- within Corporate/Commercial Law topic(s)

- in United States

- with readers working within the Business & Consumer Services industries

- within Employment and HR topic(s)

Despite federal pullback on ESG requirements, state and international ESG mandates persist, with new obligations coming into play in 2026. For corporate directors and ESG officers, compliance failures may carry both financial penalties and potential personal liability under established legal standards.

Corporate board members should ask themselves: What are the legal obligations here? Does the board and the C-suite understand ESG in today’s environment? Are there still compliance obligations given the current administration’s stance? What actions does my company need to take in 2026?

Even without US federal mandates, companies have reporting and other obligations under state and international law. For example, Thousands of US companies doing business in California and meeting certain revenue thresholds are subject to California's climate disclosure laws following the California Air Resources Board’s (CARB’s) issuance of proposed reporting regulations. And these reporting deadlines are quickly approaching. While the January 1st statutory reporting deadline for climate-related financial risk has been paused due to ongoing litigation, CARB plans to set a new deadline when the litigation has been resolved.1 Additionally, GHG emissions reporting deadlines remain set for August 2026.

This guide provides additional details on what you need to know now: immediate deadlines, reporting frameworks, legal obligations and practical next steps.

1. What Exactly Is “ESG” Anyway?

The phrase “environmental, social and governance” — or “ESG” — first gained prominence following a 2004 United Nations report commissioned by then-U.N. Secretary General Kofi Annan.2

The report presented information from the financial industry on how “to better integrate environmental, social and governance issues in analysis, asset management and securities brokerage.”3 Since then, ESG has become a charged acronym, but its components are less controversial.

The “E” in “ESG” represents a broad swath of environmental concerns, including climate change, greenhouse gas emissions and other environmental matters.4 These issues are often referred to by the term “sustainability.” A famed 2014 Harvard Business School study found corporations that voluntarily adopted sustainability policies were more likely to engage with stakeholders, had a longer-term investor base and significantly outperformed their counterparts over long-term periods, in terms of both accounting rates of return and stock market performance,5 though many have questioned these conclusions. As some scholars have put it: “Even shareholders bent on maximizing wealth would want to avoid the systemic risk of harm that climate change could wreak on the economy.”6

The “social” component includes attention to labor practices, talent, data privacy, diversity, inclusion, sexual discrimination and relationships in local communities.7 “Governance” includes executive and board compensation, internal audits and controls, anti-corruption and shareholder rights.8 In short, then, the ESG framework appears to include just about all aspects of a company excluding perhaps share price. Because of the breadth of ESG topics, we focus the remainder of this paper on sustainability issues that fall within the ESG scope.

2. What Are the Controlling Organizations and Basic Concepts in Sustainability Reporting?

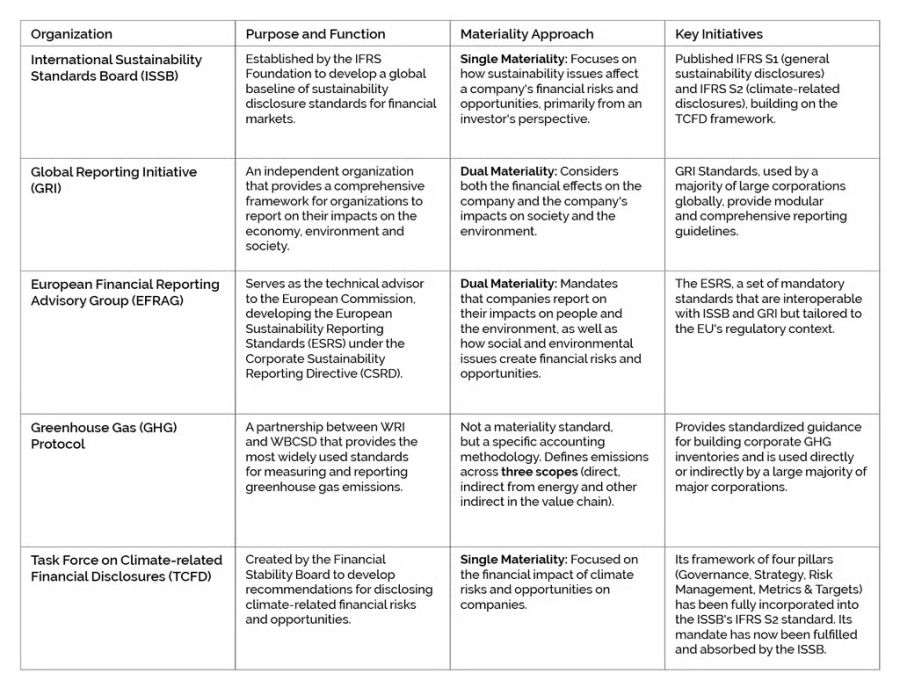

Two key issues involving sustainability reporting relate to the scope of (1) climate-related risks that need to be disclosed and (2) emissions that need to be reported. Regarding the first category, a key concept is the distinction between “single” and “dual” materiality in the sustainability reporting context. Single materiality reporting focuses on how climate risks impact an organization’s financial performance. Dual materiality, on the other hand, includes an assessment of the reverse: how a company’s operations contribute to climate change.

When considering reporting of greenhouse gas emissions, a fundamental distinction is that between Scope 1, 2 and 3 emissions:

Scope 1

Emissions directly originating from sources owned or controlled by a company, like when a company burns fuel in its own vehicles or facilities.

Scope 2

Indirect emissions resulting from the energy a company purchases and uses, like the energy a company pays for to heat its buildings.

Scope 3

Emissions that are neither produced by the company itself nor directly from its assets, but that arise from activities along the company’s value chain; like the emissions associated when a company buys, uses, or disposes of products from its suppliers.

Aside from these basic concepts, it’s helpful to have a basic understanding of the alphabet soup of organizations and standards involved in sustainability reporting. Some of the key organizations and standards are listed in this table.

3. What Does California Require From Companies for Sustainability Reporting?

At the federal level, the Trump administration has broadly backed away from ESG and sustainability initiatives. Perhaps most prominently, the current SEC has withdrawn from defending in court climate disclosure requirements that were advanced by the Biden administration. While the Biden SEC climate disclosure rule has not yet been formally rescinded, it has been voluntarily stayed pending the litigation, and the expectation is that the Trump administration will repeal the rule even if it survives legal challenges. In another, in April 2025, President Trump issued an executive order directing the US Attorney General to investigate and block enforcement of state laws promoting ESG policies, based on the premise that such laws conflict with national security and economic interests.9 The Department of Labor also recently ended its defense of a 2022 rule permitting ERISA fiduciaries to consider ESG factors when selecting among financially equal investment options.10

California, in contrast, largely persisted in its climate disclosure efforts. CARB approved the proposed initial reporting requirements package on February 26, 2026.11

In fact, the initial deadline for reporting climate-related financial risk (as explained further below) largely persisted in its climate disclosure efforts. CARB approved the proposed initial reporting requirements package on February 26, 2026,12 but has been paused due to ongoing litigation. While CARB intends to set a new deadline upon resolution of the litigation,13 more than 120 climate-related financial risk reports have already been voluntarily submitted and made publicly available.14

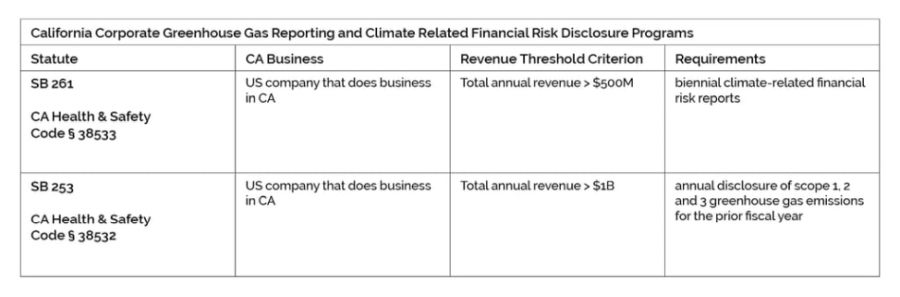

The August 10, 2026, deadline for GHG reporting, however, remains just months away.15 If a company does business in California and hits certain revenue thresholds, it will need to comply with California’s rules found in the Climate Accountability Package.

This full GHG reporting legislative bundle includes: (1) The Climate Corporate Data Accountability Act (SB 253),16 which requires companies that do business in the state and have over $1 billion in revenue to annually report Scope 1 and 2 emissions starting in August 2026, and Scope 3 emissions starting in 2027. (2) The Climate-Related Financial Risk Act (SB 261),17 which requires biennial financial disclosures on climate-related risks for US-organized companies doing business in California with total annual revenues exceeding $500 million. The law also requires reports on how the company is adapting to reduce these risks. The initial SB 261 disclosure deadline will be announced by CARB following resolution of ongoing litigation, if the legislation survives the legal challenge.

Initially, following a series of public workshops and input from stakeholders regarding key definitions related to the applicability of both disclosure laws, CARB released a list on identifying which entities the agency believes are subject to the state’s climate disclosure programs. CARB used existing databases of US-based companies including the California Secretary of State Business Entity database, to identify companies “doing business in California” that meet the annual “revenue” thresholds requirements, resulting in thousands of companies being captured in the list. Links to the applicability list, ESG reporting guidance and stakeholder comment forum are included in a recent article written by environmental attorneys at Bracewell LLP: Are You on the List? CARB Releases List of Entities Subject to Climate Disclosure Laws.

However, following stakeholder feedback, CARB has changed is approach to defining “doing business in California” in the proposed rules. Moving away from reliance on California Secretary of State’s registration databases, CARB’s proposed rules reference California Revenue and Taxation Code definitions.18 In turn, an entity is “doing business in California” if it is actively engaging in any transaction for the purpose of financial gain or profit and meeting either of the following conditions during any part of a reporting year: (1) the entity is organized or commercial domiciled in California or (2) the entity’s sales in California, as defined in Revenue and Taxation Code 25120(e) or (f), exceed the inflation-adjusted threshold of $735,019 (for 2024). For purposes of the revenue thresholds, Entities revenue amount is now determined by the lesser of entity’s two previous fiscal years of revenue. [SS1] CARB made this change to account for the “potentially large annual changes in revenue that can occur from selling property or corporation assets . . ..”19

Under California SB 261, corporate disclosures must be made in conformance with the Final Report of Recommendations to the Task Force on Climate-related Financial Disclosures (June 2017) (published by the TCFD or any successor) or the International Financial Reporting Standards Sustainability Disclosures Standards (IFRS S2) frameworks.

Alternatively, reporting entities may use any disclosure/reporting framework that is developed in accordance with any regulated exchange, national government or other governmental entity, including a law or regulation issued by the US government.20

CARB has provided initial guidance by way of a “draft checklist” for reporting entities providing the minimum requirements for disclosure.21

The first report under SB 253, covering Scope 1 and Scope 2 emissions, is due by August 10, 2026, with Scope 3 emissions reporting beginning in 2027. Reporting entities will initially be required to obtain an assurance (i.e., verification) engagement performed by an independent third-party assurance provider for Scope 1 and 2 emissions at a limited-assurance level. CARB proposed that by 2030, reporting entities must obtain reasonable-assurance engagements.22 However, CARB explained during its February 26, 2025, Board Meeting, that it plans to conduct future rulemaking to establish expanded GHG emissions reporting for 2027 and onward, as well as more stringent data assurance requirements.23 CARB has suggested several standards for developing the assurance concept, including ISSA 5000, AA1000, ISO 14060 and AICPA — but remains open to public feedback on this concept.24

These deadlines come after a 2024 law25 delayed the release of the implementation guidelines to mid-2025, as well as a 2024 CARB enforcement notice that instructs that the agency would not pursue enforcement against covered entities for incomplete reporting in 2026, provided certain conditions were met.26

Both laws faced significant opposition from a broad range of stakeholders concerned about the scope and impact of the new disclosure requirements. A coalition led by the US Chamber of Commerce challenged the constitutionality of SB 253 and SB 261, arguing that the laws violate the First Amendment.27 The US District Court for the Central District of California denied the coalition’s motion for a preliminary injunction.28 However, on appeal, the US Court of Appeals for the Ninth Circuit granted an injunction pending appeal on November 18, 2025, in a one-page order, thereby suspending enforcement of SB 261.29 The Ninth Circuit declined to enjoin SB 253, leaving its implementation on track.30 Accordingly, companies must prepare to comply with SB 253’s reporting requirements, including the first Scope 1 and Scope 2 emissions report due August 10, 2026. The Ninth Circuit will heard oral arguments on January 9, 2026. If the Ninth Circuit affirms the district court’s denial of a preliminary injunction for SB 261, it will dissolve its appellate injunction, allowing CARB to reinstate enforcement of SB 261’s obligations.

4. What Do I Need to Know About International ESG/Sustainability Commitments? How Do They Impact My Business and Decision-Making?

International ESG commitments are important for two reasons. First, any corporation with an international presence will need to be informed of other nations’ sustainability commitments to which it might be bound. Second, while the United States is pulling back on sustainability reporting requirements, the European standards suggest where reporting may return in the event of a future administration change.

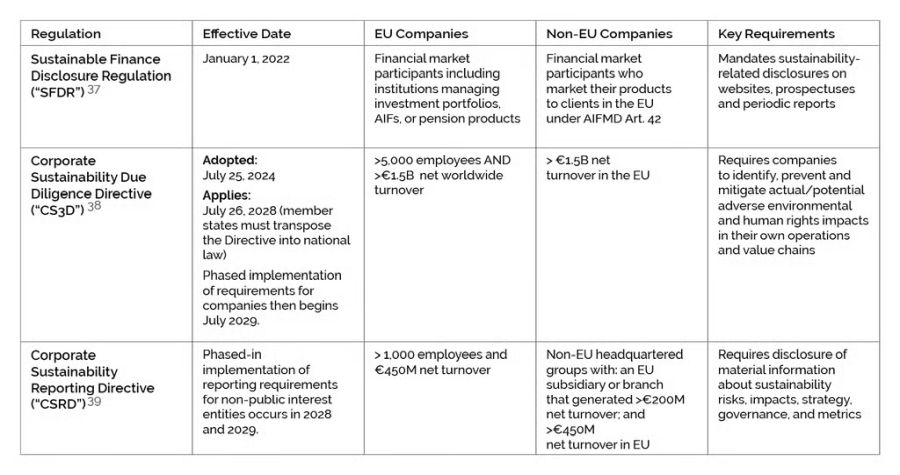

The EU Taxonomy provides a classification system that defines criteria for economic activities that are aligned with a net zero trajectory by 2050 and other broader environmental goals.31 Below is a table providing an overview of the most prominent EU sustainability and ESG regulatory requirements:

The obligations included in the chart below reflect the amendments adopted by the European Parliament in December 2025 pushing back the original implementation deadlines for these directives.32

These changes came after a months-long push by many EU lawmakers to revise the applicability and scope of the requirements via an “Omnibus I” legislative package.33 These proposed changes have come at a time when the US continues to increase pressure for the EU to pare back requirements impacting US companies.34 The European Council voted to adopt the text on February 24, 2026.35 The Official Journal of the EU will publish the text, 20 days after which it will come into force.36

5. So, What Now? Where Does This Leave My Company and Me?

For companies seeking to continue to engage in sustainability reporting, there are a number of options for implementing appropriate governance systems and keeping up to speed on the changing ESG landscape in the United States and abroad. For example, a board may choose to appoint a Chief Sustainability Officer, aligned with a dedicated sustainability board committee, who institutionalizes sustainability responsibility. Another option is to start by publishing an annual sustainability report benchmarked against industry peers, demonstrating a commitment to transparency and responsible business practices. According to some scholars, “it seems much more effective and efficient to make sure that committee-level responsibility for risk management and compliance is thoughtfully allocated among the board’s committees, rather than solely vested in the audit committee.”40

In any event, legal counsel will play a critical role if your company is trying to determine whether they are subject to any state, federal or international ESG reporting requirements, or if your company is evaluating the legal sufficiency of prepared ESG disclosures. Additionally, engaging with third-party environmental consultants to assist in the gathering, distilling and preparation of ESG data needed to prepare disclosures will help ensure that any ESG reporting process runs smoothly.

Whatever the starting point, there is opportunity when ESG is not merely treated as a checklist item, but as a driver of long-term value. Boards set the tone.

6. Do Corporate Directors Have a Standard of Care Regarding ESG?

Yes, as long as ESG-related compliance obligations are legally mandated, courts have found that directors have a duty to police compliance.

Just as Sarbanes-Oxley compliance establishes personal liability for directors for failure of internal financial controls, so too exists precedent for personal board liability in the realm of ESG. Where existing legislation and regulations impose compliance obligations in ESG-related areas, boards must follow the Caremark standard. Established under In re Caremark41 in the Delaware Court of Chancery, directors owe “a duty to attempt in good faith to assure that a corporate information and reporting system, which the board concludes is adequate, exists.” Failure to do so exposes directors to personal liability for losses caused by non-compliance.42 Indeed, Caremark itself resulted in criminal investigations and indictments, fines, penalties and other costs to the company totaling over $250 million.43 In turn, plaintiffs sought to recover these losses from individual board directors resulting in a settlement approved by the court.44

Caremark imposes two related but distinct duties on board members. These duties are to (1) implement systems of controls to prevent unlawful misconduct and (2) monitor such systems or controls. Failure to adequately discharge either duty can result in personal liability for the board member. In Marchand v. Barnhill,45 the Delaware court made clear that under Caremark, a board must make a “good faith effort” to monitor the company’s central compliance risks, or its “essential and mission critical” operations.46 Following the Marchand decision, Caremark claims have “bloomed like dandelions after a warm spring rain.”47 At least half a dozen Caremark claims have succeeded over the past four years.48

A number of ESG-related compliance obligations in the sustainability sphere may trigger Caremark duties. These could take the form of federal, state or international obligations.

For example, if the SEC’s proposed ESG Rules49 or new iterations return, boards may face liability via heightened exposure to shareholder claims that directors failed to properly oversee or mitigate climate-related risks for “mission-critical” aspects of their business. For example, if the board of a company that emits significant GHG emissions lacks climate-related expertise, a shareholder may attempt to use this allegation to show failure to competently monitor a “mission-critical” aspect of the business. Even absent stringent federal sustainability standards, however, if a covered entity with significant reporting requirements under a state or international standard fails to establish appropriate reporting processes due to a wrongful assumption that these obligations vanished with the SEC’s roll-back, it is plausible that shareholders could bring a derivative claim that board members “utterly failed to implement” any controls for known sustainability requirements. Scholars have posited that at least one EU sustainability directive “may significantly increase the exposure of directors and officers to oversight claims,”50 and that the “combination of ambitious European regulation and robust US (read Delaware) private litigation landscape may result in American directors and officers facing scrutiny over how involved they were in preventing or reducing adverse effects on human rights and the environment.”51

While Caremark was a Delaware court decision, it is possible that other jurisdictions will in the future update board compliance duties similar to Caremark. While the emphasis of these duties may not be in the sustainability space, any board obligation to monitor regulatory compliance could kick in when sustainability requirements become law.

Conclusion

While recent US federal legal and policy developments might suggest that ESG is no longer a significant issue for corporate directors, the combination of state and international sustainability requirements mean that directors may have continued obligations in the ESG space. Most immediately, directors of companies that may be doing business in California should seek to understand the applicability of California’s requirements and the nature of reporting required. US companies should further consider their European sustainability disclosure requirements. The Caremark standard means that it behooves directors to implement a system to comply with sustainability requirements despite the current trend in federal law.

Co-Authored by Matthew R. McBrady, Ph.D., is an independent investor, board member and senior advisor to public companies, venture-backed startups, hedge funds and non-profit impact investors. He was a professor at the University of Virginia’s Darden School and is currently CFO at Gopuff.

Elsie Bencke and Sarah Templeton served as research assistants.

Foonotes

1. See CARB, Enforcement Advisory (December 1, 2025).

2. THE GLOB. COMPACT, UNITED NATIONS, WHO CARES WINS: CONNECTING FINANCIAL MARKETS TO A CHANGING WORLD (2004).

3. Who cares wins : connecting financial markets to a changing world (English), WORLD BANK GRP. (last visited July 14, 2025), https://documents.worldbank.org/en/publication/documents-reports/documentdetail/280911488968799581/who-cares-wins-connecting-financial-markets-to-a-changing-world.

4. Fairfax, supra note 7, at 282.

5. Nicholas C. Lynch & Michael F. Lynch, Why Sustainability Reporting Matters to Investment Decisions, 40 J. TAX’N INV. 55 (2022) (citing Robert G. Eccles, Ioannis Ioannou & George Serafeim, The Impact of Corporate Sustainability on Organizational Processes and Performance, 60 MGMT. SCI. 2835 (2014), http://www.jstor.org/stable/24550546).

6. Grant M. Hayden & Matthew T. Bodie, A Democratic Participation Model for Corporate Governance, 109 MINN. L. REV. 1579, 1650 (2025) (citing Madison Condon, Externalities and the Common Owner, 95 WASH. L. REV. 1, 17 (2020) (describing how systemic risks such as climate change pose a threat to wealth maximization)).

7. McHugh, supra note 3, at 251.

8. Gareth McHugh, From Director Liability to Officer Liability to ESG Caremark Claims: A Natural Evolution?, 10 EMORY CORP. GOVERNANCE ACCOUNTABILITY REV. 249, 251 (2023) (citing Megan Baroni & Jonathan H. Schaefer, What is ESG and How Could It Impact You?, 12 NAT’L L. REV. 309 (2022)).

9. Exec. Order No. 14260, 90 Fed. Reg. 15513 (2025).

10. Defendant’s Status Report, Utah v. Chavez-DeRemer, No. 23-11097 (5th Cir. 2025).

11. See CARB Press Release, CARB approves climate transparency regulation for entities doing business in California (Feb. 26, 2026), available at https://ww2.arb.ca.gov/news/carb-approves-climate-transparency-regulation-entities-doing-business-california. The Board Meeting approving initial reporting requirements and related definitions can be accessed here: https://cal-span.org/meeting/carb_20260226/. The next step following approval is for CARB to respond to public comments and submit the final package to the Office of Administrative Law. Then CARB can commence implementation of fees and first-year GHG reporting deadlines for SB 253 (and later SB 261 depending on litigation outcomes.

12. CA Health & Safety Code § 38533(c)(1).

13. See CARB, Enforcement Advisory (December 1, 2025).

14 See CARB, Climate-Related Financial Risk Reports (SB 261) Docket, available at https://ww2.arb.ca.gov/approved-comments?entity_id=47456.

15 Cal. Code Regs. tit. 17, § 96206 (Proposed Dec. 1, 2025). See also CARB, Staff Report: Initial Statement of Reasons (Dec. 9, 2025) https://ww2.arb.ca.gov/sites/default/files/barcu/regact/2025/sb253-261/isor.pdf; see CARB Press Release, CARB approves climate transparency regulation for entities doing business in California (Feb. 26, 2026), available at https://ww2.arb.ca.gov/news/carb-approves-climate-transparency-regulation-entities-doing-business-california (approving August 10, 2026 deadline for SB 253 first-year reporting for Scope 1 and Scope 2 emissions).

16. Cal. Health & Safety Code § 38532 (2024). Often referred to as “SB 253” or the “California Corporate Greenhouse Gas Reporting Program.”

17. Cal. Health & Safety Code § 38533 (2024). Often referred to as “SB 261” or the “Climate Related Financial Risk Disclosure Program.”

18. See CARB Presentation at Feb. 26, 2026 Board Meeting, Proposed California Corporate Greenhouse Gas Reporting and Climate-Risk Financial Risk Disclosure Initial Regulation at 9, available at https://cal-span.org/meeting/carb_20260226/.

19. Id.

20. CA Health & Safety Code § 38533(b)(1)(A)(i), (b)(3).

21. See CARB, Climate Related Financial Risk Disclosures: Draft Checklist (Sept. 2, 2025).

22. See CARB Public Workshop (Aug. 21, 2025) (slide deck).

23 See CARB Presentation at Feb. 26, 2026 Board Meeting, Proposed California Corporate Greenhouse Gas Reporting and Climate-Risk Financial Risk Disclosure Initial Regulation at 19, available at https://cal-span.org/meeting/carb_20260226/.

24. See CARB, California Corporate Greenhouse Gas Reporting and Climate-Related Financial Risk Disclosure Programs: FAQs Related to Regulatory Development and Initial Reports (Jul. 9, 2025); CA Health & Safety Code § 38532(c)(2)(F)(ii).

25. See CARB Public Workshop (Aug. 21, 2025) (slide deck).

26. Cal. Health & Safety Code §§ 38532–38533 (2024), as amended by 2024 Cal. Stat. ch. 766 (S.B. 219).

27. California Air Resources Board, The Climate Corporate Data Accountability Act Enforcement Notice (Dec. 5, 2024), https://ww2.arb.ca.gov/sites/default/files/2024-12/The Climate Corporate Data Accountability Act Enforcement Notice Dec 2024.pdf (noting covered entities must (1) demonstrate good faith efforts to comply with the law and (2) base their initial reports on information the entity already possessed or was collecting as of the date of the enforcement notice).

28. See Complaint for Declaratory and Injunctive Relief, US Chamber of Com., et al. v. Randolph, No. 2:24-cv-00801 (C.D. Cal. Jan. 30, 2024).

29. US Chamber of Com., et al. v. Randolph, No. 2:24-cv-00801-ODW (PVCx) (C.D. Cal. Sept. 11, 2025) (order denying plaintiffs’ motion for preliminary injunction).

30. US Chamber of Com., et al. v. Randolph, No. 25-5327 (9th Cir. Nov. 18, 2025) (order granting injunction pending appeal in part).

31. European Commission, EU taxonomy for sustainable activities, https://finance.ec.europa.eu/sustainable-finance/tools-and-standards/eu-taxonomy-sustainable-activities_en#eu-taxonomy-navigator (last visited July 23, 2025).

32. See EU Parliament Press Release, Simplified sustainability reporting and due diligence rules for business (Dec. 16, 2025), https://www.europarl.europa.eu/news/en/press-room/20251211IPR32164/simplified-sustainability-reporting-and-due-diligence-rules-for-businesses.

33. Omnibus I documents are available at https://commission.europa.eu/publications/omnibus-i_en.

34. See e.g., Alice Hancock, Henry Foy, and Andy Bounds, US demands EU dismantle green regulations in threat to trade deal, Financial Times (Oct. 8, 2025), https://www.ft.com/content/678f7c25-2eff-4e98-9c7c-e0772fa69236.

35. ESG Today, EU States Give Final Approval to Omnibus Package to Cut Sustainability Reporting and Due Diligence Requirements.

36. See EU Parliament Press Release, Simplified sustainability reporting and due diligence rules for business (Dec. 16, 2025), https://www.europarl.europa.eu/news/en/press-room/20251211IPR32164/simplified-sustainability-reporting-and-due-diligence-rules-for-businesses.

37. 2024 O.J. (L. 317) 1 (available at https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32019R2088).

38. European Commission, Corporate sustainability due diligence, https://commission.europa.eu/business-economy-euro/doing-business-eu/sustainability-due-diligence-responsible-business/corporate-sustainability-due-diligence_en (last visited June 6, 2025). The directive can is available at https://eur-lex.europa.eu/eli/dir/2024/1760/oj. Amended texts adopted by EU Parliament still waiting formal approval by EU Council available here: https://www.europarl.europa.eu/doceo/document/TA-10-2025-0324_EN.html#title2.

39. 2025 O.J. (L.322) 15 (available at https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022L2464).

40. Strine, Smith & Steel, supra note 4, at 1917.

41. 698 A.2d 959, 970 (Del. Ch. 1996).

42. Id.

43. Id. at 960-61.

44. Id. at 960-961, 972.

45. 212 A.3d 805 (Del. 2019).

46. Id. at 824.

47. Constr. Indus. Laborers Pension Fund v. Bingle, 2022 Del. Ch. LEXIS 223, *3 (Del. Ch.), aff’d, 297 A.3d 1083 (Del. 2023).

48. Roy Shapira, Mission Critical ESG and the Scope of Director Oversight Duties, 2022 COLUM. BUS. L. REV. 732, 736 (2023).

49. See infra “5. That sounds like it’s all about Europe and its standards—are there any emerging standards applicable to US companies more specifically?”.

50. Luca Enriques, Matteo Gatti & Roy Shapria, How the EU Sustainability Due Diligence Directive Could Reshape Corporate America, 78 STANFORD L. REV. (forthcoming 2026) (manuscript at 51).

51. Id. at 6 (emphasis in original).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]