- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- within Accounting and Audit, Strategy and Corporate/Commercial Law topic(s)

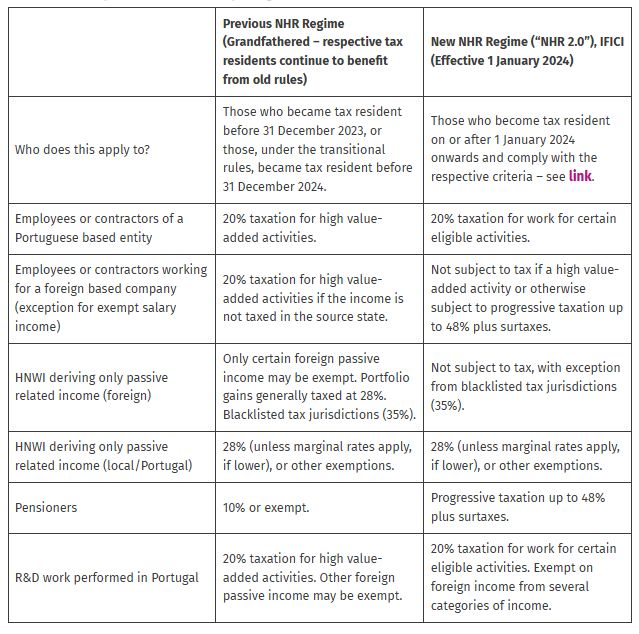

Taxpayers who are NHR (Non-Habitual Residents) or IFICI (Incentive for Scientific Research and Innovation) eligible, benefit from a package of respective tax advantages, for a period of 10 consecutive calendar years (with the option of utilising the marginal rates, if lower), from the effective date of Portuguese tax residency.

Summary of Tax Consequences Differentiating between the Previous and New NHR (IFICI/NHR2.0) Regime

I am part of the previous NHR – does this affect me?

As the previous NHR regime will be grandfathered (including those who become tax resident before 31 December 2024), there is no impact for individuals already enjoying NHR status. The regime will continue to exist until the 10-year NHR period is reached, from when each respective individual registered for NHR.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.