- within Technology topic(s)

- with readers working within the Oil & Gas and Pharmaceuticals & BioTech industries

- within Corporate/Commercial Law topic(s)

To stay ahead of litigation trends in fast-changing markets, WIT analyzes disputes in our core practice areas to spot patterns and anticipate where the next wave of challenges may emerge. Our latest deep dive focuses on crypto parent-company activity in federal district courts.

To stay ahead of litigation trends in fast-changing markets, WIT analyzes disputes in our core practice areas to spot patterns and anticipate where the next wave of challenges may emerge. Our latest deep dive focuses on crypto parent-company activity in federal district courts. Reviewing 308 matters filed from 2000 to 2025 across 50 districts and 25 parent companies, we set out to identify which carry the most exposure, in what role, and which claims are driving the docket.

We organize exposure by segment and subsegment (exchanges and wallets, peer-to-peer payment apps, gateways, remittances, ATMs, mining hardware, hardware wallets, and smaller niches) and tie those profiles to the case types we see most often, including class actions, consumer-protection, securities, contracts, and selected IP. Let's dive into the data.

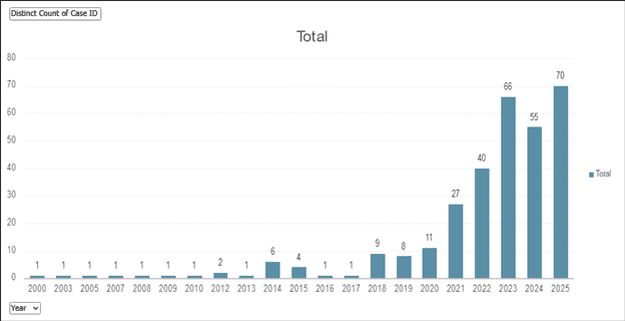

Crypto Litigation Breakdown: Cases Over Time

Nearly all filings are from the last seven years. While the data spans from 2000 to 2025, litigation didn't materially scale until 2018, when annual filings began to rise. From 2018 to 2022, filings increased from single digits to the 40s. Between 2023 and 2025, activity increased sharply, with 191 matters filed, representing more than 60% of the total. This reflects a maturing enforcement landscape as consumer adoption grew, platforms diversified their offerings, and regulators raised expectations around disclosures, custody, and access. It also means most cases involve modern products and updated contracts, requiring increased expert insight into today's systems rather than legacy ones.

Q: Where is the litigation volume, and how concentrated is it?

A: Volume sits with a short list of platforms. Cash App (Block) (104), Coinbase (71), Kraken 20, Gemini (18), Ripple (16), and BitPay (14) account for 243 of 308 matters (79%); Cash App and Coinbase alone make up 175 filings (57%). The remaining 65 cases are distributed across 19 other companies, most appearing just once or twice. This concentration highlights where litigation pressure is building, and where counsel and experts are most likely to be engaged repeatedly across similar product lines and user-facing services.

Q: What roles do crypto parent companies play across these cases?

A: As mentioned before, the vast majority of parent companies appear as defendants: 278 out of 308 matters overall. That trend is strongest among consumer-facing software platforms, particularly those offering digital wallets, exchanges, or peer-to-peer payment apps. Companies like Cash App, Coinbase, Kraken, and Gemini are nearly always defending against claims tied to onboarding practices, transaction disclosures, listing decisions, or security incidents. By contrast, hardware and mining companies such as Bitmain appear more evenly split between plaintiff and defendant roles. Their filings often involve efforts to protect proprietary technology, enforce distribution agreements, or defend against product liability claims tied to device performance.

| Total Cases by Role & Parent Company | |||

| Parent company | Defendant | Plaintiff | Grand Total |

| Cash App (Block Inc.) | 99 | 5 | 104 |

| Coinbase Global Inc. | 70 | 1 | 71 |

| Kraken | 19 | 1 | 20 |

| Gemini | 14 | 4 | 18 |

| Ripple Labs (RippleNet) | 13 | 4 | 16 |

| BitPay | 13 | 1 | 14 |

| Bitmain Technologies | 4 | 6 | 10 |

| Crypto.com | 8 | 2 | 10 |

| Ledger SAS | 9 | 9 | |

| OpenSea | 5 | 5 | |

| Canaan (Avalon) | 4 | 1 | 5 |

| Byte Federal | 4 | 1 | 5 |

| Bitcoin Depot | 4 | 1 | 5 |

| Genesis Coin Inc. | 4 | 1 | 5 |

| Solana Labs & Solana Foundation | 3 | 3 | |

| coinme | 2 | 1 | 3 |

| KIOSK Information Systems | 2 | 1 | 3 |

| Coinsource | 2 | 2 | |

| Cardano Foundation / IOHK / Emurgo | 1 | 1 | |

| Uniswap Labs | 1 | 1 | |

| Olea Kiosks | 1 | 1 | |

| Strike (Zap Solutions) | 1 | 1 | |

| MakerDAO | 1 | 1 | |

| Bitdeer / DesiweMiner | 1 | 1 | |

| KeepKey (ShapeShift) | 1 | 1 | |

| Grand Total | 278 | 31 | 308 |

Q: Which segments in crypto are seeing the most litigation?

A: Most litigation falls under the software segment, which accounts for over 80% of all matters. These are disputes involving digital wallets, exchanges, and P2P payment platforms, which are tools that interact directly with consumers and draw scrutiny over onboarding, disclosures, transaction visibility, and security events. The hardware segment accounts for about 16%, with litigation tied to performance, branding, or distribution of devices like mining rigs, ATMs, and hardware wallets. While software cases trend toward consumer and securities claims, hardware disputes more often involve IP, contracts, or product liability issues.

| Total Case Count by Parent Company & Segment | |||||

| Parent company | End-use DeFi & NFTs | Hardware | Software | Type of Cryptocurrency | Grand Total |

| Cash App (Block Inc.) | 104 | 104 | |||

| Coinbase Global Inc. | 71 | 71 | |||

| Kraken | 20 | 20 | |||

| Gemini | 18 | 18 | |||

| Ripple Labs (RippleNet) | 16 | 16 | |||

| BitPay | 14 | 14 | |||

| Bitmain Technologies | 10 | 10 | |||

| Crypto.com | 10 | 10 | |||

| Ledger SAS | 9 | 9 | |||

| OpenSea | 5 | 5 | |||

| Canaan (Avalon) | 5 | 5 | |||

| Byte Federal | 5 | 5 | |||

| Bitcoin Depot | 5 | 5 | |||

| Genesis Coin Inc. | 5 | 5 | |||

| Solana Labs & Solana Foundation | 3 | 3 | |||

| coinme | 3 | 3 | |||

| KIOSK Information Systems | 3 | 3 | |||

| Coinsource | 2 | 2 | |||

| Cardano Foundation / IOHK / Emurgo | 1 | 1 | |||

| Uniswap Labs | 1 | 1 | |||

| Olea Kiosks | 1 | 1 | |||

| Strike (Zap Solutions) | 1 | 1 | |||

| MakerDAO | 1 | 1 | |||

| Bitdeer / DesiweMiner | 1 | 1 | |||

| KeepKey (ShapeShift) | 1 | 1 | |||

| Grand Total | 6 | 50 | 248 | 5 | 308 |

At the subsegment level, two categories dominate. Digital wallets and exchanges appear in 117 matters, led by Coinbase, Kraken, Gemini, and Crypto.com. These cases often raise issues around asset listings, platform fees, and regulatory classification of tokens. Peer-to-peer payment apps, driven almost entirely by Cash App, account for 104 cases and tend to focus on internal controls, error resolution, and consumer claims. The remaining subsegments including crypto ATMs (24), payment gateways (14), remittance platforms (17), mining rigs (16), and hardware wallets (10) show smaller volumes but distinct risk profiles. A final group of niche categories including NFT marketplaces (5), platform tokens (4), DeFi platforms (1), and stablecoins (1) rounds out the docket and may signal areas of future growth.

Q: What types of claims are driving these disputes?

A: Four claim types dominate: class actions (101), consumer protection (79), securities (63), and contract disputes (39). Together, these account for more than 90% of the docket. Platforms tend to face multiple overlapping claims, particularly around how products are advertised, what users are told (or not told) at onboarding, how assets are listed or delisted, and how platforms respond when things go wrong. Hardware and infrastructure companies face a different mix: fewer securities claims, but more IP, contract, and product-based disputes. We also see smaller pockets of IP litigation including patent (17) and trademark (16), alongside lower counts in areas like civil rights, internet law, employment, and antitrust.

Q: How diversified are parents across brands or affiliates?

A: Many parents operate across multiple products or subsidiaries. The dataset includes 58 child entities under 25 parent companies, signaling layered corporate structures and varied risk across business lines. This matters for discovery. Product teams, contracts, disclosures, and technical implementation may differ between affiliates. Counsel should treat early mapping of entities and data custodians as essential, not just to avoid missed records, but to ensure expert analysis reflects the right version of the platform, wallet, ATM software, or device at issue.

| Count of Child Companies by Parent Companies | |

| Parent Company | Child Companies |

| Cash App (Block Inc.) | 7 |

| Kraken | 7 |

| Coinbase Global Inc. | 5 |

| Bitcoin Depot | 4 |

| Bitmain Technologies | 4 |

| Crypto.com | 4 |

| Solana Labs & Solana Foundation | 2 |

| OpenSea | 2 |

| Ledger SAS | 2 |

| BitPay | 2 |

| Ripple Labs (RippleNet) | 2 |

| coinme | 2 |

| Uniswap Labs | 2 |

| Genesis Coin Inc. | 2 |

| Olea Kiosks | 1 |

| MakerDAO | 1 |

| Strike (Zap Solutions) | 1 |

| Canaan (Avalon) | 1 |

| Coinsource | 1 |

| KIOSK Information Systems | 1 |

| Gemini | 1 |

| Byte Federal | 1 |

| Cardano Foundation / IOHK / Emurgo | 1 |

| Bitdeer / DesiweMiner | 1 |

| KeepKey (ShapeShift) | 1 |

| Grand Total | 58 |

Q: What should counsel prioritize based on these crypto litigation trends?

A: For platform parents, plan for defense-oriented strategies across class action, consumer protection, and securities claims. Standardized discovery kits will help as KYC/AML protocols, asset listing histories, fee disclosures, terms of service, marketing materials, customer support logs, and incident reports come up repeatedly. For hardware and infrastructure companies, expect more IP and contracts work including ownership documentation, branding and distribution agreements, supply chain controls, and product testing evidence. Across all segments, choosing experts with both technical fluency and regulatory familiarity will be key. Courts are now seeing these products less as novelty and more as infrastructure, which raises the stakes for getting expert testimony right.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.