- within Insurance, Environment and Employment and HR topic(s)

(Attribution: Ravi Kant)

- How can Hong Kong and foreign insurers currently sell insurance to Mainland China?

Despite the COVID-19 pandemic, many Mainland residents find foreign insurance policies more attractive than those found in the mainland and continue to cross borders to get their hands on them.

Take Hong Kong for example. The Provisional Statistics of Hong Kong Insurance Industry in the First Quarter of 2020 released by the HK Insurance Authority shows that new office premiums in respect of policies issued to Mainland visitors amounted to $5.4 billion in the first quarter of 2020.

Despite their popularity, when mainlanders purchase HK insurance products, there is a unique set of risks associated with the agreement for all parties concerned. In 2016, the China Insurance Regulatory Commission (“CIRC” the predecessor of the China Banking and Insurance Regulatory Commission, “CBIRC”) issued a risk reminder for Mainland citizens regarding purchasing insurance products in Hong Kong. Specifically, it warned Mainland citizens that:

- Policies issued by Hong Kong insurers are not protected by PRC legislation;

- Risks of changes to PRC or other laws applicable to foreign exchange should not be ignored;

- There is uncertainty with regard to investment-kind policy yields.

Moreover, CIRC's warning included a notice for mainland insurance intermediaries. A special 2016 campaign was launched to crack down on the illegal promotion of Hong Kong policies in Mainland China. At least one Mainland insurance intermediary has been sanctioned for illegally promoting or selling foreign insurance products in the Mainland, see Shanghai Banking Insurance Regulatory Insurance Punishment Juezi [2019] No. 36.

Hong Kong insurers, for their part, face risks in navigating restrictions on the PRC's insurance market access. They are for the most part eager to provide their services to prospective Mainland clients in the PRC's thriving insurance market. However, like other foreign insurers, they cannot directly sell insurance products unless they have successfully established a joint venture or wholly foreign-owned enterprise (“WFOE”) insurance company in Mainland China.

- Why is the Insurance Connect Significant for HK and Foreign Insurers?

Through the Greater Bay Area Insurance Connect (the “GBA IC”) Shenzhen will become a unique foothold for Hong Kong insurers serving Mainland clients. The GBA IC allows them to provide post-sale services to Mainland policyholders thanks to unique insurance market access permissions granted specifically to Shenzhen. So far, what is known is that under the GBA IC , two service centers (the “Service Centers”) will be established in Shenzhen — plus one other city, to be determined — featuring “counters for Hong Kong insurers” (the “Service Counters”). The Hong Kong Federation of Insurers, the industry body in Hong Kong, will take the lead in renting office space in each of these two cities. HK-based insurers will then be allowed to set up Service Counters in these Service Centers to serve policy holders living in the Greater Bay Area (the “GBA”). This will allow GBA policyholders to pay premiums for their policies, and modify their personal details under their policies without entering Hong Kong.

Why is this significant? Shenzhen is increasingly sharing Hong Kong's role as a GBA financial hub. To understand how significant this step is, let's place this development in context.

Shenzhen already had more financial autonomy than other Chinese cities since it became China's first special economic zone (“SEZ”) in 1980 (see 1980 Guangdong Special Economic Zone Regulations 广东省经济特区条例).

Shanghai's dominant status as China's financial hub has not lessened Shenzhen's own ambitions as a financial services center. A month after Shanghai's stock exchange (the “SSE”) reopened, Shenzhen established its own in December 1990 (the “SZSE”). To this day the SZSE remains the only exchange in Mainland China besides the SSE. Note that since 2014, both have been connected with each other and Hong Kong through the Shenzhen/Shanghai-Hong Kong Stock Connect (the “Stock Connect”). More recently, in 2017, an announcement making Shenzhen into the “ first pilot city for the development and innovation of insurance” (Shenzhen Insurance Regulatory Commission (2017) No. 14, the SIRC Announcement) was promulgated.

In 2019, Shenzhen received additional consideration as a financial center after being designated China's “Model City” through the Opinions of the Central Committee of the Communist Party of China on Supporting Shenzhen's Pioneering Zone for Building Socialism with Chinese Characteristics (2019 Shenzhen Opinions, 中共中央 国务院关于支持深圳建设中国特色社会主义先行示范区的意见). Under para 5 of the Shenzhen Opinions, the Central Committee encouraged the city to promote interconnection and mutual recognition of financial products with Hong Kong and Macao's financial markets.

In line with the city's plans for financial reforms, an announcement from this year announcements shows Shenzhen is now set to become a “pilot city” for the development and innovation of the insurance sector in China. On April 24, 2020, the People's Bank of China, CBIRC, the China Securities and Regulatory Commission, and the State Administration of Foreign Exchange (“SAFE”) released the Opinions on Financial Support to the Construction of Guangdong-Hong Kong-Macao Greater Bay Area [Yin Fa 2020, N. 95] (the “ Financial Support Opinions”).

According to the Fiancial Support Opinions, Hong Kong and Macau insurers will be invited to conduct pilot operations in GBA cities, paving the way for the further opening up of China's insurance market. In addition, it will facilitate the GBA insurance business for HK/Macau insurers and facilitate GBA financial consumers' access to HK/Macau insurance products.

Actioning these earlier goals, the GBA IC therefore represents a concrete step towards greater market access for Hong Kong insurers. It builds on the Financial Support Opinions, the Shenzhen Opinions, and the SIRC Announcement on becoming a “pilot” city for insurance innovation and development. It is also a feather in Shenzhen's cap; putting these previous goals into practice is an important confirmation of the city's direction and its promise as an insurance hub.

Note that as stated, the new GBA insurance regime will not make market access much easier than before for HK capital. At present, it only refers to post-sale transactions. Nevertheless the GBA IC and its integration with, among others, the policies mentioned in the Financial Support Opinions, will certainly make the GBA a more attractive place for foreign capital.

(Attribution: Aline Nadai)

- How does Shenzhen now compare with Beijing and Shanghai for establishing an Insurance WFOE?

Market Access

When compared to Beijing and Shanghai, Shenzhen's market access reforms are leading and offer the greatest potential for preferential treatment for foreign insurers. This section examines Beijing and Shanghai's market access reforms, and then compares them with Shenzhen's new foreign investment regime.

Beijing

Recent measures build on Beijing's role as a China's financial management center and make the city a more favorable site for investing foreign capital in the financial services and insurance sectors. For one, Beijing is the only city in the comprehensive pilot project for the extensive opening-up of the professional services industry. In 2015, the State Council issued the Reply on Approving the Overall Plan for a Comprehensive Pilot Project in Further Opening-up of the Service Industry in Beijing Municipality (国务院关于北京市服务业扩大开放综合试点总体方案的批复, the “2015 Beijing Reply”), which allows Beijing to test a wide range of innovative opening-up policies. This Reply laid out the plans for the further opening-up of Beijing's service industry, whereby the establishment of foreign-funded professional health and medical insurance institutions would be supported. Since then, the State Council has issued two replies in 2017 and 2019 (the “2019 Beijing Reply”), with the latter putting forward a three-year plan for reform and encouraging professionals in finance to work in the city. These Replies indicate the national government's past and continued support for expanding Beijing's role as a financial services center.

Beijing has also been proactive in implementing more permissive rules on foreign ownership in the finance and insurance sectors. In June 2020, the Beijing Municipal Commerce Bureau published the Beijing Action Plan for New Opening-Up Measures (北京市实施新开放举措行动方案,the “Beijing Action Plan”), taking “further opening-up of the financial sector” as a “key task”. Regarding how to further open up the financial sector, the document clearly states that life insurance companies, together with securities companies, fund management companies and futures companies can be fully owned by foreign capital, and foreign insurance institutions can establish health insurance and pension companies in Beijing. Note however that this latter item, permitting full foreign ownership of insurance companies and their provision of pension and life insurance policies, is the implementation of China's new foreign investment policy as of April 1, 2020 (see our China and the GATS article). It is not a Beijing-specific policy pilot; rather this is expected to eventually be applied by all sub-national jurisdictions in China.

Beijing's airport districts are also set to become pilot areas for certain financial reform programs. Use of airports to this end is mentioned explicitly in the 2019 Beijing Reply. For Daxing Airport Free Trade District (Beijing), a list for institutional innovations is now available. The list contains 81 measures which involve nearly all governmental institutions responsible for the reform of the District. There are several innovation measures marked as “strong implementability” in the list, among them encouraging foreign investment in the financial sector.

Shanghai

Historically, Shanghai has been a pilot zone for testing market access liberalization for financial services. For a time, Shanghai was the only city where foreign insurers could operate (see China's first Schedule of Commitments to the GATS, 1994, and our analysis of China and its GATS insurance commitments).

The past decade has been no exception. When the Shanghai FTZ was founded in 2013, one of the opening up measures included providing special market access for foreign-invested specialized health and medical insurance institutions (as a testament to this pilot's success, such market access has now been extended to cover most of China). Shortly thereafter in 2014, the CIRC issued 2 notices on supporting the development of the Shanghai FTA, which included 11 measures in the insurance sector.1 A notable development, Shanghai was also the site for the WFOE insurance holding company in China, Allianz insurance, four years earlier than initially planned. As recently as August 2020, Tesla registered with AMR for its own insurance brokerage in Shanghai to support insurance policies for Tesla owners.

Within Shanghai, the city's Lingang area will be the site for important policies to encourage insurance investment going forward. Under the Lingang Measures, Shanghai will support foreign funds to set up holding or wholly owned life insurance companies (in addition to securities, fund management, and futures companies), as well as form joint ventures. In 2020, new policies regarding Lingang New Area (Several Measures for Comprehensively Promoting the Financial Opening and Innovative Development of Lingang Special Area of China (Shanghai) Pilot Free Trade Zone/全面推进中国(上海)自由贸易试验区临港新片区金融开放与创新发展的若干措施) take this development a step further. Paragraph 4, specifically, indicates additional support for market access for foreign insurers, with the government “[s]upporting the establishment of foreign-controlled or wholly foreign-owned personal insurance companies.” Moreover, a February 2020 circular encourages insurance asset management companies to set up specialized asset management subsidiaries in Shanghai (para 10), and opens the door to pilot the permitting of insurance funds to invest in gold, oil and other commodities on a trial basis in Shanghai. It also encourages, generally, insurance institutions to invest in science and innovation investment funds in the Lingang area (para 1) ( Yinfa [2020] No. 46).

Most recently, Shanghai has announced ambitious development plans for its Hongkou district, intending to replicate “China's Wall Street” along the North Bund waterfront to drive economic growth in the aftermath of COVID-19 (the “Hongkou Plan”). The development includes plans to attract 100 major companies, particularly in the finance sector, to the North Bund's Hongkou area. This follows an earlier March announcement that Shanghai authorities would strive to bring 40 new regional headquarters for multinationals into the city and further open up controlled sectors, including insurance, as a part of its post-COVID recovery plans.

Comparison with Shenzhen

Despite Beijing and Shanghai's support for reforming and opening up their financial services and insurance sectors, neither of these cities's commitments match the level of detail available in Shenzhen commitments. Nor do they appear to share the same promise as the GBA, and particularly Shenzhen, for insurers' current and future market access.

Many of the most promising elements in Shanghai's Lingang Measures and the Hongkou Plan remain non-specific. The provisions of Yinfa [2020] No. 46 are encouraging, especially for insurance institutions planning on investing in commodities or science and innovation. However they have not yet been put into action and more details are needed to properly weigh the effects of measure. The same can be said for the other measures within the Hongkou Plan, which are even more general.

For its part, Beijing has similarly sent encouraging signals that it intends to pilot market access schemes that are beneficial to foreign insurers, but concrete policies have yet to be put into place. The role given to airport districts for financial reform, in particular, is one to watch.

Comparing the three cities, we can now see that while each has sent strong signals in favor of piloting greater market access benefits for foreign insurers, Shenzhen leads the pack and may go the furthest distance in implementation. Through the GBA IC, the Shenzhen and GBA authorities are already implementing the Financial Support Opinions, Shenzhen Opinions, and SIRC Announcement policies to bring greater market access to foreign insurers, especially for insurers based in Hong Kong. Although Shanghai's expected Lingang pilots encouraging commodity, science, and innovation investments by insurers may end up being more preferable to insurance institutions with a strong interest in these sectors, Shenzhen still offers the most insurance-specific measures. Thus while the GBA IC is currently limited to post-sales services, placed in its proper context, it becomes clear that this is a greater priority for Shenzhen than for other cities and will be the first of many market access pilots to come.

Foreign Exchange

Among the three cities, Shenzhen's foreign exchange measures are the most encouraging. This section examines and compares the foreign exchange policies of Shenzhen, Shanghai, and Beijing in turn.

Shenzhen

Currency traders within the city limits of Shenzhen enjoy special foreign exchange privileges. Under the supervision of the People's Bank of China and SAFE, Shenzhen is the first mainland city to progressively liberalize the conversion of foreign capital into the Yuan. Expanded from the city's initial Qianhai district Free Trade Zone Yuan Convertibility Pilot to now extend across all of Shenzhen, this program moves the city away from the mainland's approval-based system. This allows settlement of exchanges within minutes, rather than hours. This is in line with the above-described Financial Support Opinions. The above-described 2019 Shenzhen Opinions also encourage Shenzhen's role in internationalizing the Yuan.

According to the Financial Support Opinions, there are other plans beneficial to the introduction of foreign capital generally. This includes facilitating cross-border capital pooling and the establishment of a bank account system integrating the Yuan and foreign currencies.

Most recently, in June 2020, SAFE further approved a reform to allow eligible banking institutions in Shenzhen to support mobile foreign exchange transactions for cross-border currency conversions (facilitating payments both for Chinese workers abroad and foreigners in China).

Shanghai

Shanghai will also begin experimenting with pooling foreign capital. Under the Several Measures for Comprehensively Promoting the Financial Opening and Innovative Development of Lin-gang Special Area of China (Shanghai) Pilot Free Trade Zone (the "Lingang Measures", 全面推进中国(上海)自由贸易试验区临港新片区金融开放与创新发展的若干措施), unveiled on May 8th, 2020, the Lingang New Area of the Free Trade Zone will pilot a cross-border capital pool.

Shanghai will also support foreign funds seeking to invest in pension management and wealth management firms in Lingang. Note that one of the five basic objectives of the Shanghai FTZ, when it was founded in 2013, was “[to] deepen opening up and innovation of the financial sector.” Lingang will also host an integrated account system for local and foreign currencies. Previously, multinational companies operating in China needed to open separate Yuan (managed by the People's Bank of China) and foreign exchange accounts (under the management of SAFE). This was a burden on capital collection and payment.

Beijing

Daxing Airport Free Trade District is one of the many recent examples of Beijing's foreign-exchange initiatives, and indicates that Beijing intends to compete seriously to become a favorable destination for foreign capital. In April, the Beijing Department of SAFE released the Implementing Rules on Foreign Exchange Reform of Daxing Airport Free Trade District (Beijing)( 中国(河北)自由贸易试验区大兴机场片区(北京区域)外汇管理改革试点实施细则). About 9 new measures in the foreign exchange sector are planned to be implemented in the Daxing Airport Free Trade District (Beijing), including allowing the implementation of facilitating services for the payment of foreign exchange income from capital account; relaxation of the requirements that the contract currency, withdrawal currency, and repayment currency for cross-border financing must be consistent; and simplification of the registration, modification and cancellation procedures relating to direct investment.

Comparison

After examining each city's regime, we can now see why Shenzhen's foreign exchange reforms are the most encouraging. While each city offers promises of preferential forex pilots going forward, Shanghai and Beijing's remain in the planning stages whereas some important foreign-exchange policies have already been successfully implemented in Shenzhen. Specifically, the completed Yuan convertibility pilot and SAFE's approval of mobile forex support in Shenzhen both remove significant burdens for transactions requiring foreign exchange within the city limits.

However, Shanghai's programs are not far behind. Its Lingang integrated local/foreign currency account system is a pilot to watch for, as is the expected Lingang capital pool.

Taxes

Shenzhen's tax environment appears to be the most favourable for foreign insurers considering entering establishing a headquarters in mainland China.

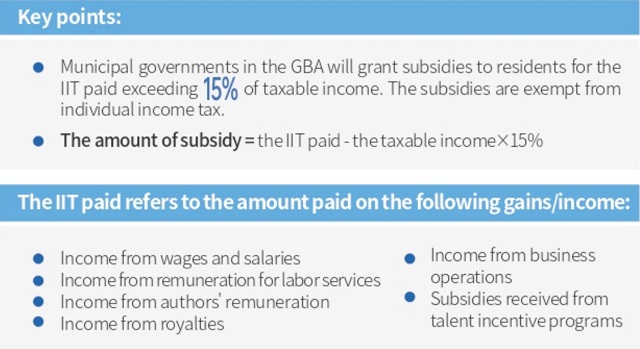

As a GBA city, Shenzhen benefits from Guangdong's preferential income tax policy for foreigners. The Ministry of Finance (MOF) and the State Administration of Taxation (SAT) issued Caishui [2019] No. 31 on March 14, 2019 (the “2019 GBA Circular”). The 2019 GBA Circular allows foreign talents working in GBA cities like Shenzhen to benefit from a tax rebate covering taxes in excess of 15% of their Individual Income Tax (“IIT”). The 2019 GBA Circular ends on December 31, 2023.

[Source: Department of Commerce of Guangdong Province, 2020 Invest Guangdong]

Measures for the other two cities are positive but non-specific. In Shanghai, there have been some generally favourable announcements applicable within the Lingang area, but they remain general in nature. Specifically, under No.6 (9) of the Lingang Measures, overseas high-end and urgently-needed talents working in Lingang will be allowed to benefit from certain IIT subsidies. A similar claim is made in the 2020 Shanghai Foreign Investment Guide (p. 59), which specifies that financial professionals are eligible for this subsidy, but otherwise does not provide particulars. Beijing, for its part, does not appear to have implemented or announced preferential IIT tax measures of this nature.

Shenzhen also benefits from Guangdong province's preferential foreign investment awards. On August 21, 2020, Guangdong issued the revised version of the Policies and Measures of Guangdong Province on Further Expanding Opening-up and Actively Attracting Foreign Direct Investment (Ten Policies and Measures for Foreign Investment). One enumerated incentive is an award (one-time) of 30% of a foreign investor's financial contribution made when establishing a regional or national headquarters within Guangdong. Beijing and Shanghai do not offer such an award.

Administration

The financial costs for WFOE formation will be similar across Shenzhen, Beijing, and Shanghai, although local requirements and processing standards may lead to slightly faster service depending on the city.

Across Beijing, Shenzhen, and Shanghai, some interactions with SAMR are moving online. In each of these cities, the Application Form for Foreign Funded Enterprises in China (在中国设立外资企业申请表) is being replaced by SAMR-administered online forms. For example, the Shanghai form (the “one window, one form”, exclusively in Chinese) is available on the Shanghai government's website.2 Similarly, Shenzhen has its own online portal,3 as does Beijing. This “one window, one form” policy is in line with a broader push by the Chinese government to improve the country's business environment and lessen bureaucratic red tape.4

Once the greatest hurdle is cleared, namely of getting approval from CBIRC, each city provides relatively similar processing times:

|

Statutory time limit (Working day) |

Promised time limit (Working day) |

|

|

Shanghai |

15 |

1 |

|

Shenzhen |

7 |

1 |

|

Beijing |

15 |

3 |

Note that when establishing a WFOE, an applicant must already have possession of an office address within the desired city at the time of application. Planning ahead on how to satisfy this administrative requirement will help avoid costly delays in company formation.

(Attribution: Matheus Natan)

Data

For data management and control, an important consideration for insurers entering China, the applicable laws are national. The Guidelines on the Information System Security Management of Insurance Companies(2011)/ 保险公司信息系统安全管理指引, together with the Cyber Security Law, apply with equal force in Beijing, Shanghai and Shenzhen.

As such data management rules should not be a factor in how a foreign insurer evaluates individual cities for its market-entry analysis.

Conclusion

For decades now, Beijing, Shanghai, and Shenzhen have attracted significant foreign investment in the financial and insurance sectors.

However, in light of Shenzhen's recent pilots and reforms, in particular the GBA IC, it is now the most favourable destination for foreign insurers seeking to establish a WFOE in mainland China. In terms of market access, foreign exchange controls, and tax policies, the city has shown the greatest level of initiative and implemented the greatest number of preferential policies that benefit foreign insurance institutions.

Nevertheless, this does not mean that insurers already based in Beijing and Shanghai should relocate to Shenzhen. Both Beijing and Shanghai have clearly demonstrated that they intend on piloting their own reforms in these areas. Additionally, as China's “Model City”, many pilots that succeed in Shenzhen are, eventually, well-received in other cities. Thus the above-described competitive advantages in Shenzhen may, relative to cities like Shanghai and Beijing, be temporary. That said, developing a dynamic and robust insurance sector is clearly a priority for Shenzhen, and its special support from both the state and provincial levels, combined with its proximity to well-established players in Hong Kong's own insurance sector, allow it to act on that priority in exceptionally promising ways.

Have questions about accessing China's insurance market? Anjie is a Chambers ranked, Band 1 law firm for PRC Insurance law, and has the largest insurance practice in mainland China

Feel free to send consultation requests to An Na (anna@anjielaw.com) or An Chencheng (anchencheng@anjielaw.com).

Footnotes

1 Please refer to: 1)Notice of the CIRC on Supporting the Development of the China (Shanghai) Pilot Free Trade Zone/保监会支持中国(上海)自由贸易试验区建设的通知

2) Notice of the General Office of the CIRC on Further Simplifying Administrative Examination and Approval to Support the Development of the China (Shanghai) Pilot Free Trade Zone/中国保监会办公厅关于进一步简化行政审批支持中国(上海)自由贸易试验区发展的通知

3) Administrative Measures of the China (Shanghai) Pilot Free Trade Zone for the Record-Filing of Insurance Institutions and Senior Management Personnel/中国(上海)自由贸易试验区保险机构和高级管理人员备案管理办法

2 Shanghai Municipal Government, “上海市开办企业 ‘以窗通‘网上服务”. Due to the presence of its free trade zone, Shanghai was able to pioneer online registration for companies doing business in areas not on the negative list before any other administrative area.

3 Shenzhen Municipal Government, “深圳市开办企业 ‘一窗通‘网上服务”, online: https://amr.sz.gov.cn/aicmerout/jsp/gcloud/giapout/industry/aicmer/processpage/step_prewin.jsp.

4 Dezan Shira & Associates, “Shanghai Business Registration: Online Platform for Foreign Invested Enterprises Launched” China Briefing, August 22, 2018, online: www.china-briefing.com/news/shanghai-business-registration-online-platform-foreign-invested-enterprises-launched/

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.