- within Litigation and Mediation & Arbitration topic(s)

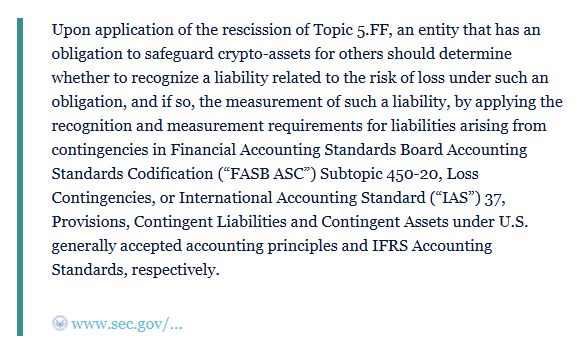

On January 23, 2025, the SEC staff issued SAB 122, which rescinds the interpretive guidance previously found in SAB 121. That earlier guidance required companies holding crypto-assets for customers to recognize both a safeguarding liability and a corresponding asset. By rescinding it, the SEC staff directs entities back to the established requirements in ASC 450-20 (US GAAP) or IAS 37 (IFRS) for assessing whether and when a liability should be recognized.

Key points from SAB 122 include:

- Retroactive Application: Entities must remove SAB 121's accounting treatments and apply the rescission fully retrospectively in annual periods beginning after December 15, 2024 (with optional earlier adoption).

- Use of Existing Contingency Guidance: Instead of automatically recognizing safeguarding liabilities, companies must evaluate whether a loss contingency exists under ASC 450-20 or IAS 37.

- Disclosure Obligations Remain: The SEC staff stresses that entities should continue providing clear and thorough disclosures about risks, obligations, and uncertainties related to safeguarding crypto-assets.

Companies should review their financial statements to determine whether previously recorded safeguarding assets and liabilities need to be adjusted. As they revert to traditional contingency frameworks, organizations must still address how safeguarding risks and obligations are disclosed to meet investor and regulatory expectations.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.