On September 19, 2022 in the case of SEBI v. Abhijit Rajan, the Hon'ble Supreme Court (SC) held that the motive of the insider to make an unlawful gain, the direction of the trade made by the insider and the reason for which such trade was carried out, are all relevant factors which should be taken into consideration to prove an insider trading charge under the SEBI (Prohibition of Insider Trading) Regulations, 1992 (1992 PIT Regulations). The facts of the case are briefly discussed hereinbelow.

Background Facts

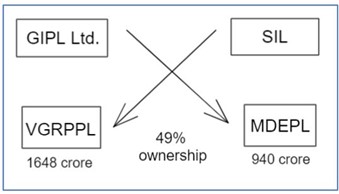

In the case, two infrastructure companies, Gammon Infrastructure Projects Ltd. (GIPL) and Simplex Infrastructure Ltd (SIL), both listed on Indian stock exchanges, had been awarded contracts from the National Highway Authority of India. In this regard, both GIPL and SIL had set up Special Purpose Vehicles (SPVs) for execution(s) of their respective contracts. Further, GIPL and SIL had entered into shareholder agreements (SHAs), whereby both the listed entities had to acquire around 49% stake in the SPV of the other entity, as depicted from the following figure:

The value of the contract awarded to the GIPL, however, was

larger in terms of value compared to the one awarded to SIL.

Subsequently, the board of GIPL passed a resolution terminating

both the SHAs, which was disclosed to the stock exchanges twenty

days later. As per SEBI, such termination was unpublished price

sensitive information (UPSI). Since Mr. Abhijit

Rajan (Respondent), the chairman and MD of GIPL,

had sold shares before the information about termination of the

SHAs was disclosed to the NSE and BSE, Mr. Rajan was held liable

for indulging in insider trading and violation of Regulations 3(i)

and 4 of the 1992 PIT Regulations.

On appeal by Mr. Rajan, SAT allowed the appeal inter alia

on the following grounds: (i) the termination of SHAs did not

constitute PSI as the investment of GIPL in the SIL SPV was a

miniscule portion of the order book value and turnover of GIPL, and

(ii) Mr. Rajan had sold the shares to fund promoter's

contribution towards a corporate debt restructuring

(CDR) package of the parent company of GIPL,

failing which the parent company would have had to file for

bankruptcy.

SC Ruling

Upon appeal by SEBI against the SAT order, the SC observed that while the termination of the SHAs did constitute PSI, the charge of insider trading against Mr. Rajan could not sustain on the following basis.

It held that there must be an intention to make unfair gains on part of the insider to take advantage of the UPSI so possessed to prove the charge of insider trading. Further, the direction of the trade made by the insider was a relevant factor. In the present matter Mr. Rajan had sold his shares prior to the disclosure of the UPSI, despite the fact that such UPSI was positive and would have led to an increase in share price of GIPL after the UPSI came into public domain. Therefore, the direction of the impugned trade was opposite to the anticipated movement of the share price. The SC observed that any person desirous of indulging in insider trading would have waited for the positive information to come into public domain and thereafter sold his holdings. The SC held that the fact that Mr. Rajan had not waited for the information to become public, showed his intention to not indulge in insider trading.

The Supreme Court further observed that Mr. Rajan had sold his

shares out of necessity, i.e., for the CDR package payment. It was

thus concluded by the SC that there was no motivation on part of

the Respondent to make undeserved gains by encashing on the

UPSI.

Regulation 3 of the 1992 PIT Regulations deems any insider who

trades while in possession of UPSI liable for insider trading. The

SC, instead of relying on a literal interpretation of the

provision, has adopted a purposive interpretation in the above case

and factored in the direction of trade and necessity to trade, to

determine whether the person intended to encash on the benefit of

the UPSI.

The above interpretation of the SC is consistent with the intent of the regulations, which is to prevent insiders from gaining an unfair advantage of the UPSI they possess so that other investors are not disadvantaged.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.