- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Oil & Gas and Construction & Engineering industries

Bennett Jones Spring 2016 Economic Outlook Brochure

This Spring Outlook has three sections. The first section sets out our view of the economic outlook commencing with a very short summary of recent world economy dynamics, followed by a review of the outlook for global growth and Canadian growth for 2016 to 2018. The second section examines the expected adjustment of the Canadian economy to the oil price fall of the last year and a half and discusses how productivity growth could be raised through strategic infrastructure investment in order to counter the effects of lower future terms of trade on Canadian real income. The third section analyzes likely global trade developments and their implications for Canada.

Section I: Global Short-Term Outlook: 2016-2018

Recent World Economy Dynamics

Global economic activity evolved quite unevenly early in 2016. A soft patch in the United States, which had started at the end of last year, persisted in the first quarter of 2016 as falling investment and exports continued to depress aggregate demand growth. Brazil and Russia experienced further severe contractions in the fourth quarter with adverse spillover effects on their regions of the world. On the other hand, growth in the first quarter resumed in Japan to reach 1.7 percent, accelerated to a relatively high rate of 2.1 percent in the Euro area, and remained about the same on an annual basis in China (6.7 percent).

The WTI oil price, which had halved to US$42/bbl in the 12 months up to November 2015, fell further to a trough of US$26 in mid-February, partly on concerns over the outlook for the global economy. The price recovered to close to US$50 at the end of May due in part to supply disruptions, and in part due to both a stronger than anticipated global demand and further depreciation of the U.S. dollar. These factors also supported some firming up of base metals prices this Spring.

The U.S. Federal Reserve raised its policy rate last December for the first time since 2008 and indicated then that further moves would be data dependent. A further ¼-point increase is now expected this summer. In contrast, the ECB, the Bank of Japan and the People's Bank of China loosened further their monetary policy stance in the first quarter in response to concerns about downside risks to their economies.

The Canadian dollar hovered around 75-76 U.S. cents in the three months prior to late November. The Canadian dollar then weakened to 70 U.S. cents on average in January before erratically rising to the 76-77 cent range at the end of May. This profile was attributable to two main factors: (1) the evolution of commodity prices, particularly oil prices which reached a low point in mid-February and then substantially recovered; and (2) expectations regarding the Canada-U.S. differentials with respect to economic growth and the future path of interest rates. Those expectations turned in favour of the U.S. at the end of last year and were validated by the rise in the U.S. policy rate in December. Subsequently, however, weak economic indicators led to lower expectations about U.S. growth and the prospects for further rises in U.S. interest rates. As a result, the U.S. dollar depreciated significantly on a multilateral basis from February until April. All in all, due to changing expectations with respect to central bank policy in the U.S., the Canadian dollar at the end of May appears to have been about two U.S. cents stronger than warranted by the expected level of oil prices alone.

Global Growth Outlook: 2016-2018

We project a "low for long" scenario with the global economy growing on average at about three percent per year from 2016 to 2018 the same as in the Fall 2015 Economic Outlook. In this scenario, projected global growth rates for both advanced and emerging economies are about the same as that achieved in 2015. U.S. growth is expected to be lower than in 2015, but this would be offset by slightly stronger growth in other advanced economies. Likewise, Chinese growth is expected to continue on its downward trend going forward, but this would be offset by firmer growth in other emerging economies, some likely to recover in part from recent severe recessions.

Several factors underpin our "low for long" scenario. First, for the advanced economies and several emerging economies, notably China, we take the view that potential output growth is and will remain lower than it was prior to 2008 due to less favorable demographic developments and productivity trends. Our projections for 2018 reflect slower labour force growth and the weak productivity performance experienced since 2010 which we project to largely continue for the remainder of this decade.

A second factor is that we do not anticipate that the stimulus to the world economy to be expected from relatively low oil prices will provide a significant boost to global growth going forward. Several factors have counteracted the expected positive response of global demand to this price shock in the last year and a half. Oil price declines have had a depressing effect on capital investment worldwide. In addition, slower growth of industrial production in China, continued deleveraging in some economies and generally low pass-through of spot oil prices to retail prices have reduced the anticipated positive impact of lower oil prices. Some of these factors may exert less restraint going forward, but oil prices are expected to partially recover over the next several years, thereby reducing their potential positive effect on global growth.

A third factor underpinning the "low for long" scenario is that the room for effective policy stimulus to prop up aggregate demand both in advanced and emerging economies is perceived as being quite limited. In advanced economies interest rates are now about as low as they can be, and the marginal effectiveness of taking further unconventional monetary policy measures in stimulating the economy is widely seen to be diminishing. Such measures may help support confidence and keep exchange rates competitive; but if at the end of the day they merely result in "competitive devaluation", they bring no net stimulus to the world economy. On the fiscal side, worries about the unsustainability of further increases in already high levels of deficit and/or public debt would prevent many governments (especially in Southern and peripheral Europe, Africa and Latin America) from putting in place significant stimulus packages. In the face of what is increasingly perceived as over-reliance on monetary policy to support aggregate demand and the reluctance of some governments (in particular Germany and the U.S.) to use expansionary fiscal policy even when there is room to do so, the IMF itself felt the need to recently state that "fiscal policy should be used flexibly to support aggregate demand, in particular in advanced economies."1

We project the WTI oil price to remain volatile and subject to supply disruptions. For planning purposes we suggest that the following assumptions be used: US$45-55 in the second half of 2016, US$50-60 in 2017 and US$55-65 in 2018. We note that substantial increases in shale oil supply are likely to occur once the WTI price reaches or exceeds US$60/bbl. This limits the upper end of the projected price range over the next two years.

Based on oil prices alone, we would expect the Canadian dollar exchange rate to trend upward. But expectations of Canada-U.S. differentials in growth and interest rates may undergo abrupt shifts over time as they are largely data dependent. We are inclined to think that the current "premium" on the Canadian dollar of about two U.S. cents noted earlier may erode somewhat if the U.S. economy performs better and the Federal Reserve starts raising its policy rate on a more sustained basis. Therefore we would expect the Canadian dollar exchange rate to fluctuate rather than to trend upward steadily as oil prices increase. For planning purposes, we envision the actual range of values to be 75-81 U.S. cents over the projection period.

Short-term Prospects for Output Growth (%)*

| Share (%) | 2015 | 2016 | 2017 | 2018 | |

|---|---|---|---|---|---|

| Canada | 1.5 | 1.1 (1.3) | 1.4 (2.0) | 2.4 (2.3) | 1.9 |

| United States | 16.4 | 2.4 (2.5) | 1.9 (2.6) | 2.3 (2.4) | 2.1 |

| Euro area | 12.3 | 1.5 (1.4) | 1.6 (1.5) | 1.6 (1.4) | 1.5 |

| Japan | 4.6 | 0.5 (0.6) | 0.8 (0.8) | 0.7 (0.7) | 0.6 |

| China | 17 | 6.9 (6.8) | 6.1 (6.0) | 5.2 (5.2) | 4.8 |

| Rest of the World | 48.2 | 2.7 (2.6) | 2.9 (2.9) | 3.2 (3.1) | 3.2 |

| World | 100 | 3.1 (3.0) | 3.0 (3.1) | 3.1 (3.0) | 2.9 |

*Figures in brackets are from the Bennett Jones Fall 2015 Economic Outlook.

U.S. growth weakened further from an already low 1.4 percent at annual rate at the end of last year to only 0.8 percent in the first quarter of 2016, with non-residential investment, exports and changes in inventories making the largest negative contributions to growth. We take the view that this is another of the soft patches that the U.S. economy has experienced since the last recession and that growth will rebound to 2.5 percent in the rest of 2016 and gradually diminish a little during the next two years. This would yield average annual rates of 1.9 percent in 2016, 2.3 percent in 2017 and 2.1 percent in 2018. This projection assumes status quo policies and is therefore subject to unusually large risks due to political uncertainty related to the outcome of the November presidential and congressional elections. There is much uncertainty about the programs that presidential candidates, especially Donald Trump, would and could effectively implement if elected.

Headwinds from earlier movements of the exchange rate and the oil price are expected to lose intensity as time goes by. Moreover, abstracting from political changes, status quo fiscal policy is projected to stop exerting a drag on growth in 2016. Even with expected small increases in rates set by the Federal Reserve, monetary and credit conditions would remain accommodative, supporting growth in household consumption and housing investment for most of the period ahead.

Our projected growth scenario for the U.S. of 2–2½ percent over the next two years is not without risks, however. On the down side, headwinds could come from three sources: intensified political and economic uncertainty that would prompt higher saving rates by businesses and households; weaker exports due to slower growth abroad; and a more substantial rise in U.S. interest rates. The latter would not only boost the U.S. dollar, but also have adverse balance-sheet effects in emerging economies. On the upside, non-residential investment could make a stronger contribution to growth once businesses gain confidence as political and economic uncertainties are reduced, and government spending could increase providing fiscal stimulus.

In the Euro area, the relatively robust momentum in aggregate demand over the last year is expected to carry on over the next three years, generating growth in the order of 1.6 percent annually. The stimuli from weaker oil prices, the ECB's continuing unconventional monetary policy, the depreciation of the euro, and diminishing drag from fiscal policy are expected to overcome the negative effects of lingering deleveraging by European banks and slowing growth in China. This scenario is predicated on Britain deciding to remain in the European Union and continuing, but not increasing, political uncertainty in the rest of Europe. Intensified political uncertainty alone would be sufficient to dampen spending.

In Japan, growth is expected to accelerate mildly from 0.5 percent in 2015 to an average rate of 0.7 percent over the next three years as final domestic demand responds to extended fiscal stimulus, easier unconventional monetary policy and low oil prices. Slowing growth in China, relatively weak growth in other emerging economies, and a significant appreciation of the yen since last January (which offsets about half the depreciation experienced between mid-2014 to mid-2105) are expected to blunt the contribution of exports to growth. We expect that the Bank of Japan will generally engineer its monetary policy with a view to prevent the yen exchange rate from becoming uncompetitive.

Growth in China should continue to decelerate over the next three years as its economy continues to rebalance away from investment toward consumption (and from industrial production to services). This rebalancing involves lower investment, which has adverse consequences for aggregate demand growth in the short term. At the same time, export growth is set to be constrained by lower trend growth in the world economy and the marked renminbi appreciation since early 2014. The transition to a rebalanced economy is made more risky by the fact that excessive lending to real estate, state-owned enterprises and local authorities has considerably weakened the financial sector. While easier monetary policy, expansionary fiscal policy and further progress in implementing structural and financial reforms could buffer the impact of this transition on demand, a gradual but nonetheless cumulatively important slowing in growth is anticipated.

We believe that the risks to our global projection are reasonably balanced. The U.S. economy faces counterbalancing downside and upside risks, as explained earlier. There is an upside risk to our lower-than-consensus projection of China growth, but the risk of a "hard landing" in China cannot be excluded either. There are both upside and downside risks related to the future path of oil prices and the responsiveness of demand and supply to price changes. Adverse geopolitical developments may erupt at any time. On the other hand, any dissipation of currently high political and economic uncertainty has the potential to release pent-up investment and boost growth more than expected. On balance we conclude that our projected "new normal" three-percent global growth rate for the next three years is consistent with our estimated increase in potential, and that upside and downside risks are reasonably balanced.

This projection of modest global GDP growth suggests that global trade should expand at a subdued pace over the next three years. Clearly, a faster pace of trade liberalization would help to raise the trade intensity of global economic activity (See Section III below for prospects in this regard). But instead, protectionist forces could intensify, particularly from the U.S. and Europe. This would not be without consequence for the Canadian economy, given its dependence on trade.

Outlook for Canada: 2016-2018

In the longer run, after adjustment to earlier cyclical developments and policies, the economy tends to grow at its potential rate. Potential growth in Canada is expected to be marginally higher than 1½ percent from 2016 to 2018 compared to around 2 percent over 2010-14. The cause of the decline is adverse demographics. Growth of the working-age population and trend labour force participation are projected to slow. The consequence of lower potential growth is that the economy has less room to grow before provoking inflationary pressures. The rather subdued growth for the Canadian economy shown in this projection reflects not only the effects of cyclical developments but also this lower potential growth.

Canadian growth appears to have been quite choppy recently. It fell to 0.5 percent at annual rate in the fourth quarter of 2015, but rebounded to 2.4 percent in the first quarter on the strength of exports and residential investment. Business non-residential investment continued to fall, mainly reflecting further cutbacks of capital spending in the oil and gas sector. Going forward, the profile of Canadian growth will be largely determined by external factors (global growth, geopolitical developments and commodity prices) and by domestic fiscal policies. In addition, the Fort McMurray wildfires in the second quarter will affect growth in 2016 and 2017 (see Effect of the Wildfires in the Fort McMurray Area on Canadian Growth).

On net, we expect growth in Canada to pick up from a low 1.1 percent in 2015 to 1.4 percent in 2016 and to a solid 2.4 percent in 2017, before declining to 1.9 percent in 2018, a rate closer to potential. Part of the weaker growth rate for 2016 relative to the Fall 2015 Economic Outlook (2.0 percent) reflects a lower starting point for the projection from the end of 2015, due to data revisions by Statistics Canada, as well as weaker than expected growth during the first quarter of 2016. The projected average rate of quarterly expansion going forward accelerates from -1.1 percent at annual rate in the second quarter of 2016 to nearly 3.0 percent on average in the next four quarters before slowing to less than 2 percent during 2018.

At least three sets of factors would support growth going forward. First, we expect any retrenchment of investment in the oil and gas sector in the second half of 2016 to diminish in severity and, consequently, contribute much less negatively to aggregate demand growth both directly and indirectly. In fact, total business non-residential investment, which has been depressed by the retrenchment in the oil and gas sector, should resume growth in 2017, albeit at a slow pace.

Second, while the size and exact timing of the impact on growth of the fiscal stimulus package announced in the recent federal budget are uncertain, it will undoubtedly have a significant positive effect on growth in the short term. We would expect the level of real GDP to be 0.6-1.0 percent higher in 2017 than it would have been without the additional federal tax and expenditure actions announced in the 2016 budget.3 This is equivalent to a boost of $13-21 billion to the 2017 level of GDP in nominal terms out of discretionary budget measures cumulating to $14.9 billion in 2017-18.

Third, the expansion would also be supported by relatively firm growth in the U.S., continued very low interest rates in Canada, and an expansionary fiscal policy in Alberta. However, by 2017 the contribution of exports to growth will likely diminish and residential investment will likely lose steam as excess supply in the housing market becomes more evident.

The Canadian projection is not without risks, related in particular to the response of net exports to movements in competitiveness, to the drag on growth from low oil prices, to the future profile of oil prices themselves, to the impact of the federal fiscal stimulus and that of uncertainty on business investment. While the first half of 2016 will show weak growth, going forward the risks appear to be balanced.

Effect of the Wildfires in the Fort McMurray Area on Canadian Growth

The negative performance in the second quarter is due to wildfires which erupted in the Fort McMurray area in April, eventually destroying part of the city and prompting most oil sands operations to take the precautionary measure of stopping all or part of their production. The economic impact of the wildfires is difficult to measure with confidence as they would have negatively affected household spending on goods and services, boosted government expenditures, and led to cuts in production from oil sands. Here we limit our analysis to the impact of the oil production cut and the expected rebuilding of Fort McMurray. Looking ahead, we assume that oil production will return completely to normal sometime in June and that the rebuilding of the city will start in the second half of the year. On the assumption that oil production would have been lower by 1.2 million bpd for the equivalent of 30 days in the second quarter, we estimate that this temporary loss would subtract 0.13 percentage points (p.p.) from annual Canadian GDP growth in 2016, based on an average WCS oil price for 2007 of about C$65 per barrel.2 At annual rates, growth would fall to around -1.1 percent in the second quarter and rebound to nearly 4.5 percent in the third quarter. The rebuilding of Fort McMurray (around $1.0 billion) might add 0.05 percentage point to growth in 2017. Thus, the temporary cut in oil production would reduce growth by about 0.13 p.p. in 2016 and reconstruction in Fort McMurray would raise it by about 0.05 p.p. in 2017. Of course, these estimates must be seen as indicative only.

Section II. Adjustment to the Recent Oil Price Shock4

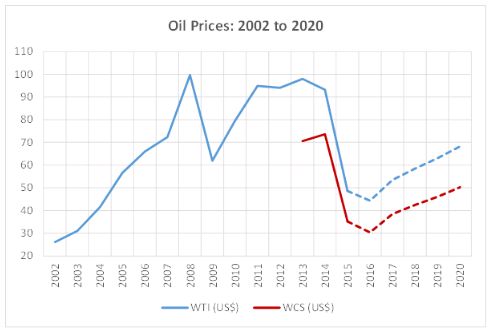

As outlined in Section 1, we project WTI oil prices to gradually rise from an average of about US$45 in the last 1½ years to nearly US$60 in 2018 and to edge up at the general U.S. inflation rate thereafter. This represents a substantial persistent shock relative to expectations that centered on US$95 over the period 2010-2014.5 This shock is expected to permanently cut the level of output, investment and consumption in Canada relative to what they would have been had oil prices adjusted for inflation continued at their previously expected levels. Moreover, the shock will be more severe inasmuch as lack of new oil pipeline capacity results in increased use of expensive rail transportation and hence larger discounts on Western Canada Select (WCS) oil prices relative to benchmark West Texas Intermediate (WTI). For planning purposes, it seems appropriate to assume that the discount will increase somewhat in the future, for example from US$14 in 2016 to US$20 by 2020 as illustrated in Chart 2.1.

Chart 2.1:

The oil price shock is working its ways through the Canadian economy through three main channels:

- The drop in oil prices brings a fall in the terms of trade to permanently lower levels which, in turn, reduces profits and labour earnings, and hence domestic demand and output. Of course, the effects will be felt primarily in the oil-producing regions, but there will be spillovers in the other regions of the country as well. The corollary on the industrial side is a permanent reduction of jobs, unit profits and investment in the oil and gas industry and of output in engineering construction and a host of other industries that meet domestic demand for goods and services across the country.

- The drop in oil prices contributes to a depreciation of the Canadian dollar exchange rate, which in turn stimulates non-oil exports and depresses imports, especially in the regions that are most open to international trade.

- The negative effects of the drop in oil prices on the economy automatically lead to more expansionary macro policies, both monetary and fiscal, which in turn provide support to aggregate demand.

Terms of Trade Effects

Because Canada is a substantial net exporter of oil, the recent oil price shock reduces the level of the terms of trade: this means that less goods and services could be purchased out of the revenues from the sale of oil. The implied loss of income, first profits and soon thereafter labour earnings, depress domestic demand inasmuch as the oil price shock is perceived to be relatively permanent. The effect would be primarily felt in the oil-producing regions: first investment would fall, followed by a more gradual reduction in household spending as first weekly hours, then jobs and finally hourly compensation are adjusted downwards in response to declining activity. Other regions would then experience a decline in their exports of goods and services to oil-producing provinces, with negative effects on their own income and domestic demand via the same types of adjustment as in the oil-producing provinces, but on a smaller scale. Exports to Alberta account for about 4½ percent of GDP in the rest of Canada but for as much as 7½ percent of GDP in the other Western provinces.

The terms of trade effects are expected to depress economic growth in Canada over a period of about three years, thus more or less to the end of 2017. Probably more than half of the total effect has occurred by now if only because the expected massive cutback of investment by the oil and gas industry, which is a key element of the negative terms of trade effects, has been front-end-loaded, with a particularly severe reduction of investment early in 2015. As mentioned in Section 1, we project total business non-residential investment, which has been depressed by the retrenchment in the oil and gas sector, to resume growth in 2017, albeit at a slow pace.

Much of the adjustment in the oil and gas sector applies to investment rather than production. Indeed production as measured by real GDP has continued to rise on average in 2015 and the first quarter of 2016, as an increase in production from oil sands more than offset a decline from other sources. While the downward adjustment of conventional oil production to lower oil prices is probably completed by now given that prices have started trending upwards since February 2016, oil sands production is expected to continue to increase in coming years as new capacity resulting from previous investment over many years comes on stream.

Even if total oil production increased, pressures to cut costs likely prompted labour-saving measures in the oil and gas sector, which would have raised productivity but reduced jobs and hours in the industry and its suppliers. This has significantly depressed labour earnings from oil and gas extraction and supplier industries. Data from Statistics Canada on employment and earnings reveal that employment in the oil and gas industry in Canada was relatively stable in the year to December 2015 at six percent below its peak of April 2014, and then fell rapidly during the first quarter of 2016 when oil prices reached their bottom. The adjustment most likely occurred in the conventional oil sector, which more than accounted for the growth of employment in the overall oil and gas industry over the years of high oil prices.6 The data also reveal that average weekly earnings in the industry fell rapidly in the spring of 2015, probably because overtime was cut, and remained significantly lower than in early 2015 until January 2016.

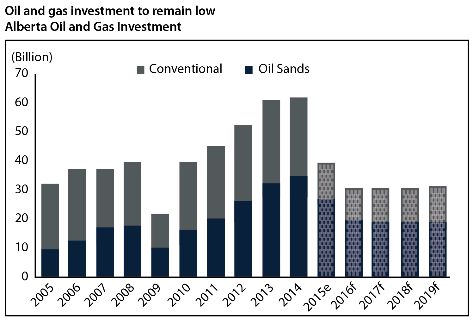

In the decade to 2014, a rise in oil price expectations to high levels prompted a much faster rise of real investment in the oil and gas sector than in the rest of the economy. Much lower price expectations for the medium term have since induced a sharp fall of investment in 2015 in the conventional oil sector and to a lesser extent in the oil sands. Investment is expected to decline at a slower pace in 2016 and to roughly stabilize in 2017, before edging up in subsequent years as illustrated by the Alberta Treasury Board and Finance projection in Budget 2016.

Chart 2.2:

Source: Alberta Treasury Board and Finance, Fiscal Plan 2016-19, Budget 2016, p. 68.

The sharp fall of investment in the oil and gas sector has depressed output and jobs directly and indirectly in the oil-producing regions. The construction sector there has been particularly hit hard, not only through the collapse of non-residential construction but also through the decline in residential construction as jobs and population growth have fallen. In Alberta's case, the share of construction in total GDP appears to have been tied to the evolution of the oil price in Canadian dollars since at least the late 1990s. A marked reduction in the share of construction in the future is to be expected, although perhaps not as severely as the relationship over the ascending phase of oil prices would suggest. This is because much larger net residential and non-residential capital stocks than during this phase would require larger construction expenditures for renovation, repair, modernization and replacement of structures. Moreover much larger public infrastructure spending than during the phase of rising oil prices will provide additional support to construction for a number of years. Finally, reconstruction of the damaged or destroyed structures at Fort McMurray will provide an additional boost to construction in Alberta.

Exchange Rate Effects

Expectations of lower oil prices has contributed to the observed depreciation of the Canadian dollar since the third quarter of 2014. This was not the only factor at play—the decline of other commodity prices and expectations of wider differentials in growth and interest rates in favour of the U.S.7 also contributed to the weakening of the Canadian dollar. But it did exert a very significant influence. Such a depreciation, from over 90 U.S. cents in 2014 to an average of 75 U.S. cents over August 2015-April 20168 and an assumed range of 75-81 U.S. cents going forward, is expected to continue stimulating real net exports over the next year or two. This would have an uneven influence across industries, depending inter alia on their exposure to the exchange rate and the amount of spare capacity they have. Manufacturing and hospitality services, for instance, would be particularly sensitive to the exchange rate and most likely to gain from the recent depreciation. Since provinces have different industry mixes, some should respond more to the depreciation than others. Ontario and Quebec, for instance, may well see their net exports increase more rapidly relative to GDP than other provinces. In any event, for Canada as a whole the higher level of net exports to GDP resulting from the full adjustment of net exports to the weaker exchange rate should partly compensate for the lower levels of investment and household spending relative to GDP resulting from weaker terms of trade.

Impact of Macroeconomic Policies

Monetary and fiscal policies are designed to respond quasi-automatically to shocks to domestic output and prices. The inflation-targeting framework for conventional monetary policy would prompt the central bank to lower (raise) its policy rate in order to support aggregate demand when there are clear indications that a shock would move output further below (above) potential and inflation further below (above) target. And indeed the Bank of Canada cut its target overnight rate in January and July 2015 by 25 basis points each time. These actions eased monetary conditions not only directly through lower interest rates but also through a weaker Canadian dollar. Given already very low interest rates, however, the room for further easing through reductions in the policy interest rate is very limited.

When economic conditions deteriorate, the action of fiscal "automatic stabilizers" provides a stimulus to the economy: tax receipts decline and transfer payments increase, thereby reducing government saving and supporting aggregate demand. The fiscal stance of the federal and provincial governments, as measured by the changes in their net borrowing,9 eased markedly in 2015 relative to 2014, by the equivalent of 0.5 percent of Canadian GDP in each case. The increased net borrowing of governments essentially reflected the work of automatic stabilizers, with Alberta accounting for a disproportionately large share of the total increase in net borrowing given the much sharper deterioration of its economy and the collapse of its royalty revenues.

In their 2016 budgets, both the federal government and the Government of Alberta, which had fiscal room to implement more expansionary policies, opted to amplify the stimulus provided by automatic stabilizers by introducing new discretionary measures to stimulate the economy. In contrast, the Government of Newfoundland and Labrador, which had no room for fiscal expansion, introduced in its 2016 budget discretionary austerity measures that will more than offset the effects of automatic stabilizers.

Partly in response to actual and expected adverse effects of lower oil prices, the 2016 federal budget has incorporated a fiscal stimulus package that would support growth in the second half of 2016 and in 2017 through a variety of measures, including notably increased expenditures on, and transfers for, infrastructure investment. We expect the federal measures alone to add between 0.3 and 0.5 percentage points to Canadian real GDP growth in each of 2016 and 2017 and to raise the level of real GDP in 2017 by between 0.6 and 1.0 percent. The 2016 Alberta budget has also included discretionary measures that on balance would stimulate growth in 2016-17 only, largely through increased capital spending. Governments will have to take further measures in view of the negative impact of the wild fires in the Fort McMurray area in 2016 and the need for reconstruction.

Conclusion: How to Restore and Enhance Real Income in a World of Lower Terms of Trade and Adverse Demographics

Persistently lower oil prices entail persistently lower real domestic income in Canada relative to what it would have been had real oil prices remained at their previously elevated levels. To some extent, the negative impact of such an adjustment is mitigated by the positive effects of a lower Canadian dollar exchange rate and more accommodative monetary and fiscal policies. Nevertheless, growth is reduced during the period of adjustment of the economy to lower oil prices. Once the adjustment is completed, growth would eventually return to its potential rate and the level of real income would remain permanently lower than under elevated oil prices and terms of trade, absent action to raise potential output growth.

The question then is: what can be done in a world of permanently lower terms of trade and adverse demographics to bring the level of Canadian real income in the longer run back to where it would have been in a more favourable world of elevated oil prices and terms of trade? In other words, what policies can be implemented to raise the rate of potential Canadian growth in the future? Higher potential implies we need to raise productivity and this requires new investments in talent and equipment, new products to sell, and access to new markets. Strategic infrastructure that unlocks private-sector investment and innovation, and provides gateways to new markets is an essential part of the solution. With real interest rates near zero and under-utilized design and construction capacity, particularly in the oil-producing regions of the country, there is an opportunity over the remainder of the decade to make large infrastructure investments without creating inflationary pressures.

Clearly the private sector must take the lead in investing and innovating but governments need to create favourable conditions for business sector productivity growth by promoting competition and better access to foreign markets and, most importantly, by investing in strategic public infrastructure.

The primary filter for strategic infrastructure proposals should be whether they are of the scale, scope and impact to raise Canadian productivity levels. Key analytic metrics would include the private-sector investment multiplier, the economic efficiency gains, and the direct and spillover benefits from investing in the economy and ecosystems of the future. To align incentives up front as well as condition public expectations, projects should be selected with a view to be able to sell or lease the infrastructure to the private sector.

Second, executing a strategic investment plan focused on enhancing long-term productivity growth will require institutional structures with the resources and credibility to attract first-class talent in infrastructure investment, a sufficient scale and runway to attract large outside pools of capital, and sufficient independence to provide transparent and rigorous investment advice to government. Such a fit-for-purpose vehicle would be arm's length and have the analytic capacity to expertly review the many project proposals and rigorous benchmarks for what is strategic and excellent. It would also have a mandate to seek co-funding partnerships.

Third, squaring the scale of infrastructure investments required with the prudent public borrowing capacity available will require additional sources of finance. Fortunately, as the experience in Australia and the U.K. demonstrates, private capital is a willing partner where the risk-return calculus is attractive and there is a commitment to scale. The design of a number of greenfield infrastructure projects by the public sector should include the possibility of direct revenue generation (user charges) as this creates additional revenues and thus the conditions for the future involvement of private capital.10

In the face of permanently lower terms of trade, it is more important than ever to raise productivity growth in order to enhance potential growth and standards of living. Getting the strategic infrastructure we need is a productivity imperative. Developing a sound execution plan should be a policy priority for both federal and provincial governments.

Section III: Global Trade Developments – Implications for Canada

Bumpy Road Ahead – Slow Trade Growth Continues

The leading nations continue to pursue trade liberalization through negotiations and the G7 at the recent Ise-Shima Summit committed to "encourage trade liberalization efforts in various forms".11 However, it is unclear whether these promises and all the negotiating activity will result in trade agreements which are actually implemented.

There are also serious risks that economic pressures in certain key countries may boil over, impacting on trade liberalization plans and resulting in protectionist actions with serious adverse impacts.

Nor is the view from the WTO reassuring. WTO economists reported on April 7,12 that growth in the volume of world trade is expected to remain sluggish in 2016 at 2.8 percent, unchanged from the 2.8 percent increase registered in 2015. Global trade growth should rise to 3.6 percent in 2017. Risks to the projection are mostly on the downside. Because of strong fluctuations in commodity prices and exchange rates the dollar value of trade fell 13 percent in 2015.

WTO Director-General Roberto Azevêdo commented on an increasingly troubled trade outlook, "... while the volume of global trade is growing, its value has fallen because of shifting exchange rates and falls in commodity prices. This could undermine fragile economic growth in vulnerable developing countries. There remains as well the threat of creeping protectionism as many governments continue to apply trade restrictions and the stock of these barriers continues to grow."

In their Declaration in Ise-Shima, G7 leaders recognized "the negative impact of global excess capacity across industrial sectors, especially steel, on our economies, trade and workers." How they plan to deal with this problem was not very clear. The Declaration went on to say, "... we are prepared to consult with other major producing countries, utilizing venues such as OECD and other fora, and, as necessary and consistent with the WTO rules and disciplines, to consider the broad range of trade policy instruments and actions to enforce our rights." Of course, China, although not mentioned specifically, was very much in the minds of the Summit participants.

Over the coming months these concerns will play out in part around the question of whether WTO Members can continue after 2016 to automatically treat China as a non-market economy when imposing antidumping or countervailing duties on Chinese imports. There are markedly different views about how to interpret China's Protocol of Accession to the WTO on this matter, with some arguing that the presumption of non-market economy status expires in December 2016, while others argue the contrary. These pressures and disagreements could lead to a major trade row and wind up in WTO dispute settlement.

Trade Negotiations – Some Positives but Significant Uncertainty

Considerable uncertainty about the likely American approach to trade is being created by the unusual protectionist rhetoric from the remaining candidates in the U.S. presidential election. We offer more comment on this below. Additional political uncertainties are created by the prospect of Brexit and its potential impacts on the U.K. and the E.U. Both these factors make it harder to forecast likely developments in trade over the medium term.

Many of the observations in our Fall 2015 Economic Outlook remain relevant today. In the following sections we will essentially update what has happened since and consider the prospects for certain major trade files as we look ahead.

The American Political Scene

Now that Donald Trump is the presumptive candidate of the Republicans for the Presidency of the United States, we have decided to offer a few comments about some of his pronouncements on trade and how they might play out given the checks and balances in the U.S. system.

Mr Trump has said that NAFTA is the worst trade agreement ever negotiated in history and that he would renegotiate it or abrogate it. It is not as straightforward as he suggests. If the United States did wish to withdraw from the Agreement, it would have to give six months' notice. Moreover, the decision is not one the President can take on his/her own. It is Congress which has the responsibility under the Constitution "to regulate commerce with foreign nations". In our Fall outlook we reported on the Trade Promotion Authority (TPA) enacted by Congress less than a year ago. This law establishes the framework for the negotiation of trade agreements by the President including setting the objectives to be pursued and the requirement for working closely with Congress. These provisions would be directly relevant to any effort to renegotiate NAFTA. In the unlikely event that the President were to invoke the clause to withdraw from NAFTA, it is not clear what exactly would happen. But one thing is clear, absent action by Congress, the NAFTA implementation would remain a part of U.S. law. In addition, there would likely be a huge effort by the American business community to preserve the structure of trade agreements negotiated by the U.S. because they would not want to lose market access benefits obtained through these agreements and the investment and intellectual property protections they afford.

The same considerations would pertain to Mr Trump's stated intention to renegotiate other trade agreements. Similarly, his proposals to raise duties on imports from countries like China and Mexico would require Congressional legislation, as would penalties on firms that move production outside the U.S.

This is not to suggest complacency because there are fortunately real constraints on implementing such proposals. Clearly, if a sitting president were to pursue these initiatives it would cause serious uncertainty that would undermine business confidence at home and abroad.

So, against this background, what are the prospects for TPP ratification in the U.S.? The three remaining presidential candidates are all on record as being hostile to the TPP, with Hillary Clinton being the least hostile. Meanwhile President Obama has made it clear he intends to submit the agreement to Congress for approval later this year probably in the "lame duck" session after the American elections in November. A number of Republican Congressmen are working with the administration to try to address the concerns they have identified with a limited number of provisions in the TPP. They have indicated they are open to voting on the TPP in the lame duck session. Importantly, consideration is being given to how to address these concerns without actually reopening the TPP itself. All three presidential candidates are opposed to the idea of dealing with TPP this year. However, the real power to decide what to do will rest with Congress. If Secretary Clinton is the eventual winner, she will probably maintain her opposition but not too vigorously. She does not want to have the TPP land on her desk on her first day in office with the risk that she would need to preside over a year of Democratic infighting about what to do about it.

On May 18, as required under U.S. law, the United States International Trade Commission (USITC) issued its report13 assessing the likely impact of the TPP on the U.S. economy. Using a CGE model it estimates very small positive effects on the U.S., including an increase of 0.15 percent in GDP over the entire 15-year implementation period for the agreement. However, the report also identifies a range of regulatory provisions establishing trade rules, the impact of which are "difficult to quantify". The report goes on to assert that these provisions "have the potential to positively affect the U.S. economy by strengthening and harmonizing regulations, increasing certainty, and decreasing trade costs for firms that trade and invest in the TPP region." The report will be an important reference document as Congress considers its course of action but it will definitely not bring closure to the debate.

We believe there is a 50-percent chance that Congress will approve the TPP and pass the implementing legislation in the lame duck session later this year.

If TPP is not approved this year it will then be up to the next U.S. president to decide what to do. The TPA authority for fast track approval is potentially in force until 2021.

Canada and the TPP

Our comments in our Fall 2015 Economic Outlook remain largely relevant today. We continue to believe this is a useful deal for Canada that would enhance the productivity and competitiveness of Canadian business while increasing competition in the domestic market to the benefit of consumers. In addition, it remains our view that there would be very sizable costs to not participating in the agreement if it were to come into force. For grains and oilseeds and red meat there would be significant benefits from the TPP and very large costs of standing aside. For industrial products the main effects of the TPP on Canada will be in North America, particularly in the U.S. These effects will be felt through changes in supply chains under the influence of the new, more liberal rules of origin, and through the erosion of Canadian NAFTA preferences in the U.S. market. If the U.S. is in TPP, the only way to mitigate, or benefit, from these developments is to be part of the agreement.

The government continues to consult Canadians on whether to ratify the agreement. A great number of comments have been received. The House of Commons Standing Committee on International Trade is holding hearings in Ottawa and around the country. The government has promised an eventual full debate in Parliament. Frankly, it is hard for Canadians to comment effectively on the agreement given its complexity. The government could help rectify this by enhancing its efforts to explain the provisions to Canadians.

David Lametti, the Parliamentary Secretary to the Minister for International Trade is quoted in an article in the Hill Times of May 18, responding to a question about the most striking thing he had heard in the consultations. His answer was that it was the "passion" – "People who are passionately for this agreement, people who are passionately against this agreement."

Given the passion in the debate it is useful to put it in context.

First, much of the debate, while focused on the TPP, is really about whether Canada should be entering trade agreements that address the real issues of global commerce in 2016, which involve such core matters as investment, services, and intellectual property. Indeed, many of the criticisms of TPP could also be levelled at NAFTA and CETA.

Second, it is instructive to look at the geographic makeup of Canada's merchandise trade with TPP signatories. While goods trade is only part of the story, it has been a key focus of both proponents and detractors of the agreement. For Canada the TPP is mostly NAFTA. Within the region made up by the signatories to the TPP, 94 percent of Canada's trade (exports plus imports) is with our NAFTA partners. If we include Japan with the U.S. and Mexico then the figure increases to 97 percent of Canada's goods trade. Canada has been negotiating separately an FTA with Japan. Extending the free trade area to include the other eight TPP partners, accounting for three percent of Canada's TPP trade is not likely to have a significant effect in aggregate terms on Canada's economy either positive or negative. As previously noted, the biggest prize for Canada in the TPP is access to the Japanese market, putting Canada back on an even footing with countries like Australia and Mexico that already have FTAs with Japan and, in addition, eliminating or reducing protection for the Japanese market itself.

The government is taking the view that it has until February 4, 2018, to ratify, the first date on which the TPP could come into force with fewer than all 12 signatories. The TPP is designed so that it cannot come into force without both the U.S. and Japan being parties to it. It is perhaps understandable that before proceeding to ratify the TPP the government would like to know the outcome of the ratification battle in the U.S. The trouble with this approach is that it gives the impression to Canadians that the government is uncertain about whether the TPP is beneficial for Canada and is really leaving the decision about whether Canada should ratify up to the Americans. It also sends an unfortunate message to our partners in Asia that Canada is not really committed to the region in its own right and that we define our relationship with Asian countries through our defensive interests in the U.S.

We recommend that the government give serious consideration to dealing with this situation by announcing publicly its support for the TPP but leaving actual ratification until after the U.S. has ratified.

CETA

The prospects for CETA ratification improved considerably on February 29 when Canada and the E.U. announced they had completed the legal review of the text, and that as part of that review they had agreed to substantial modifications to the provisions dealing with investor state dispute settlement. As a result both Chrystia Freeland, Minister of International Trade, and Cecilia Malmström, European Commissioner for Trade, have expressed confidence that CETA will be signed in 2016 and will enter into force in 2017. While there remain pockets of resistance to the agreement on both sides of the Atlantic it is looking more and more like a done deal. However, a number of potential hurdles are still being encountered with the most significant at the moment being the position of Romania and Bulgaria, who are using CETA ratification as a tool to address their concerns about Canadian visa requirements for their citizens.

A U.K. vote in favour of Brexit would clearly have negative effects on global commerce and contribute to uncertainty. We do not believe that it would stop the CETA from being implemented although it would certainly provide some distraction, which might further delay ratification.

On balance, we believe that CETA will be ratified in Canada and by the European Parliament within the next 12 to 18 months and that it will then come into force provisionally. Final ratification by all 28 E.U. member states will take longer.

Mexico

Efforts are underway to revitalize Canada's partnership with the U.S. and Mexico. On June 29, Prime Minister Trudeau will host the North American Leaders' Summit in Ottawa with President Obama and President Peña Nieto. President Obama has been invited to address Parliament and a state dinner is being offered for President Peña. However, there still remains a hitch regarding the government's commitment to lift the visa requirement for Mexicans. Apparently it is intended that this will be done through the new electronic visa processing system for all countries. However, the roll out is taking longer than expected. This issue has become a real stumbling block to better relations that are so full of potential. The government must find a way to remove the visa requirement before the end of June even if it is only on a temporary basis pending the introduction of the new system.

China

The government continues to pursue as a top priority the development of a targeted strategy to promote trade and investment with China. While some quiet discussions have taken place with Canadian businesses, it is not clear exactly how the government will proceed. The Chinese have made clear that they would like to negotiate an FTA with Canada but the Canadian government has not responded. Many Canadian exporters mindful of the FTAs that Australia and New Zealand have with China favour negotiation of an FTA. It is expected that the Prime Minister will make a bilateral visit to China in advance of the G20 Leaders' Summit in Hangzhou, September 4-5. That could well be the point at which the government would announce its China strategy.

WTO

The Trade Facilitation Agreement (TFA) remains a bright spot with the number of ratifications now at 81, up from 53 at the time of the last outlook, and getting closer to the two-thirds required to bring the agreement into force. The WTO considers the TFA could boost trade by up to US$1 trillion per year. For some reason Canada has still not ratified.

The December Ministerial Conference of the WTO turned out to be more useful than we had suggested in our last outlook. Particularly noteworthy was a commitment to abolish export subsidies for farm exports.

This commitment was set forth in a Ministerial Decision rather than an amendment to the provisions of the WTO, which means it does not require two-thirds of the membership to file an instrument of acceptance before it comes into force and could therefore take effect much earlier than an amendment would have done. Several WTO members have already started domestic legal procedures to eliminate their export subsidy entitlements. Getting 162 members to agree by consensus to make this change was a major achievement and was hailed by Director-General Azevêdo as the "most significant outcome on agriculture" in the WTO's history.14 However, the drawback of this technique for amendment is that it does not become part of the WTO "covered agreements" and is therefore not subject to the dispute settlement procedures in, for instance, the not unlikely event there is a disagreement about whether a particular measure is an export subsidy.

Finally, dispute settlement activity remains very high at the WTO, with the total number of disputes filed reaching 507 last month. Trade remedies continue to dominate, but several important disputes in the SPS (sanitary and phytosanitary), TBT (technical barriers to trade) and Services areas are also underway. Canada is currently pursuing cases against the U.S. and China, and is defending a case brought by Chinese Taipei.

Plurilateral Negotiations

At the Nairobi Conference final agreement was reached on the deal to expand the WTO Information Technology Agreement (ITA) to include elimination of duties on an additional 201 IT products. Azevêdo noted, "Trade in the products covered by the agreement is valued at approximately $1.3 trillion each year. This is larger than global trade in automotive products. Or, to take another example, it is larger than global trade in textiles, clothing, iron and steel combined."15

According to Global Affairs Canada,16 new progress has been made in several of the sectors under negotiation in the Trade in Services Agreement (TiSA) negotiations and an active series of sessions are planned for the remainder of the year. As previously reported, this negotiation is an effort by 23 countries accounting for 75 percent of the world's $44-trillion services market to expand and improve on the provisions of the WTO Agreement on Trade in Services.

Work continues in the Environmental Goods Agreement (EGA) negotiations among the U.S., Australia, Canada, China, Costa Rica, the E.U., Hong Kong, Japan, Korea, New Zealand, Norway, Singapore, Switzerland and Chinese Taipei. These countries account for 86 percent of global trade in environmental goods, estimated at some US$1 trillion annually. On June 2 in Paris, Trade Ministers and senior officials from seven EGA members—Australia, Canada, the European Union, Japan, Korea, New Zealand, and the U.S.17 —"welcomed the significant progress that has been made" in these negotiations. These seven governments share "the aim of concluding an ambitious EGA with all participants ahead of when G20 Leaders meet in Hangzhou in September for the G20 Summit".

Conclusion

The trade outlook is a mixed picture clouded by political uncertainties in many countries, including some of our closest partners. A populist political backlash against trade agreements and open markets is creating pressure that could result in action against Canadian products. Two very large Canadian exports are already facing some difficulties—softwood lumber in the U.S. and canola in China.

Despite perceptions that the trade agenda is completely blocked, there are quite a few significant accomplishments, but a lot more remains to be done to ensure that these positive developments are turned into actual implemented agreements.

In our view, Canada should remain focused on opportunities to achieve and consolidate further trade liberalization. At the same time, the government needs to remain vigilant and ready to take tough action to defend the interests of Canadian producers from protectionist actions abroad.

Footnotes

1 Fiscal Monitor: Acting Now, Acting Together, April 2016, p.14. [compare also G7 statement]

2 Real GDP (at basic prices) for oil production is based on oil production valued at 2007 prices. The underlying WCS price of US$60 was estimated using the actual 2007 WTI price of US$72 and an assumed discount of US$12 for WCS. Data on WCS oil price available from the Alberta Government only start in January 2009.

3 The federal government expects a one percent boost to the level of GDP in the fiscal year 2017-18.

4 For an earlier, broader analysis, see J. Champagne, N. Perevalov, H. Pioro, D. Brouillette and A. Agopsowicz, "The Complex Adjustment of the Canadian Economy to Lower Commodity Prices", Staff Analytical Note 2016-1, Bank of Canada, January 2016.

5 Based on two-year ahead projections of WTI oil prices in the Alberta government budgets from 2010 to 2014. Such projections are established after consultations with the private sector.

6 See A. Sharpe and B. Waslander, "The Impact of the Oil Boom on Canada's Labour Productivity Performance, 2000-2012", International Productivity Monitor, Centre for the Study of Living Standards, Spring 2014.

7 These expectations not only relative to Canada but also relative to other major countries would largely explain the appreciation of the multilateral exchange rate of the U.S. dollar in the same period.

8 This masks a sharp but brief depreciation of the Canadian dollar to 70 U.S. cents in January before rising steadily to 79 U.S. cents in April. See Section 1 for a discussion of the causes of these movements.

9 Net borrowing is equivalent to total revenues less current expenditures, debt charges and capital expenditures.

10 See also David Dodge, Kevin Lynch and Tiff Macklem, "How do we get the infrastructure we need?", Globe and Mail, May 13, 2016.

11 See the G7 Leaders' Declaration form the G7 Ise-Shima Summit May 27-28 2016 - http://www.japan.go.jp/g7/summit/documents/index.html

12 For more information see the WTO press release at: https://www.wto.org/english/news_e/pres16_e/pr768_e.htm

13 https://www.usitc.gov/publications/332/pub4607.pdf While the report is 792 pages in length, there is a 22-page Executive Summary which provides a useful synopsis.

14 https://www.wto.org/english/news_e/news15_e/mc10_19dec15_e.htm

15 https://www.wto.org/english/news_e/spra_e/spra104_e.htm

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]