This decision relates to a European patent application for a method for recording usage data for an industrial truck. Here are the practical takeaways from the decision T 0199/16 () of 14.10.2021 of Technical Board of Appeal 3.4.03:

Key takeaways

The generation of fee calculations is of a non-technical nature and as such without a technical connection is excluded from patentability by Article 52 (2) EPC.

The invention

The application relates to a method for user data acquisition of a truck for calculating fees for the use of the truck. It is proposed to report the wear-relevant measured variables via a wireless connection to a central processing unit, where the fee can be calculated.

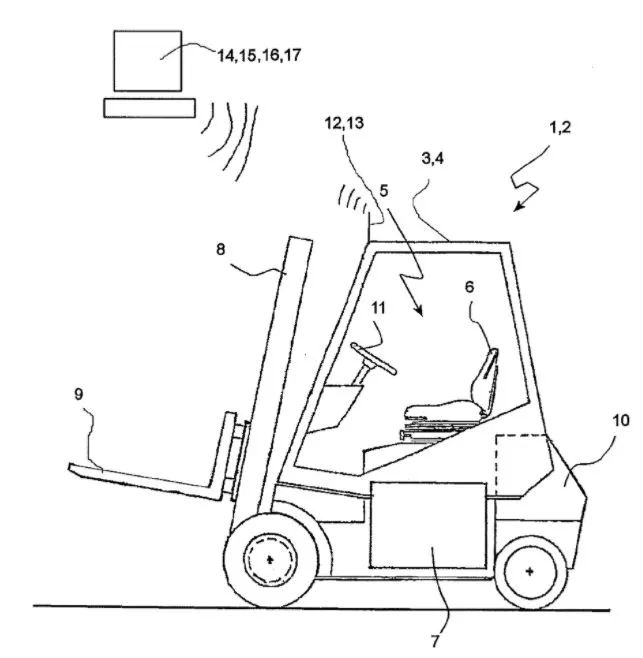

Figure of EP2518681

Here is how the invention was defined in claim 1:

Claim 1 (main request), translated from German to English

(A) Method for collection of usage data of a Industrial truck (1) with at least one industrial truck (1),

(B) the recording means, in particular sensors, for the recording of usage and / or wear-relevant measured variables,

(C) and a wireless data transmission device (12), and

(D) with a wireless data receiving device (16) and with a computing unit (17) which is connected to the data receiving device (16),

(E) wherein the measurement variables relevant to use and / or wear are recorded by the recording means, characterized in that

(F) that the measured variables are transmitted from the data transmission device (12) and the data receiving device (16) to the computing unit (17),

(G) and the measured variables are processed and evaluated by the arithmetic unit (17),

(H) to determine usage data in the form of a usage fee.

Is it patentable?

The Examining Division had refused the application for lack of inventive step, as the subject-matter of the claims related to a business method that would not result in a combined technical effect with the technical features known from telematics systems and would not change the technical character of these known technical features.

During the appeal stage, D4 was considered as the closest prior art for claim 1. The Board considers that D4 discloses features (A) to (G), but not "to determine usage data in the form of a usage fee" (feature (H)), i.e. the calculation of the (leasing) fee from the measured variables, e.g. the operating hours.

The appellant tried to argue that the distinguishing feature has technical effect because the calculated fee could also be used to correct the measured variables.

However, the Board was not convinced. The Board cannot directly deduce from the application that the calculated fee will be used for a data correction. Rather, it is examined how a data correction affects the pay. On the other hand, a data correction is not part of the wording of the claim.

Feature (H) therefore only has the effect that an automated billing based on the user time or the wear and tear of the device used can be created. Feature (H) thus has a non-technical effect, since it is primarily used for business purposes. The features (A) to (H) are technical in their entirety and some have purely technical purposes. However, this does not apply to feature (H) when considered in isolation.

The Board essentially agrees with the reasoning of the examining division that feature (H) in itself is a purely commercial, non-technical feature. The established problem-solution approach in the presence of non-technical features has been established since decision T 641/00. The solution to the problem is obvious in the present case simply by including the non-technical features in the problem.

In addition, the Board does not see any structural technical features in the wording of the claim that would pose technical problems for the specialist. The technical problem would more likely lie in how the measured quantities are determined. On the other hand, the application for the implementation of the feature (H) does not specify any special technical solutions that go beyond what the specialist could achieve by reprogramming the central computer, would have an additional or special technical effect or would represent an unexpected and non-obvious solution. The technical means used to solve the problem are not specified any further. The task to be solved is simply a fee calculation from measured variables. It follows directly from the task,

Therefore, the Board concluded that the subject-matter of claim 1 does not involve an inventive step (Article 56 EPC). The appeal was thus dismissed.

More information

You can read the whole decision here: T 0199/16 () of 14.10.2021 of Technical Board of Appeal 3.4.03.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.