- within Antitrust/Competition Law and Intellectual Property topic(s)

- with readers working within the Retail & Leisure industries

Amid economic uncertainty, 23 European companies have emerged as some of the fastest-growing firms in the world. In our recent study of the top 50 fastest-growing companies across North America and Europe, measured by revenue growth from 2021 to 2023, European companies represent nearly half of these high-growth firms. Despite economic headwinds and structural constraints, these companies have demonstrated remarkable resilience and innovation, harnessing unique regional dynamics to thrive.

While North America continues to dominate the technology landscape, with all top 10 fastest-growing tech firms based in the U.S., Europe's supergrowers excel across a broader spectrum of industries. Europe's growth leaders span Consumer, Retail, Industrials, and Media & Telecommunications, proving that rapid disruption can fuel diverse success stories. This contrast highlights Europe's strength in a wide range of sectors, even as technology remains a key battleground.

The European Growth Landscape: Challenges and Opportunities in Key Sectors

European companies operate within unique macroeconomic and regulatory frameworks that present both opportunities and obstacles. Factors like regulatory complexity, specific labor market constraints, and a challenging funding environment can sometimes slow growth, particularly in certain sectors, and have contributed to Europe's lag in leading global tech expansion. However, these very challenges have also driven resilient and innovative growth strategies in other industries.

In sectors such as Consumer, Retail, Industrials, and Media & Telecommunications, Europe's supergrowers capitalize on strong fundamentals, diversified innovation approaches, and adaptable business models to overcome these barriers. Here, we examine what sets them apart and how they navigate challenges to achieve growth in competitive global markets.

| Industry | Industry Rank | Company Name | Headquarters | 2-Year CAGR % Last Twelve Months (LTM)* | Revenue - LTM* (USD Millions) | Company overview; year founded |

| Consumer | 1 | Sadot Group Inc. | US | 738% | 727 | Agricultural products; 1995 |

| Consumer | 2 | Karelia Tobacco Company Inc. | Greece | 142% | 1,353 | Tobacco Products; 1888 |

| Consumer | 3 | Celsius Holdings, Inc. | US | 105% | 1,318 | Soft Drinks and Non-alcoholic Beverages; 2004 |

| Consumer | 4 | On

Holding AG |

Switzerland | 57% | 2,128 | Footwear Products; 2010 |

| Consumer | 5 | e.l.f. Beauty, Inc. |

US | 53% | 890 | Personal Care Products; 2004 |

| Consumer | 6 | Samsonite

International S.A. |

Luxembourg | 35% | 3,682 | Travel luggage bags; 1910 |

| Consumer | 7 | Freshpet,

Inc. |

US | 34% | 767 | Natural fresh meals and treats for dogs and cats; 2006 |

| Consumer | 8 | Lamb

Weston Holdings, Inc. |

US | 29% | 6,551 | Producers and processors of frozen potato products; 1950 |

| Consumer | 9 | Victoria

PLC |

UK | 27% | 1,651 | Flooring Products; 1985 |

| Consumer | 10 | Ascend

Wellness Holdings, Inc. |

US | 25% | 519 | Multistate cannabis operator; 2018 |

| Industrials | 1 | Symbotic

Inc. |

US | 60% | 1,500 | Automated warehouse systems using AI; 2007 |

| Industrials | 2 | HMS Bergbau

AG |

Germany | 42% | 1,454 | Fiber optic products & services for telcos; 1993 |

| Industrials | 3 | FTAI

Aviation Ltd. |

US | 33% | 1,305 | Construction and infrastructure; 1946 |

| Industrials | 4 | Hexatronic Group AB (publ) |

Sweden | 55% | 770 | Smart grids, energy storage, EV charging equipment; 1937 |

| Industrials | 5 | AAON,

Inc. |

US | 22% | 889 | Trading and logistics for coal products and other ores; 1995 |

| Industrials | 6 | Mota-Engil, SGPS, S.A. |

Portugal | 55% | 5,552 | Aircraft and engine leasing, engine repair; 2011 |

| Industrials | 7 | Alfen

N.V. |

Netherlands | 50% | 546 | Transformers for electrical equipment systems; 1917 |

| Industrials | 8 | Trinity

Industries, Inc. |

US | 12% | 2,023 | HVAC engineering and manufacturing; 1988 |

| Industrials | 9 | Hammond Power Solutions Inc. |

Canada | 30% | 552 | Air treatment and climate solutions; 1955 |

| Industrials | 10 | Munters

Group AB (publ) |

Sweden | 17% | 927 | Railroad transportation products and services; 1933 |

| Media & Telco | 1 | fuboTV |

US | 46% | 1,368 | Live TV streaming platform focused on sports; 2015 |

| Media & Telco | 2 | Team

Internet Group |

UK | 43% | 837 | Online advertising and domain name service provider; 2000 |

| Media & Telco | 3 | The

Trade Desk |

US | 28% | 1,946 | Demand side ad platform; 2009 |

| Media & Telco | 4 | Helios

Towers |

UK | 27% | 721 | Telecommunications tower provider; 2009 |

| Media & Telco | 5 | Believe

S.A. |

France | 24% | 973 | Digital music company; 2005 |

| Media & Telco | 6 | Auto

Trader Group |

UK | 21% | 648 | Automotive online marketplace; 1975 |

| Media & Telco | 7 | Roblox

Corporation |

US | 21% | 2,799 | Video game developer; 2004 |

| Media & Telco | 8 | Entravision

Communications Corp |

US | 21% | 1,107 | Diversified global media, marketing, and technology company; 1996 |

| Media & Telco | 9 | Viaplay

Group AB |

Sweden | 20% | 1,757 | Media and entertainment company; 2018 |

| Media & Telco | 10 | Spotify

Technology S.A. |

Sweden | 17% | 14,642 | Digital music service; 2006 |

| Retail | 2 | Avolta

AG |

Switzerland | 81% | 15,188 | Duty-free & convenience stores; 1865 |

| Retail | 1 | PDD

Holdings Inc. |

Ireland | 62% | 34,924 | Parent of Temu & Pinduoduo, recently moved to Ireland; 2015 |

| Retail | 8 | WH Smith

PLC |

UK | 42% | 2,272 | Travel stores (e.g., newspapers, magazines, gifts); 1792 |

| Retail | 5 | The

Chefs' Warehouse (US) |

US | 40% | 3,434 | Specialty food distributor; 1985 |

| Retail | 6 | Dino Polska

S.A. |

Poland | 39% | 6,528 | Supermarket operator in Poland; 1999 |

| Retail | 3 | Redcare Pharmacy NV |

Netherlands | 30% | 1,988 | Online pharmacy; 2001 |

| Retail | 9 | AMCON

Distributing Company |

US | 26% | 2,047 | CP distributor to retail stores & health food store operator; 1981 |

| Retail | 10 | Kitwave

Group plc |

UK | 26% | 730 | Food, alcohol, and grocery wholesaler; 1987 |

| Retail | 7 | Orsero S.p.A. |

Italy | 20% | 1,703 | Fruit & vegetable distributor; 1940 |

| Retail | 4 | Matas

A/S |

Denmark | 18% | 889 | Cosmetics & consumer health care products; 1949 |

| Technology | 1 | SentinelOne, Inc. |

US | 74% | 621.2 | AI-powered cybersecurity platform provider; 2013 |

| Technology | 2 | BILL Holdings,

Inc. |

US | 70% | 1,192 | Financial automation software for small and midsize businesses; 2006 |

| Technology | 3 | Clear

Secure, Inc. |

US | 55% | 614 | Biometric travel document verification systems; 2010 |

| Technology | 4 | Klaviyo,

Inc. |

US | 55% | 698.1 | Marketing automation platform provider; 2012 |

| Technology | 5 | Snowflake Inc. |

US | 52% | 2,807 | Cloud-based data storage and analytics service; 2012 |

| Technology | 6 | GitLab

Inc. |

US | 52% | 579.9 | DevOps software package provider; 2014 |

| Technology | 7 | NVIDIA

Corporation |

US | 51% | 60,922 | Provider of advanced chips, systems, and software for the AI; 1993 |

| Technology | 8 | Super

Micro Computer, Inc. |

US | 49% | 9,253 | High performance server and storage solutions provider; 1993 |

| Technology | 9 | Zscaler,

Inc. |

US | 49% | 1,896 | Security cloud platform provider; 2007 |

| Technology | 10 | Samsara |

US | 48% | 937.4 | Connected operations cloud platform; 2015 |

How have the supergrowers adapted?

In analyzing the key drivers of growth across multiple industries, we can explore how European supergrowers have leveraged the macro- and micro-trends to their advantage and outperform their competitors.

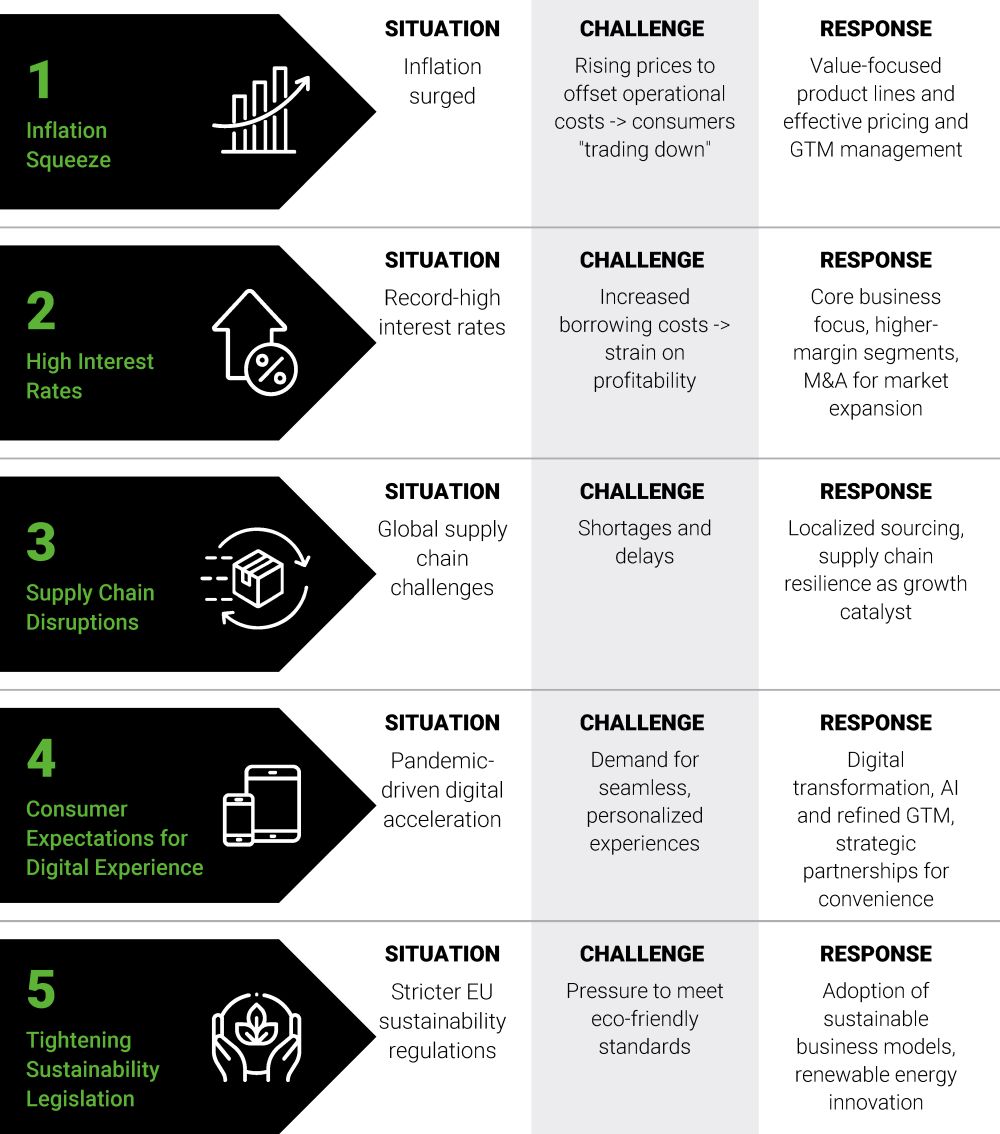

We note five common themes that encapsulate the economic and business environment faced in Europe in the last couple of years, reflecting significant challenges related to geopolitical tensions, energy crises, and shifting consumer behaviors. As illustrated by the examples below, these are influencing consumer spending patterns and reshaping corporate strategies in response:

1. The inflation squeeze: Addressing the "trading down" trend with value-focused and tiered pricing strategies and products

In the past couple of years, inflation has surged due to supply chain disruptions, labor shortages, and soaring energy costs linked to the Russia-Ukraine conflict. Companies raised prices to offset rising operational costs, further straining household budgets. As the cost-of-living crisis deepened, consumers increasingly turned to discount retailers and private-label products, fueling a "trading down" trend.

To address this shift, many companies introduced strategies such as a branded product and price tier ladder—offering "good, better, best" options to retain consumer demand and provide choice across different price points. Another critical approach was "design to value," where packaging sizes were reduced while prices remained steady, maintaining product appeal and profitability.

Especially in the consumer and retail sector, the supergrowers Kitwave Group and Dino Polska adapted by offering value-focused product lines with competitive pricing, successfully attracting budget-conscious consumers. This emphasis on affordability, while managing rising operational expenses, created a delicate balance between pricing and profitability. Effectively managing this balance became essential for navigating inflationary pressures, enabling both companies to remain competitive without eroding margins.

2. Interest rates at their highest since the Global Financial Crisis: Re-focusing the core business and doubling down on higher-margin segments

Record-high inflation prompted aggressive interest rate hikes by the European Central Bank and Bank of England, driving borrowing costs to levels unseen since the Global Financial Crisis. This forced businesses to reassess their resources allocations, shifting their focus towards core strengths and higher-margin segments to sustain profitability.

For example,Mota-Engil divested lower-margin assets to concentrate on high-return infrastructure projects. On Holding capitalized on growing demand for premium sportswear and footwear, appealing to health-conscious, high-spending consumers. M&A became a key strategy for reducing competition and solidifying positions in lucrative markets. For instance, Auto Trader Group acquired CarGurus' stake in Carwow, further expanding its presence in the premium car marketplace and enhancing margins. In focusing on these high-margin areas, these companies were able to maintain profitability despite the challenging economic conditions.

3. Supply chain disruptions: Effective management becomes a growth catalyst

The global supply chain was significantly disrupted by pandemic-related disruptions, geopolitical tensions, and other factors, impacting nearly every industry. Effective supply chain management became a critical differentiator between growth and stagnation.

Hexatronic maintained a steady flow of fiber-optic components to meet growing broadband infrastructure demand, while competitors struggled with shortages. Alfen localized its sourcing strategies for energy storage and EV charging solutions, reducing dependency on global suppliers and strengthening resilience. Similarly, Helios Towers secured infrastructure components and leveraged local resources to deliver projects faster than competitors. These supergrowers demonstrated how managing supply chains effectively turned disruptions into growth opportunities during disruptive periods.

4. Consumer expectations for a seamless experience and novelty: Growth through digital transformation and strategic partnerships

The pandemic significantly accelerated digital transformation, raising consumer expectations for seamless, personalized digital experiences to new heights. As e-commerce and online services became essential, supergrowers started to integrate advanced technologies like AI and enhance digital infrastructure to meet growing demands for convenience and customization. Digital transformation and strategic collaborations allowed companies to stay competitive by meeting evolving consumer needs for personalization and convenience.

Redcare Pharmacy upgraded its digital infrastructure to support increasing demand for online health products. Spotify Technology partnered with Google Cloud to improve AI-powered features like Discover Weekly, boosting user engagement and retention. WH Smith teamed up with InPost to offer flexible click-and-collect services, addressing consumer demand for convenient online shopping.

5. Tightening legislation for Sustainability and ESG: Rising to the top of the business agenda

Sustainability evolved from a "nice to have" to a core pillar of business strategy, supported by stricter European regulations, such as the EU Green Deal and Fit for 55, aiming to make Europe climate-neutral by 2050. Customers also demand eco-friendly options, further pressuring companies to accelerate their environmental commitments.

Munters and Orsero adopted sustainable business models, such as energy-efficient systems and sustainable agriculture, to meet demand for green solutions. Also, Alfen continued to innovate in renewable energy infrastructure, positioning itself as a key player in Europe's green energy transition. By aligning their business models with sustainability goals, these supergrowers ensure long-term competitiveness in an increasingly eco-conscious market.

In the upcoming second part of this series, we will double-click for industry-specific assessments of the European supergrowers to extract the key takeaways for success in driving optimistic market outlooks and enhanced resilience in a disrupted world.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.