- within Employment and HR topic(s)

- with readers working within the Business & Consumer Services industries

FOREWORD - A drive towards $5 trillion economy

As the Modi Government 2.0 presents its first budget of the new decade, there have been a lot of deliberations around various measures that may be looked at for providing stimulus to the economy, means for meeting fiscal deficits, and addressing the NBFC liquidity issues, among other concerns.

Last year's path-breaking measures to alleviate economic concerns, such as the reduction of corporate tax rates and boosts for the export and real estate sectors, soared the expectations of the taxpayer fraternity in general for further relief measures.

The Finance Minister, in her second budget, discussed the vision of having a common goal of shared prosperity for the people of what is now the World's fifth-largest economy. Focusing on its four-wheel wagon of vibrant and dynamic economic development, liberalization and optimum utilization of technology, fundamental and structural reforms, and delivering ease of life, the Government continues to drive towards achieving its goal of a USD 5 trillion economy.

Dividing the budget into three broad themes of Aspirational India, Economic Development, and Caring society, a slew of measures have been proposed by the Finance Minister touching upon various areas, ranging from infrastructural development, improving healthcare and sanitization, addressing agrarian issues, rural development, education, and skill development.

On the direct tax front, reforms have been proposed towards the simplification of tax laws and the reduction of compliances to be undertaken. The introduction of the new personal tax regime is proposed to be in line with the relaxations offered to the corporates. Acceptance of the long-standing demand for removal of the Dividend Distribution Tax is definitely a welcome move.

The Government also seems to be committed to ensuring hassle-free and transparent litigation resolution, as it has sought to extend the faceless facility to appeals as well. Another key highlight in this area is the introduction of the 'Vivaad se Vishwas Scheme' to settle the litigation.

On the indirect tax front, acknowledging the contribution of Goods and Service Tax (GST) towards the structural reforms envisaged in the past, measures have been proposed to simplify and also automate the processes.

Overall, the budget is an optimistic one, especially considering the tightrope that the Finance Minister was to walk on. There are several positives emanating from the budget - Private Sector Focus, healthcare push, a strong impetus for consumption, agrarian focus, to name a few. While these moves are certainly in the right direction, with all the fiscal challenges, the real boost to the economy would depend upon the successful implementation of these measures in the times to come.

ECONOMIC OVERVIEW

GDP Growth

- The Union Budget announcement and the Economic Survey estimate the real GDP growth at ~5.0% in FY 19-20 (breaking up to 5.0% in Q1 and 4.5% in Q2), down from 6.8% of FY 18-19 as well as the provisional estimate of 7.2% for F 19-Y20 as estimated in the last budget session.

- The slowing trend is attributed to a general weakening of the supply side, as well as slow fixed capital formation. Government estimates show that demand on private final consumption and net exports have held the GDP growth.

- The current budget tries to improve the slowdown drivers, by giving policy impetus to improve private consumption, as well as enhancing physical infrastructure development, by embracing the PPP model.

- A rebound in GDP growth is expected from the Q1 of FY 20-21, and the expectations for FY 20-21 are positive, with an estimated GDP growth rate of 5.8% projected by the International Monetary Fund.

Index of Industrial Production (IIP)

- The IIP is estimated to have seen a modest growth of 0.6% in April-November 2019, compared to 3.8 % in FY18-19 and 4.4% for FY17-18.

- IIP for Manufacturing and Electricity sectors grew 0.9% and 0.8% respectively for April-November 2019 against 3.9% and 2.9% ins FY 18-19.

- The declining trend can be attributed to factors like the slow growth in the automobile industry and the plateauing output of the eight core industries (coal, crude oil, natural gas, refinery products, fertilizers, steel, cement, and electricity) that account for 40% of this index. More specifically, it is tagged to the contraction in production in the energy and refinery sectors.

Inflation

- Headline inflation, based on Consumer Price Index – Combined (CPIC) rose to 4.1% in April-Dec 2019, up from a three-year declining trend (3.4% in FY18-19, 3.6% in FY17- 18, and 4.5% in FY16-17).

- Wholesale Price Index (WPI) inflation stood at 2.6% in December'19, averaging at 1.5% in April to December 2019. This is a welcome decline from the previous upward trend seen in FY16-17 to FY 18-19 (when it stood at an estimated 4.3%)

- Initiatives proposed in the Budget and over the last year targeting price stabilization on essential food items, trade and fiscal measures, supply chain improvements, etc. should bolster these indicators in the long run

Trade

- The Merchandise exports in April-Dec 2019 stood at USD 239.3 billion, declining 2% from the corresponding period in the previous year. This was moderated by the simultaneous decline of merchandise imports, which saw a negative growth of 8.9% in the same period, leveling down partly due to the reduced spend on crude oil (by ~11.8% valuing to ~USD 12.8 bn), due to the decline in oil prices.

- Policy exemptions and initiatives announced in the budget, and policies for local manufacturing (like the NIRVIK scheme for higher export credit disbursement) aim to drive exports.

- The net impact so far shows an improvement in the Balance of Payments, with the Current Account Deficit coming down to 1.5% in the first half of FY 19-20 (form 2.1% in FY 18-19).

- While the 'Assemble in India' concept introduced in the Economic Survey (as an extension to 'Make in India') was not elucidated in the announcement, if driven ahead over the year, it could play an important role in India's positioning as a manufacturing major.

Fiscal Deficit

- Revised estimates place fiscal deficit at 3.8% of GDP and revenue deficit 2.4% of GDP in 2019-20, while the budgeted estimate fiscal deficit for FY20-21 stands at 3.5%.

- In the recent policy statements, a strong emphasis has been placed on maintaining fiscal discipline, resulting in contained deviations from the targets in the preceding years. The policies use disinvestment as one of the routes of achieving this, and the execution of the IPO for the Life Insurance Corporation of India (LIC) is a noteworthy development.

- It is important to note that recent initiatives have shown a higher commitment towards the development of physical and transport infrastructure, which would bear fruit in the longer term.

Foreign Investments

- The net FDI in H1 of FY2019-20 stood at USD 21.3 billion. In this period, India's global ranking of the 'Ease of Doing Business', as published by the World Bank, went up by 14 positions to the 63rd rank in 2019. FDI Inflows in FY 19-20 (April-November) stood at USD 24.4 billion compared to USD 21.2 billion, a clear indication of the positive global outlook of India and belief in its growth story and reform strategy.

- The policy focus on infrastructure development, promotion of the PPP model in critical sectors like healthcare, investment in skill development, simplification and revision of the taxation structure, etc. are expected to stimulate FDI inflows into the economy.

Foreign Exchange Reserves and External Debt

- FY19-20 saw a higher accretion of foreign exchange reserves, which stood at USD 457.5 billion at the end of December'19 and reaching a historic high in January 2020.

- Focused campaigns to boost other avenues of income like tourism will be beneficial in boosting FOREX.

- External debt remains low at 20.1% of GDP, as at the end of September 2019. After the significant decline since 2014-15, India's external liabilities (debt and equity) to GDP ratio has increased at the end of June 2019. This is primarily driven by an increase in FDI, portfolio flows, and external commercial borrowings (ECBs).

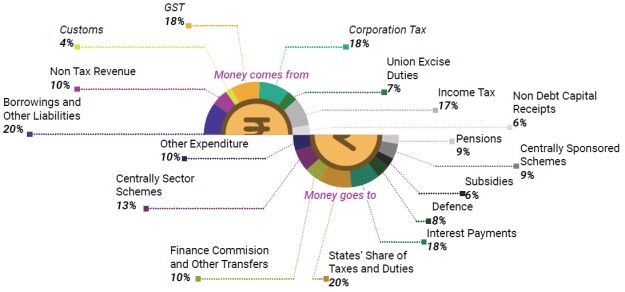

Source and Allocation of Funds

PERSONAL INCOME TAX

Tax Rates Changes

- The tax payer can follow the new regime, with reduced tax rates and no specified exemptions/ reductions or the tax payer can continue to follow the existing tax rate system. The rates according to both are as follows (Exclusive of surcharge and cess):

-

Income (INR) Existing Tax rate* Under new regime (optional) Upto 250,000 NIL NIL From 250,001 to 500,000 5% 5% From 500,001 to 750,000 20% 10% From 750,000 to 1,000,000 20% 15% From 1,000,001 to 1,250,000 30% 20% From 1,250,001 to 1,500,000 30% 25% Above 1,500,000 30% 30% - *For Resident Individual having (a) age of 60 years to less than 80 years, the income up to INR 300,000 is non-taxable and (b) age from 80 years and above the income up to INR 500,000 is non-taxable.

- Under the new regime, individuals and HUFs have to forego all deductions and exemptions such as standard deduction, interest on housing loan, PPF and other 80 C investments, Mediclaim, etc. and can only get a deduction in respect of employees' contribution to pension scheme and a deduction in respect of employment of new employees.

Amendments in residency rules

Currently, an Indian citizen, employed overseas, will be considered as a resident if his stay in India amounts to 182 days or more. Now, this duration is proposed to be reduced to 120 days.

It is now proposed that an individual or HUF will be considered as "not ordinarily resident" in India if he has been a non-resident in India in seven out of ten years preceding that year.

It is proposed that an Indian citizen who is not liable to tax in any other country by reason of domicile, residence, etc. would be deemed to be a resident of India and thus, their global income would be taxable in India.

Cap on tax benefits available for Provident Fund, Superannuation Fund and National Pension Scheme

- Under the current tax regime, the employer's contribution to Recognised Provident Fund (RPF) up to 12% of salary, Superannuation Fund (SF) up to INR 150,000 and National Pension Scheme (NPS) up to 10% of salary is not taxable in the hands of the employee. However, there is no cap on the overall amount of exemption claimed by the employees with respect to these three funds.

- It is now proposed to provide a combined upper limit of INR 0.75 million in respect of employer's contribution in a year to RPF, SF and NPS, and any excess contribution is proposed to be taxable. Consequently, it is also proposed that any annual accretion by way of interest, dividend or any other amount of similar nature during the previous year to the balance at the credit of the fund or scheme will also be considered under the umbrella of total employer contribution."

Our Comments

- The personal tax rate changes seem attractive at first blush, but it may turn out to be undesirable if an individual avails various deductions and exemptions. Infact, the current tax regime would be more beneficial. Under the pretext of simplification of taxes, the government has granted every citizen the means to compare both taxation regimes to make an informed decision.

- For Indians employed/living overseas, the reduction in duration of stay in India from 183 to 120 is adverse for people making frequent visits to India or staying in India for an extended duration.

- The deemed residency for Indian Citizens residing in countries where they are not liable to tax is a significant departure from the erstwhile regime of determining residency based on the number of days of stay. Indian citizens who have gone abroad for employment or business, especially to Middle East countries where there is no tax, will face now tax consequences in India and also have to undertake compliances in India.

- The cap on the employer's contribution to various social security schemes provided considerable benefits to employees earning high salaries, which now would be adversely impacted.

Click here to continue reading ...

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.