- within Finance and Banking topic(s)

- in Ireland

- with readers working within the Banking & Credit industries

- within Finance and Banking, Consumer Protection, Media, Telecoms, IT and Entertainment topic(s)

On March 19, 2026, the federal banking agencies issued a package of proposed changes to the regulatory capital requirements for banking institutions of all sizes, from the largest GSIBs and super-regional banks to community banks (the “Proposed Rules”). This package of proposals is a second full attempt at implementing the 2017 “Basel III Endgame” international framework—following the agencies’ initial package of proposals in July 2023 (the “2023 NPR”)—to better reflect credit, trading and operational risk in the calculation of minimum regulatory capital ratios. If finalized, the rules would mark the culmination of a nearly decade-long effort to complete the fundamental overhaul of bank capital requirements initially spurred by the 2008-2009 financial crisis.

Given the complexity of the sProposed Rules, it will take time to fully absorb their potential implications. Below are high-level take-aways from the Proposed Rules, including their structural revisions to the 2023 NPR and current capital rules. Additional detail on key provisions is included in the accompanying summary chart.

- Broad Relief for Category III and IV Banks: While the 2023 NPR would have largely collapsed regulatory “tailoring” efforts by applying an “expanded risk-based approach” (“ERBA”) to every bank with at least $100 billion in assets, the Proposed Rules restore the threshold for mandatory ERBA compliance to banks in Categories I and II (and, to a modified extent, those with significant trading or derivatives activity), generally consistent with the thresholds for “advanced approaches” and market risk requirements under existing capital rules.1 Banks of any size would be permitted to opt in to ERBA standards, and Category III and IV banks would be required to recognize AOCI in regulatory capital, subject to a five-year phase-in period. The Proposal estimates that several Category III and IV banks, and up to one-third of smaller banks, would see significant reductions in capital requirements by opting in to the ERBA standards.

- Modified Standardized Approach: The Proposed Rules would revise the “Standardized Approach” (broadly applicable to banks not subject to the ERBA) to improve the risk sensitivity of capital risk weightings and deductions applicable to various asset classes.

- “Single Stack” Structure: The Proposed Rules would eliminate “dual stack” RWA calculations (e., as currently applicable to “advanced approaches” institutions), and instead require only a single calculation of capital requirements for each bank under either the ERBA or Standardized Approach.

- Improved Risk-Sensitivity for Core Businesses: The Proposed Rules would implement a structural shift in the banking agencies’ approach towards mortgage, consumer and corporate finance, pivoting away from the gold-plated surcharges and punitive risk weights of the 2023 NPR in favor of a framework that prioritizes alignment with international standards and the restoration of risk-based regulatory tailoring to “better support the flow of credit to households and businesses” and reduce incentives for these activities to “migrate outside of the regulated banking sector.” Reductions in risk weights for residential mortgage loans (and elimination of capital deductions for mortgage servicing assets), as well as corporate and consumer loans (other than credit cards) are expressly intended to expand bank lending in these areas.

- Fresh Approach to Operational and Market Risk: The proposed ERBA would include standardized operational and market risk capital requirements with the goal of avoiding the perceived uncertainty and volatility associated with the current model-based methods. The revised operational risk component would use three-year averages to smooth fluctuations, recalibrate proxy measurements of business volume for non-interest-related operations, and reduce capital charges for activities that historically exhibit lower operational risk levels, such as investment management and treasury services. The revised market risk component would introduce a default standardized approach for market risk, allowing a bank to use internal models for calculating market risk only with supervisory approval, and only if its models are sufficiently robust on a trading desk-by-desk basis.

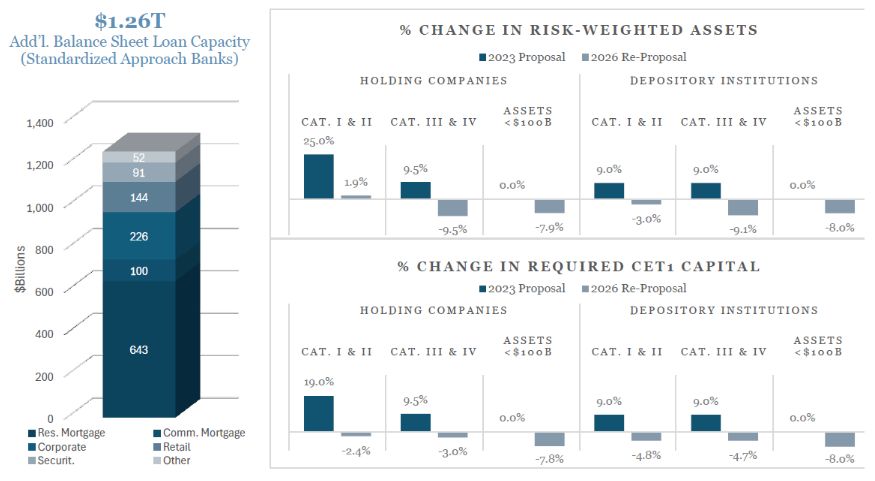

Projected Capital Impacts2

Basel III Endgame Re-Proposal – Key Provisions

|

Areas of Impact |

2023 Proposal |

2026 Re-Proposal |

|

Scope and Tailoring |

||

|

Scope of Application – |

|

|

|

Scope of Application – |

|

|

|

Elimination of “Dual-Stack” Risk-Weighted Assets Calculation Requirements |

|

|

|

GSIBs |

||

|

GSIB Surcharge Score – Indicator Recalibration |

|

|

|

GSIB Surcharge Score – Cliff Effects and Volatility |

|

|

|

Wholesale Funding |

Retained following current rule features:

|

|

|

Client-Cleared Derivatives |

Included bank guarantees of client performance on derivatives to a central clearing counterparty in “interconnectedness” and “complexity” indicators (which commenters claimed would result in higher costs and more volatility for derivative end-users) |

Does not include client-cleared derivatives in Interconnectedness and Complexity indicators (avoiding 2023 proposal’s possible disincentive to provide client access to central clearing) |

|

Mortgages |

||

|

Residential Mortgages |

Risk weights varied based on LTV and whether the property is income-producing, with risk weights for each LTV “band” gold-plated by 20 percentage points above Basel III standards |

|

|

Exposures to Income Producing Residential Real Estate |

Deemed mortgage loans (except on a borrower’s principal residence) to be “dependent” on cash flows from underlying real estate (and subject to higher risk-weighting bands) if bank considered any proceeds from underlying property in underwriting borrower’s repayment ability. |

Does not accommodate widespread calls from public commenters to narrow scope of “cash flow dependent” mortgages subject to higher risk-weighting bands |

|

Mortgage Servicing Assets |

Eliminated simplified threshold capital deduction framework for MSAs for Category III and IV banks, reducing individual deduction threshold from 25% to 10% and applying a 15% aggregate deduction threshold (shared with DTAs and unconsolidated financial institution investments)—same as Category I and II banks |

Removes any requirement to deduct MSAs from regulatory capital for all banks, and applies a 250% risk weight to all MSAs (while seeking comment on whether a different risk weight would be more appropriate) |

|

Private Mortgage Insurance |

Explicitly refused to recognize risk-mitigating benefits of PMI for purposes of calculating LTV ratios or assigning risk weights |

Does not accommodate widespread calls from public commenters to recognize PMI credit risk mitigation, but seeks public comment on appropriate role of PMI as a credit risk mitigant for regulatory capital purposes |

|

Other Credit Risk |

||

|

Retail Exposures – General |

Risk weights varied based on product type, portfolio diversification and payment history, with risk weights for each retail exposure category gold-plated by 10 percentage points above Basel III standards |

|

|

Retail Exposures – Credit and Charge Cards |

|

|

|

Retail Exposures – “Regulatory” Retail |

|

|

|

Corporate Exposures |

Allowed preferential 65% risk weight for exposures to investment-grade companies, but only if the obligor company is publicly traded |

|

|

Small & Medium Enterprise Exposures |

Did not incorporate Basel III’s separate preferential risk weight (85%) for exposures to SMEs; defaults SME exposures to 100% risk weight |

Does not accommodate calls from public commenters to adopt separate 85% risk weight for SMEs |

|

“Credit Conversion Factors” – Not Unconditionally Cancellable |

|

|

|

“Credit Conversion Factors” –Unconditionally Cancellable |

Increased CCF for unconditionally cancelable off-balance sheet commitments from 0% to 10% |

|

|

Other Investments |

||

|

Equity Exposures |

|

|

|

“Sin Bucket” Capital Deductions |

Eliminated simplified threshold capital deduction framework for DTAs, MSAs and investments in unconsolidated financial institutions for Category III and IV banks (with a single 25%-of-CET1 individual deduction threshold), requiring regional banks to instead apply more onerous 10%-of-CET1 individual deduction threshold and 15%-of-CET1 aggregate deduction threshold (shared across MSAs, DTAs and unconsolidated financial institution investments) |

|

|

Operational Risk |

(All Category I-IV Banks) |

(Category I and II Banks Only) |

|

Internal Loss Multiplier (ILM) |

Proposed ILM (scalar to adjust operational risk capital requirements to firm-specific history of operational losses) assigned a floor of 1.0, allowing firm’s operational loss history to increase—but not decrease—capital charges |

ILM eliminated, so that operational risk capital charges based solely on business volume (“business indicator” proxy) and not adjusted upwards or downwards by loss history |

|

Business Indicator – Subcomponents |

|

|

|

Business Indicator – Non-Interest Income / Expenses |

Services component business volume based on gross amounts of income / expenses, reflecting the larger of either income or expense |

Non-interest component business volume calculated on a net basis to avoid overly punitive capital charges for fee-based businesses |

|

Business Indicator – Preferential Treatment for Lower-Risk Services |

No differentiation among businesses that have demonstrated history of posing lower operational risk within Business Indicator calculation |

Includes a 70% discount for net income attributable to investment management, investment services, and non-lending treasury services when calculating Business Indicator volume |

|

Market Risk |

(All Category I-IV Banks) |

(Category I and II Banks, and Others with Significant Trading Activity) |

|

Internal Models Approach |

|

|

|

Consequences for Insufficiently Accurate / Conservative Internal Models |

|

|

|

Default Risk Capital (DRC) Requirement |

Prohibited internal modeling for DRC requirements to capture losses on credit and equity positions in the event of obligor default, and instead required standardized approach for all DRC calculations |

Does not accommodate calls from public commenters to allow banks’ internal models for DRC requirements, but allows a single, entity-wide calculation of standardized DRC |

|

CVA Risk |

(All Category I-IV Banks) |

(Category I and II Banks, and Others with Significant Trading & Derivative Activity) |

|

Client-Facing and Cleared Derivative Exemptions |

Excluded derivative transactions directly facing a central counterparty, but imposed CVA capital charges against client-facing legs of derivatives (e.g., where the bank enters into an offsetting transaction with a CCP or guarantees client performance to a CCP) |

Excludes CCP-facing cleared derivatives as well as client-facing leg of cleared derivatives from CVA capital requirements (preserving incentives for central clearing) |

|

End-User Derivatives |

Did not exempt derivative transactions with commercial end-users (e.g., non-financial corporations, municipalities, funds)—which are often uncollateralized and lack access to large pools of marginable liquidity–from CVA capital charges, resulting in significantly higher capital requirements for an uncollateralized end-user derivative compared to existing requirements under SA-CCR |

Does not accommodate widespread calls from public commenters to broadly exempt commercial end-user derivatives (e.g., corporate hedging) from CVA Risk capital requirements |

|

Collateralized Transactions |

||

|

Securities Financing Transactions (SFT) – Collateral Value Haircuts |

Introduced mandatory minimum SFT haircut floors (which were not adopted by major jurisdictions like U.K. and EU)—effectively establishing minimum amounts of collateral banks must receive when engaging in certain repos and margin loans—and imposed heightened capital requirements for repos / margin loans that did not meet minimum collateral requirements |

|

|

Credit-Linked Note Recognition |

Ad hoc Federal Reserve determinations (on a bank-by-bank basis) regarding RWA treatment for CLNs issued by the bank against exposures in the banking book that fulfil some, but not all, of the criteria for synthetic securitizations (e.g. whether pre-funded cash proceeds are eligible credit mitigant similar to cash collateral) |

Codifies treatment of “prepaid credit protection” (e.g., directly issued, cash-funded CLN transactions) as eligible credit risk mitigants—expanding, e.g., eligibility for “synthetic securitization” treatment |

Industry-Focused Series on Basel III Endgame Re-Proposal

Alternative Asset Management

Proposal presents both opportunities and risks for various sectors of the alternative asset management industry—including private equity, private credit, and fund finance—by enhancing banks’ ability to serve as upstream credit and liquidity providers while also empowering banks to compete more effectively with non-bank lenders and asset managers.

Read more here»

Retail Banking

Proposal would implement a structural shift in the agencies’ approach towards mortgage and consumer banking, with a goal of supporting “the flow of credit to households” and reducing incentives for these activities to “migrate outside of the regulated banking sector”

Read more here»

Investment Banking and Global Markets

Proposal would recalibrate costs for market intermediation and investment banking services, bolstering the capacity of large U.S. banks to contribute to liquidity in the primary and secondary financial markets and permitting market participants to manage financial risk more holistically

Read more here»

Footnotes

1 The Proposed Rules do not adjust supervisory “category” thresholds (e.g., by indexing to growth or inflation), despite Vice Chair Bowman and others having discussed the merits of such changes.

2 Based on federal banking agency projections included in the Proposed Rules. Includes impacts of AOCI recognition and GSIB surcharge proposal.

3 Category II banks that would be subject to Operational Risk, Market Risk, and CVA Risk frameworks also include banks with ≥ $75B in cross-jurisdictional activity, regardless of asset size. Market Risk and CVA Risk frameworks would also apply to banks that are not in Category I or II but have significant trading activity (and, in the case of the CVA Risk framework, significant OTC derivative exposures).

Descriptions in this summary chart of provisions applicable to banks with “≥$700B in assets” would also apply to these other banks that have ($700B in assets but also significant cross-jurisdictional, trading and/or derivatives activities.

4 Federal Reserve used special data collection exercise to determine weighted average risk weights that would apply to applicable assets of Category III and IV U.S. banks under the ERBA (as if those banks were subject to ERBA).

5 The separate supplementary leverage ratio rules would continue to apply a minimum 10% CCF for off-balance sheet exposures, even if a bank subject to the SLR is not subject to the ERBA (like Category III banks).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]