- within Insurance topic(s)

Introduction

On April 24, 2024, the U.S. Department of the Treasury ("Treasury") and the Internal Revenue Service (the "IRS") issued final regulations1 on the definition of "domestically controlled" real estate investment trusts ("REITs") (the "Final Regulations"). The Final Regulations retain the controversial "foreign-controlled domestic corporation look-through rule" from the proposed regulations, under which a domestic corporation must be "looked through" to its owners to determine whether a REIT is domestically controlled, but this rule is narrowed to apply only to non-public domestic corporations that are more than 50% owned, directly or indirectly (by value), by non-U.S. owners, rather than 25% - or greater (which was the threshold under the proposed regulations). The Final Regulations also add a limited 10-year transition rule for certain investors in existing REIT structures.

The Final Regulations are effective as of April 25, 2024.

Background

Section 897 of the Code,2 enacted as part of the "Foreign Investment in Real Property Act", or "FIRPTA", subjects a non-U.S. person to U.S. tax on any gain recognized upon a disposition of a "United States real property interest" (a "USRPI") at regular U.S. tax rates. A USRPI includes real property located in the United States or the Virgin Islands, and also equity interests in a domestic "United States real property holding corporation" (a "USRPHC"), which is generally a corporation whose assets consist of 50% or more USRPIs by value.

However, equity interests in a "domestically controlled qualified investment entity" (which includes a REIT) are not USRPIs. Therefore, a non-U.S. investor may sell shares in a domestically controlled REIT without being subject to U.S. income tax under the FIRPTA rules.

A REIT is domestically controlled if less than 50% of its stock by value is held "directly or indirectly" by foreign persons (i.e., 50% or more of its stock is held by U.S. persons) at all times during the period during which the REIT was in existence or, if shorter, the five-year period ending on the date of a sale of shares in the REIT.

The Final Regulations

Foreign-Controlled Domestic Corporations

The Final Regulations provide that, to determine whether a REIT is domestically controlled, all "look through persons" are looked through to their owners. A look-through person is any person other than a "non-look through person." A "non-look through person" is any individual, any domestic C corporation other than a "foreign-controlled domestic corporation", certain publicly-traded REITs or regulated investment companies ("RICs"), any nontaxable holder, any foreign corporation or foreign government, any publicly-traded partnership (domestic or foreign), any estate (domestic or foreign), any international organization, any qualified foreign pension fund (a "QFPF"), and any foreign trust or corporation that is directly or indirectly owned by a QFPF.

Under the Final Regulations, a "foreign-controlled domestic corporation" (which is looked through) is a non-public domestic corporation that is more than 50% owned, directly or indirectly (by value), by non-U.S. owners. The proposed regulations had provided that non-public domestic corporations that are 25% - or greater owned by non-U.S. owners are looked through. Thus, the Final Regulations are more taxpayer-friendly than were the proposed regulations. Still, the Final Regulations will limit the ability of foreign investors to invest in a REIT through a domestic blocker in order to ensure that the REIT is treated as domestically controlled.

The Transition Rule

The Final Regulations exempt an existing REIT from the foreign-controlled domestic corporation look-through rule for up to ten years, if (i) the aggregate fair market value of any USRPIs acquired by the REIT directly or indirectly after April 25, 2024 do not exceed more than 20% of the aggregate fair market value of the USRPIs held directly or indirectly by the REIT as of April 25, 2024;3 and (ii) the percentage of REIT stock held directly or indirectly by one or more non-look-through persons does not increase by more than 50 percentage points in the aggregate over the percentage of stock of the REIT owned directly or indirectly by the non-look through persons.

For purposes of the first condition of the transition rule, direct or indirect acquisitions of USRPIs or stock of a REIT under a written agreement that was binding before April 25, 2024 are treated as owned before April 25, 2024.

For purposes of the second condition, (i) the transferor corporation and resulting corporation in an F reorganization are treated as the same corporation and (ii) a class of publicly-traded REIT stock that is held by less than 5% shareholders is treated as if it is owned by a single non-look-through person (unless the REIT has actual knowledge regarding the ownership of any person).4

The transition rule will cease to apply with respect to transactions occurring on or after the earlier of (i) the date immediately following the date on which the requirements are not met and (ii) April 24, 2034 (i.e., 10 years after the effective date of the Final Regulations).

Guidance Related to Section 892

The Final Regulations omit the guidance under the proposed regulations relating to the section 892 exemption from U.S. federal income taxation for foreign governments. The preamble to the Final Regulations provides that this guidance will be addressed in separate rulemaking.

Possible Structuring In Light of the Final Regulations

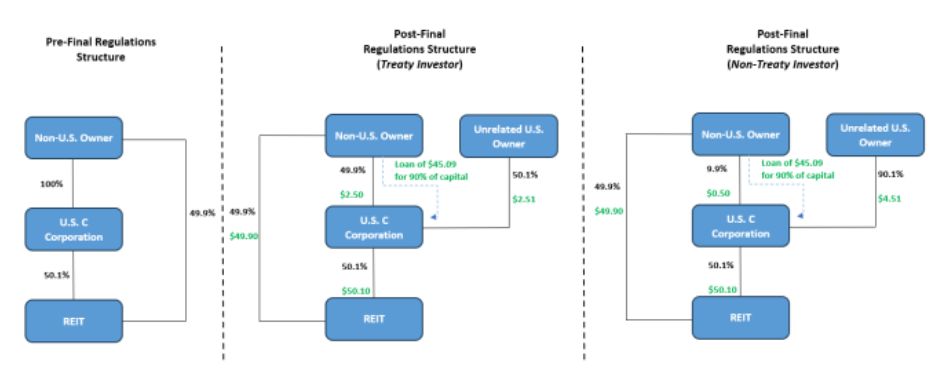

As mentioned above, a domestic C corporation cannot be more than 49.9% owned by non-U.S. persons without looking through it. However, shareholder loans by those non-U.S. shareholders can mitigate the effect of the Final Regulations.5 However, if a shareholder loan is used by non-U.S. shareholders of a domestic C corporation and those shareholders do not qualify for the benefits of a tax treaty with the United States that provides a zero rate of withholding on interest, those shareholders' interests would generally be limited to 9.9% in order to benefit from the portfolio interest exemption.6

As shown in the following picture, with 90% leverage and zero-rate treaty investors, as little as 2.51% of capital would need to come from unrelated U.S. investors (or 4.51% for non-treaty investors).

For example, assume that a REIT requires funding of $100. Non-U.S. zero-rate treaty investors could fund the REIT directly with $49.90, contribute capital of $2.50 to a U.S. C corporation, and make a loan of $45.09 to the U.S. C corporation. Unrelated U.S. investors would only have to contribute $2.51 of capital to the U.S. C corporation for 50.10% of the equity.

If the non-U.S. investors do not qualify for a tax treaty, they would fund the REIT directly with $49.90, make a loan of $45.09, and purchase 9.9% of the equity for $0.50. The unrelated U.S. investors would contribute capital of $45.01 for 90.1% of the equity of the C corporation.

Footnotes

1. T.D. 9992.

2. All references to "section" are to the Internal Revenue Code of 1986, as amended, or to the Treasury Regulations promulgated thereunder.

3. For these purposes, the fair market value of the USRPIs is the lue of that property as calculated under section 851(b)(3) or section 856(c)(4) as of the date of the most recent quarter of the REIT's taxable year before the date on which the Final Regulations are effective.

4. There is some similarity between the transition rule and the "ownership change" rule under section 382 as both rules include "increase in 50 percentage points" and "5% shareholder" concepts. It remains to be seen whether the IRS will interpret the transition rule in a similar fashion as the ownership change rule (Section 382 limits the carryforward of net operating losses and certain built-in losses following an "ownership change".).

5. This assumes that the loans are respected as indebtedness for U.S. federal income tax purposes.

6. If the non-U.S. owner is resident in a jurisdiction with a tax treaty with the United States that provides for a zero rate of withholding on interest, the non-U.S. owner could own up to 49.9% of the domestic C corporation. Otherwise (and absent a "decontrol" structure for the domestic C corporation), the non-U.S. owner would be limited to 9.9% in order to receive interest on its loan to the domestic C corporation free of U.S. withholding tax under the portfolio interest exemption.

Final Regulations On Domestically Controlled REITs

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.