- within Tax topic(s)

- within Tax topic(s)

- with Finance and Tax Executives

- with readers working within the Accounting & Consultancy and Media & Information industries

Introduction

In November 2024, the Federal Inland Revenue Service (FIRS) announced the planned adoption of the Merchant Buyer Solution (MBS) also called the e-invoicing initiative for enhanced tax administration and tax collection. This is a national initiative involving various government agencies, such as the Nigeria Customs Service (NCS), Central Bank of Nigeria (CBN), National Information Technology Development Agency (NITDA), etc., but is primarily driven by the FIRS. Electronic invoicing is simply a process of sending and receiving invoices electronically rather than through paper-based methods.

Nigeria will be adopting the clearance and reporting model of e-invoicing in line with the Pan-European Public Procurement Online (PEPPOL) framework. This model of e-invoicing is used for Business-to-Business (B2B) and Business-to-Government (B2G) transactions. The clearance model facilitates seamless creation, validation, and exchange of electronic invoices between transacting parties. Under this model, each invoice generated by taxpayers must include an invoice reference number (IRN), Quick Response (QR) code, and a digital signature to be considered valid for payment. The e-invoicing system automatically generates the IRN. For Business-to-Consumer transactions (B2C), FIRS is likely to adopt a simplified invoice/fiscalisation method that will involve real-time or near real-time transmission of transaction data. E-Invoices can be issued and processed in all currencies.

The FIRS is currently pilot testing this initiative with selected large taxpayers. Full-scale deployment is expected to begin in July 2025 but may be delayed if the President has not assented to the Tax Reform Bills by then. Roll-out will begin with large taxpayers, focusing on B2B and B2G transactions, and thereafter, B2C transactions. This phased approach allows for careful monitoring and troubleshooting of taxpayer's system before it is expanded to the broader consumer base.

A typical e-invoice will include eighty (80) fields (both mandatory and optional fields), some of which are already present in taxpayers' Enterprise Resource Planning (ERP) systems and existing e-invoicing solutions. The remaining fields would need to be configured by a System Integrator (SI). The SI guarantees data compatibility in line with Universal Business Language (UBL) and facilitates accurate transmission of invoices to the Access Point Provider (APP). The APP, on the other hand, validates and securely transmits invoices from the client's invoicing solution to the FIRS's MBS solution. Taxpayers have the flexibility to choose from a list of licensed APPs and SIs for support in transmitting e-invoices between trading partners and the FIRS. They also have the option to become SIs or APPs themselves, provided they meet the necessary requirements. Please see the link to the requirements.

The FIRS has conducted several stakeholders' engagement sessions, including sector-specific sessions to educate stakeholders and encourage their active participation in e-invoicing.

Legal basis

Section 25 (3-4) of the Federal Inland Revenue Service (Establishment) Act (FIRSEA) 2007, as amended, provides that"The Service may deploy any proprietary or third-party payment, processing or other digital platform or application to collect and remit taxes due on international transactions in the supply of digital services to and from a person in Nigeria, in the case of transactions carried out through remote, digital, electronic or other such platform. The Service may deploy proprietary technology to automate the tax administration process including tax assessment and information gathering provided it gives 30 days' notice to the taxpayer."

Section 23 of the harmonised Nigeria Tax Administration Bill (NTAB) provides that "where the Service deploys an Electronic Fiscal System (EFS), any person making a taxable supply shall use the EFS for recording and reporting all supplies..."

Furthermore, Section 157 (1-2) of the harmonised Nigeria Tax Bill states that "a taxable person making a taxable supply shall implement the fiscalisation system deployed by the Service in accordance with the Nigeria Tax Administration Bill. The fiscalisation system may include fiscal equipment consisting of electronic devices, software solutions or a communication system involving a secured network, or any such combination of the components for electronic invoicing and data transfer as the Service may prescribe or deploy".

Consequences for non-compliance

In accordance with the powers granted to the FIRS as shown in the legislation above, taxpayers are mandated by the FIRS to integrate their systems with the FIRS's platform using Application Programming Interfaces (APIs). Failure to grant access for the deployment of technology after 30 days of receipt of the deployment notice will attract an administrative penalty of ₦25,000 for each day that it fails to grant access, according to the provision of Section 4(b) of the FIRSEA and ₦1,000,000.00 for the first day of default and ₦10,000 for each subsequent day of default, according to Section 103 of the proposed NTAB. Section 104 of NTAB also provides that a taxable person who fails to process a taxable supply through the fiscalisation system is liable to an administrative penalty of N200,000 plus 100% of the tax due, plus an interest at the prevailing CBN's Monetary Policy rate per annum.

Additionally, without an IRN, taxpayers may be unable to claim VAT credit on invoices presented. This requirement will also be considered as transaction validation for allowable deduction for Companies Income Tax (CIT) purposes and capital allowance claim. The invoice would be unrecognised for payment by the customer who receives it through an APP.

Commentaries

The e-invoicing initiative by the FIRS is another milestone toward the Federal Government's commitment to widening the tax net and enhancing government's tax revenues. With the introduction of this initiative for tax purposes, Nigeria joins other progressive tax jurisdictions like India, Kenya, Mexico, Chile, Italy, Denmark, etc. There are also many African countries that are implementing e-invoice.

If properly implemented, this initiative has the potential to enhance transparency in tax audit processes as it provides an auditable trail of invoice transactions. It can significantly lower compliance costs as disputes may be reduced due to the use of technology which allows for accurate data tracking, efficient reconciliation processes, and real-time monitoring. In addition, the initiative supports decision making through advanced analytics of data collected, enhances tax compliance predictively, and promotes a risk-based approach to tax audits/ investigations. This, in turn, could broaden the tax base by capturing a wider range of transactions and entities within the fiscal framework.

There are also benefits for taxpayers. Taxpayers can benefit from cost savings due to reduction in the use of paper, printing, and mailing costs. It enables faster processing of payment and helps to increase efficiency by reducing errors and processing time associated with manual processes.

However, to support a successful implementation of the initiative, government needs to address the following concerns that taxpayers have expressed:

01 Quality of supporting infrastructure – Reliable internet connectivity and data storage capacity are key for the effective implementation of e-invoicing. The transmission of invoices between the ERP systems and FIRS's portal requires internet speeds of upwards of 1 Mbps1 and data storage capacity would have to be in multiples of petabytes. In response to this challenge, we understand that the FIRS will upgrade its current internet access and allow offline invoice processing capabilities so that taxpayers can still issue invoices during internet downtime and upload these invoices when internet service becomes available. The data will be stored on local servers. In some other jurisdictions, it is common for the regulators to use dedicated data farms to store the data and information collected via electronic invoicing.

02 Data privacy and security – Considering that the invoices that will be exchanged digitally will contain sensitive financial data, data security is paramount. There are provisions in the current and proposed tax laws in Nigeria that prescribe penalties for any official of the tax authority who divulges any submission by taxpayers. Also, the Nigerian Data Protection law provides rules and regulations for the collection, storage and processing of data in Nigeria. However, these laws require the demonstration of deliberate action from the regulator to protect this information, including the implementation of a multilayered approach of technical, organisational and regulatory measures. Internal data polices will have to be updated properly to manage all risks associated with this initiative, and the policies can be published for a high level of transparency.

03 Cost of compliance for taxpayers – Taxpayers would have to contend with the added cost of compliance associated with the acquisition of innovative technology where necessary, and to engage the services of SIs and APPs for the initiative. This added cost would affect the profitability of taxpayers. The FIRS could consider some form of incentives for taxpayers, for instance, granting an investment cost uplift for companies that adopt the initiative within the 30-day window stipulated in Section 25 (4) of the FIRSEA.

04 Challenges for small businesses – E-invoicing can be capital intensive and may be difficult for small businesses to implement. To ensure that small businesses can participate in this initiative, we understand that the FIRS intends to create an e-invoicing solution that is accessible and practical for small businesses to use. In line with our comments in point 3, this solution should be cost-effective for small businesses to promote widespread voluntary compliance.

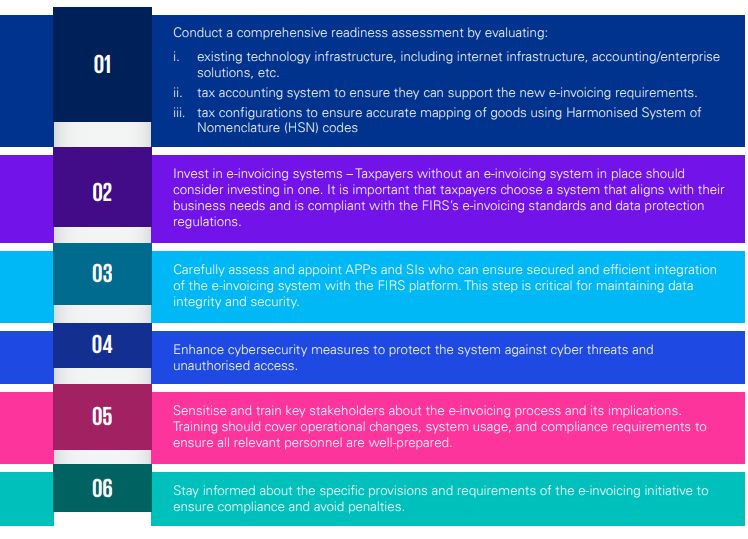

It is important for taxpayers to recognise that the e-invoicing initiative will become a significant part of tax administration in Nigeria, offering more than just compliance with regulatory requirements. Benefits such as the ability to claim input VAT, improved accuracy in invoice processing, faster payment processing and enhanced security would collectively enhance taxpayers' financial operations. Given these advantages, it is imperative for taxpayers to proactively prepare for the integration. To ensure a smooth transition, taxpayers should do the following:

Taxpayers need to be fully prepared ahead of the complete rollout of the e-invoicing initiative. Doing this would minimise business disruptions and ensure full compliance with the new system

The opinion expressed in this article is solely personal and does not represent the views of any organization or association to which the authors belong.

[View Source]