- within Government and Public Sector topic(s)

- in United Kingdom

- with readers working within the Banking & Credit, Business & Consumer Services and Technology industries

- within Law Department Performance topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

This bulletin provides an update on trends observed in Indigenous equity investments in energy and related infrastructure projects across Canada over the last two years, from 2024 to 2026 year‑to‑date ("YTD"). It follows our April 2025 bulletin 1, which examined announcements from 2023–2025 YTD, and continues our ongoing reporting of publicly announced Indigenous equity participation in major energy and infrastructure projects on a rolling two-year basis for consistency 2.

Indigenous equity investments continue to play a central role in advancing economic self‑determination and long‑term community development. Ownership interests — particularly where Indigenous communities hold significant or controlling stakes — are increasingly shaping how energy and related infrastructure projects are developed, financed, and governed.

To date, we have identified almost 200 energy and related infrastructure projects across Canada that are partially or wholly owned by Indigenous communities 3. Approximately 30% of all projects currently in our database were announced in the last two years (2024–2026 YTD). This is consistent with last year's findings 4 and reflects steady growth at a similar pace, though it may not yet capture the full impact anticipated as access to affordable capital continues to expand, particularly through government‑backed loans and loan guarantee programs. This suggests that much of that capital is still available to be deployed, indicating much more potential for growth.

1. Distribution of Indigenous Equity Investments Across Canada

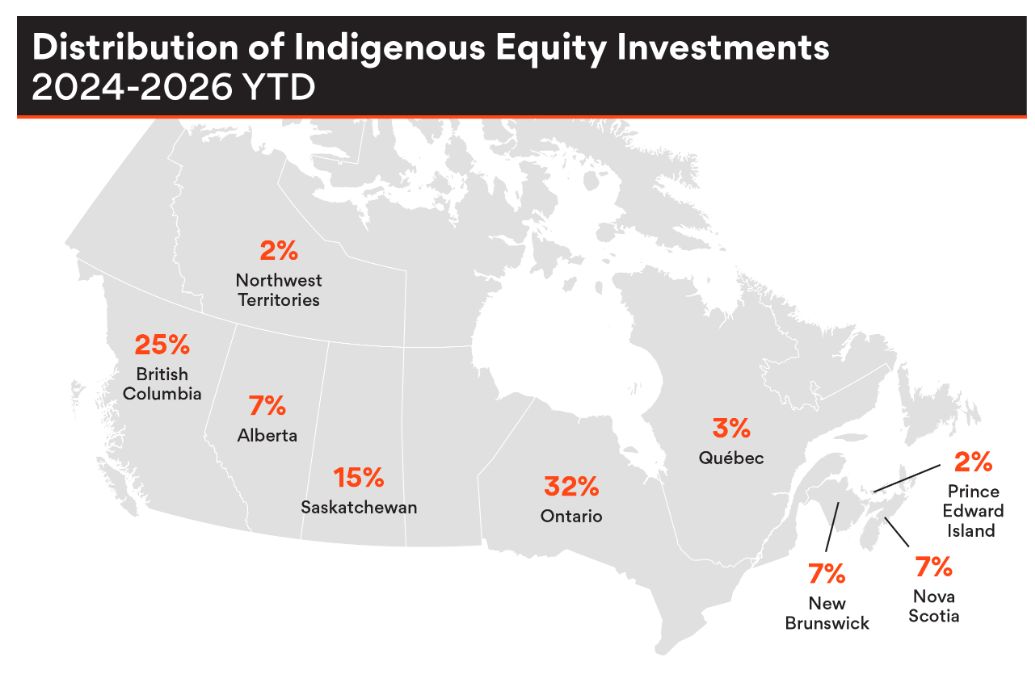

- Ontario: In the past year,Ontario has experienced notable developments and emerges as the leading province for energy projects with Indigenous equity investments, accounting for 32% of announcements in the 2024–2026 YTD period 5. Most recently, in April 2026, the Independent Electricity System Operator ("IESO") in Ontario announced it has offered 20-year contracts to 14 new renewable energy proposals (12 solar projects and two wind projects) under its ongoing competitive long term energy procurement program. All of these projects include at least 50% Indigenous equity ownership 6. These are the latest examples resulting from Indigenous equity participation incentives established by the IESO 7. Earlier in the year, in February 2026, the Ontario government announced a $250 million investment by Saugeen Ojibway Nation in Bruce Power's medical isotopes business. The transaction was supported by a provincial guarantee under the Indigenous Opportunities Financing Program, administered by the Building Ontario Fund 8. In addition, Ontario recently announced the expansion of the Indigenous Opportunities Financing Program9 and Hydro One's 50/50 First Nation equity partnership model for transmission projects 10.

- British Columbia: In our 2024 bulletin 11, we predicted that British Columbia would see an increase in projects with Indigenous equity components, driven in large part by the BC Hydro Call for Power 2024 12. That prediction has borne out, and British Columbia accounted for 25% of projects announced from 2024–2026 YTD. With additional projects from the BC Hydro Call for Power 2025 expected to be announced later this year (with mandatory Indigenous equity ownership) 13, we anticipate continued growth in the province. As well in British Columbia, in July 2025, we saw the first transaction to benefit from the newly established federal $10 billion program administered by the Canada Indigenous Loan Guarantee Corporation to provide Indigenous loan guarantees to help unlock access to the capital needed for Indigenous groups to pursue ownership in major projects. With a $738 million investment, 38 Indigenous communities in British Columbia acquired a 12.5% ownership interest in Westcoast Energy, the natural gas distribution system operated by Enbridge Inc. The investment was supported by secured bond issuances to facilitate the Indigenous equity investment, including a $400 million federal loan guarantee 14.

- Saskatchewan: A notable development this year is Saskatchewan's emergence as the jurisdiction with the third highest number of projects, representing 15% of projects announced from 2024–2026 YTD. Of these projects, eight are solar and two are wind, reflecting Saskatchewan's growing role in Indigenous‑led renewable energy development.

- Maritime Provinces: We are also seeing increased activity in the Maritime provinces. For example, in 2025, three wind energy projects with Indigenous equity were announced in New Brunswick, along with one wind energy project in Prince Edward Island. In Nova Scotia, we have seen energy project investments supported by the Canada Indigenous Loan Guarantee program. One example is the Nova Scotia energy storage project that received a significant loan from Canada Infrastructure Bank. The financing supports Indigenous equity investments by 13 Mi'kmaw communities in energy storage facilities jointly owned with Nova Scotia Power Inc 15.

- Manitoba: We have not yet seen the significant anticipated growth in projects in Manitoba, but we continue to expect increased activity as new procurement and financing frameworks take effect. Manitoba Hydro has launched a call for Indigenous majority‑owned wind projects 16, supported by a new provincial Indigenous loan guarantee program17.

- Québec: Québec remained steady, representing 3% of projects announced nationally, consistent with what we reported last year. Participation may nonetheless increase in the coming years, as recent procurement processes in Québec, aligned with the Hydro-Québec 2035 Action Plan, incentivize significant community participation by awarding substantial weighting to equity participation and, more distinctively, to community control participation exceeding 50% 18.

- Alberta: We observed a decrease in the proportion of projects located in Alberta, which accounted for 7% of projects in the 2024–2026 YTD data, down from 18% in the 2023–2025 YTD data. As noted in our previous bulletin 19, Alberta's relatively strong performance in earlier reporting periods was driven in part by Indigenous equity investments in larger oil and gas projects and existing energy infrastructure. That dynamic shifted in the 2024–2026 YTD period, where there were no announcements of new equity investments in these types of projects in Alberta. At the same time, Alberta's seven‑month pause on renewable energy development in 2023–202420, ongoing uncertainty associated with the Alberta Electric System Operator's Restructured Energy Market implementation21, and the Phase 2 Large Load integration process 22 likely contributed to fewer new project announcements and the province's declining share in the current reporting period as investors take a wait-and-see approach.

No new Indigenous equity investment announcements were identified in our 2024–2026 YTD dataset for energy and related infrastructure projects located in Manitoba, Newfoundland and Labrador, Nunavut, or the Yukon. Across all jurisdictions, the distribution of announcements in this period was: Ontario (32%), British Columbia (25%), Saskatchewan (15%), Alberta (7%), Nova Scotia (7%), New Brunswick (7%), Québec (3%), Northwest Territories (2%), and Prince Edward Island (2%).

2. Breakdown Across Sectors

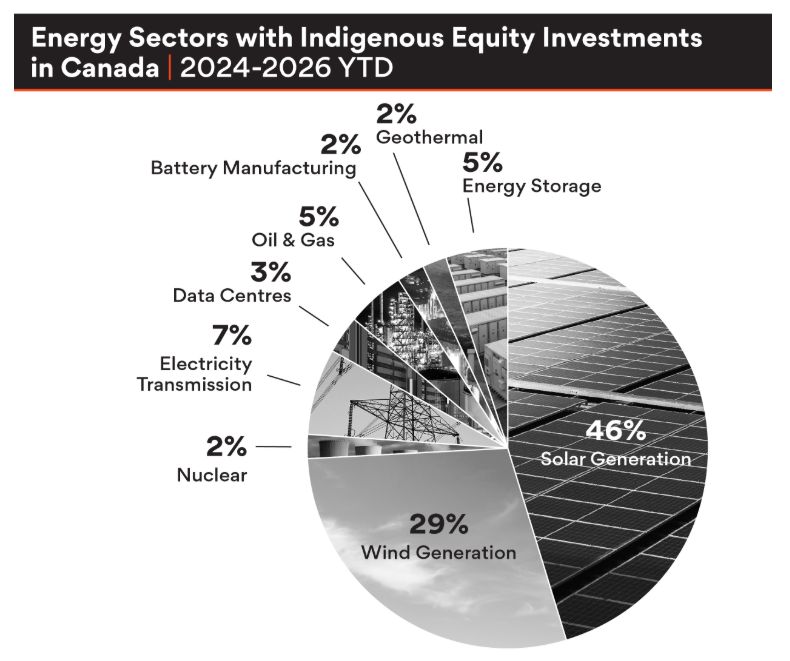

- Solar and Wind: In the 2024–2026 YTD period, solar projects have become the leading sector for new Indigenous equity investments, representing 46% of projects announced, compared to 18% in the 2023–2025 YTD dataset. This is due in large part to the contracts recently offered by IESO to 12 solar projects in Ontario. Wind has dropped to the second-highest proportion of projects, representing 29% of new investments, which is significantly lower than last year's figure (40%).

- Hydroelectric Generation: Hydroelectric generation projects, which represented a significant share (21%) of pre‑2024 investments, did not feature in recent announcements. This shift appears to align with newer equity‑driven procurement programs, such as the IESO's competitive long term energy procurement program 23 and the recent BC Hydro Calls for Power 24, which emphasized new clean energy generation, through more distributed projects with relatively shorter development and construction timelines (i.e., wind or solar projects).

- AI Data Centres: A noteworthy new trend is the emergence of AI data centres as a new project category with Indigenous equity participation. Two such projects have now been announced, one in BC and one in Alberta. While still limited in number, these investments suggest that Indigenous equity participation is beginning to extend beyond traditional energy generation into energy‑intensive digital infrastructure.

- Electricity Transmission: We also observed slight growth in electricity transmission projects, which now represent 7% of projects announced, up from approximately 4% in last year's dataset. This trend aligns with expectations that Indigenous equity will play an increasing role in transmission development, particularly as utilities such as Hydro One advance new Indigenous equity partnership models 25.

Other sectors represented in 2024–2026 YTD announcements include: oil and gas (5%), energy storage (5%), battery manufacturing (2%), geothermal (2%), and nuclear (2%) 26.

3. Size of Projects

We have observed that the average size of projects involving Indigenous equity is increasing, particularly for wind and solar developments.

For projects announced in 2024–2026 YTD, average project sizes were approximately 145.9 MW for wind projects, and 52.9 MW for solar projects. By comparison, for projects announced prior to 2024, the averages were 80.5 MW for wind, and 16.4 MW for solar. It remains an open question whether these gains are consistent with technological advancements improving equipment capacity and efficiency, or if Indigenous participation has helped to unlock development of larger projects based on other factors, such as access to capital, tax attributes and/or social license.

4. Size of Equity Interest

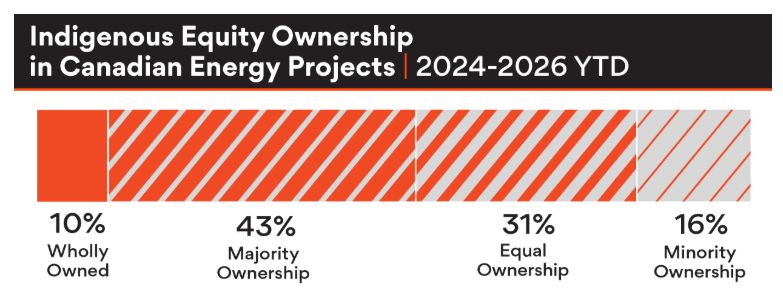

Where ownership data was publicly available for projects announced in 2024–2026 YTD, we observed a continued trend toward majority Indigenous ownership.

43% of all projects were majority‑owned by Indigenous communities (i.e., more than 50% ownership but excluding wholly owned projects), while 10% were entirely Indigenous‑owned. This represents an increase in majority‑owned projects compared to the 2023–2025 YTD dataset (up from 40%), alongside a decrease in wholly Indigenous‑owned projects (down from 22%).

An additional 31% of projects involved equal ownership between Indigenous and non‑Indigenous partners, consistent with observations in our previous bulletin. In contrast, only 16% of announced investments involved minority Indigenous ownership (less than 50%), reinforcing a clear trend in favour of at least 50% Indigenous equity ownership.

5. Number of Indigenous Communities Involved

In 2024–2026 YTD, we identified approximately 100 different Indigenous communities that announced an equity investment in this period — approximately 25 more than were identified in the 2023–2025 YTD data. This increase is partly attributable to a refinement in our methodology, as we disaggregated entities such as tribal councils and economic limited partnerships into their individual communities for the 2024–2026 YTD dataset. As a result, we expect to be able to provide more meaningful commentary on trends in community participation in future updates.

6. Conclusions

The data from 2024–2026 YTD reinforces several key conclusions from our prior bulletin: Indigenous equity participation in energy and related infrastructure projects continues to grow steadily, ownership stakes are increasingly substantial (trending to majority), and government‑driven procurement and financing frameworks are shaping outcomes.

Some new trends we observed in this data set include Ontario's emergence as the jurisdiction with the highest number of projects announced in the 2024–2026 YTD timeframe, as well as the emergence of AI data centres as a new category of projects that are financed with Indigenous equity investments.

The 2024–2026 YTD data also suggests that announcements of Indigenous equity investments in legacy energy infrastructure remain relatively limited. While announcements of Indigenous investment in existing infrastructure are still occurring, they are heavily outweighed by new renewable energy projects. Looking ahead, it remains to be seen whether other forms of existing assets, including electricity transmission, will drive another wave of Indigenous equity participation in legacy projects.

Recent policy developments, including the federal government doubling the funding available under the Indigenous Loan Guarantee Program27, the upcoming results of the BC Hydro Call for Power 2025 28, and equity or procurement model reforms in Ontario 29, Québec 30 and elsewhere, suggest that Indigenous equity participation is likely to expand further, both in scale and in scope, in the years ahead.

We will continue to monitor announcements of new Indigenous equity investments in these projects.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.