PREFACE

The recent financial crisis has resulted in the largest number of bank failures since the savings and loan crisis in the late 1980s and early 1990s ("S&L Crisis"). In March 1982, as the General Counsel to both the Federal Home Loan Bank Board and the Federal Savings and Loan Insurance Corporation (which was later merged into the Federal Deposit Insurance Corporation ("FDIC")), I introduced the policies and standards upon which directors and officers of failed banks would be held responsible for any misconduct. Those policies were followed by a similar statement issued in 1992 by the FDIC.

During the S&L Crisis, directors, officers, attorneys, accountants and other professionals became the prime targets of litigation conducted by the FDIC and the Resolution Trust Corporation ("RTC") seeking to recover losses sustained by failed banks. In the aftermath of the S&L Crisis, the FDIC and the RTC brought suit or settled claims against hundreds of former directors and officers of failed banks and recovered approximately $1.3 billion in claims against former directors and officers. The FDIC is now again initiating an aggressive litigation strategy against the former directors and officers of recently failed banks.

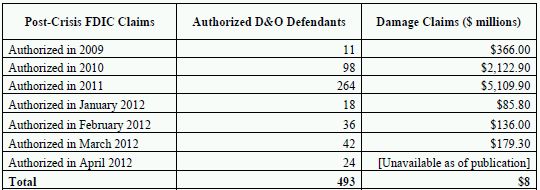

In preparation for this latest wave of litigation, the FDIC has been increasing its internal legal staff and engaging outside law firms to perform professional liability investigations and to prosecute claims. To date, the FDIC has commenced twenty-nine lawsuits as of April 25, 2012 against former directors or officers of recently failed banks. In addition, the FDIC has announced that it has authorized lawsuits against 493 individuals for D&O liability in connection with recently failed banks in an effort to recoup over $8 billion in losses.

While seeking to recover from those responsible for a bank's failure is a fundamental part of any system that includes a federal safety net (such as FDIC deposit insurance), the FDIC's decision to commence failed bank litigation should not be influenced by a desire simply to collect damages from anyone who happened to be at the scene of the accident when the bank failed, whether or not they were responsible for the bank's failure or its losses. Any decision by the FDIC to sue the former directors and officers of a failed bank should only be made in compliance with the highest standards expected of a federal agency when it mounts an attack on an individual.

This guide has been prepared to assist directors and officers who may potentially find themselves opposite the FDIC in a lawsuit to understand how to avoid an investigation or to respond as effectively as possible.

Thomas P. Vartanian

Washington, D.C.

FDIC PROFESSIONAL LIABILITY INVESTIGATIONS

An insured depository institution ("bank") fails when it is seized by its primary banking regulator and its charter is terminated. The bank's primary regulator immediately appoints the FDIC as receiver for the bank (or, in rare circumstances, as conservator for the institution). By operation of law, the FDIC, as receiver, succeeds to all rights, titles, powers and privileges of the insured depository institution, and of any stockholder, member, accountholder, depositor, officer or director of such institution with respect to the institution and the assets of the institution.

It is important to note that the FDIC wears several hats: (i) in its capacity as a regulator, the FDIC has back-up supervisory responsibility for all insured depository institutions and is the primary federal regulator of state non-member banks; (ii) in its corporate capacity, the FDIC is responsible for maintaining the Deposit Insurance Fund ("DIF"); and (iii) in its capacity as receiver or conservator, the FDIC has responsibility for resolving or rehabilitating failed insured depository institutions. As a result of these distinct roles, an action commenced by the FDIC in its capacity as receiver of a failed bank is not a claim by the FDIC in its corporate capacity as a regulatory agency.

Among the most important assets acquired by the FDIC, as receiver, is the right to bring professional liability claims against a failed bank's former directors and officers and its accountants, attorneys, appraisers and other professionals. Professional liability claims are claims brought by the FDIC to recover losses sustained by a failed bank as a result of the acts or omissions of the bank's former directors and officers and other professionals, and such claims may ultimately result in civil claims.

Following the closure of an insured depository institution, the FDIC's professional liability division will conduct an investigation to determine, among other things, whether the failed institution's former directors, officers or third-party professionals were responsible for the institution's losses and, if so, how to hold them accountable. The FDIC's professional liability section generally opens as many as eleven different types of professional liability investigations with respect to each failed institution, including, but not limited to, investigations of directors, officers, attorneys, accountants, fidelity bond carriers, appraisers and perpetrators of mortgage fraud. The extent to which the FDIC will investigate the circumstances surrounding the failure of an insured depository institution will depend upon several factors, including the extent of any losses suffered by the institution. If the institution has suffered relatively few losses, the FDIC may take the view that any investigation or lawsuit conducted to recoup such small losses would not be cost effective. Whether the FDIC initiates an investigation or ultimately brings a lawsuit does not ensure that the primary state or federal bank regulators will not begin their own administrative enforcement proceedings, or that the Department of Justice ("DOJ"), which has jurisdiction with regard to criminal liability and concurrent jurisdiction with regard to civil liability, will not also jump into action. Thus, there may be multiple fronts to be concerned about after a financial institution fails.

During the course of a professional liability investigation, the FDIC may make a pre-litigation demand on the former directors or officers of the failed bank for the payment of civil money damages and may send a copy of the demand letter to the appropriate insurance carrier(s). The purpose of such demand letters is to put the director or officer on notice of a potential lawsuit and to provide the requisite notice to the appropriate insurance carrier(s) of a "claim" made against the insured director and officer under the applicable insurance policy, in order to preserve insurance coverage as a potential source of recovery in the event that litigation is commenced and liability is established.

The FDIC reportedly has already sent hundreds of "demand" letters to former officers, directors and other employees of failed banks, as well as to their professional liability insurers, putting them on notice of potential claims. While the FDIC generally does not publicly release its demand letters, they may become public through disclosure in court proceedings, among other avenues. For instance, the demand letter sent by attorneys representing the FDIC to fifteen directors and officers of BankUnited, FSB, which was closed by the Office of Thrift Supervision in May 2009, was attached to a motion filed in a bankruptcy court. In addition to sending demand letters, the FDIC may issue subpoenas to the former directors and officers of a failed bank requiring them to testify at a deposition or produce documents relating to their personal financial affairs, including a personal financial statement showing their net worth. Such subpoenas may be issued prior to the FDIC actually initiating a lawsuit.

The FDIC's Office of Inspector General ("FDIC OIG") also may conduct an independent investigation into the reasons for an institution's failure. The FDIC OIG's Office of Material Loss Reviews is statutorily required to complete a "material loss review" with respect to the failure of insured institutions that cause material losses to the DIF. A material loss review consists of an investigation of the FDIC's supervision of the institution, including the implementation of prompt corrective action, a determination as to why the institution's problems resulted in a material loss to the DIF and recommendations to prevent future losses. The FDIC-OIG's material loss reports may also identify the actions or omissions of the institution's former directors and officers as a major cause for the institution's failure. As such, these reports may act as a road map for the FDIC and other potential plaintiffs to follow in seeking to bring professional liability claims against those allegedly responsible for the institution's failure, including directors and officers.

An FDIC professional liability investigation may take an extended period of time to complete. The FDIC has a stated goal of seeking to make a decision whether or not to pursue professional liability claims against a failed institution's former directors, officers and other professionals within 18 months of the institution's failure. The FDIC does not always complete its investigation within 18 months, however, and there may be a significant time lag between the date of an institution's failure and the date on which any litigation is actually commenced by the FDIC. In that regard, the FDIC generally has three years from the date a bank fails and the receivership begins to bring a breach of fiduciary duty case against the former directors and officers of a failed depository institution. As part of the investigation process, however, the FDIC may seek to enter into tolling agreements with potential defendants to allow settlement discussions to proceed without the need for the FDIC to file a lawsuit within the otherwise applicable statute of limitations.

In addition to conducting an investigation to determine the possibility of bringing civil claims arising from a bank's failure, the FDIC's investigators will seek to identify signs of possible criminal activity. While the FDIC has no criminal jurisdiction, it may refer potential cases to the DOJ. The FDIC OIG also may work with the Federal Bureau of Investigation on matters involving suspected criminal activity.

Directors and officers of a failed institution should be alert to the possibility that they may be the subject of both civil and criminal claims. Individuals may wish to assert certain rights, including Fifth Amendment rights, in a criminal proceeding that may not be available or may have adverse consequences in a civil suit. The existence of parallel investigations or judicial proceedings may have a significant impact on defense strategy.

|

CASE STUDY In July 2010, two former senior officers of Integrity Bank of Alpharetta, Georgia, a $1 billion institution that was placed into FDIC receivership in August 2008, pled guilty to criminal charges that included counts of conspiracy to commit bank fraud, receiving bribes, tax evasion, securities fraud and insider trading. This law enforcement action was part of President Obama's interagency Financial Fraud Enforcement Task Force, which was established in November 2009 to wage an aggressive, coordinated and proactive effort to investigate and prosecute financial crimes. The task force includes representatives from a broad range of federal agencies (including each of the federal banking agencies), regulatory authorities, inspectors general and state and local law enforcement who, working together, bring to bear a powerful array of criminal and civil enforcement resources. Cases such as this point out the need to treat even what may appear to be a civil-focused investigation of a bank failure with great care given the potential for DOJ intervention under either its civil or criminal authority. |

While the FDIC is the most likely plaintiff in any lawsuit against the former directors and officers of a failed bank, other potential plaintiffs include the institution's shareholders, creditors and employees, other government agencies, other federal or state banking regulators through their enforcement authority jurisdiction and the trustee of the institution's holding company if the parent is placed in bankruptcy. These potential plaintiffs may "compete" with one another in order to establish their right to sue the directors and officers of a failed institution in order to recoup their losses.

While such actions are beyond the scope of this manual, the FDIC and its sister agencies have also sought recoveries from third party advisors, vendors and holding companies and their shareholders that might have been responsible for the failure of the bank. Indeed, lawyers and accountants have frequently been sued where there is an alleged connection between their actions and a loss to the bank. Holding companies and their shareholders have not often been the target of an FDIC claim, but there is at least one significant precedent to note. After Superior Bank, FSB, of Hinsdale, Illinois failed in 2001, the FDIC Inspector General found that "the failure of Superior Bank was directly attributable to the Bank's Board of Directors and executives ignoring sound risk management principles." Without a suit being filed, owners of the thrift's holding company agreed to pay $460 million to the FDIC to settle all claims.

More recently, as a result of the failure of Guaranty Bank, of Austin, Texas in 2009, the FDIC has assigned certain receivership claims to the liquidation trustee in the bankruptcy proceeding of the thrift's holding company, Guaranty Financial Group, Inc. ("GFG"). The liquidation trustee has brought an action against GFG's former parent company, Temple-Inland, Inc., alleging fraudulent transfers for the benefit of Temple-Inland and a breach of fiduciary duty in connection with Temple-Inland's spin-off of GFG. These cases often raise more complex issues and defenses than D&O cases do.

|

FDIC INVESTIGATIVE ELEMENTS During an FDIC professional liability investigation of the failure of an insured depository institution, the FDIC's investigators and attorneys will seek to:

|

THE FDIC POLICY STATEMENT

In the aftermath of the S&L Crisis, and in response to concerns expressed by representatives of the banking industry and others regarding civil damage litigation risks to directors and officers of federally insured banks, the FDIC issued in 1992 a Statement Concerning the Responsibilities of Bank Directors and Officers ("Policy Statement"). The Policy Statement provides that the filing of lawsuits by the FDIC against former directors and officers of failed banks is authorized only after a rigorous review of the factual circumstances surrounding the bank's failure if (1) the claim would be sound on the merits and (2) litigation would likely be cost-effective.

In determining whether litigation will be cost-effective, the FDIC considers whether the defendant has sufficient personal assets or insurance coverage to pay any damages. In cases where there is sufficient evidence of wrongdoing, but not enough reliable sources of recovery for the FDIC to justify the cost of pursuing litigation, the FDIC still may refer the matter to the institution's primary bank regulator to take appropriate supervisory and enforcement action. In addition, in matters involving suspected criminal activity, the FDIC may make criminal referrals and provide ongoing support to the DOJ, which also has concurrent civil liability jurisdiction.

An important factor considered by the FDIC in determining whether to sue the former directors of a failed bank is the distinction between inside and outside (independent) directors. In contrast to an inside director, who may be an officer of the institution or its controlling shareholder, an outside director usually has no connection to the bank other than his or her directorship and, perhaps, a small or nominal shareholder position. Outside directors generally do not participate in the conduct of the day-to-day business operations of the institution. The most common suits brought against outside directors involve insider abuse or situations where the directors failed to heed warnings from regulators, accountants, attorneys or others that there was a significant problem in the bank that required correction. In the latter instance, if directors fail to take steps to implement corrective measures, and the problem continues, the directors may be held liable for losses incurred after the warnings were given.

|

ELEMENTS OF AN FDIC SUIT The following are common examples of lawsuits brought by the FDIC against the former directors and officers of failed institutions:

|

THE STANDARD FOR ESTABLISHING LIABILITY

An important threshold issue that arises in FDIC litigation against the former directors and officers of a failed bank is the degree of wrongdoing the FDIC must prove in order to establish liability. In that regard, the critical issue is whether it is sufficient for the FDIC to prove that the former directors or officers engaged in mere negligence, or whether the FDIC must prove a greater degree of culpability, such as gross negligence or intentional wrongdoing. Proving a greater degree of culpability is obviously more difficult. A related question is whether federal or state law establishes the applicable standard of care for this purpose. Congress sought to address these and other issues when it enacted the Financial Institutions Reform Recovery and Enforcement Act of 1989 ("FIRREA").

Prior to the enactment of FIRREA, a number of states adopted statutes that sought to insulate bank directors and officers from liability by providing that a bank's organizational documents may limit the civil liability of its directors and officers by requiring proof of gross negligence or a higher degree of culpability to establish liability. In enacting FIRREA, Congress sought to limit the effect of such insulating statutes as they applied to lawsuits brought by or on behalf of the FDIC, as receiver of a failed institution. Under FIRREA, a director or officer of a federal or state insured depository institution may become personally liable for money damages in any civil action brought by or on behalf of the FDIC for "gross negligence," including any similar conduct or conduct that demonstrates a greater disregard of a duty of care, including intentional tortuous conduct, as such terms are defined and determined under applicable state law.

There was significant dispute as to the impact of FIRREA on liability standards until the U.S. Supreme Court addressed the issues in Atherton v. FDIC, 519 U.S. 213 (1997). In that case, the Supreme Court held that FIRREA preempted state law to the extent that state law would require the FDIC to prove a greater level of culpability than gross negligence (such as intentional wrongdoing) in order to establish a breach of duty of care by directors or officers of the failed institution. Importantly, the Supreme Court also concluded that if state law provided that directors and officers of a bank could be found liable upon a lesser showing of culpability (such as mere negligence), the FDIC need only prove a breach of such lesser standard of care (and not gross negligence) to establish liability.

|

IMPORTANT DEFENSIVE CONSIDERATIONS: ACTIONS BEFORE THE BANK FAILS Obviously, the best way for directors and officers to avoid FDIC litigation is to ensure that the bank does not fail. That can be a difficult task, particularly where the bank's precarious financial position results from a sharp downturn in the economy. The following are important tools to guard against potential liability:

|

DEFENSES TO LIABILITY

A. Business Judgment Rule

With respect to FDIC claims against directors and officers involving negligence or breach of fiduciary duty, the first layer of defense will often be reliance upon the business judgment rule. The business judgment rule protects directors and officers from liability, even if they make a wrong decision, as long as they acted prudently and in good faith under the circumstances. Under the rule, a director is entitled to rely on management, advisers and others to perform their duties properly, unless the director knew or should have known such reliance was misplaced. In appropriate circumstances, the business judgment rule may shield the former directors and officers of failed banks from suits brought by the FDIC based upon a theory of negligence or breach of fiduciary duty. The business judgment rule is only as good as the record that was created, however, and accurate board minutes are essential in that regard.

In FDIC v. Cassetter, 184 F.3d 1040 (9th Cir. 1999), the Ninth Circuit Court of Appeals held that when directors acted under the belief that their actions were in the best interests of the bank, the California business judgment rule insulated the directors from liability. More recently, in a suit against officers and directors of Integrity Bank, a Georgia district court held that Georgia's business judgment rule protected directors against the FDIC's claims of mere negligence, carelessness, and lackadaisical performance of their duties. (See section below on "Recent FDIC Litigation.")

In another recent case, the former CEO of IndyMac Bank asserted the California business judgment rule as a defense to FDIC claims. In July 2011, a California district court held that the state's business judgment rule only protected directors and did not protect corporate officers. The ruling is on appeal to the Ninth Circuit.

B. Statute of Limitations Defense

The statute of limitations may also provide a defense to claims brought by the FDIC. Under the Federal Deposit Insurance Act ("FDI Act"), a special statute of limitations applies to contract or tort actions brought by the FDIC as receiver or conservator of a failed institution. The FDI Act provides that, notwithstanding any provision of any contract, the applicable statute of limitations with regard to any contract claim brought by the FDIC as conservator or receiver is six years beginning on the date the claim accrues or, if longer, the period applicable under state law. In the case of any tort claim, the statute of limitations generally is three years beginning on the date the claim accrues or, if longer, the period applicable under state law. For these purposes, the date on which the statute of limitations begins to run on any contract or tort claim is the later of (1) the date of the appointment of the FDIC as conservator or receiver or (2) the date on which the cause of action accrues.

Professional liability actions brought by the FDIC against the former directors and officers of a failed depository institution are usually tort claims. Thus, the FDIC generally has three years from the date of its appointment as receiver for the failed institution to file such claims. A special provision of the FDI Act provides, however, for the revival of certain expired state causes of action. The FDI Act provides that with respect to any claim arising from fraud, intentional misconduct resulting in unjust enrichment or intentional misconduct resulting in substantial loss to a failed institution, the FDIC may bring such claim as receiver or conservator without regard to the expiration of the statute of limitation applicable under state law, so long as the statute of limitations for such action did not expire not more than five years before the appointment of the FDIC as conservator or receiver.

C. Causation

In order for the FDIC to prevail in a suit against a director or officer, it must prove that the losses incurred by the failed bank were caused by the acts or omission of the director or officer. A near collapse of the world's financial markets followed by a deep recession may provide interesting and useful defenses and arguments regarding the allocation of blame and liability for a failed bank's losses. While the defense may assert that comprehensive market dislocations caused the demise of a particular bank, there are likely to be counter-arguments concerning the specific facts at the institution in question that the FDIC will make and to which a defendant must be prepared to respond.

D. Negligent Supervision and Regulation by the Banking Regulators

Directors and officers sued by the FDIC may seek to defend themselves in such actions by asserting that the appropriate banking regulators failed to properly supervise or regulate the institution. This defense is particularly difficult to establish as courts have tended not to be receptive to second-guessing banking regulators' conduct.

E. Contributory Negligence and Mitigation of Damages

Directors and officers may also seek to defend themselves by alleging that the post-receivership conduct of the FDIC, as receiver, caused or contributed to the losses sustained by the failed institution. Federal district courts have issued mixed rulings as to whether such defenses may be asserted.

F. Losses Caused by Third Parties

Directors or officers may also seek to prove that the institution's losses resulted not from their acts or omissions, but from the acts or omission of third parties, including the company's financial advisers, auditors, lawyers or other professional advisers. Under principles of proximate causation, the losses recoverable from directors and officers may be reduced to the extent that the institution's losses are attributable to the wrongful acts of third parties, and the directors may be able to seek contribution from them based on the parties' comparative fault.

DIRECTOR AND OFFICER INSURANCE COVERAGE

Directors and officers of insured depository institutions are typically covered under D&O insurance policies, which may provide protection against liability for claims for negligence, gross negligence or breach of fiduciary duty. Such policies typically exclude from coverage losses resulting from dishonesty, fraud and other intentional misconduct. Certain losses arising from such dishonest or fraudulent acts may be separately covered under fidelity bond insurance policies purchased by an insured depository institution. Criminal behavior is typically not insurable.

During the S&L Crisis, D&O liability insurance and fidelity bonds were a principal source of recovery for alleged misfeasance and malfeasance by directors and officers. Beginning in the early 1980s, insurance carriers began to include a number of exclusionary endorsements in D&O liability insurance policies and fidelity bonds purchased by financial institutions. One exclusionary endorsement that began to be added to insurance policies during the 1980s was the so-called "regulatory exclusion" provision. A regulatory exclusion provision seeks to exclude from coverage all claims brought by any government agency, including any claim by the FDIC, as receiver of a failed institution, against an insured party. Until FIRREA was enacted, a number of courts found that regulatory exclusions were generally unenforceable because such provisions were ambiguous or against public policy. Following the enactment of FIRREA, however, courts began to uphold regulatory exclusion provisions, often citing the failure of Congress in FIRREA to express a specific public policy against enforcing such provisions.

A second exclusionary endorsement that began to be added to insurance policies was the so-called "insured-versus-insured" exclusion. This exclusion began to be added to D&O insurance policies as a reaction to several lawsuits in the mid-1980s in which insured corporations sued their own directors to recoup operational losses caused by improvident or unauthorized actions. Under the insured-versus-insured exclusion, claims made by one insured party against another insured party are excluded from coverage under the insurance policy. When the FDIC is appointed as receiver for a failed institution, the insurance carrier may seek to invoke the insured-versus-insured exclusion in order to deny coverage for any claims made by the FDIC, as receiver of a failed institution, against the former directors and officers of the failed institution.

The insurance carrier may argue that the FDIC steps into the shoes of the failed institution (an insured party) upon its appointment as receiver, and thus no coverage exists when the FDIC makes a claim against the institution's former directors and officers (also insured parties) because of the insured-versus-insured exclusion. Similarly, an insurance carrier may seek to invoke the insured-versus-insured exclusion to deny coverage for claims brought by a bankruptcy trustee or debtor-in-possession against the former directors or officers of a bankrupt holding company of a depository institution in receivership.

D&O insurance coverage may also be available through a D&O policy at the level of the institution's holding company. The availability of funds under such coverage may be the subject of dispute if, as is often the case, the institution's holding company is in bankruptcy. In such circumstances, the court may place limitations on the use of funds available under the insurance policy.

DIRECTOR AND OFFICER INDEMNIFICATION

An insured depository institution may seek to indemnify its officers, directors and employees against expenses and costs incurred in civil, criminal or administrative actions. The provisions governing indemnification and advance of expenses may be set forth in the institution's bylaws or through a separate indemnification agreement with a director, officer or employee of the institution. Indemnification provided by an insured depository institution to its directors and officers is subject to the requirements of federal laws, rules and regulations (as well as state rules if a state-chartered bank), which may in certain circumstances limit the making of indemnification payments or the advancement of expenses.

Indemnification coverage, particularly provisions for the advancement of fees, is generally a valuable resource to a director or officer in the event of a lawsuit. The right to have one's legal fees covered throughout an ongoing suit or administrative action is critical to most individuals, who do not normally have the resources to fight the U.S. government. The ability to engage and pay for experienced counsel in these situations is a large part of the battle. Said another way, if legal fees cannot be advanced and the individual must cover them on an ongoing basis until there is a resolution that qualifies for indemnification, it often means that the individual cannot adequately defend himself and may have to accept a very unfavorable settlement.

In the context of failed bank litigation, however, the right of the institution's former directors and officers to be indemnified or have fees advanced by the failed institution may have little or no value once the FDIC is in charge of the bank. A number of courts have held, when an insured depository institution's former directors or officers were sued by the RTC as receiver of such institution, that indemnification from the failed institution was simply unavailable. Furthermore, even if indemnification liability could be established on the part of the receivership estate by a former director or officer of the failed institution, the claim for payment would be an unsecured general creditor claim against the receivership and not against the FDIC in its corporate capacity, which would be paid, if at all, only after the payment in full of all secured creditor claims and administrative expenses.

Indemnification may, however, be available under the parent holding company's indemnification provisions that extend to directors and officers of subsidiary institutions. As a practical matter, the value of such indemnification rights may be limited if the holding company itself is in bankruptcy or in a troubled financial condition. These are issues that a director should assess at the time he or she goes on the board.

RECENT FDIC LITIGATION

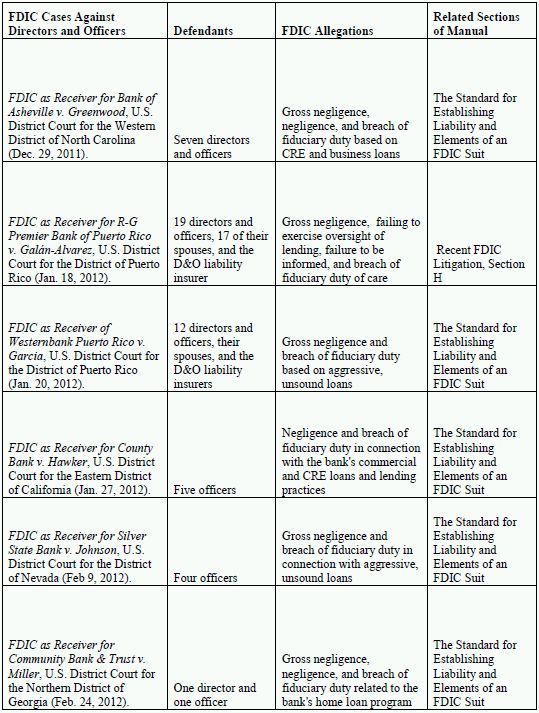

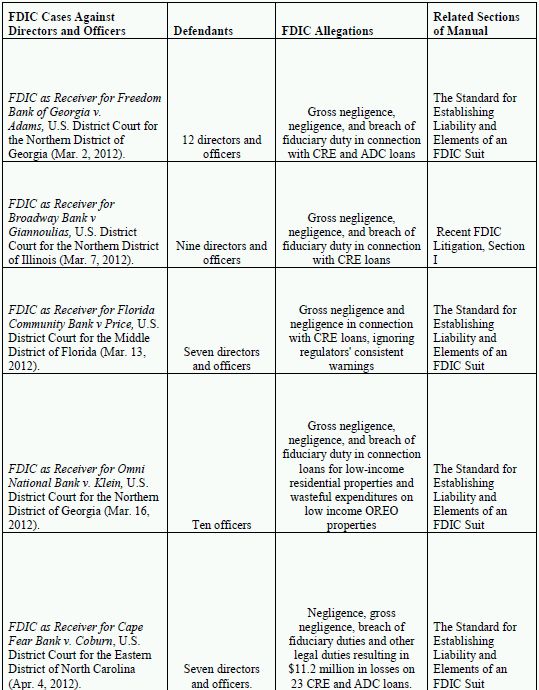

To date, the FDIC has commenced fourteen lawsuits against former directors or officers of recently failed depository institutions. A brief description of some of the lawsuits commenced by the FDIC is provided below:

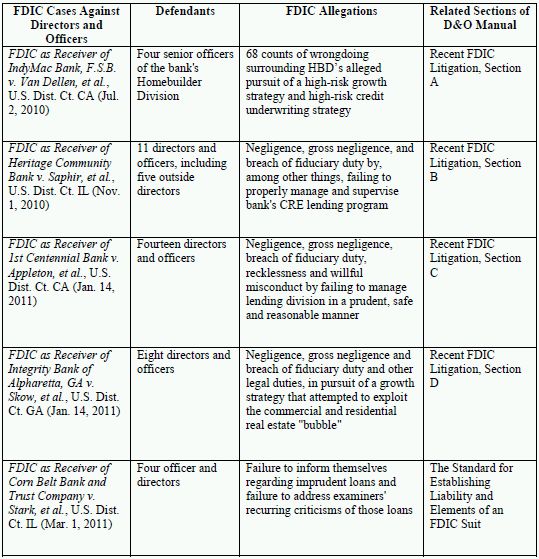

A. IndyMac Bank

Approximately two years after IndyMac Bank, F.S.B. ("IndyMac") was closed by the OTS in July 2008, the FDIC, as receiver of IndyMac, brought suit in a federal district court in California against four former senior officers of IndyMac's Homebuilder Division ("HBD").

The complaint, which runs over 300 pages and includes 68 counts of alleged wrongdoing, revolves around HBD's alleged pursuit of a high-risk growth strategy an d high-risk credit underwriting strategy. The allegations made by the complaint include, among other things, that the defendants negligently approved loans (i) where one or more of the sources of repayment of the loan were not likely to be sufficient to fully retire the debt; (ii) that violated applicable laws and regulations and/or IndyMac's internal policies; (iii) where borrowers were or should have been known not to be creditworthy and/or to be in financial difficulty; (iv) with inadequate or inaccurate financial information regarding the creditworthiness of the borrower and/or guarantors; (v) with inadequate appraisals; (vi) that were renewals or extensions for borrowers who were not creditworthy or were known to be in financial difficulty but were made without any reduction in principal and without taking proper steps to obtain security or otherwise protect IndyMac's interests; (vii) continuing and even expanding HBD's homebuilder lending despite knowledge of deteriorating market conditions; (viii) despite IndyMac's having a high geographic concentration of loans in the same market; and (ix) where there was very little likelihood of the loan being repaid within the term of the loan. The FDIC estimated in the complaint that IndyMac's losses on HBD's portfolio exceeded $500 million.

B. Heritage Community Bank

On November 1, 2010, the FDIC, as receiver of Heritage Community Bank, Glenwood, Illinois ("Heritage"), filed suit in a federal district court in Illinois seeking to recover losses of at least $20 million allegedly suffered by Heritage, an institution that had approximately $230 million in assets, which was closed by Illinois banking regulators in February 2009. The complaint alleges that eleven of Heritage's former directors and officers engaged in negligence, gross negligence and breach of fiduciary duty by, among other things, failing to properly manage and supervise Heritage's commercial real estate ("CRE") lending program. The eleven defendants include former members of Heritage's board of directors, including five outside directors ("Heritage Defendants"), and former officers.

The complaint alleges that the Heritage Defendants failed to protect Heritage from the substantial inherent risks of large-scale CRE lending. The complaint also alleges deficiencies in Heritage's CRE lending program, including deficient loan underwriting and monitoring. The complaint claims, among other things, that Heritage routinely financed CRE projects without any meaningful analysis of their economic viability and often with inadequate appraisals, repeatedly made loans with excessive "loan-to-value" ratios and failed properly to evaluate the creditworthiness of CRE borrowers and guarantors to ensure they could reliably repay their loans.

The FDIC alleges that the Heritage Defendants tried to mask Heritage's mounting problems by making new CRE loans and renewing and making additional loan advances on existing troubled loans, allegedly often replenishing "interest reserves," which the FDIC alleges allowed borrowers to pay interest with more borrowed funds. The FDIC alleges that the director defendants breached their fiduciary duties by approving dividends and incentive awards to senior management at a time when they should have increased loan loss reserves and the bank's capital.

The action against the Heritage Defendants demonstrates the continuing application of the Policy Statement with its focus on director liability being based in part on the failure of the defendants to heed regulatory criticism warning them to control the bank's CRE lending and set appropriate limits to avoid over-concentration in that area. The action also shows a willingness by the FDIC to seek to recover losses from directors and officers of even relatively small community banks in order to recoup what may be considered by some to be relatively small losses.

The FDIC's action in Heritage is particularly noteworthy because it shows a willingness by the FDIC to bring an action to recover losses against directors and officers of failed institutions, including outside directors, for simple negligence. During the S&L Crisis in the 1980s, which resulted in the last widespread collapse of banking institutions and a wave of FDIC litigation, the FDIC reportedly applied a threshold review standard of "gross negligence" in determining whether to pursue director liability claims. In this case, the FDIC's suit alleges simple negligence and breach of fiduciary duty by the six outside director defendants. Federal law sets a "gross negligence" standard of liability as a floor for actions brought by the FDIC to recover losses against directors and officers of failed institutions, which applies as a substitute for state standards that require greater culpability.

In a prior action brought in federal court in California, the FDIC brought suit against directors of a national bank to recover losses sustained by the failed bank under a theory of simple negligence. FDIC v. Cassetter, 184 F.3d 1040 (9th Cir. 1999). Under the circumstances of that case, the Ninth Circuit Court of Appeals held that the directors had acted in good faith and with the belief that their actions were in the best interests of the bank and that as a result, the California business judgment rule insulated the directors from liability. Thus, in appropriate circumstances, the business judgment rule may shield directors and officers of failed institutions from suits brought by the FDIC based upon a theory of simple negligence or breach of fiduciary duty.

C. 1st Centennial Bank

The FDIC, as receiver for 1st Centennial Bank of Redlands, California ("Centennial"), filed a suit on January 14, 2011 in a federal district court in California against 14 of the former directors and officers of Centennial ("Centennial Defendants"). In the complaint, the FDIC alleges that the Centennial Defendants engaged in breaches of fiduciary duty, negligence, gross negligence, recklessness and willful misconduct by "utterly fail[ing] to manage [Centennial] and its commercial real estate lending division in a prudent, safe and reasonable manner." Specifically, the FDIC alleges that the Centennial Defendants implemented an unsustainable business model that involved heavy concentrations in high-risk commercial real estate lending without having adequate policies and practices in place to manage the risk, despite at least one warning by the FDIC regarding the bank's risk profile. Further, the FDIC alleges that the Centennial Defendants failed to follow the policies that did exist by, among other things, lending heavily to friends and repeat customers without analyzing the risks of the projects and the creditworthiness of the borrowers. The FDIC also alleges that the Centennial Defendants failed to staff the bank with an adequate number of competent and non-conflicted managers, particularly with respect to the bank's construction lending operations.

D. Integrity Bank

On January 14, 2011, the FDIC filed a suit as receiver for Integrity Bank of Alpharetta, Georgia ("Integrity") in a Georgia federal district court against eight of the bank's former directors and officers ("Integrity Defendants"). In the suit, the FDIC seeks to recover over $70 million in losses that Integrity suffered on 21 commercial and residential loans. The suit alleges that the Integrity Defendants breached their fiduciary duties and/or other legal duties and committed numerous acts of negligence and gross negligence.

The Integrity Defendants were members of Integrity's Director Loan Committee ("DLC"). The FDIC alleges that, in connection with their service to the DLC, the Integrity Defendants caused Integrity to pursue an unsustainable, aggressive and overly risky growth strategy in an attempt to exploit the commercial and residential real estate "bubble" between February 2005 and May 2007. The FDIC alleges that Integrity focused on higher risk, speculative lending in the Atlanta area as well as in South Carolina and Georgia, including a high concentration of loans to certain "preferred" borrowers, in contravention of Integrity's policies and Georgia statutory limits. The FDIC further alleges that the policies that were in place with respect to Integrity's lending practices were "void of the most basic prudent lending controls." The FDIC claims that the Integrity Defendants ignored repeated warnings from state and federal regulators regarding Integrity's increasing risk profile and made no effort to reduce the bank's risks or to change the bank's controls, allegedly betting that real estate demand in Integrity's chosen markets would continue indefinitely.

The district court recently sided with the Integrity Defendants. The FDIC had made claims of both gross negligence and simple negligence. The court held that the business judgment rule protected Integrity Defendants under Georgia corporate law against claims "amounting to mere negligence, carelessness, or 'lackadaisical performance.'" That is, the FDIC was only entitled to bring claims for gross negligence.

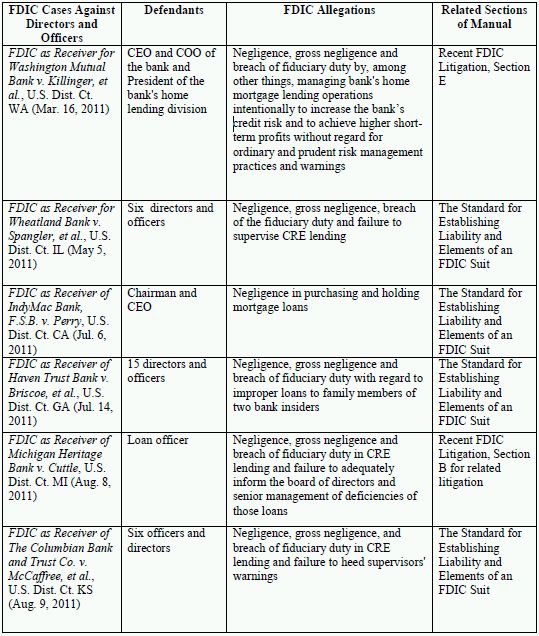

E. Washington Mutual Bank

Washington Mutual Bank ("WaMu"), a federal savings institution, is the largest insured depository institution ever to be placed in receivership. On March 16, 2011, nearly two and a half years after WaMu was placed in receivership, the FDIC as receiver brought suit in a Washington federal district court against three former senior officers, alleging that they engaged in negligence, gross negligence and breach of fiduciary duty by, among other things, managing WaMu's home mortgage lending operations from 2004 until shortly before the savings institution was closed intentionally to increase its credit risk and to achieve higher short-term profits without regard for ordinary and prudent risk management practices or the warnings of WaMu's credit risk and enterprise risk management professionals.

The complaint alleges that the savings institution's Chief Executive Officer, its Chief Operating Officer, and the President of the home lending division developed and executed a five-year plan to adopt a higher risk lending strategy. This involved, among other things, the objective of tripling the bank's subprime market share. The complaint describes instances in which this strategy either led to or encouraged the layering of multiple risks, such as by extending adjustable rate, non-amortizing, high loan-to-value loans without documentation of the borrower's ability to repay and without adequate means to detect fraud. The complaint also alleges that the executives disregarded warnings, and should have known based on their own positions and experience, thatWaMu lacked the infrastructure and training to execute this strategy with proper consideration of the risks involved, and that they proceeded notwithstanding the growing concentration of credit risk and geographic risk, the slowdown in relevant housing markets and the savings institution's rapidly deteriorating asset quality.

The complaint also alleges that certain asset transfers by the Chief Executive Officer and his wife and by the Chief Operating Officer and his wife in the months preceding WaMu's failure were fraudulent transfers. Based on these allegations, the FDIC, among other things, sought to freeze these individuals' assets, as provided under the FDI Act, and to require them to provide advance notice to the FDIC of any intended future transfers of assets in the amount of $10,000 or more in a single transaction.

This suit was settled in December 2011. The FDIC announced that it received $64.7 million in the form of cash payments and defendants' bankruptcy claims against the bank holding company. The FDIC received (1) cash payments from the defendants, (2) payment from the defendants' D&O insurance policies, and (3) the defendants' claims against WaMu's holding company in its bankruptcy proceedings.

F. Silverton Bank

On August 22, 2011, the FDIC filed a suit as receiver for Silverton Bank, N.A. of Atlanta, Georgia ("Silverton") in a Georgia federal district court against 15 former directors and two former officers ("Silverton Defendants"). In the suit, the FDIC seeks to recover over $70 million from the Silverton Defendants. The suit alleges that various Silverton Defendants engaged in negligence, gross negligence, breached their fiduciary duties and engaged in corporate waste.

Silverton was originally established in 1986 as a "bankers bank," which was intended to provide services to community financial institutions. In 2007, the bank converted to a national bank. Coinciding with its conversion to a national bank, Silverton grew rapidly from $2 billion in assets on December 31, 2006 to $4.2 billion in assets by March 31, 2009. The FDIC alleges that this growth involved aggressive out-of area acquisition development and construction lending and a high level of commercial real estate lending. The FDIC alleges that the bank had serious weaknesses in its underwriting and credit administration and disregarded the impact of the decline in the economy.

All but one of the directors sued by the FDIC were executives at community financial institutions that did business with Silverton. The FDIC's complaint argues that Silverton is "a text book case of officers and directors of financial institution being asleep at the wheel and robotically voting for approval of transactions without exercising any business judgment in doing so." The FDIC contends that board members as bank executives had specialized knowledge and expertise and should have fully understood the manner in which they were required to discharge the duties owed to the bank.

The FDIC also alleges that the Silverton Defendants allowed the bank to engage in extravagant spending that constituted corporate waste. The FDIC cited the bank's purchase of two new aircraft, a new airplane hangar and what it described as a lavish new office building as well as the employment of as many as eight private pilots and the holding of expensive meetings of the board of directors and meetings with correspondent banking customers.

The FDIC also raises D&O insurance issues in its complaint. The FDIC alleges that the D&O insurance policy binder included a regulatory exclusion, but that this exclusion was not included in the policy actually delivered and that as a result there is no regulatory exclusion in effect under the policy. The FDIC further argues that the insured-versus-insured exclusion provision did not preclude coverage under the policy. It asserts that the exclusion was intended to protect the insurance company against collusive lawsuits between insureds, which it argues is not an issue in this case. Moreover, the FDIC argues that the receiver did not simply step into the shoes of the bank, since under the FDI Act the receiver also succeeds to all claims of "any stockholder, member, accountholder, depositor, officer, or director" of the bank. Thus, according to the FDIC, its actions are brought not just on behalf of the bank but also pursuant to the authority described in the preceding sentence. The FDIC seeks a declaratory judgment that the regulatory exclusion and the insured-versus-insured exclusion do not apply to claims by the FDIC.

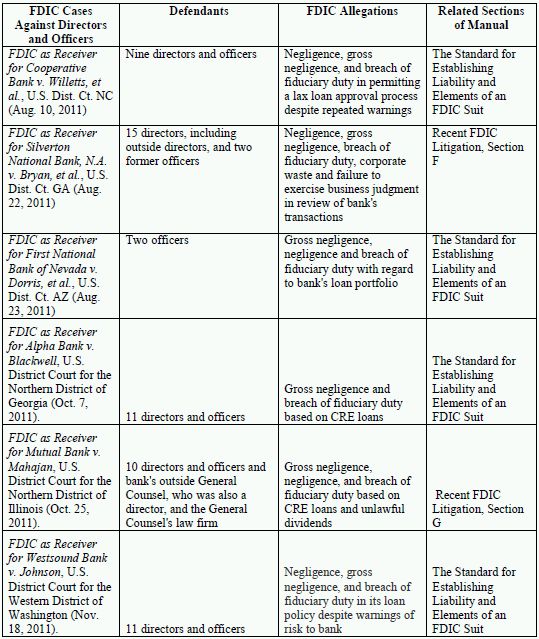

G. Mutual Bank

On October 25, 2011, the FDIC filed a suit as receiver for Mutual Bank of Harvey, Illinois in an Illinois federal district court against ten of the bank's former directors and officers ("Mutual Defendants"). In the suit, the FDIC seeks to recover $115 million lost on 12 CRE and acquisition, development and construction ("ADC") loans and $11.6 million in unlawful dividend payments and wasted corporate assets.

The FDIC alleges that eight directors on the Directors' Loan Committee and two officers (the Chief Credit Officer and a loan officer) were negligent, grossly negligent, and breached their fiduciary duties by recklessly pursuing asset growth with risky CRE, ADC, and out-of-area loans to a small group of high-volume borrowers, ignored the bank's loan policies and underwriting and loan standards, and disregarded warnings from regulators about the bank's lending. The FDIC further alleges that the director defendants approved $10.5 million in dividends that violated Illinois law. The FDIC asserts that the director defendants permitted the waste of corporate assets by permitting payments for (1) the wedding of the son of the Chairman of the Board of Directors, (2) criminal defense costs of Mutual Bank's President's wife who had been indicted for Medicaid fraud, (3) a board of directors meeting in Monte Carlo, and (5) excessive payments to friends and relatives of Director Defendants for renovations to Mutual Bank offices..

The FDIC also brought suit against an individual who served on Mutual Bank's board of directors who also acted as the Bank's general counsel as well as his law firm. The FDIC alleged that the attorney and the firm's failed to protect the Bank's interests in connection with a range of loan transactions and in regard to unlawful payment of dividends.

H. R-G Premier Bank of Puerto Rico

On January 18, 2012, the FDIC filed a suit as receiver for R-G Premier Bank of Puerto Rico in a federal district court in Puerto Rico against 19 of the bank's former directors and officers ("R-G Defendants"), 17 of their spouses, and the bank's D&O liability insurer. The FDIC sought damages in excess of $257 million in connection with 77 transactions, claiming that RG Defendants were grossly negligent, failed to inform themselves about the bank's lending, failed to exercise oversight over the bank's lending, and breached their fiduciary duties of care.

The FDIC alleges that the board in 2001 gave the Chief Lending Officer a mandate to increase commercial real estate lending, but failed to implement controls over his activities. In particular the FDIC noted that the Chief Lending Officer was given control over the Bank's Credit Risk Management Department. According to the FDIC, this hierarchy created a clear conflict of interest for bank personnel in the Credit Risk Management Department: on one hand, they were required to be prudent and moderate the bank's credit risk; on the other hand, their immediate supervisor badly wanted to grow the bank's loan portfolio. Exacerbating this problem in the view of the FDIC was the Board's failure to oversee lending and failure institute adequate loan reviews. The FDIC also alleges that the directors failed to heed numerous warnings from regulators regarding the concerns the Bank's CRE operations.

I. Broadway Bank

On March 7, 2012, the FDIC filed a suit as receiver for Broadway Bank of Chicago, Illinois in an Illinois federal district court against nine of the bank's former directors and officers ("Broadway Defendants"). The Broadway Defendants face claims of negligence, gross negligence, and breach of fiduciary duty of care for approving 17 CRE and ADC loans on which the FDIC seeks recovery of $104 million. The FDIC alleged that the Board of Directors and bank's Loan Committee pursued rapid growth by approving high-risk loans. In approving the loans, Broadway Defendants failed to conduct proper due diligence about the risk they posed to the bank, disregarded the bank's loan policies, failed to ensure safe and sound underwriting, failed to guarantee sufficient collateral for the loans, failed to prevent unsafe and unsound concentrations of credit, and failed to monitor the loans' performance.

Further, the FDIC alleged that Broadway Defendants ignored warnings from regulators regarding the asset quality problems the Bank was facing. In this regard the complaint alleges that the Broadway Defendants approved two of the worst loans immediately following a meeting with the bank's regulators on the same day in which Broadway Defendants were specifically warned that their CRE and ADC loans posed risks to the bank and in which they discussed entering into a Memorandum of Understanding with regulators that would restrict the bank from making such loans. After that meeting, Broadway Defendants approved three loans that allegedly caused $20 million in losses to the bank. At the time of Broadway Bank's failure, it had $1.06 billion in assets, and its failure cost the Deposit Insurance Fund $391 million.

CONCLUSION

It is essential that directors, officers and professionals recognize that in the event of the failure of an insured depository institution their conduct in regard to that institution is likely to be carefully scrutinized. Such parties should take steps to ensure that they have the information necessary to carry out their responsibilities and that the rationale for their actions is appropriately documented. As is often said, an ounce of prevention is worth a pound of cure. Developing a record showing that appropriate care and diligence were exercised, even if an institution fails, can be critical to reaching a favorable outcome in the event of an FDIC investigation.

Once an institution fails, potential defendants should recognize that they may be in for a long and often frustrating process. They should consult with experienced counsel to develop a strategy to best utilize the defensive resources available to them and to be in the best position to defend their conduct in regard to the failed institution either in the course of an FDIC investigation or in litigation brought by the FDIC.

APPENDIX A

FDIC-Authorized D&O Actions

After a bank is put in receivership, the FDIC Board of Directors generally has three years to bring tort claims against former officers and directors and six years to bring breach of contract claims. In some cases, state law may allow the FDIC a longer period to bring suit, or the FDIC may request the target of an investigation to enter into a tolling agreement to allow more time for an investigation to be completed. Suits commonly allege negligence, gross negligence and breach of fiduciary duty. According to the FDIC, as of April 25, 2012, the FDIC Board of Directors had authorized suits in connection with 58 failed institutions against 493 individuals for D&O liability with damage claims over $8 billion. The running total of those claims is described below, including additional claims identified by the FDIC during each month of 2012.

APPENDIX B

Recent FDIC Suits against Bank D&Os

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.