any changes will be effective before the end of 2028.

Fund management companies should take the opportunity to review the SFDR 2.0 proposal and raise any pertinent issues during the consultation period.

The core product categories are ESG Basics, Transition and Sustainable. Impact can be an add on category to Transition and Sustainable. There is also the possibility for a combination version where a fund, such as a fund of funds, invests in other categorised funds. Details will be settled once the legislation, including any relevant Level 2 measures, is agreed and published.Fund managers can already begin to undertake an exercise mapping existing SFDR Article 8 and 9 products to the new product requirements to see if they will fall to be classified under the new product categories or whether any changes may need to be made to comply with the new product requirements.

Fund managers planning new products with sustainable features can also look to the SFDR product category proposals.

A detailed review of the proposal and product categories can be found here.

ESMA review of Compliance and Internal Audit functions

ESMA's 2026 work programme states that it will issue its report on the 2025 common supervisory action on Compliance and Internal Audit functions of UCITS Management Companies and AIFMs in Q2 2026. Fund management companies will need to review the report, assess any recommendations and take appropriate steps if necessary

To read this article in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.