On May 3, 2023, by a 3-2 vote, the Securities and Exchange Commission (SEC) adopted amendments to disclosure rules (the "new buyback disclosure rules") relating to repurchases of equity securities by issuers (or repurchases on their behalf), a practice that has continued to attract regulatory attention as the pace and volume of stock buybacks has shown no signs of abating. Despite a brief dip during the COVID-19 pandemic, continued economic uncertainty and a now-effective federal excise tax on stock buybacks that imposes a 1 percent tax on all repurchase activity (net of issuances)1, stock repurchases in 2023 by S&P 500 companies are projected to surpass $1 trillion for the first time, with announced buybacks as of January 2023 already reaching $132 billion, or more than triple the amount from the comparable period last year.

Under the prior disclosure rules, domestic SEC registrants were required to include in their periodic reports on Forms 10-Q and 10-K, tabular disclosure of the monthly aggregate totals for all repurchase activity during the applicable fiscal quarter(s) covered by the report.2 Similar requirements were also previously imposed on Foreign Private Issuers, (FPIs) and registered closed-end management investment companies that are exchange-traded (Listed Registered Closed-End Funds). The new buyback disclosure rules impose substantially enhanced disclosure requirements on each of these classes of issuers, including that: (i) domestic issuers disclose daily repurchase activity (rather than aggregate monthly totals) on a quarterly basis on a new exhibit to be filed with their Form 10-Q and Form 10-K filings, (ii) FPIs disclose such information in annual reports on Form 20-F and quarterly on a new "Form F-SR," (iii) issuers provide narrative disclosure regarding the objectives and rationale of each repurchase plan and all repurchase activity that takes place under such plans and (iv) issuers affirmatively indicate by check box whether any officers or directors have engaged in purchase or sale activity within four business days before or after the public announcement of a new repurchase plan (or an announcement of the increase of capacity under an existing plan).

Although the new amendments will likely invite enhanced scrutiny of share repurchase programs generally, it is notable that the final rules reflect a significant step-back from the even more onerous requirements contemplated by the SEC's original rule proposal, which, for example, would have imposed a next-day reporting obligation with respect to all repurchase events. The SEC's press release announcing the adoption of the final rules is available here and the text of the adopting release and a summary fact sheet are available here and here. The final rules will become effective 60 days after their publication in the Federal Register.

An overview of the material features of the new share repurchase disclosure amendments and certain considerations for issuers going forward is provided below:

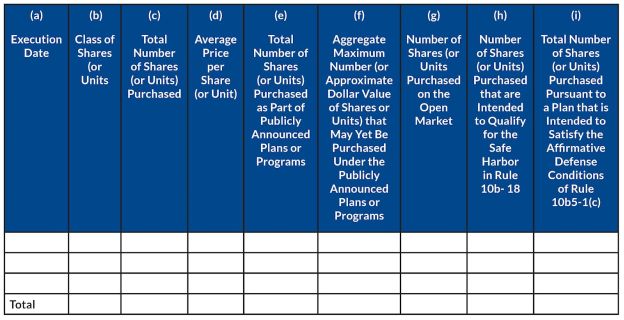

- Quarterly Reporting of Daily Repurchase

Activity. The new buyback rule requires quarterly

reporting by an issuer of daily repurchase data. The disclosure

must be presented in a tabular format on a new Exhibit 26 to a

company's periodic reports on Form 10-Q and Form 10-K,

beginning with the first full quarter that starts on or after

October 1, 2023 (i.e., for domestic issuers with a December 31

fiscal year-end, beginning with their upcoming 2023 Form 10-K

filing). Later effective dates apply for FPIs and Listed Registered

Closed-End Funds, but there are no delays or phase-in periods for

other categories of registrants, such as smaller reporting

companies. An example of the newly-required tabular disclosure,

which must be provided in XBRL-tagged format, is presented

below:

- Narrative Disclosure. In addition to the

tabular disclosure described above, under the new rule, each

company will also be required to disclose, with corresponding

references to the relevant activity in the tabular disclosure: (i)

the objectives and/or rationales for each share repurchase plan or

program, (ii) the process used to determine the amounts of any

repurchases that occurred under the relevant plan, (iii) the number

and nature of any share repurchases that occurred other than

through a publicly announced program (such as pursuant to equity

compensation arrangements) and (iv) any policies, procedures or

restrictions relating to the purchases or sale of equity securities

by its officers and directors during a repurchase program. This

disclosure is in addition to existing requirements that a company

disclose: (a) the date each of its existing repurchase plans was

publicly announced and went into effect, (b) the dollar or share

amounts approved for repurchase with respect to such plans, (c) the

expiration date of such plans and (d) each plan that has expired in

the relevant period or under which the company does not intend to

make any further purchases.

- Indication of Director or Officer Purchases or Sales

Within Four Business Days of Plan Announcement. The

amendments also require that an issuer indicate by a checkbox

preceding the tabular disclosure whether any officer or director

subject to reporting requirements under Section 16(a) of the

Securities Exchange Act of 1934 (Exchange Act) purchased or sold

shares that were the subject of the issuer's publicly-announced

repurchase plan within four business days before or after the

company's announcement of such plan (or its announcement of an

increase of repurchasing capacity under the relevant plan). In

determining whether to check the box for this purpose, domestic

issuers are permitted to rely upon Section 16 filings (on Forms 3,

4 and 5) made by "Section 16" officers and directors.

Since FPIs' officers and directors are not subject to reporting

requirements under Section 16(a), FPIs will be required to ask

their directors and members of senior management to provide

relevant written representations to assist FPIs in preparing and

verifying their related disclosure. The SEC noted that additional

disclosure that provides explanatory context with respect to any

such activity may be included if the company believes such

disclosure would be helpful to investors.

- Issuer 10b5-1 Trading Plans. In connection

with their buyback programs, many companies adopt 10b5-1 trading

plans, which, if properly adopted and executed, are designed to

provide an issuer with an affirmative defense to insider trading

claims relating to an issuer's purchase of securities.

Consistent with the SEC's December 2022 adoption of amendments

to disclosure requirements with respect to Rule 10b5-1 trading

plans adopted by officers and directors (Katten's previous

coverage of which is available here), the new buyback rule requires a company

that adopts, modifies or terminates a Rule 10b5-1 trading plan to

disclose the date on which it adopted, modified or terminated the

plan, the duration of the plan, and the aggregate number of shares

to be purchased or sold under the plan in its filings on Form 10-Q

and Form 10-K. Note that, in contrast to the recent rule amendments

applicable to officers and directors (and in a step back from

previous iterations of the buyback disclosure rule proposals

applicable to issuers which had included them), the SEC declined to

impose under the new buyback disclosure rules additional conditions

on the availability of the Rule 10b5-1 affirmative defense with

respect to Rule 10b5-1 plans adopted by issuers, such as requiring

a cooling-off period or limiting the use of overlapping

plans.

- Foreign Private Issuers. The new rules require

that FPIs (other than FPIs that are eligible to utilize the

US-Canadian Multijurisdictional Disclosure System (MJDS)) provide

the tabular disclosures described above of aggregate daily

repurchase activity on a quarterly basis on new Form F-SR,

beginning with each FPI's first full fiscal quarter that begins

on or after April 1, 2024. The new rules replace the current

requirements under Item 16E of Form 20-F to disclose monthly

repurchase data. The disclosure requirements apply to any FPI that

has a class of equity securities registered pursuant to Section 12

of the Securities Exchange Act and does not file Forms 10-Q and

10-K (e.g., because it instead files Forms 6-K and 20-F). New Form

F-SR must be filed within 45 days of the FPI's fiscal quarter

end. Additionally, the narrative disclosure requirements described

above must be included in Form 20-F filings subsequent to the

effective date and after the FPI's first Form F-SR has been

filed.

- MJDS-Eligible Issuers. Since MJDS-eligible

issuers are subject to a separate reporting regime that is, in most

respects, governed by Canadian disclosure requirements promulgated

by Canadian securities regulatory authorities, the SEC declined to

extend the new buyback disclosure rules to MJDS-eligible

issuers.

- Listed Registered Closed-End Funds. Listed Registered Closed-End Funds are required to provide the tabular and narrative disclosures described above semi-annually, beginning with the Form N-CSR that covers the first six-month period that begins on or after January 1, 2024. However, closed-end investment companies that elect to be regulated as business development companies under the Investment Company Act of 1940, as amended, will need to comply with the reporting requirements that apply to all registrants that file periodic reports on Form 10-K and Form 10-Q.

Considerations Going Forward

Agreements with intermediaries. In light of the new buyback disclosure rules, companies should evaluate their existing internal processes and procedures for collecting and reporting data related to share repurchases, including consulting with the agents and broker-dealers administering the execution of such repurchase programs on their behalf to ensure they are able to track and populate all of the information required to be disclosed (for example, whether any trading activity by directors and officers has occurred within four business days before or after a plan announcement as discussed above). Companies may wish to review the agreements in place with these intermediaries and update the agreements if necessary to ensure any additional required information by the issuer for compliance purposes is obligated to be provided.

Considerations around narrative disclosures. Companies will also need to carefully consider the content of their narrative disclosures with respect to repurchase activity and, specifically, the requirement that the "objectives or rationales" underlying their share repurchase plans and activity be disclosed. It is recommended that a company's board of directors carefully evaluate these matters and record the criteria and rationale behind their buyback programs in their board and committee meeting minutes and resolutions. In the SEC's adopting release, the SEC noted that the provision of "boilerplate disclosure" regarding objectives or rationales would not be considered sufficient and that repurchase plans and events must be analyzed on a case-by-case basis to ensure that any related disclosures are accurate (which may require the provision of multiple objectives or rationales in the event of multiple plans and/or multiple purchases under singular or multiple plans). The SEC highlighted the following areas as potentially helpful contextual information issuers may wish to disclose:

- The source of funds for the repurchase and the decision to use such funds for repurchases as opposed to other expenditures.

- The anticipated impact of the repurchases on the value of remaining shares.

- Whether the issuer believes its stock is undervalued at the time of repurchase.

Compliance and training measures. To ensure compliance with the new buyback disclosure rules, companies may wish to consider establishing specific disclosure controls, including quarterly reviews of repurchase disclosure. It may also be appropriate to establish or supplement periodic training programs for management and directors that engage with the public (for example, on earning calls) regarding the contours of the new rules, in order to ensure that the nature and content of their dialogue is consistent with the company's existing disclosure and that proper controls regulating the timing and nature of their trading activity is monitored. Issuers may also wish to consider whether updates to their insider training policies prohibiting trading activity within the four business days before or after an announcement of a new repurchase program is appropriate, given the new requirement that issuers indicate via check box whether such activity has occurred.

Strategic timing considerations. Given the increased amount of information that will be available regarding repurchase plans and activity, and the increasingly granular nature of such information, companies should expect increased scrutiny of both their existing plans and of specific repurchases from regulators and the public. As a result, thought should be given to both the timing and optics of announcements with respect to repurchases, the plans themselves, and specific repurchase events, particularly when sale or purchase activity by prominent insiders may overlap with activity under an issuer's repurchase plan, to avoid suggestions of impropriety.

Footnotes

1. The 1 percent federal excise tax on stock buybacks does not apply, among other exemptions, to repurchases by a regulated investment company (as defined in Section 851 of the Internal Revenue Code of 1986, as amended) or a real estate investment trust.

2. See Item 703(a) of Regulation S-K and Item 16E of Form 20-F. Previously, Foreign Private Issuers were required to report such information in Form 20-F filings with respect to each month in the fiscal year covered by such report. Registered closed-end management investment companies that are exchange-traded were also required to disclose such share repurchase activity, semi-annually on Form N-CSR.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.