- within Litigation, Mediation & Arbitration, Media, Telecoms, IT, Entertainment and Insolvency/Bankruptcy/Re-Structuring topic(s)

- with readers working within the Media & Information, Securities & Investment and Construction & Engineering industries

- Introduction

Overseas Direct Investment ("ODI") through Foreign Direct Investment ("FDI") transactions (often referred as "round-tripping") has had a checkered past on account of suspicion over whether they constitute a bona fide transaction. Round-tripping typically refers to an Indian entity investing in a foreign company which invests or already has investments in India.1 In this context, round-tripping is regulated by the Foreign Exchange Management Act, 1999 ("FEMA"), which gives the Reserve Bank of India ("RBI") the power to formulate rules, regulations, and notifications thereunder. Though the RBI had adopted a strict approach on this subject in the past, this approach saw a change in August 2022, when the RBI along with the Ministry of Finance issued revised rules, regulations, and directions for overseas investment. These are (i) the Foreign Exchange Management (Overseas Investment) Rules 2022 ("OI Rules"), (ii) the Foreign Exchange Management (Overseas Investment) Regulations 2022 ("OI Regulations") and (iii) the Foreign Exchange Management (Overseas Investment) Directions 2022 ("OI Directions"), discussed below.

This newsletter focuses on how the RBI has historically considered and may potentially evaluate such transactions.

Applicable Framework

For a proper understanding of the key changes, it is necessary to examine both the old and new framework of overseas investment.

- Old Framework

Overseas investment was governed by the Foreign Exchange Management (Transfer or Issue of Any Foreign Security) (Amendment) Regulations, 2004 ("2004 Regulations"). While the 2004 Regulations were silent on round-tripping, the RBI often penalized such transactions by applying Regulation 6(2)(ii), or Regulation 5 read with Regulations 13 and 15.

Regulation 6(2)(ii) states that a person resident in India ("Indian Party") may directly invest in a Joint-Venture ("JV") or a Wholly-Owned Subsidiary ("WOS") outside India provided that direct investment is made in an overseas JV/WOS engaged in a bona fide business activity. Under this regulation, RBI often did not consider ODI through FDI transactions as a bona fide business activity permissible under the automatic route2 and penalized the relevant entities. The term bona fide business activity was not defined under the 2004 Regulations and was, therefore, entirely subject to RBI discretion. Regulation 5(1) prohibits an Indian Party from investing overseas unless it is permitted under FEMA Act, rules, regulations, or directions, or through express approval of the RBI. In case of deviations, the Indian Party would face penalties if it does not adhere to reporting requirements under Regulation 133 and 154.

Contravention of the aforesaid regulations attract penalties under section 13 of FEMA. This provision prescribes up to thrice the sum involved in the contravention if the amount is quantifiable, or up to INR 200,000 (about USD 2,448)5 where the amount is not quantifiable, and a further penalty of up to INR 5,000 (about USD 61) for every day during which the contravention continues. The RBI's position on the subject can be illustrated through the following two compounding orders on such transactions.

(i) R Systems International Limited (CA No. 5041/2019)

R Systems was involved in the business of software development. In September 2000, it invested SGD 3,500 through ODI in its WOS named R Systems (Singapore) Pte Ltd. In April 2015, the WOS, acquired an entity in Singapore called IBIZ Consultancy Services Pte Ltd which subsequently purchased 49,999 shares of an Indian entity, called IBIZ Consultancy India Pvt. Ltd. for INR 499,900 (about USD 6,121) thereby creating an ODI through FDI structure which was not reported. In August 2019, R Systems directly acquired IBIZ Consultancy India and reported the same thereby ending the erstwhile structure. The RBI took note of the non-compliance and passed a compounding order for INR 143,500 (about USD 1,758) against R Systems for contravening Regulation 13 by not reporting the ODI through FDI structure and Regulation 15 by not submitting the annual performance reports for 2004-2014 in time.

(ii) Binani Industries Limited (CA No. 3867/2015)

BIL was a holding company for subsidiaries engaged in the manufacture of glass fiber products. In September 2011, it incorporated a special purpose vehicle in Luxembourg called 3B Binani, for acquiring 100% stake in PBH Group Companies which owned 3B Fibreglass, with its operating units in Belgium and Norway. BIL also held 100% shares in Goa Glass Fibre Limited based in India. As part of its M&A strategy, BIL merged the operations of Goa Glass with 3B Binani. BIL sold its stake in Goa Glass in two different tranches – in February 2012, 49% was sold and in October 2012 balance 51% was sold. The consideration came through multiple inward remittances totaling to INR 1,559,233,934 (about USD 19 million). Thus, Goa Glass became a WOS of 3B Binani which itself was a WOS of BIL, creating an ODI through FDI structure. When the RBI reviewed the statutory reporting for the transfer, it commenced proceedings. It eventually held that this was not a bona fide business transaction under Regulation 6(2)(ii) and imposed a penalty of INR 10,185,000 (about USD 125,000).

Additionally, in May 2019, RBI updated the FAQs on ODI to reflect its intent to prohibit round-tripping. The FAQs state that the 2004 Regulations do not permit an Indian Party to establish an Indian subsidiary through its foreign WOS or JV nor do the provisions permit an Indian Party to acquire a WOS or invest in a JV that already has direct/indirect investment in India. This was widely considered as an incorrect method for addressing such a crucial issue. FAQs are not binding in nature and issues of such gravity cannot be appropriately addressed in such an informal way.

- New Framework

The new framework has introduced some changes, discussed below.

New definitions: The definition of "subsidiary" under Rule 2(1)(y) of the OI Rules has diverged from the definition under Section 2(87) of the Companies Act, 2013 ("CA") to mean an entity in which the foreign entity has "control." Under the OI Rules, "control" has been defined as the right to appoint majority of the directors or to control management or policy decisions by a person acting individually or in concert, directly or indirectly, including by virtue of shareholding or management rights or shareholders' or voting agreements that entitle them to 10% or more of voting rights or in any other manner in the entity. Meanwhile, section 2(87) of CA defines a "subsidiary" to mean a company in which the holding company controls the composition of Board of Directors, or exercises or controls more than 50% of the total voting power. Thus, a foreign entity may be considered as a subsidiary under the OI Rules even if it does not meet the 50% criteria under the Companies Act.

Bona fide business activity: The OI Rules have taken note of the issues surrounding the wide ambit of the term and adopted the definition proposed under the Draft Foreign Exchange Management (Non-debt Instruments – Overseas Investment) Rules, 2021("Draft Rules")6. The explanation to Rule 9 defines bona fide business activity to mean any business activity permissible under any law in force in India and the host country. This hopefully will mean that RBI will exercise its discretionary powers sparingly and judiciously.

Restriction on number of subsidiaries: The new OI Rules liberalize norms for overseas investment. Rule 19(3) provides that no financial commitment will be permitted in a foreign entity which has invested or invests in India, directly or indirectly, resulting in a structure with more than two layers of subsidiaries. By inference, the OI Rules implicitly allow any transaction which falls below two layers. The restriction on layers of subsidiaries is in accordance with restrictions under the Companies (Restriction on Number of Layers) Rules, 20177 ("Company Rules"). However, this has led to a contradiction between the two laws which is addressed subsequently below.

Two Illustrations: The types of transactions which would be permissible is illustrated below:

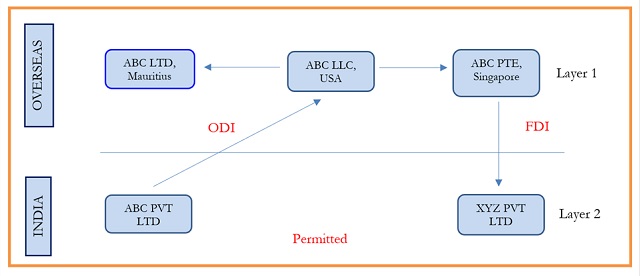

Diagram 1

In the above diagram, the Indian entity ABC can indirectly invest in XYZ. By investing in ABC LLC, a US-based entity which has indirect control of XYZ through its Singapore subsidiary. The total number of subsidiaries in this transaction is two, i.e., ABC PTE and XYZ Pvt Ltd. The transaction would not be permissible if there was an additional subsidiary company between ABC LLC and XYZ Pvt Ltd, as illustrated below:

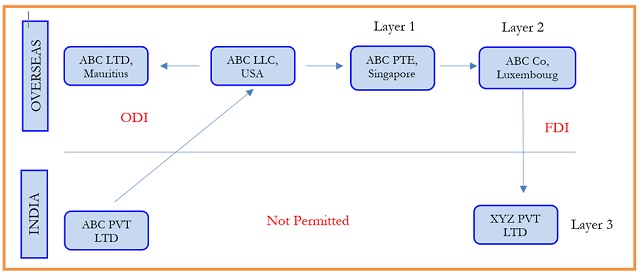

Diagram 2

In the above diagram, ABC cannot indirectly invest in XYZ through ABC LLC because the number of subsidiaries is over the permissible threshold. The key point is regardless of the fact that the layers are outside India, ABC PTE and ABC Co. would be considered as subsidiaries.

The application of the OI Rules becomes clearer when read with Clause 20 of the OI Directions which provides that no further layer of subsidiaries shall be added to any overseas investment structure which already has two or more layer of subsidiaries. The 10% control rule is also reiterated in the OI Directions.

- Issues Ahead

While the new framework is a welcome change, there are a couple of concerns. Firstly, while Rule 2(1) of the Company Rules exempt both WOS and overseas entities having more than two subsidiary layers if permitted by the applicable foreign laws from being counted as layers, a similar exemption is not provided under Rule 19(3) of the OI Rules. Therefore, there is a dichotomy between the two set of rules, one issued under CA and the other under FEMA. Secondly, the OI Rules omitted Rule 6(3) of the Draft Rules which expressly prohibited round-tripping for tax avoidance. Inclusion of this restriction could have formalized the objective of regulators to promote bona fide round-tripping transactions and prevent tax evasion and other fraudulent behavior.

- Conclusion

The layering concerns above, coupled with differing positions and inconsistencies spread across different laws, need immediate attention and resolution. In the past, RBI has dealt with such inconsistencies by issuing FAQs. Such an approach is inadvisable because FAQs are an informal guideline, is often prone to different interpretations and does not garner much confidence in the minds of investors. It would be more expedient for the business if RBI and the Ministry of Finance amend the applicable framework to address the present ambiguities and conflicts with prevailing law. If not, the route to FDI through ODI may prove to remain as circuitous as ever.

Footnotes

1 P Upadhyay, Overseas Investment Rules Bring Round Tripping Relief, Commercial Flexibility; But Frown On Startup Bets, Bloomberg Quint, available at: https://www.bqprime.com/law-and-policy/overseas-investment-rules-bring-round-tripping-relief-commercial-flexibility-but-frown-on-startup-bets [last accessed on November 22, 2022]

2 The Consolidated FDI Policy Circular of 2020 defines the “Automatic route” to mean the entry route in certain sectors through which investment by a person resident outside India does not require the prior approval of the Reserve Bank of India or the Central Government

3 This requires an Indian Party to report any decision of the overseas JV or WOS to diversify or alter shareholding or set up a step-down subsidiary

4 This requires an Indian Party to provide an annual performance report of the overseas JV/WOS

5 USD 1 = INR 81 and rounded off

6 The explanation to Rule 4 of the Draft Rules defines bona fide business activity to mean any business activity legally permissible both in India and host jurisdiction

7 Rule 2(i) of the Company Rules places a restriction that no company, other than a one belonging to a class specified, shall have more than two layers of subsidiaries. It is interesting to note that the exceptions under this rule with respect to wholly owned subsidiaries are not counted as a layer and exemption for lawful subsidiaries outside India have not been incorporated in the OI Rules

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]