- within Technology, Antitrust/Competition Law and International Law topic(s)

- with readers working within the Technology industries

Originally published 6 May 2008

Please click on the following link to view "Auction-Rate Securities: Bidder´s Remorse? A Primer in its entirety, inclusive of all charts, footnotes and glossary of terms.

Auction-rate securities (ARS) are long-term variable-rate instruments with their interest rates reset at periodic and frequent auctions. They are often marketed to issuers as an alternative variable-rate financing vehicle and to investors as an alternative to money market funds. Investors have historically been able to liquidate ARS positions at face value at frequent auctions, leading many to consider them cash-like. After hundreds of auction failures in February 2008, however, the Wall Street Journal declared that the ARS market had "virtually collapsed."

Recent media coverage has pointed to broker-dealers withdrawing support from this market. Many articles have discussed credit rating downgrades of monoline insurers. We believe the auction-rate market encompasses securities and issuers of varying characteristics and that an understanding of recent events requires detailed analyses of these characteristics.

This paper explores auction-rate securities in depth. First, we describe the ARS market and explain the "Dutch auction" process. Next, we review the evolution of these securities through the present crisis. We then describe responses to auction failures including issuer restructuring, corporate write-downs, and litigation.

The Auction-Rate Securities Market

Auction-rate securities (ARS) are long-term variable-rate instruments with their interest rates reset at periodic and frequent auctions. They are often marketed to issuers as an alternative variable-rate financing vehicle and to investors as an alternative to money market funds. Investors have historically been able to liquidate ARS positions at face value at frequent auctions, leading many to consider them cash-like. After hundreds of auction failures in February 2008, however, the Wall Street Journal declared that the ARS market had "virtually collapsed."1 As seen in Exhibit 1, the percentage of failing auctions rose dramatically in February 2008.

The auction-rate market is estimated at about $330 billion

outstanding.2 There are two primary types of

auction-rate instruments: long-term, often tax-exempt, debt

instruments issued by municipalities or other entities

(approximately 75% of the market)3 and perpetual

preferred equity instruments primarily issued by closed-end

mutual funds (approximately 20% of the

market).4

Other types of issuers, which represent but a small portion of

the market, include corporations

and collateralized debt obligations (CDOs). Exhibit 2

(following page) shows the size and composition of the

auction-rate market.

While we present data on auction-rate securities by issuer type, we believe the auction-rate market encompasses securities and issuers of varying characteristics and that an understanding of recent events requires detailed analyses of these characteristics. We focus most of this paper's discussion on auction-rate securities issued by municipal and closed-end fund issuers.

Municipalities such as counties and school districts issue debt to fund specific projects like construction of roads, bridges, buildings, and sewer systems, or to meet general financing needs. They make debt payments with revenues from sources such as taxes and tolls. While municipalities are major participants in the auction-rate market, ARS comprise a small portion of municipal debt outstanding.5 That said, for any particular municipal issuer, ARS may comprise a large share of its debt.

Closed-end mutual funds are investment companies that issue a fixed number of shares; these shares are typically traded on an exchange. After issuance, an investor does not purchase or redeem shares directly with the fund but instead buys and sells shares of the fund on the open market.6 Unlike open-end mutual funds, which are prohibited from using most types of leverage, closed-end funds typically do use leverage to enhance returns to their common shareholders.7 Closed-end funds are required to have a 300% asset coverage ratio when using debt, meaning that the value of their assets must be at least three times larger than the value of their debt; they are only required to have 200% asset coverage when using preferred stock.8 This may be one reason why preferred stock has become the dominant form of leverage for closed-end funds.9 One might find that a closed-end mutual fund has one-third of its assets funded by preferred stock and two-thirds funded by common equity. Auction-rate preferred is one type of closed-end fund preferred stock.

Motivations for issuing auction-rate securities will vary from issuer to issuer. Once an issuer has determined that it prefers a variable-rate instrument to a fixed-rate instrument, it can choose from different types of variable-rate instruments. If it issues a traditional variable-rate instrument for which it pays a set spread over a benchmark rate, this fixes the issuer's credit spread for the life of the instrument.10 Auction-rate securities allow the issuer's credit spread to vary over time. In addition, some alternative variable-rate instruments may require the issuer to periodically renew a liquidity facility, which auction-rate securities do not.11 For some issuers, the auction-rate market has historically been attractive as a source of lower cost financing.12 Issuer and investor preferences at the time of issuance will influence the choice of financing instrument.

Purchasers of auction-rate securities are generally wealthy individuals or corporate treasuries, and the minimum investment amount is usually $25,000. This contrasts with the broader set of buyers in the overall municipal debt market which also includes commercial banks, insurance companies, and government-sponsored enterprises, among others.13 In general, closed-end fund investors are individuals who "tend to have much greater household financial assets than either individual stock or mutual fund investors."14 A May 2006 study by the Association for Financial Professionals indicated that just 35% of companies allowed any portion of their short-term investments to be allocated to ARS, as the left panel of Exhibit 3 shows.15 ARS made up a relatively small fraction of corporate treasury investments, as the right panel of Exhibit 3 shows, averaging only 5% for surveyed corporations. However, for any individual corporation, its auction-rate holdings might comprise a much larger portion of its short-term investments.

Recent auction failures have focused attention on this relatively small corner of the debt world. Recent disruptions in this market provide an interesting example of the interconnectedness of modern financial markets.

The Auction Process

In general, coupon-paying bonds may be "fixed-rate" or "variable-rate." Fixed-rate bonds pay coupons of the same amount every period based on one fixed rate, while variable-rate coupons vary in amount and are based on a rate that changes from one period to the next. This variable rate is typically set as a spread over some benchmark rate, for example, LIBOR or Fed Funds.16 In the case of auction-rate securities, this variable rate is periodically re-determined through modified "Dutch auctions," as detailed below.17 In other words, the auction is an alternative mechanism for resetting the coupon rate or dividend on the bond or preferred stock. The auctions are facilitated by broker-dealers ("remarketing agents")18 and are generally held every 7, 28, 35, or 49 days. ARS are auctioned at par and are remarketed by one or more broker-dealers. There is rarely a resale market outside the periodic auctions. After a successful auction, new purchasers and continuing holders receive the rate determined at auction, and sellers, who have been receiving interest payments, get back the face value of their investment. If the auctions are continuously successful, ARS share characteristics with short-term, liquid securities.

Prior to a typical ARS auction, broker-dealers survey investor interest and give guidance to potential investors called "price talk." This is the range of rates within which the broker-dealer believes the auction is likely, though not guaranteed, to clear. The broker-dealer may consider factors such as prevailing market conditions and clearing rates for recent auctions of comparable securities. Current holders may sell, continue to hold at any clearing rate, or indicate that they wish to hold only if the clearing rate is at or above a particular level. Interested buyers submit purchase bids, and sellers submit sale bids.

In summary, there are four types of bids:

|

Buy |

The potential investor's bid includes a given rate and a quantity it will buy if the clearing rate is equal to or greater than this given rate; |

|

Hold |

The current holder will continue to hold a given quantity at any clearing rate; |

|

Hold-at-Rate |

The current holder will continue to hold a given quantity if the clearing rate is equal to or greater than the given rate, otherwise it will sell at the clearing rate;19 |

|

Sell |

The current holder will sell a given quantity at any clearing rate. |

Bids are submitted to broker-dealers, who collect the information and pass it on to the "auction agent" by a particular deadline. Some broker-dealers allow bid submission right up until their own deadline with the auction agent, and some have an earlier internal deadline to allow time for processing. The auction agent determines if bids are such that the auction will succeed, i.e., if there is enough buyer demand to cover seller supply. Then the auction agent determines the clearing rate. Bids for each broker-dealer are then filled, sometimes on a pro rata basis, generally with settlement on the next business day. Broker-dealers in turn fill bids for their individual clients. Hold bids are filled first, followed by hold-at-rate and buy bids below the clearing rate, followed by hold-at-rate bids at the clearing rate, and finally, buy bids at the clearing rate. Hold-at-rate and buy bids above the clearing rate are not filled. An example helps illustrate.

An Example Auction

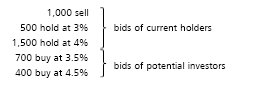

Take a hypothetical $100 million ARS. With a unit size of $25,00020 this equates to 4,000 units outstanding. If holders of all 4,000 units decide to hold regardless of the clearing rate, i.e., they all submit "hold" bids, an "all-hold" auction occurs and the rate automatically resets to the all-hold rate specified in the security's official documents. If there are any hold-at-rate or sell bids, an all-hold auction cannot occur. For this example assume holders of 1,000 units have submitted holds (to hold at any rate). This means that there are 3,000 units potentially for sale in this auction. Assume the following bids:

Given these bids, will this auction succeed or fail?

In order for an auction to succeed, buys must equal or exceed sells. This example auction will succeed because there are 1,100 buy bids and 1,000 sell bids. This calculation can also be expressed in terms of the supply of and demand for units. As we stated previously, there are 3,000 units potentially for sale in this auction. Demand totals 3,100 (2,000 hold-at-rate bids + 1,100 buy bids). Thus this auction will succeed as the demand of 3,100 units is greater than the supply of 3,000 units.21 Exhibit 4 illustrates.

If, in our example, the supply of units increased by more than 100, or the demand for units fell by more than 100, the auction would fail (supply would exceed demand). Thus, we can see that auctions fail with an increase in holders wishing to sell units, a decrease in new buyers, or a combination of the two.

Now that we know this auction is successful, what is the clearing rate? First, we sort the bids and order them from lowest to highest rate:

Then, we fill bids in order. The auction clears at the rate at which the last bid is fully or partially filled, in this case 4.5%. This is shown in Exhibit 5 (following page).

In a second example, assume that bidder #2's bid size increased from 700 to 1,000:

In this case the auction would clear at 4%, and bidder #4 would not make a purchase.

In a third example, assume that bidder #2 had only bid for 250 units. Total demand would be 2,650 (2,000 hold-at-rate bids + 650 buy bids), less than the supply of 3,000 units. This is depicted in Exhibit 6.

In this third example, the auction would fail, in which case all current investors would continue to hold, and the rate would reset to the penalty rate from the offering documents.

Auction "Failures" and "All-Hold" Auctions

There are two auction outcomes with no clearing rate. One is when all current investors decide to continue holding at any rate: an "all-hold" auction. Until the next auction, holders will earn the all-hold rate set forth in the offering prospectus. The all-hold rate is typically a below-market rate. In February 2008, for example, the California Housing Finance Agency experienced an all-hold auction and the interest rate was set to 1.4%.22

The other auction outcome with no clearing rate is a failed auction, when seller supply outstrips buyer demand. In the case of failure, the rate reverts to the "penalty" or "maximum rate" set in the official documents. The maximum rate is typically an above-market rate that is also greater than the all-hold rate. After an auction failure, the securities remain with current holders, who may or may not have wished to sell, but who now receive the higher penalty rate. Penalty rates for municipal ARS tend to be much higher than those for the auction-rate preferreds of closed-end funds. For example, after an auction failure on 12 February 2008, the Port Authority of New York and New Jersey had one penalty rate of 20%, up from 4.25% one week prior and costing $300,000 in extra interest payments per week.23 Closed-end funds with auction failures, on the other hand, might see increases of only 20 or 30 basis points.24 For example, the average penalty rate for one type of closed-end fund was 3.8% as of March 2008.25 Some states, such as Illinois, have caps which limit penalty rates for municipal issuers.26

A Brief History of the Auction-Rate Market

The 1980s: Auction Rates are Born

To reduce the high inflation of the late 1970s and early

1980s, the Federal Reserve raised the

target Federal Funds rate to almost 20% by the early 1980s,

resulting in a dramatic increase in borrowing costs for many

institutions. In response to a demand for variable-rate and

potentially lower-cost financing alternatives, investment banks

began devising new and complex financial instruments. While

some of these were short-lived, others became staple products,

including the auction-rate security.

The first ARS was registered by American Express in July 1984.27 The instrument was conceived by Ronald Gallatin, managing director of new product development in the Lehman Brothers Unit of Shearson Lehman/American Express.28 American Express initially filed a shelf registration29 with the SEC for $300 million of money market preferred shares (MMPs), with the first auctions to be held on 16 and 23 October.30 Before the first auctions took place, two other issuers had entered the market, City Federal Savings & Loan with a registration of $75 million and US Steel Corp. with a registration of $250 million.31 Several other issues followed. In November 1984, First Boston Corp. followed Shearson Lehman as an ARS underwriter with the issuance of $100 million for Lincoln National Corp.32

Market Evolution and the First Auction Failures

While the original auction-rate securities were uninsured and uncollateralized, US Steel's 1985 issue of MMPs, its second, was insured, thus paying a dividend rate 200 basis points less than its first issue.33 The insurance directly reduced default risk to investors. In September 1987, Mattel introduced an issue of ARS collateralized by trade receivables backed by an insurance firm's agreement to buy the receivables at a preset price.34 This reduced the default risk associated with the issue and Mattel's borrowing cost.

In addition to the possibility of default, the inherent risk of auction failure was evident early on. While bond insurance provided many issues with the highest possible credit ratings, these ratings addressed the likelihood of issuer default, not the likelihood of auction failure. In a 1985 Wall Street Journal article, Ann Monroe wrote:

The Dutch auction only works because investors believe it will work. So anything that shook investor confidence—for example, severe financial problems among a group of issuers—could make the concept unworkable and jeopardize price stability.35

Twenty-two years later, PIMCO managing director Paul McCulley wrote:

Liquidity is not a pool of money but rather a state of mind& liquidity is about borrowers' and lenders' collective appetite for risk, a function of the willingness of investors to underwrite risk and uncertainty with borrowed money and the willingness of savers to lend money to investors.36

The year 1987 saw the first auction failure, causing the dividend rate on a $125 million MCorp preferred stock issue to jump to a maximum allowed rate exceeding 10%. Following this failure, Shearson Lehman provided liquidity to the market by offering to buy the issue from investors. In 1988 Shearson Lehman disclosed that it held $117.5 million of these securities, and in the first half of 1989 MCorp filed for bankruptcy. Due to the bankruptcy, Shearson Lehman wrote down the entire value of its MCorp auction-rate position in 1989.37 Two auctions for the Kroger Company also failed in 1988, though these issues were quickly redeemed at par value as part of a restructuring plan.38

The auction-rate market was initially dominated by corporate issuers and corporate investors. Prior to The Tax Reform Act of 1986, corporate investors could exclude 85% of their preferred dividends from taxation. After the '86 Act and an additional reduction in the exclusion for dividends after 31 December 1987, this tax advantage diminished. In addition, explicit tax advantages for traditional debt increased with changes in the tax code in the late 1980s.39

Continuing Market Development and the May 2006 SEC Settlement

The auction-rate market continued to develop and expand throughout the 1990s and 2000s. Other types of issuers saw the value in these products which generally allowed them to finance long-term assets at short-term borrowing rates. While the total par value of outstanding municipal auction-rate securities is small relative to the entire municipal debt market, its importance increased during this time. Municipal ARS bonds comprised less than one-half of one percent of new issuance in 1990, but represented over 8% in 2006.40 Closed-end mutual funds used auction-rate preferreds to provide leverage and enhance returns to their common shareholders. Student loan lenders issuing student loan asset backed securities (SLABS) tapped the auction-rate market. More recently, while only representing a small slice of the auction-rate market, even CDOs issued auction-rate securities.

After an investigation, beginning in 2004, of underwriting practices and the auction process, the SEC issued cease and desist orders and settled with 15 banks and broker-dealers for a collective $13.375 million in May 2006.41 The SEC's order identified several "violative practices" related to

- Completion of Open or Market Bids: "&allowed the Respondent to designate some or all of the bid's parameters, such as the specific security, rate, or quantity."

- Interventions in Auctions

- Bids To Prevent Failed Auctions: "Without adequate disclosure, certain Respondents bid to prevent auctions from failing."

- Bids To Set a "Market" Rate: "Without adequate disclosure, certain Respondents submitted bids or asked investors to change their bids so that auctions cleared at rates& considered to be appropriate market' rates."

- Bids To Prevent All-Hold Auctions: "Without adequate disclosure, certain Respondents submitted bids or asked investors to submit bids to prevent the all-hold rate."

- Prioritization of Bids: "Before submitting bids to the auction agent, certain Respondents changed or prioritized' their customers' bids to increase the likelihood that the bids would be filled."

- Submission or Revision of Bids After Deadlines: "In certain instances, these practices& advantaged investors or Respondents who bid after a deadline by displacing other investors' bids, affected the clearing rate, and did not conform to disclosed procedures."

- Allocation of Securities: "Certain Respondents exercised discretion in allocating securities to investors who bid at the clearing rate instead of allocating the securities pro rata as stated in the disclosure documents."

- Partial Orders: "When [investors would have received a pro rata allocation of securities after an oversubscribed auction]& certain Respondents did not require certain investors to follow through with the purchase of the securities even though the bids were supposed to be irrevocable."

- Express or Tacit Understandings To Provide Higher Returns: "[for example] certain Respondents provided a higher return by delaying the settlement date for certain investors."

- Price Talk: "Certain Respondents provided different price talk' to certain investors."42

Three additional broker-dealers reached a $1.6 million settlement with the SEC in January 2007 regarding a subset of these practices.43 In May 2007, the SEC fined Citigroup Global Markets, as successor by merger to Legg Mason Wood Walker, $200,000 for "interven[ing] in auctions by bidding for its proprietary account to prevent failed auctions without adequate disclosure& LMWW submitted bids to ensure that all of the securities would be purchased to avoid failed auctions and thereby, in certain instances, affected the clearing rate."44

In 2007, the Securities Industry and Financial Markets Association (SIFMA) issued "Best Practices for Broker-Dealers of Auction Rate Securities."45 These addressed topics such as the broker-dealer's obligations, bidding by the broker-dealer, bidding by investors, and the relationship between broker-dealers and the auction agent.

The Current Situation: 2007 to the Present

After more than two decades of stable auction-rate market conditions, this market has experienced unusual and difficult conditions in the last several months. These originated with the broader subprime and credit crisis, which the President's Working Group recently described:

Since mid-2007, financial markets have been in turmoil. Soaring delinquencies on US subprime mortgages were the primary trigger of recent events. However, that initial shock both uncovered and exacerbated other weaknesses in the global financial system. Because financial markets are interconnected, both across asset classes and countries, the impact has been widespread& uncertainty about asset valuations in illiquid markets and about financial institutions' exposures to asset price changes left investors and markets jittery.46

Auction-rate markets saw several failures during the second half of 2007; these issues were generally poorly collateralized or had less creditworthy issuers. As early as September 2007, some corporations took write-downs on their auction-rate holdings.47 Through the end of 2007, a few other auction failures occurred, but these were generally believed to be isolated in nature. By late 2007, as defaults on subprime mortgages soared, markets began to question the ability of monoline insurers to support their obligations.48 As a result, the major ratings agencies began to downgrade or review the credit ratings of the monolines. Many of these, such as Ambac, MBIA, FGIC, and XL Capital, are major insurers backing auction-rate bonds.49 If part of a bond's value is attributable to its insurance, and investors believe this insurance has become less valuable, the bond is worth less. In the case of an auction-rate bond, this will be expressed as a higher clearing rate at auction, as investors will demand a higher rate to hold the same bond. If investors demand a rate higher than the maximum rate specified in the bond's official documents, the auction will fail.

By February 2008, rattled by the widening credit crisis and problems at the monoline insurers, auction-rate demand dried up, leading to numerous auction failures. Three days in February alone marked the failure of more than 1,000 auctions.50 A Standard & Poor's analyst commented, "I don't think anyone could have predicted in the winter of 2008 the auction-rate market was going to move away from everybody."51

As seen in Exhibit 7, spreads between ARS rate indices and their typical benchmarks have sharply increased over the last several months.

Response to Current Failures

Issuers: Maximum Rates and Restructuring

While different types of issuers face varying problems in the current environment, they are all generally very focused on the recent auction failures. Responses have naturally been driven by the characteristics of each type of issuer and of their auction-rate issues. We explore related problems and possible responses for two issuer types, municipalities and closed-end mutual funds, below.

Municipal Issuers

Many municipal issuers have seen sharply increased interest payments on their ARS, due to rates resetting to punitive penalty rates after failed auctions and to increased clearing rates in successful auctions. Some municipal issuers entered into floating-for-fixed interest rate swaps at the time of issuance to hedge their interest rate risk and make their total interest payments more predictable (as described in Appendix 2), but for those with fixed penalty rates, the hedges may not be working as initially anticipated.52 Many have no interest rate hedges, working as anticipated or otherwise, and have not budgeted for higher interest costs. Municipalities therefore have strong incentives to restructure their auction-rate debt.

Depending on the terms of the original bond documents, municipal issuers may be able to change the "mode" of their auction-rate securities from "auction mode" to "tender mode." This means the auction-rate security would be restructured into a bond that included a "tender option," for example, a variable-rate demand note. Variable-rate demand notes (VRDNs)53 are short-term variable-rate bonds that include a "hard put" or "tender" option to force either the issuer or a third party agent ("tender agent," usually the sponsoring bank) to purchase the bonds, generally at par, at certain designated times. This liquidity provision occurs via a liquidity facility or a letter of credit and the tender agent effectively provides a liquidity backstop for the VRDN. Interestingly, to create an index for benchmarking use in municipal swaps, SIFMA uses interest rate data from VRDNs.54

Acting with great dispatch, both the IRS and the SEC have responded to help address municipal issuers' current concerns.55 It was important for tax-exempt issuers to get reassurance from the IRS that switching interest rate modes would not trigger retesting of all their various program requirements for tax purposes. In addition, issuers wanted guidance from the SEC that if they self-bid at their own auctions, this would not be prosecuted as market manipulation. The Municipal Securities Rulemaking Board (MSRB)56 issued three recent notices related to auction-rate securities that addressed application of MSRB rules to ARS, a plan for increased reporting of ARS data, and remarketing of auction-rate issues.57 In addition to switching interest rate mode on multi-modal issues, municipal issuers may pursue other possibilities such as holding less frequent auctions.58

While municipalities work furiously to restructure, they may encounter some problems in doing so. Due to recent credit market conditions, many banks are looking to deleverage their own balance sheets,59 potentially making it more difficult for them to offer additional liquidity backstops. Not only have letters of credit become much more expensive in recent months, it may be difficult to obtain one at all without an existing relationship in place.60 Finally, municipal issuers may need to make payments to eliminate interest rate swaps before moving forward with restructuring.

Recent events have not been uniformly negative for municipal issuers. For example, one utility district in northern California restructured its auction-rate bonds at the beginning of 2008 into lower-cost variable-rate financing without bond insurance.61

Closed-End Mutual Funds

While the goal of municipal issuers is clear—to minimize interest costs—closed-end funds that have issued auction-rate preferred stock must grapple with fiduciary duties to both their preferred stock and common shareholders. Some preferred shareholders who are now holding illiquid preferred stock have suggested that the closed-end fund sell assets in order to redeem the preferred at par, thus providing liquidity.62 This may present a conflict, however, if their auction-rate preferred is currently paying a rate below that earned on the assets, as common shareholders benefit from the fund's leverage in this scenario. In addition, when potentially restructuring out of preferred stock into debt, fund advisors must consider the higher regulatory asset coverage required for debt leverage (300%) than for equity leverage (200%).63 NERA's forthcoming paper on closed-end municipal bond funds will further explore the impact of recent events on these issuers.

Corporate Holders: Liquidity, Financial Statement Effects, and Fair Valuation

Hundreds of corporate ARS holders have recently experienced failed auctions.64 This reduced liquidity may (a) cause corporate holders to reassess whether to continue investing in ARS, (b) affect current or future operating or investing decisions while money invested in ARS is inaccessible, and/or (c) impact financial statements due to a different accounting treatment for ARS, potentially including a new methodology for determining fair value. Other ARS-related economic impacts may include stock analyst downgrades, credit rating agency downgrades, and concerns about the ability to meet operating cash flow needs. We further explore the impact on financial statements by examining a recent write-down by Bristol-Myers Squibb.

During the fourth quarter of 2007, Bristol-Myers Squibb (BMS) wrote down the value of its ARS by almost 50%. This impacted its 2007 financial statements in several ways: [1] ARS were reclassified on the balance sheet from current to non-current assets, [2] the value of these assets was adjusted downward, [3] the other-than-temporary portion of this adjustment appeared as an expense on the income statement, and [4] the temporary portion of this adjustment bypassed the income statement and appeared on the balance sheet in other comprehensive income. Disclosures for these four effects are marked below as [1], [2], [3], and [4].

Bristol-Myers Squibb's 2007 10-K describes its ARS holdings:

The Company's investments in ARS represent interests in collateralized debt obligations supported by pools of residential and commercial mortgages or credit cards, insurance securitizations and other structured credits, including corporate bonds. Some of the underlying collateral for the ARS held by the Company consists of sub-prime mortgages.65

Looking back to Exhibit 2, Size and Composition of the Auction-Rate Market, Year End 2007, we can see that BMS's auction-rate securities fall into the "other category," which constitutes approximately 5% of the total auction-rate market. BMS's 10-K also describes some recent problems with these particular holdings:

The ARS& have experienced multiple failed auctions& in the fourth quarter of 2007, $79 million of principal invested in ARS held by the Company were downgraded and others were placed on credit watch.66

As a result, BMS reclassified its ARS holdings:

Historically& ARS were presented as current assets under marketable securities. Given the failed auctions& remaining ARS [in the company's portfolio] ha[ve] been reclassified from marketable securities to non-current other assets [1].67

In addition, BMS wrote down the carrying value of its ARS holdings:

The estimated market value of the Company's ARS holdings at December 31, 2007 was $419 million, which reflects a $392 million adjustment to the principal value of $811 million [2]. Although the ARS continue to pay interest according to their stated terms, based on valuation models and an analysis of other-than-temporary impairment factors, the Company has recorded a pre-tax impairment charge of $275 million in the fourth quarter of 2007, reflecting the portion of ARS holdings that the Company has concluded have an other-than-temporary decline in value [3]. In addition, the Company recorded an unrealized loss of $117 million (pre-tax and net of tax) in accumulated OCI as a reduction in shareholders' equity, reflecting adjustments to ARS holdings that the Company has concluded have a temporary decline in value [4].68

As of 31 December 2007, BMS owned auction-rate securities with a total principal value of $811 million, but it determined that the fair value of these was $419 million at that time. This downward adjustment in value had an "other-than-temporary" portion ($275 million) and a "temporary" portion ($117 million). While FAS 115, Accounting for Certain Investments in Debt and Equity Securities, states that the investor must determine if impairment is temporary or other-than-temporary, it does not define these terms explicitly in terms of a specific length of time.69 An SEC Staff Accounting Bulletin tells us that "other-than-temporary" does not mean "permanent."70 In practice, auditors may use a several month rule of thumb in determining when impairment has taken place.71 In BMS' case, the other-than-temporary portion was part of a line on the income statement called "other expense, net" while the temporary portion appeared in other comprehensive income (OCI) on the balance sheet. Items in OCI bypass the income statement, thereby directly reducing owners' equity.

Finally, Bristol-Myers Squibb describes how it determined the fair value for its ARS, but provides no quantitative analyses or valuation models:

Due to the lack of availability of observable market quotes on the Company's investment portfolio of marketable securities and ARS, the Company utilizes valuation models including those that are based on expected cash flow streams and collateral values, including assessments of counterparty credit quality, default risk underlying the security, discount rates and overall capital market liquidity.72

FAS 157, Fair Value Measurements, effective for fiscal years beginning after 15 November 2007, establishes a hierarchy for the inputs used to determine fair value: "Level 1" (quoted prices in active markets for identical assets or liabilities), "Level 2" (non-Level I inputs that are observable either directly or indirectly), and "Level 3" (unobservable inputs).73 While we cannot say how all investors will treat their various auction-rate holdings, it is clear that, in the absence of observable prices for identical securities, valuation inputs for failed ARS can no longer be considered Level 1 inputs.

Investors

When auctions of their holdings fail, investor responses are generally limited to continuing to hold or attempting to sell in very limited secondary markets. The Financial Industry Regulatory Authority (FINRA) issued an investor alert on 31 March 2008, that outlined four investor options: continuing to hold, selling in the secondary market, borrowing on margin (while continuing to hold), and liquidating other investments (also while continuing to hold).74 If available, secondary market sales are likely to be below par. On 2 April 2008, Barry Silbert of Restricted Stock Partners, one of the few secondary markets for ARS, said the average range of bids on their exchange has been 75 to 95 cents on the dollar.75

On 28 March 2008, UBS announced they would mark down many

ARS in their retail clients' portfolios. More than 90%

would be marked below par in some way, but more than

two-thirds

of auction rates being marked down would be valued at 97% or

better.76 On 31 March 2008, Merrill Lynch told its

brokers that most of its clients' ARS would not be

priced at discounts in

March statements.77

Litigation

While there is some historical precedent for litigation

related to auction failures, the relative stability of the

market had previously discouraged any widespread litigation. In

those cases where auctions failed, broker-customer disputes

were generally resolved at arbitration. Since the onset of

widespread failures in mid-February 2008, many law firms have

filed arbitration claims on behalf of individual investors

similar to the ARS broker-customer disputes seen in the early

1990s. In addition, some law firms have filed complaints

against several broker-dealers and are seeking class action

status. These complaints allege that broker-dealers created an

"artificial market for ARS which would dry up as soon as

these broker-dealers decided to remove themselves from the

auction process."78 In late March 2008, the

Massachusetts Securities Division issued subpoenas to UBS, Bank

of America, and Merrill Lynch. William Galvin, the Secretary of

the Commonwealth, said his office is looking into the

suitability of these investments for individuals, and into the

role the major investment banks played in auction

failures.79 In addition, both the SEC and FINRA have

launched investigations into how broker-dealers marketed

ARS.80 Several other states, including New York, are

also investigating

this market.

Exhibit 8 summarizes auction rate litigation and regulatory investigations announced or filed from

17 January 2008 to 17 April 2008.

Conclusion

The recent failures in the ARS market have adversely affected numerous issuers that have relied on this market in past decades. Many issuers are attempting to restructure their debt, but are paying sharply higher penalty rates in the meantime. For municipal borrowers, higher borrowing costs are ultimately paid for by taxpayers. Impacts on closed-end municipal bond funds are further explored in NERA's forthcoming paper on this topic. Meanwhile, investors holding ARS have found that what they believed was highly liquid may now be a longer-term illiquid investment. Without well-developed secondary markets, holders cannot access their principal when auctions fail. For corporate investors, a general reclassification of ARS from short-term to long-term investments may be necessary and this will impact their financial statements. In addition, auction failures could adversely affect corporate investors' liquidity and leverage ratios.

The legal and regulatory implications may also be substantial. ARS investors may claim that these securities were unsuitable given their investment objectives. Corporate investors may face scrutiny for allegedly investing in inappropriate assets that have been written down, adversely impacting earnings. As these events unfold over the coming months, all parties involved will closely watch the impact of auction failures and the associated legal and regulatory implications. We believe any analysis of auction-rate securities requires close analysis of the particular securities at issue, their individual characteristics, and their markets.

*Consultant, NERA Economic Consulting. I thank Nathan Saperia for extensive collaboration and outstanding research assistance. For encouragement in researching this topic, and discussion of the underlying issues, I thank Robert Mackay and NERA's Global Securities and Finance Practice Chair, Vinita Juneja. I also thank Jeffrey Baliban, Elaine Buckberg, David Tabak, Jake George, James Jordan, Alison Landgraf, Chi Mac, Tom Porter, and Raymund Wong for helpful comments on earlier drafts of the paper and Ying Cao, Nolan Scaperotti, and Kristen St. Martin for excellent research assistance.

Please click on the following link to view "Auction-Rate Securities: Bidder´s Remorse? A Primer in its entirety, inclusive of all charts, footnotes and glossary of terms.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.