The Tax Department has recently published an Informative Guide, in the Greek language, which explains the tax treatment of certain benefits offered by employers to employees and persons who hold or are deemed to hold an office. It is soon expected that the Informative Guide will also be issued in English in the official website of the Tax Department.

The taxation of benefits is provided in Article 5 of the Income Tax Law, according to which benefits from any office or employment, provided to an employee or to a member of his family either in cash or otherwise, are subject to tax.

The guide describes how the Tax Department intends to apply the law as from 1 January 2019, however, the various methods of estimating the value of the benefits in kind mentioned in the guide can be applied for previous years as well.

What is a benefit in kind?

"Benefit in kind" means the benefit that is, or is deemed to be, granted in connection with any employment or the holding of an office.

Scope of application:

The rules apply with reference to benefits in kind provided to:

- Employees, and

- persons who hold or are deemed to hold an office.

When the benefit is granted to a member of the family or household of the person who is employed or holds the office, then the benefit shall be deemed to be provided to that person.

Keeping records

Employers are required to keep records indicating how the value of the benefits in kind has been determined and such records should be available for inspection when requested by the Tax Department.

Deductible expense

Since benefits in kind are taxed in the same way as salaries, the employer who will bear the cost of providing them will be able to deduct such cost from his taxable income under the same conditions that it would be deducted had it been a salary payment.

Employers' registration and obligation to pay the relevant tax

Any person providing "benefits in kind" to an employee and any company or corporation providing benefits to its officers, even in cases where it does not have employees, is considered as an employer by the Tax Department and should register on the Employers' Register and receive a T.I.C, which will enable the submission of the Employer's Return (T.D. 7).

The value of benefits in kind is taxed in the same way as the gross earnings, through the submission of the Form T.D. 7. Employers are required to declare the benefits in kind provided by them or by their connected companies.

Categories of Benefits in Kind

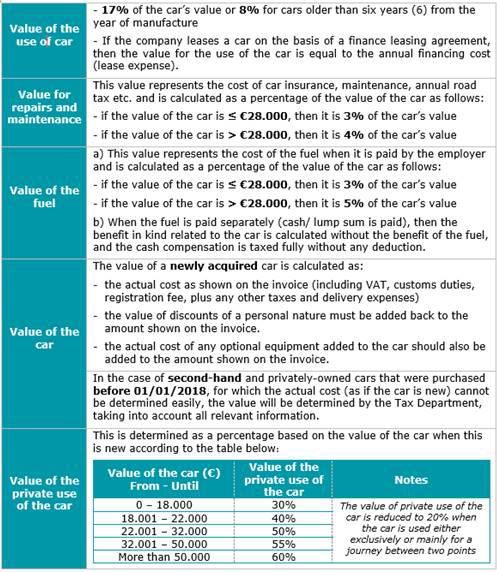

1. Benefits in kind in relation to cars

Benefits in kind that relate to cars can be classified into three types:

a) Use of cars

A benefit in kind arises where there is a usual element of private use and its value is calculated as follows:

b) Commercial Cars (Van type)

The annual value of the benefit in kind for commercial cars is defined as a single amount of €500 per year, regardless of the type, model or year of manufacture/registration of the relevant commercial vehicle.

c) Direct cash payments for car use

The value of the benefit in kind is calculated as 50% of the annual compensation (up to €3.000) to employees in relation to the use of his/her own vehicle for business purposes, subject to conditions. If the annual compensation exceeds €3.000, then the value of the benefit in kind is equal to the annual compensation minus €1.500.

When the compensations are granted to the employee who uses his private car for business purposes on the basis of the distance travelled (with a maximum of 25 cents per kilometer), these repayments do not constitute a benefit in kind, on the provision that the employer keeps a log book for at least six years.

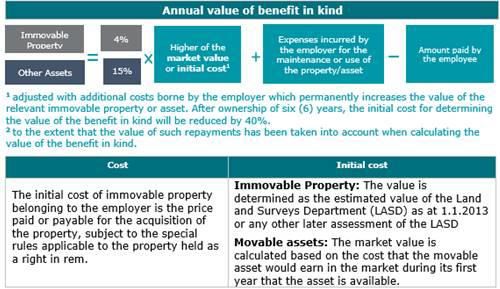

2. Accommodation and use of assets

The provision of assets (e.g. accommodation, furniture, boats, machinery, etc.) to the employee when they belong to the employer and/or leased and/or rented by the employer, can be considered as benefits in kind.

The annual value of the benefits in kind for the use of assets, including accommodation, applies for as long as the asset is at the disposal of the beneficiary and is determined as follows:

3. Other benefits in kind

Any other benefit in kind that does not fall within the above categories, is considered to fall into this category and includes:

- Provision of assets at subsidized prices,

- repayment of personal expenses (benefits, fees, etc.),

- free supply of goods or the sale of goods and services with discounts such as travel, entertainment, meals, domestic services, professional advice, transport etc.

The determination of the value of the benefits in kind which are defined as a supply of goods or a provision of services, is usually determined as the difference between the normal selling price less discounts provided to the general public less the price paid by the employee.

Exemptions

As a general principle, exemptions apply only to the extent where the payment or reimbursement to the employee is made against actual costs supported by payment receipts. They don't apply where the relevant benefit in kind takes the form of cash.

Other specific exemptions mentioned in the guide include amongst others:

- Computer equipment

- Telephone services

- Childcare facilities

- Goods consumed in the workspace

- Newspapers

- Awards for long-term service

- Christmas parties and events

- Subscriptions to professional bodies

- Training Courses/scholarships to employees

- Uniforms and specialized attire

- Recreation areas

- Relocation expenses

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.