- in United States

- with readers working within the Media & Information and Law Firm industries

- within Transport, Strategy, Litigation and Mediation & Arbitration topic(s)

1. INTRODUCTION

One of the better reasons for which the year 2020 will be memorable, is the resurgence in the rise of SPACs in the US. 'Special Purpose Acquisition Companies' or "SPACs" as they are more popularly known, were the buzzword in the American financial markets in 2020, with SPACs raising a record USD 83 billion with an average of nearly USD 335 million per listing for 248 listings. For comparison, in 2010, SPACs only managed to raise about USD 503 million with an average of only about USD 72 million per listing for 7 listings. 2021 is set to break these records, with 166 deals already in the offing.1

Though SPACs are dominating headlines now, they have actually been around since the 1990s in the USA in the technology, healthcare, logistics, media, retail and telecommunications industries attracting interest from primarily institutional investors. Initially, SPACs had a reputation for taking greenhorn companies public, resulting in high rates of failure and low stock prices, all at the expense of investors. However, with the backdrop of funds needed to be raised by companies for working capital, and also to provide exits to existing investors, companies are increasingly looking towards the bourses. The Covid-induced volatility in the stock market however was proving to be a dampener in this quest for liquidity since companies are unsure of the quantum of funds that will be raised and the price at which funds will be raised. Consequently today, SPACs are commonly emerging in various sectors including consumer goods, energy, construction, financial services, healthcare and other technology-driven services, media, sports and entertainment sectors.

In a nutshell, SPACs are shell companies which are already listed in the public market with no business operations, sponsored by experienced investors/ management, formed with the purpose of merging or acquiring other operational businesses within a specified timeframe. SPACs can be considered as a 'reverse-IPO' route, because while traditionally a company seeking to go public would undergo a lengthy listing process after justifying its business proposition to the public market regulator, here, the operating company gets acquired by a company which is already a listed company. It is for this reason that SPACs have earned the monikers of 'blank-cheque companies', 'blind shell companies', 'blind pools' or 'public shells'.

For growing companies based in emerging jurisdictions, and with the right investment team backing them, SPACs are an attractive option to get listed abroad and get access to public market funds, without the extended time period, protracted process, price uncertainty and regulatory baggage that listing in one's native jurisdiction may entail, and the additional uncertainty and hassle of going through the conventional direct listing route. Sponsors of SPACs collect a large fee (also referred to as 'promote') for their involvement, which largely remains intact even if the stock price falls post-listing. Institutional investors are entitled to redeem their shares if they don't approve of the target company.

Being part of one of the biggest emerging economies in the world, Indian companies have not escaped the eyes of seasoned private equity investors - prominent examples of Indian companies which have listed abroad through the SPAC route include online travel agent Yatra in 2016 and Videocon DTH.

These examples may seem few and far in between, but the SPAC trend is steadily approaching Indian shores, with ReNew Power having just entered into definitive agreements for acquisition by a SPAC at a valuation of almost USD 8 billion2, and reports of online car rental company Zoomcar3 and online grocer Grofers4 also exploring the SPAC route. With more investors training their binoculars towards the subcontinent, we examine SPACs as an acquisition route from an Indian regulatory and feasibility standpoint.

2. SPAC MECHANICS AND REGULATORY ISSUES

2.1 US Regime

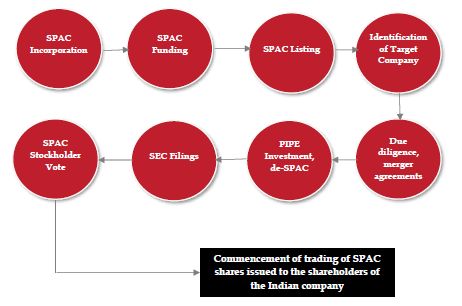

Typically, a SPAC is formed by an experienced team of investors, which follows the traditional IPO process of registering with the US Securities and Exchange Commission ("SEC"), filing prospectuses, and conducting investor roadshows (similar to an IPO roadshow, but potential investors are sold the capabilities and experience of the SPAC team instead of the company itself) to raise the initial capital for the SPAC.

At the time of seeking registration/ public company status, the SPAC is not an operating company - it is marketed as a shell company looking to acquire a single, or multiple companies in a similar sector, which may be spread across jurisdictions. The company responds to SEC's comments, seeks underwriters and prices the IPO, culminating in the listing of the SPAC. Getting a SPAC listed is a relatively easy process compared to a traditional IPO, given that it has no history or operations to disclose.

SPAC funds raised from the investors are placed in a trust account to earn interest until they can be deployed to purchase the target businesses. In order to release funds from the SPAC's trust account, an affirmative vote of its stockholders is required. Generally, SPACs have a timeframe of around two years to acquire their target companies (called the "de-SPAC" transaction), pursuant to which the shareholders of the target companies acquire units of the SPAC in exchange for their shares in such target companies.

Typically, there are two routes through which a SPAC can acquire its target - one is where the SPAC directly merges/acquires an existing operational company, and the other is where the SPAC merges with a pooling entity which acquires a single or a group of operating companies.

After successful listing, the SPAC commences the task of identifying potential targets and entering into definitive acquisition/ combination agreements with them. This involves due diligence on the targets and negotiating acquisition agreements. Typically, the cost of acquisition/combination of the target entity would be higher than the amount raised by the SPAC through it listing process. This shortfall is bridged by the SPAC raising financing from institutional investors (through "PIPE" - private investment in public equity). One consequence of raising investment through PIPE route is that the promote payable to the sponsors of the SPAC gets diluted.

Once the target company is identified, diligence processes have been completed and the necessary documentation has been negotiated and finalized, the SPAC submits the proxy statement giving detailed disclosures associated with the proposed business combination (equivalent of a prospectus in a general IPO) with the SEC. Then, the SPAC seeks its stockholders' approval for the proposed combination. Upon receiving SEC approval on the proxy statement and receiving stockholder approval, the de-SPACing transaction is completed, and the shareholders of the acquired companies become holders of listed stock. Certain members of the management team are typically subject to statutory lock-up restrictions under US securities laws (typically one year from the date of listing). In many cases, these lock-up restrictions are also agreed contractually and extended to certain other unitholders of the SPAC who acquire the SPAC securities pursuant to the de-SPACing process.

However, the SPAC's stockholders also have the right to vote against the proposed combination and seek redemption of the funds held in the trust account. Further, even if they vote in favour of the proposed combination, they are entitled to exercise their redemption right within a specified time period. This is one of the most significant risks that needs to be borne in mind while evaluating SPACs as potential exit structures.

2.2 Indian Perspective

Where an Indian company is looking to achieve indirect listing through the SPAC route, there are a number of structures that may be considered - these could be inbound mergers, outbound mergers and share acquisition (through cash and/or stock swap routes).

Inbound mergers (where the foreign company gets absorbed into the Indian company) and outbound mergers (where the Indian company is absorbed into the foreign company) necessitate procuring approvals from the National Company Law Tribunal or "NCLT", in addition to any sector-specific approvals which may be applicable. Approval from the Reserve Bank of India (the "RBI") are deemed to be given for such direct mergers if the companies involved follow the relevant foreign exchange regulations including the pricing guidelines, adhering to the limit of USD 250,000 per financial year for resident individuals as prescribed under the Liberalised Remittance Scheme ("LRS")5, compliance with overseas direct investment ("ODI") regulations for residents not being individuals, compliance with the RBI's regulations for branch offices, etc. The dependence on the NCLT process, compliance with LRS limits, ODI conditions, RBI's branch office regulations and the time involved in such process makes this option an unfavourable one.

A popular route that is commonly explored is that of a 100% share acquisition of the Indian target companies by the SPAC, where the consideration may be a combination of cash plus stock swap. The significant advantage of this route is that it does away with the lengthy NCLT process. However, an analysis of the relevant RBI regulations in relation to pricing guidelines, LRS restrictions for portfolio investors (RBI approval will be required if the remittance for foreign shares exceeds the USD 250,000 limit), requirement of an RBI approval for consummating a swap of shares by a resident, restrictions under the foreign exchange regulations on deferment of payment of consideration, and requirements under the ODI regulations for the Indian promoter group, is important while structuring an exit for the Indian promoter group and other India-resident shareholders.

In light of such regulatory restrictions, including that of obtaining RBI approval for swap of shares by resident shareholders, parties may consider certain alternative structures which satisfy both the commercial requirement of providing an upside to the India-resident shareholders and avoiding the hassle of approaching the regulators for approval for the de-SPACing event.

Generally, while evaluating whether SPAC is the right route for an Indian company to provide exits to its shareholders (which may include venture capital, private equity investors as well as India-resident individuals), in addition to the regulatory considerations, taxation aspects are also required to be examined in detail. For instance, the direct and indirect tax incidence on each of the shareholders of the Indian entity at the time of giving effect to the swap, at the time of the de-SPACing event, as well as the eventual sale of listed securities on the recognized stock exchange in the US, must be examined. Further, analysis and considerations regarding availability of treaty benefits to certain shareholders with respect to grandfathering provisions under the relevant tax treaties, are also essential elements in structuring a SPAC transaction.

In the Indian context, even though lawmakers are seeking to make direct listing of Indian companies on stock exchanges abroad easier from the perspective of compliance with Indian reporting and disclosure obligations6, a comprehensive regulatory framework in connection with listing of Indian companies abroad, is still lacking. Recently, in a consultation paper recently released by SEBI on Proposed International Financial Services Centres Authority (Issuance and Listing of Securities) Regulations, 2021, a framework for listing of shares by a SPAC in the International Financial Service Centre (currently present in Gujarat) has been contemplated. This is subject to fulfillment of certain conditions such as minimum offer size being USD 50 million, acquisition timeline for SPACs being 3 years extendable by 1 year, etc. It remains to be seen whether the framework that is finally approved will be attractive enough for SPACs to list in the IFSC in India rather than abroad.

3. CONCLUSION

Globally, SPACs have worked very well for: (a) sponsors who stand to gain even if the prospects of the target company dip after the IPO; and (b) institutional investors who are provided liquidity and a safety net. There is no denying that the SPAC boom will continue to dominate conversations about listing routes for Indian companies in the near future because of some of the advantages listed above.

While the SPAC path is not a currently well-worn one yet, companies intending to tread it will be keeping a close eye on any compliance/regulatory/tax issues that may crop up with the first wave of companies using this structure - and then, it is possible that the current trickle of companies listing using the SPAC route will turn into a flood.

Footnotes

1 https://spacinsider.com/stats/

5 https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=10192

6 www.mca.gov.in/Ministry/pdf/CompaniesSpecification2ndAmndtRules_22022021.pdf

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.