- within Corporate/Commercial Law, Intellectual Property and Accounting and Audit topic(s)

- with readers working within the Pharmaceuticals & BioTech industries

On 1 January 2020, the Foreign Investment Law of the People's Republic of China ("FIL") came into force, and at the same time, the three-decades-old-plus Wholly Foreign-owned Enterprises Law of the People's Republic of China ("WFOE Law") and its relevant regulations were simultaneously repealed. With respect to the existing c.375,000 WFOEs already established in accordance with the previous WFOE Law and regulations, the new FIL and its Implementation Regulations provide a 5-year transition period ("Transition Period") for them to make the necessary adjustments and conversion to ensure compliance by the end of 2024. The Company Law of the People's Republic of China ("Company Law") shall universally govern the WFOEs in the same way as it does domestic Chinese companies.

In order to help existing WFOEs and their foreign shareholders better understand the impact of the new FIL and its relevant regulations, we hereby set out the main compliance issues to be attended to in the Transition Period, mainly in respect of the corporate governance, foreign exchange and foreign investment reporting obligations etc.

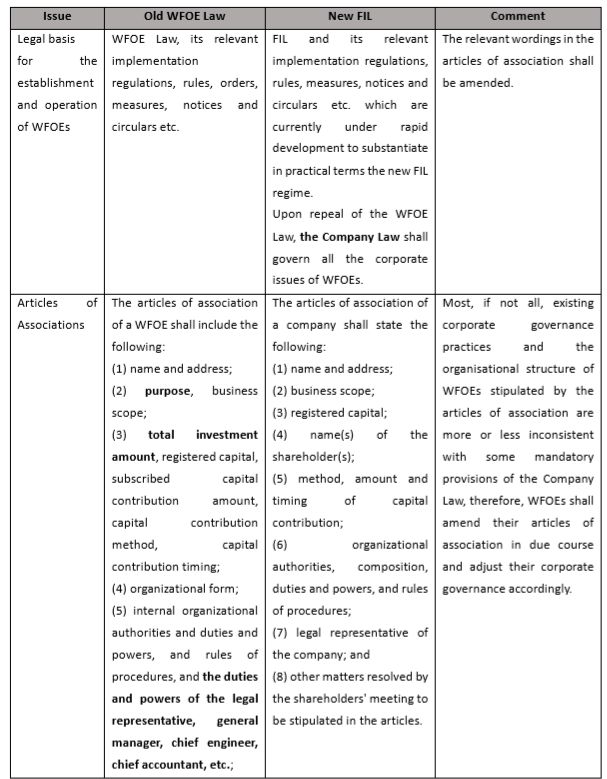

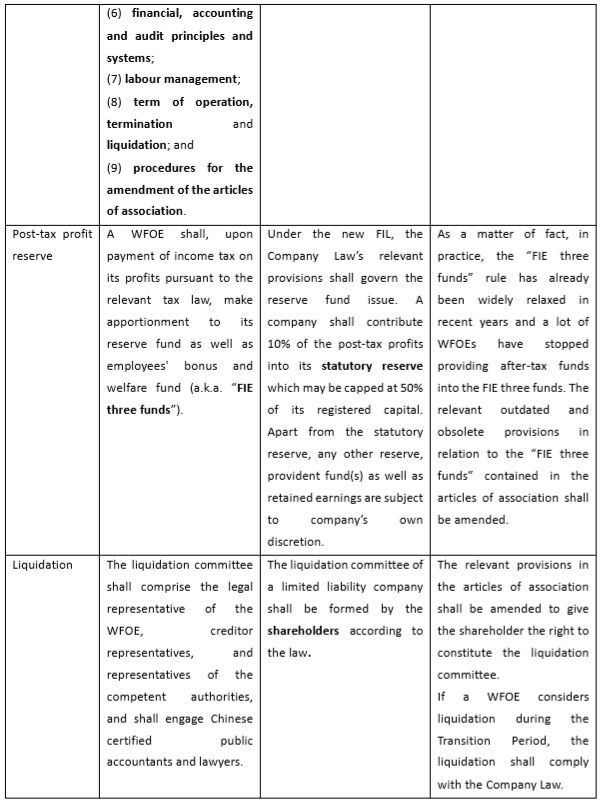

1. Corporate Governance

In order to quickly identify the to-be-complied issues, we have conducted an overhaul of all the corporate governance aspects under the old WFOE Law regime and the new FIL regime. Accordingly we have prepared the below detailed table which sets out the main issues.

2. Foreign Debt Management

Under China's foreign exchange regulatory regime, the foreign debt management system involving the total investment ("投资总额") and the stipulated gap between the registered capital and the total investment ("投注差") have been in place for many years. A WFOE is allowed, not obliged, to take out loans and incur foreign debt within such a gap. In 2017, the Notice of the People's Bank of China on Full-coverage Macro-prudent Management of Cross-border Financing specified a new alternative foreign debt management system.

Technically speaking, the total investment and the stipulated gap between the registered capital and the total investment are no longer mentioned in either the new FIL or the Company Law. However, the competent authorities have not yet promulgated new regulations formally repealing the old foreign debt management system, i.e. the old and new foreign debt management systems co-exist for the time being. Practically speaking, the total investment provisions in the articles of association may not need any immediate change where a WFOE prefers at present not to switch to the new system.

There has recently been some kind of transitional regulatory practice. For example, pursuant to a notice issued by SAFE1 Beijing Bureau in March 2020, non-financial enterprises/companies in Beijing may choose to change their current foreign debt regime where the gap between the registered capital and the total investment is essential, to the more flexible Macro-prudent Management of Cross-border Financing System2 which may offer an easier approval/registration process and a higher permitted amount of foreign debt raised. It is advisable to pay continuous close attention to the subsequent updates of regulations in this regard.

3. Foreign Investment Report

Since 2016, while the "restricted" foreign investment within the scope of the relevant negative lists continues to be subject to approval of the relevant authorities, "encouraged" and "permitted" foreign investment has been subject to filing requirements.

Effective from 1 January 2020, the Measures on Reporting of Foreign Investment Information ("Reporting Measures") established a new foreign investment information reporting system, under which the WFOEs shall submit investment information reports (incl. initial report, change report, deregistration report, annual report, etc.) through the online Enterprise Registration System and the Enterprise Credit Information Publicity System.

Pursuant to the Reporting Measures, where there is a registerable change such as the name, address, legal representative, shareholder(s), scope of business, registered capital etc., a WFOE shall report the same via the Enterprise Registration System at the same time as processing the relevant change(s) registration. Where the change does not involve any registerable item but is subject to the relevant filing requirement, a WFOE shall report the same via the Enterprise Registration System within twenty (20) working days from the occurrence of the changed matter (e.g. the date of the related resolutions).

The annual report for the preceding year should be submitted before 30 June annually through the National Enterprise Credit Information Publicity System, which may include WFOE's basic corporate information, the investors and their actual controllers, business conditions, assets and liabilities, etc. Please note in accordance with the Company Law, a company shall have its annual financial statements audited; however for the time being the reporting obligation might not explicitly require the audited financial statements to be uploaded via the reporting system.

4. Timing Considerations

It is worth noting that

(1) the FIL is new and Chinese authorities are still in the process of ramping up the necessary implementing rules and measures, practice needs to be time tested;

(2) although the 5-year Transition Period seems to be plenty of time, a timely compliance conversion has been encouraged by the Chinese authorities;

3) 31 December 2024 is a hard deadline; from 1 January 2025 if a WFOE has not fully complied with the new FIL, the registration window will be closed thus jeopardizing the foreign investor's investment in that WFOE and a public notice listing incompliant companies will be published.

Undoubtedly with due care penalties for the delay should be avoided.

Footnotes

1 State Administration for Foreign Exchange

2 http://www.safe.gov.cn/beijing/2020/0310/1194.html

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.