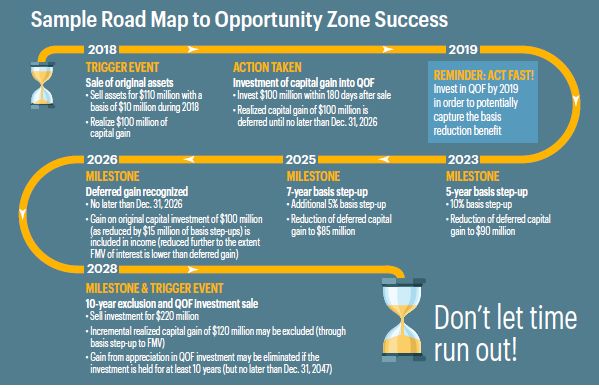

Of the many changes that came from the Tax Cuts and Jobs Act ("The TCJA"), Qualified Opportunity Zones ("QOZ") have been one of the most talked about provisions as the 2018 tax season progresses. As a recap, through QOZs, taxpayers may elect to temporarily defer the tax to be paid on capital gains until the 2026 tax year that are invested in a Qualified Opportunity Fund ("QOF") within 180 days of gain recognition, the QOF must invest 90 percent of its capital in QOZ Property. Taxpayers who hold investments in a QOF for at least five years may exclude 10 percent of the original deferred gain, and investments held for more than seven years qualify for an additional five percent exclusion of their original deferred gain. In what could be the most attractive feature of the new law, after 10 years, post-acquisition appreciation is 100 percent excluded from taxable income for federal tax purposes. Many states are still evaluating how they are going to deal with the new QOZ rules.

On Thursday, February 14, the IRS held a public hearing addressing QOZ and sought input related to the proposed regulations released in October of 2018. While many who attended the hearing spoke positively on the planning opportunities that now exist through use of QOZs, there were some common points that were brought up:

- The Treasury's proposed regulations specified that a QOZ business must be at least 70 percent within a QOZ to qualify, but these rules also stated that at least 50 percent of gross income receipts must be from business within a QOZ. Many concerns were raised about businesses that conduct their business primarily through e-commerce or manufacturing and whether or not they would be able to easily meet those standards. Many believe that this is poor wording within the legislation. In the case of the manufacturer, where the business activity is conducted, and in turn where the benefit to the capital infusion is felt, would be located in the QOZ and the taxpayer should qualify.

- Concerns were raised about the ability of investors to invest QOF in other types of businesses beyond real estate. There have been certain industry verticals, such as the cannabis and gaming industries, which some groups would like to have disallowed as eligible businesses.

- Attendees also requested that the IRS provide rules for detailed and comprehensive reporting, so that funds and investors can make informed decisions relating to their investments and so there is a mechanism for tracking the effectiveness of the program as a whole.

- Suggestions were made encouraging the flexibility of QOFs, pushing the IRS to allow QOF to reinvest gains within a reasonable time period into other QOZ businesses without triggering a taxable event.

- Questions arose as to whether a refinancing during the 10-year window, followed by a distribution of the proceeds from the refinancing to investors, would be in violation of the 10-year holding period. Determination of this key fact would significantly sway the decision as to what is the most beneficial entity choice for QOFs.

- Attendees called for the IRS to include vacant land or property not otherwise in service to qualify as "original use property" so that such plots can be rejuvenated in QOZ areas. This would definitely serve as a catalyst to stimulate the construction industry in the more rural geographically located Opportunity Zones.

- The IRS was asked to clarify how the QOZ program and its tax benefits will work with currently existing tax benefits, such as the New Market Tax Credit and the Low Income Housing Tax Credit. We have also seen a movement whereby state and local governments have attempted to parallel tax benefits at the local jurisdictional level. Some local governments have real estate tax and sales tax incentives that are applicable to various parcels located in an Opportunity Zone.

While the IRS did not comment on any of the points that were brought up during the hearing, they will continue to review the comments and suggestions provided and intend to release a second round of Proposed Regulations shortly, perhaps as quickly as later this month. An additional hearing is also planned to address any proposed changes in the program. Most commentators are projecting the possibility that the first set of final regulations will be released in late Spring. We will follow the releases from the Treasury and provide follow up in our next article to address the legislation's progress.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.