- within International Law topic(s)

- in United States

1 Trade agreements

1.1 Which bilateral, regional and multilateral trade agreements have effect in your jurisdiction?

The United Kingdom was a founding party to the General Agreement on Tariffs and Trade 1947 and is one of the original members of the World Trade Organization, having joined on 1 January 1995.

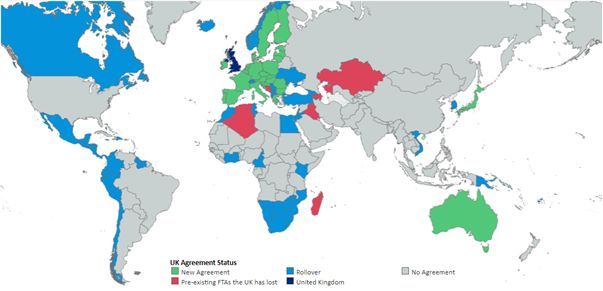

The United Kingdom is currently a signatory to 40 free trade agreements with 91 countries. It has sought to replicate the trading agreements that previously applied to it through its membership in the European Union to ensure continuity for UK business. Following Brexit, a Trade and Cooperation Agreement between the United Kingdom and the European Union is currently in place. The United Kingdom's most recent agreement is with Australia and will enter into force following both parties' completion of domestic procedures for ratification.

Figure 1 Overview of UK free trade agreements

Source: International Economics Consulting's Trade After Brexit Dashboards

1.2 Which authorities are responsible for the negotiation of trade agreements? What does this process typically involve and how long does it take?

The UK Department for International Trade (DIT) is responsible for conducting negotiations of trade deals/agreements.

A typical process for negotiating trade agreements involves the following steps:

- Identify new market opportunities of interest to British businesses and assess the scope of opening up to new partners by undertaking any commitments for further liberalisation.

- Agree on a mandate for free trade agreements (FTAs)/trade agreements, in which the DIT, among other things, seeks to define the scope and depth of negotiations.

- Prepare to negotiate the FTA, including an assessment of the potential benefits and costs of any potential trading arrangements that could emerge as negotiation outcomes.

- Negotiate the FTA once the details of a trade agreement are settled. The DIT has committed to briefing the relevant parliamentary committee throughout negotiations, and thus the FTA is open to parliamentary scrutiny and public consultation during the negotiation.

- Ratify the FTA. At the end of the negotiations, the full treaty text is placed before Parliament. A full impact assessment is also published. Trade agreements may require a combination of legislation and some statutory measures. If changes to primary legislation are necessary, the government will need to bring forward a bespoke bill for the FTA to provide an opportunity for Parliament to scrutinise all the legislative changes before the FTA is ratified.

- Implement the FTA. After ratification, trade agreements provide a legal framework for trade with new partners. However, deriving benefits from the new agreements is dependent on businesses acting to exploit the new commercial opportunities available.

Most of the trade deals that the United Kingdom has concluded since Brexit have been achieved relatively quickly (within around one year), as the parties agreed to rollover existing agreements with the European Union. Agreements with third countries, such as India and the United States, are expected to take significantly longer.

1.3 Do interim provisions apply while new trade agreements are under negotiation?

Depending on the circumstances, interim provisions can apply. For instance, such provisions were applied under the EU-UK Trade and Cooperation Agreement for the transmission of personal data from the European Union to the United Kingdom.

Interim provision and bridging mechanisms have also been applied in a number of FTAs, including:

- the Caribbean Forum-UK Economic Partnership Agreement;

- the UK-Ghana Interim Trade Partnership Agreement;

- the Agreement on Trade in Goods between Iceland, Norway and the United Kingdom;

- the UK-Moldova Strategic Partnership;

- the Trade and Cooperation Agreement;

- the UK-Pacific Economic Partnership Agreement; and

- the UK-Vietnam Free Trade Agreement.

2 Customs and imports

2.1 What laws and regulations govern customs in your jurisdiction?

The primary legislation governing the customs procedure that applies to goods imported into the United Kingdom is prescribed in:

- the Customs and Excise Management Act 1979;

- the Taxation (Cross Border Trade) Act 2018;

- the European Union (Withdrawal) Act 2018; and

- the Taxation (Post-transition Period) Act 2020.

Additionally, there are various statutory instruments (SIs) governing customs, value added tax and excise duties. Provisions on customs tariffs can be found in:

- SI 2020/1430 – The Customs Tariff (Establishment) (EU Exit) Regulations 2020;

- SI 2020/1431 – The Customs (Reliefs from a Liability to Import Duty and Miscellaneous Amendments) (EU Exit) Regulations 2020;

- SI 2020/1432 – The Customs (Tariff Quotas) (EU Exit) Regulations 2020;

- SI 2020/1433 – The Customs (Origin of Chargeable Goods) (EU Exit) Regulations 2020;

- SI 2020/1434 – The Customs (Tariff-free Access for Goods from British Overseas Territories) (EU Exit) Regulations 2020;

- SI 2020/1435 – The Customs Tariff (Suspension of Import Duty Rates) (EU Exit) Regulations 2020;

- SI 2020/1436 – The Customs (Origin of Chargeable Goods: Trade Preference Scheme) (EU Exit) Regulations 2020;

- SI 2020/1437 – The Customs (Import Duty Variation) (EU Exit) Regulations 2020;

- SI 2020/1438 – The Trade Preference Scheme (EU Exit) Regulations 2020;

- SI 2020/1457 – The Customs Tariff (Preferential Trade Arrangements) (EU Exit) Regulations 2020;

- SI 2020/1657 – The Customs Tariff (Preferential Trade Arrangements and Tariff Quotas) (Amendment) (EU Exit) Regulations 2020;

- SI 2021/63 – The Customs Tariff (Establishment and Suspension of Import Duty) (EU Exit) (Amendment) Regulations 2021;

- SI 2021/241 – The Customs Tariff (Preferential Trade Arrangements) (EU Exit) (Amendment) Regulations 2021;

- SI 2021/380 – The Customs (Tariff etc) (Amendment) Regulations 2021;

- SI 2021/382 – The Customs Tariff (Preferential Trade Arrangements and Tariff Quotas) (EU Exit) (Amendment) Regulations 2021;

- SI 2021/520 – The Customs Tariff (Establishment) (EU Exit) (Amendment) Regulations 2021;

- SI 2021/527 – The Customs Tariff (Preferential Trade Arrangements and Tariff Quotas) (EU Exit) (Amendment No 2) Regulations 2021;

- SI 2021/661 – The Customs Tariff (Establishment) (EU Exit) (Amendment) (No 2) Regulations 2021;

- SI 2021/693 – The Customs Tariff (Preferential Trade Arrangements and Tariff Quotas) (EU Exit) (Amendment) (No 3) Regulations 2021;

- SI 2021/870 – The Customs (Tariff etc) (Amendment) (No 2) Regulations 2021;

- SI 2021/871 – The Customs Tariff (Preferential Trade Arrangements) (EU Exit) (Amendment) (No 2) Regulations 2021;

- SI 2021/1191 – The Customs Tariff (Establishment and Suspension of Import Duty) (EU Exit) (Amendment) (No 2) Regulations 2021;

- SI 2021/1192 – The Customs Tariff (Preferential Trade Arrangements and Tariff Quotas) (EU Exit) (Amendment) (No 4) Regulations 2021;

- SI 2021/1489 – The Customs (Miscellaneous Provisions) (Amendment) (EU Exit) Regulations 2021;

- The Customs Tariff (Preferential Trade and Tariff Quotas) (EU Exit) (Amendment) Regulations 2022; and

- SI 2022/525 The Customs Tariff (Preferential Trade and Tariff Quotas) (Ukraine) (Amendment) Regulations 2022.

2.2 Which authority is responsible for enforcing the customs regulations? What powers does it have?

Her Majesty's Revenue and Customs (HMRC) enforces the UK customs laws and regulations, as set out in the UK Customs and Excise Management Act 1979 and its amendments.

HMRC is a non-ministerial department established by the Commissioners for Revenue and Customs Act (CRCA) 2005. HMRC is the United Kingdom's tax, payments and customs authority. Among other things, it is responsible for collecting taxes and customs duties, and facilitating legitimate international trade. HMRC is also a law enforcement agency. It undertakes criminal investigations relating to serious organised fiscal crime, including tobacco, alcohol and oil smuggling. Its investigation officers have wide-ranging powers of arrest, entry, search and detention, and recover criminal assets through the Proceeds of Crime Act 2002 (for more information, see "HMRC's criminal investigation powers and safeguards"). HMRC is also part of the mechanism which contributes to intelligence collection, analysis and assessment.

2.3 What is the authority's general approach to enforcing the customs regulations? How vigorously are the rules enforced?

The United Kingdom's general approach to customs management is reflected in the 2025 UK Border Strategy, which aims to:

- have the world's most effective border that creates prosperity and enhances security for a global United Kingdom; and

- protect the public and encourage legitimate trade and travel for businesses and passengers.

In order to deliver this objective, the UK government has developed a Target Operating Model that comprises, among other things:

- an enhanced Trusted Trader Programme which is recognised across border agencies;

- a Single Trade Window through which traders and their intermediaries can submit information just once to government; and

- application programming interfaces to build supply chain data pipelines direct to government. The emphasis on technology application at the border is expected not only to provide enforcement agencies with more information, but also to bring about more opportunities to perform processes away from the border, minimising delays at ports and making the border more resilient.

HMRC is in charge of applying the relevant customs laws and regulations, and does so vigorously.

2.4 What customs import tariffs and duties apply in your jurisdiction? How are they levied?

Following the expiry of the Brexit transition period, imports into the United Kingdom are governed by the UK Trade Tariff. Currently, the United Kingdom applies a simple average most-favoured nation tariff of 3.67%. Out of the 8,613 tariff lines, 4,462 receive duty-free treatment, with the remaining 4,151 applying a tariff rate of between 2% and 70%.

Customs duties are assessed on the fair market value of imported goods at the time of arrival in the United Kingdom. Import prices are generally calculated on the basis of cost, insurance, freight and duty. A standard value added tax (VAT) rate of 20% is levied on the aggregate value; while reduced VAT rates of 5% and 0% apply to some goods, such as children's car seats, home energy, food and children's clothing.

Customs duties and other charges that are due must be paid, deferred or secured before the goods are cleared by Customs. The deferred payment of customs duties and other charges is subject to the provision of adequate security and other conditions, following the guidance under Notice 101: Deferring Duty, VAT and Other Charges. Notice 101 also contains details of the Simplified Import VAT Accounting scheme which allows approved businesses to reduce the security requirement for deferred import VAT.

Customs duties and other duties are payable through the Flexible Accounting System, which is maintained by Customs Handling of Import and Export Freight. Goods will not be cleared from customs control unless the credit balance in the account is sufficient to cover all charges due.

2.5 What types of preferential tariffs are available in your jurisdiction? What are the criteria for eligibility?

The United Kingdom applies different preferential regimes to multiple countries and territories, depending on the existing arrangements. For those countries with which the United Kingdom has free trade agreements, the applicable preferential tariffs are specified in the relevant schedule of concessions. For other countries – particularly developing countries – the UK Generalised Scheme of Preferences (GSP) is applicable, which has been in place since 1 January 2021. The UK GSP largely replicates the EU GSP in terms of reducing and eliminating duty (tariffs) rates on imports from developing and least developed countries (LDCs). The UK GSP is provided under three schemes:

- the LDC Framework (similar to Everything but Arms);

- the Enhanced Framework (similar to GSP+); and

- the General Framework (equivalent to Standard GSP).

At present, around 67 developing nations are eligible for the UK GSP under the three frameworks.

The LDC Framework grants duty-free quota-free imports from eligible beneficiary countries for all goods other than arms and ammunition. Currently, 46 LDCs, as classified by the United Nations, enjoy trade preferences in the UK market under this scheme.

The General Framework provides duty concession for two-thirds of UK tariff lines. Currently, 12 countries that are low-income and lower-middle income countries, as classified by the World Bank, are eligible for the General Framework.

The Enhanced Framework provides duty suspension for two-thirds of UK tariff lines. To be eligible for the Enhanced Framework, low-income or lower-middle-income countries must satisfy two additional criteria:

- The eligible beneficiary country must be economically vulnerable due to a lack of export diversification and a low level of integration with the international trading system; and

- The economically vulnerable country must implement 27 international conventions related to human and labour rights, environment and good governance.

In any case, the application of preferential tariffs is subject to compliance with the rules of origin applicable in the United Kingdom (and contained in the respective trade agreements). The Customs Tariff (Preferential Trade Arrangements) (EU Exit) Regulations 2020 (SI 2020/1457) provide information on the preferential import duty rates and the related rules of origin requirements.

2.6 Are tariffs applied to safeguard national security?

The World Trade Organization (WTO), through Article XXI of the General Agreement on Tariffs and Trade, allows WTO members to deviate from their obligations and impose the necessary measures, including tariffs, to protect their national security. While the United Kingdom has the option to impose tariffs to safeguard national security, this option has not been used. The United Kingdom uses sanctions in certain cases to support foreign policy and national security objectives, as well as to maintain international peace and security, and prevent terrorism. Sanctions measures can include arms embargoes and other trade restrictions.

2.7 What import controls and restrictions apply in your jurisdiction? What exemptions are available?

The Import, Export and Customs Powers (Defence) Act 1939 (with its amendments and updates as applicable) is the main legislation covering the United Kingdom's approach to import controls and restrictions. The Open General Import Licence (OGIL) is the national trade control measure run by the Department for International Trade (DIT) that allows the import of all goods into the United Kingdom, subject to the relevant exceptions. Goods that are subject to import controls under OGIL include firearms, anti-personnel mines and certain nuclear and chemical goods.

The United Kingdom also uses sanctions in certain cases to support foreign policy and national security objectives, and to maintain international peace and security and prevent terrorism. Sanctions include arms embargoes, trade and transit controls, and restrictions on terrorist organisations. The Foreign, Commonwealth & Development Office is responsible for UK policy on sanctions. The DIT implements trade sanctions and has overall responsibility for trade sanctions licensing.

2.8 How are customs and import decisions challenged in your jurisdiction? What does this process typically involve and how long does it take?

Decisions made by HMRC on the application of customs duties are treated as indirect tax decisions for the purposes of appeal. Therefore, they are subject to a two-stage appeal process: first to the internal HMRC decision maker and then to an independent tribunal.

Before an adverse customs decision is issued, HMRC will issue a pre-notification letter explaining the reasons for that adverse decision. This pre-notification (the ‘right to be heard') will give concerned traders a period of 30 days to make further representations or provide further information to HMRC concerning the decision in question. At the conclusion of the right to be heard period, the officer will then issue a decision.

If a trader is dissatisfied with this decision, it can have recourse to two options. The first option is to request review by another officer, independent from the one who made the decision. A review must be requested in writing and should set out the reasons for disagreement with the original decision. A formal review of the decision will be conducted and the outcome will be notified in writing to the concerned trader. Alternatively, if the trader does not want a review or does not agree with the review conclusion, it can appeal to an independent tax tribunal under the Ministry of Justice.

There is a 30-day time limit from the date of written notification of a decision to submit either a formal review request or a tribunal appeal. Similarly, there is a 30-day limit from the date of the written review decision to submit an appeal to the tribunal. Once a review is requested, HMRC has 45 days to conduct its investigation and notify the outcome. This time limit may be extended by mutual agreement.

Decisions of the UK regulatory authorities on licensing and other import restrictions are also subject to appeal under the UK legal procedures applicable to the relevant licensing or regulatory regime. Import restrictions can be challenged before a WTO panel where WTO rules are violated.

2.9 What penalties are imposed for breach of the customs rules?

The penalties for breach of the customs rules are provided for under the Finance Act 2003 and further detailed in other regulations.

Sections 24 to 41 of the Finance Act 2003 provide for two types of civil penalty for breaching customs rules:

- the civil evasion penalty, which is dealt with separately in Notice 300: Customs Civil Investigation of Suspected Evasion; and

- the civil penalty for contraventions of customs rules relating to certain specified taxes and duties.

Generally, there are two types of customs civil penalty actions: warning letters and financial penalties. The maximum penalties provided in law are £2,500 per contravention for the more significant irregularities and £1,000 per contravention for others.

3 Exports

3.1 What export controls and restrictions apply in your jurisdiction? What exemptions are available?

Export controls and restrictions: Export controls and restrictions are undertaken depending on the nature and destinations of the proposed exports. For example, the United Kingdom imposes trade controls on trafficking and brokering of military goods from one overseas country to another. Goods subject to trade controls are specified in Category A, Category B and Category C of Schedule 1 to the Export Control Order 2008, as amended. Article 20 of the Export Control Order 2008, as amended, sets out the specific trade controls applicable to embargoed destinations. The export of strategic goods and technology is the specific remit of the Export Control Joint Unit (ECJU). Exports are controlled for various reasons, including:

- concerns about internal repression, regional instability or other human rights violations;

- concerns about the development of weapons of mass destruction;

- foreign policy and international treaty commitments, including as a result of the imposition of EU or UN trade sanctions or arms embargoes; and

- national and collective security of the United Kingdom and its allies.

Export controls and restrictions are applicable to a wide range of goods, including:

- military items;

- dual-use items (items with both civil and military uses);

- firearms; and

- goods subject to trade sanctions.

Export controls also apply:

- to goods, software and technology appearing on control lists;

- when there are concerns about end use or end users; and

- when destinations are subject to sanctions or other restrictions.

For more information, see "Export controls applying to academic research". Specific controls are applicable to nuclear material as listed in the Schedule referred to in Article 2 of the UK Export of Radioactive Sources (Control) Order 2006.

Export control exemptions: Controls on technology aim to prevent essential information from becoming available to proliferators and procurers of either weapons of mass destruction (WMD) or conventional weapons or goods that may cause national security concerns. There are several exemptions in export controls, including:

- technology that is already in the public domain;

- basic scientific research;

- technology required for the installation, operation, maintenance or repair of non-military controlled items, whose export has been previously authorised; and

- the minimum information required for patent applications.

More information can be found at "Guidance Exporting military or dual-use technology: definitions and scope".

3.2 Which authority is responsible for enforcing the export controls? What powers does it have?

The ECJU administers the United Kingdom's system of export controls and licensing for military and dual-use items. The Department for International Trade (DIT) has overall responsibility for the statutory and regulatory framework of export controls, and for decisions to grant or refuse an export licence.

3.3 What is the authority's general approach to enforcing the export controls? How vigorously are the rules enforced?

The Export Control Act 2002 and the Export Control Order 2008 provide the legal framework for the United Kingdom's export controls. The ECJU, under the DIT, administers the government's system of export controls. and brings together policy and operational expertise from the DIT, the Foreign, Commonwealth and Development Office (FCDO) and the Ministry of Defence (MOD).

The principal advisory departments are the FCDO and the MOD, which provide the DIT with advice and analysis on foreign policy, defence and development matters relevant to licensing, in line with the Consolidated EU and National Arms Export Licensing Criteria.

The MOD considers the military, operational, technical and security aspects of proposals to release classified material or export-controlled goods to foreign end users. It also operates a procedure – the MOD Form 680 (F680) approval process – that enables the government to control the release of classified equipment or information to foreign entities without compromising the United Kingdom's national security.

Her Majesty's Revenue and Customs (HMRC) is responsible for enforcing export and trade controls, as well as sanctions and embargoes. HMRC works with Border Force to prevent, detect and investigate breaches. The Central Fraud Group in the Crown Prosecution Service leads on any subsequent prosecutions.

3.4 How are export decisions challenged in your jurisdiction? What does this process typically involve and how long does it take?

Challenging export decision involves a two-stage appeal process:

- an appeal to the internal HMRC decision maker; and

- an appeal to an independent tribunal.

In the first stage, if a trader does not agree with the HMRC's decision, it can write to the HRMC to appeal within 30 days of the decision. This can be done by the trader or its accountant or other advisers.

If the trader is not satisfied with the outcome of the discussions with HMRC, it can have its case:

- reviewed by a different officer from the one who made the decision; or

- heard by an independent tax tribunal.

If the trader chooses to have the case reviewed, it will still be able to appeal to the tribunal (stage 2) if it disagrees with the outcome of that review.

To appeal to a tax tribunal, traders must write to the Tribunals Service within 30 days of the decision letter. The guidance for the process can be found at HM Revenue and Customs decisions - what to do if you disagree, and the forms used in the tribunal can be found at Tax (First-tier Tribunal) forms.

3.5 What penalties are imposed for breach of export controls?

The Customs and Excise Management Act 1954 (CEMA) sets out the penalties for non-compliance with export regulations when exporting from the United Kingdom. Non-compliance is subject to enforcement actions ranging from withdrawal of licences and audit requirements to civil monetary penalties and criminal prosecution. To facilitate audits and enforcement, the UK Export Control Order 2008 imposes specific record-keeping obligations.

Offences in relation to the export of prohibited or restricted goods are subject to up to seven years' imprisonment and unlimited fines, although most cases involve much less severe penalties (Section 68 of CEMA).

HMRC and the Crown Prosecution Service are responsible for enforcing these penalties. HMRC has discretionary power to issue monetary penalties alongside prosecutorial enforcement, which can result in the imposition of criminal fines or imprisonment. HMRC may decide to issue a compound penalty depending on:

- the seriousness of the offence; and

- whether the exporter:

-

- has taken remedial actions to correct compliance issues; and

- has voluntarily made a full and comprehensive disclosure of violations.

4 Trade remedies

4.1 What laws and regulations govern trade remedies in your jurisdiction?

The UK Trade Act 2021 sets out the role of the Trade Remedies Authority (TRA) as the public body responsible for conducting investigations, consulting interested parties and making recommendations to the government on UK trade remedy measures.

The UK Taxation (Cross-border Trade) Act (TCTBA) 2018 internalised the World Trade Organization framework into UK law. Schedules 4 and 5 of the TCTBA set out the procedure for trade remedy investigation and the criteria for the relevant offending measures.

Secondary legislation include:

- the Trade Remedies (Dumping and Subsidisation) (EU Exit) Regulations 2019 (SI 2019/450);

- the Trade Remedies (Increase in Imports Causing Serious Injury to UK Producers) (EU Exit) Regulations 2019 (SI 2019/449); and

- the Trade Remedies (Reconsideration and Appeals) (EU Exit) Regulations 2019 (SI 2019/910).

4.2 Which authority is responsible for enforcing the trade remedy regulations? What powers does it have?

The United Kingdom established the Trade Remedies Authority on 1 June 2021 under the Trade Act 2021. The TRA is responsible for:

- conducting trade remedies investigations and reviews; and

- making recommendations to the secretary of state for international trade regarding the imposition, variation or revocation of trade remedy measures.

Some changes have been made to the way in which the TRA assesses trade remedy measures since the United Kingdom left the European Union. New ‘call-in' powers have been adopted by the government, allowing the secretary of state for international trade to ‘call in' transition reviews that the TRA is conducting into transitioned legislation. This affords the secretary of state more leeway in determining how the review should be conducted. This authority applies only to reviewing what the TRA is currently doing, as well as any reconsiderations that the TRA may be conducting following its transitional measures evaluations. Not all transition reviews will be referred to as such.

4.3 What is the authority's general approach to enforcing the trade remedy regulations? How vigorously are the rules enforced?

Following Brexit, the United Kingdom has been actively implementing its new independent trade remedies regime. In addition to the new investigations of dumping, subsidies and safeguards, and recommendations on measures imposed to protect the interests of domestic industries, the TRA is tasked with reviewing the existing EU trade remedy measures (‘transition reviews'). In adopting trade remedy measures, the TRA will consider whether such measures meet the economic interest test.

The Taxation (Cross-border Trade) Act 2018 sets out the approach to enforcing the trade remedy regulations. It provides that the secretary of state for international trade has the power to:

- impose, suspend, vary or revoke trade remedy measures; and

- make associated regulations.

In terms of the process for the imposition of trade remedies, the process is as follows:

- UK businesses or the secretary of state for international trade may request that the TRA initiate a trade remedies investigation.

- If the relevant criteria to initiate an investigation are met, the TRA will:

-

- conduct its investigation;

- determine whether the legal conditions for the application of remedies are met; and

- calculate the duty that may be imposed

- If the legal conditions are met, and unless it finds that the remedy would not be in the economic interest of the United Kingdom, the TRA must then make a recommendation to the secretary of state for international trade on the application of remedies and the applicable level of duties.

- The secretary of state for international trade can then decide whether to impose remedies; but if the secretary of state is satisfied that it would be against the United Kingdom's public interest, he can reject the TRA's recommendation.

4.4 How is a trade remedy action initiated in your jurisdiction and on what grounds? Can the authority initiate an action ex officio?

The TRA may carry out three types of investigation:

- investigation of applications for new UK trade remedies to be applied;

- transition reviews for existing EU measures to be carried across to the United Kingdom or terminated; and

- reviews of other existing measures.

Dumping investigations are carried out on imported goods at export prices less than the normal value in the exporter's country, causing material injury to the UK industry. Subsidy investigations assess whether subsidised imports are causing material injury to a domestic industry. These two types of investigations normally run for between 11 and 13 months, depending on the investigation. Safeguard investigations assess whether an unforeseen surge of imports is causing or threatening serious injury to UK producers. Safeguard investigations normally run for between eight and 10 months, depending on the investigation.

The TRA may initiate an investigation upon receiving an application from UK industry representatives. The application must meet all of the following requirements:

- The applicant must be a UK business;

- The applicant's market share must be generally at least 1% UK market, based on UK sales by volume or by value;

- The application must be supported by producers holding at least a 25% market share in the United Kingdom; and

- The UK producer support for the application must be greater than producer opposition.

In addition to the investigation initiated based on the application made by or on behalf of a UK industry, the TRA may initiate an ex officio investigation in exceptional circumstances, by the secretary of state, if it is satisfied that it appears from that evidence that:

- in the case of an antidumping/subsidy investigation:

-

- the volume of dumped/subsidised goods (whether actual or potential) and the injury are more than negligible; and

- the margin of dumping/the amount of subsidy in relation to those goods is more than minimal (see Part 2, Schedule 4 of the Taxation (Cross-border Trade) Act 2018); and

- in the case of a safeguard investigation:

-

- the goods have been or are being imported into the United Kingdom in increased quantities; and

- the importation of the goods in increased quantities has caused or is causing serious injury to UK producers of those goods (see Part 2, Schedule 5 of the Taxation (Cross-border Trade) Act 2018).

4.5 What does the action typically involve and how long does it take?

A trade remedy investigation typically involves the following steps.

Initiation of investigation: The TRA may initiate an investigation when a UK industry applies to do so or, in exceptional circumstances, at the request of the secretary of state. For the industry to request the initiation of an investigation, the applicant should set out the grounds for such request and the trade remedy to be imposed. An investigation will be initiated only where the application contains sufficient evidence. The TRA takes approximately 30 to 40 days to assess the application and to notify the applicant of whether it will initiate an investigation.

TRA investigation: Depending on each specific case, the TRA's investigation may normally run for:

- 11 to 13 months for dumping and subsidisation investigations; and

- eight to 10 months for safeguard investigations.

Once the investigation is initiated, interested parties and contributors will have the chance to contact the TRA over a set period (‘registration period'). In order to contribute, the parties should register online through the Trade Remedies Service. During this period, the TRA may request information from a broad range of stakeholders, including:

- foreign governments;

- exporters or importers of the goods concerned;

- UK producers of like goods; and

- trade or business associations representing one or many of these parties.

The TRA may conduct hearings at any time during an investigation upon the request of interested parties or on its own initiative. The TRA will also conduct an economic interest test to determine whether the trade remedy proposed would be in the United Kingdom's wider economic interests.

Determination: The TRA may make a provisional affirmative determination and recommendation for a provisional remedy to the secretary of state before the final determination and based on evidence of dumping/subsidy and injury to the UK industry. A recommendation for a provisional remedy will be made only if:

- such measure is necessary to prevent injury being caused during the investigation to a UK industry in the relevant goods; and

- the economic interest test has been met.

A statement of essential facts will be sent to parties before the issuance of the final determination. The statement of essential facts sets out the reasoning on how the TRA reached its decision; interested parties will have the opportunity to provide comments and submissions. The TRA will then publish a final determination setting out its recommendation of measures.

Appeals and challenges: Parties that disagree with a decision of the TRA may have the opportunity to apply for a decision to be reconsidered via the Trade Remedies Service. Applications to reconsider must be received within one month and one day of the decision being published or (if this is a later date) coming into effect. Appeals can also be brought to the Tax and Chancery Chamber of the UK Upper Tribunal under two circumstances:

- following the rejection of a request to reconsider a TRA decision under the reconsideration process; or

- to appeal a trade remedies decision made by the secretary of state for international trade.

In most cases, an interested party involved in the original investigation can appeal.

The overall investigative process is a lengthy one. Anti-dumping and anti-subsidy-related investigations are expected to take up to 11 months (but in no case more than 13 months) after the initiation of an investigation. Safeguard investigations are expected to take between eight and 10 months, depending on the investigation.

4.6 How can interested parties defend against a trade remedy action in your jurisdiction?

Paragraph 30 of Schedule 4 and paragraph 29 of Schedule 5 of the Taxation (Cross-border Trade) Act 2018 provide regulations to govern the reconsideration of, or appeal against, decisions made by the TRA or the secretary of state.

The Trade Remedies (Reconsideration and Appeals) (EU Exit) Regulations 2019 (SI 2019/910) (‘R&A Regulations') set out the process for the reconsideration of decisions taken in trade remedy investigations and reviews. Depending on the role of the party concerned and the nature of the decision under challenge, as a matter of domestic law, trade remedy decisions can be challenged by:

- requesting a reconsideration by the TRA;

- appealing to the Upper Tribunal (Tax and Chancery Chamber); or

- applying for judicial review

4.7 How are trade remedy decisions challenged in your jurisdiction? What does this process typically involve and how long does it take?

The R&A Regulations set out the process for the reconsideration of decisions taken in trade remedy investigations and reviews.

The regulations set out a list of decisions that can be reconsidered and who can apply for a reconsideration in each case. Generally, any interested party can apply. When the decision is to reject an application, only the person that made the application can apply.

The regulations stipulate that where an application is made for the reconsideration of an original decision that was published in a notice, the TRA must not reject the application unless it receives the application:

- after one month beginning on the day after the notice is published; or

- (if later) after one month beginning on the day after the notice comes into effect.

A late application, however, may be accepted in limited situations. Application for reconsideration must be submitted via the Trade Remedies Service.

In a reconsideration application, the applicant should:

- set out the grounds for the application;

- explain the outcome it is looking for; and

- demonstrate that it is eligible to apply for reconsideration of this decision.

When the TRA reconsiders a decision, it will follow a process in which it re-examines relevant information, testing both processes and conclusions of the challenged decision. This will be carried out by a team which did not work on the original case. At the end of this process, the TRA may decide either to uphold the original decision or to vary the original decision.

As part of this process, the TRA may:

- request further information from the applicant and/or from any other person, and set a time limit for responses;

- review relevant material, which may include:

-

- information it has asked for;

- the application and any information provided with it; and

- any information obtained from secondary sources;

- carry out hearings;

- disregard information submitted outside the specified timeframe or that does not conform to the request; and

- take any other action as appropriate in line with the relevant regulations.

At the end of the reconsideration process, the TRA will either:

- uphold the original decision if it is satisfied that it was correct; or

- vary the original decision.

If the original decision was a recommendation to the secretary of state, then the secretary of state must accept or reject the reconsidered decision.

4.8 What strategies should be considered to ensure compliance with a trade remedy decision? What penalties are imposed for non-compliance?

Once a trade remedy decision has been issued, the interested parties should comply with its provisions. Interested parties have the right to request a review of the imposition of trade remedy measures in accordance with the provisions of law.

The evasion of trade remedies – that is, actions aimed at evading some or all obligations to enforce the existing trade remedy imposed on products subject to these measures – should be avoided. The trade remedy that is imposed will be expanded if the investigating authority discovers the evasion of a trade remedy.

5 Trade barriers

5.1 What laws and regulations govern trade barriers in your jurisdiction?

Trade barriers include the tariff and non-tariff measures that traders face when exporting to or importing from a specific country.

Specifically, trade in special goods (eg, animals and animal products, plants and plant products, food products, drugs and medicines, waste, chemicals, nuclear materials and weapons) may be subject to requirements relating to licences and certificates, marking, labelling and marketing standards. Imports entering the UK market under preferential treatments must also comply with the rules of origin requirements under such arrangements.

5.2 Which authority is responsible for enforcing the trade barrier regulations? What powers does it have?

Relevant authorities governing trade barrier regulations in the United Kingdom include the following:

- Department for International Trade (DIT): This is the lead department focused on trade deals, market access, export promotion, and inward and outward investment. The DIT includes the Export Control Joint Unit, which administers military and dual-use items for international markets.

- Her Majesty's Revenue and Customs (HMRC): HMRC administers, regulates and enforces the UK tax, payments and customs laws. HMRC's enforcement powers are set out in the Customs and Excise Management Act 1979. Officers have a range of powers to ensure that customs and excise duties are fully accounted for, and to ensure that the market and compliant businesses are not impacted detrimentally. These include the power to:

-

- enter and inspect premises;

- examine goods; and

- open or unpack any container or require that it be opened or unpacked in order to search it or anything in it.

- Trade Remedies Authority (TRA): The TRA determines whether new trade remedies are needed to prevent injury to UK industries caused by unfair trading practices and unforeseen surges in imports. These remedies usually take the form of additional duties on such imports.

Additionally, the UK Office for Sanitary and Phytosanitary (SPS) Trade Assurance and the UK Office for Product Safety & Standards play an important role in setting SPS measures and technical barriers to trade, respectively.

5.3 What is the authority's general approach to enforcing the trade barrier regulations? How vigorously are the rules enforced?

Like most countries, the United Kingdom maintains a range of measures that affect trade, such as:

- labelling requirements;

- import controls on certain sensitive goods, such as military equipment;

- animal and plant health-related measures, such as SPS certification requirements and restrictions on plant and animal imports; and

- environment-related restrictions.

While barriers to trade in the United Kingdom are not currently significant, there are still uncertainties given the ongoing regulatory reforms post-Brexit.

Her Majesty's Revenue and Customs is responsible for ensuring that goods entering the UK market meet the appropriate requirements and comply with the relevant trade measures.

5.4 How is a trade barrier action initiated in your jurisdiction and on what grounds?

The United Kingdom is a very open market and has few trade barriers regarding imports. Most barriers to imports relate to technical barriers to trade and SPS measures necessary for the protection of human, animal and plant life and health; and therefore, complaints in this regard should be raised with the UK Office for SPS Trade Assurance and the UK Office for Product Safety & Standards.

In the particular case of the Office for Product Safety & Standards, affected companies and individuals can try to solve their actions informally, via the office's line manager, or through the formal channel (see question 5.5).

5.5 What does the action typically involve and how long does it take?

For domestic trade barriers, affected parties have the right to seek a solution before the relevant authorities and the domestic courts. In the case of the formal channel of the Office for Product Safety & Standards, there are two basic steps. The first involves launching a formal complaint that explains the issue at hand. This will prompt a response from the office within 20 days, unless otherwise stated. If the matter is not solved, the second step involves a deeper review of the matter by an independent senior official within the relevant department. The office is expected to resolve the second step within 20 working days.

If a solution is not reached, the relevant party can submit a complaint to its member of Parliament, asking for the complaint to be referred to the Parliamentary and Health Service Ombudsman (PHSO). The PHSO can carry out independent investigations into complaints that injustice has been caused by maladministration on the part of UK government departments.

5.6 What measures can the authority take against a foreign trade barrier?

The DIT is responsible for maintaining a record of trade barriers that affect UK exporters and investigating complaints. A list of trade barriers – including local content preferences, complex customs procedures, subsidies, tariffs and other discriminatory practices – is available at www.gov.uk/barriers-trading-investing-abroad.

The DIT has set up a procedure for checking and reporting on barriers to trading and investing abroad. It is suggested that before reporting, traders should check:

- whether the problem is a barrier to goods or barrier to services; and

- whether the problem has already been reported through the portal on barriers to trading and investing abroad.

In the follow-up process, the DIT may decide to:

- explore a diplomatic resolution;

- discuss strategic barriers through overseas ministerial visits;

- start government-to-government talks;

- raise the barrier with the World Trade Organization; or

- feed into free trade agreement negotiations.

There is a set procedure for filing a complaint against foreign trade barriers. Exporters can report a new trade barrier at www.great.gov.uk/report-trade-barrier/.

5.7 What non-tariff trade barriers are imposed in your jurisdiction?

A limited number of non-tariff barriers applicable to goods have been retained after Brexit, including:

- import bans and licence requirements for defined goods;

- phytosanitary certification and limited restrictions on plants;

- sanitary certification and limited restrictions on animals;

- special import rules on potentially dangerous products such as chemicals and pharmaceuticals; and

- use of ‘CE' labelling requirements consistent with the EU-UK Trade and Cooperation Agreement.

6 Sanctions

6.1 What laws and regulations govern sanctions in your jurisdiction?

As a UN member, the United Kingdom is obliged to apply sanctions largely in line with those agreed by the UN Security Council, subject to limited variations.

The Sanctions and Anti-Money Laundering Act 2018 (SAMLA) contains the United Kingdom's trade sanctions. Under Section 1, an ‘appropriate minister' will have the power to impose sanctions:

- for the purposes of compliance with a UN obligation or any other international obligation; or

- for a purpose that would:

-

- further the prevention of terrorism;

- be in the interests of national or international security;

- further a foreign policy objective of the UK government; or

- promote the resolution of armed conflicts or the protection of civilians in conflict zones.

Additionally, the Global Human Rights Sanctions Regulations 2020 (SI 2020/680) empower the government to designate persons involved in serious human rights violations.

6.2 Which authority is responsible for enforcing the sanctions regulations? What powers does it have?

The Foreign, Commonwealth and Development Office is responsible for overall UK government policy on international sanctions. The United Kingdom currently implements sanctions agreed by:

- the UN Security Council, according to international law requirements; and

- the European Union, as provided for in EU legislation and UK implementing legislation.

SAMLA facilitates the continued application of UN sanctions and significantly expands the scope of the United Kingdom's autonomous sanctions powers. SAMLA gives powers to the ‘appropriate minister' in the United Kingdom – defined as the relevant secretary of state or Her Majesty's Treasury (HMT) – to make regulations imposing sanctions.

Additionally, a number of authorities are responsible for enforcing sanctions in different areas:

- Financial: HMT designs, implements and enforces financial sanctions. HMT is also responsible for the domestic counter-terrorism sanctions regulations. These are administered and enforced by the Office of Financial Sanctions Implementation.

- Trade: The Department for International Trade implements trade sanctions. This responsibility is divided between the Export Control Joint Unit and the Import Licensing Branch.

- Transport: The Department for Transport implements and enforces sanctions in the aviation and maritime sectors. The enforcement of these sanctions is supported by:

-

- the Civil Aviation Authority;

- the Maritime and Coastguard Agency;

- the National Air Traffic Services; and

- airport operators.

- Immigration: The Home Office implements and enforces immigration sanctions, also known as travel bans, through the powers of the 1971 Immigration Act.

6.3 What is the authority's general approach to enforcing the sanctions regulations? How vigorously are the rules enforced?

Sanctions regulations are rigorously enforced in the United Kingdom. For example, non-compliance with trade restrictions and financial sanctions is subject to enforcement actions ranging from withdrawal of licences and audit requirements to civil monetary penalties and criminal prosecution.

The Customs and Excise Management Act 1954 (CEMA) sets out the penalties for non-compliance with export regulations when exporting from the United Kingdom. Offences in relation to the export of prohibited or restricted goods are subject to up to seven years' imprisonment and unlimited fines, although most cases will incur less severe penalties (Section 68 of CEMA).

The penalties for breaches of financial sanctions include:

- custodial sentences;

- monetary penalties;

- deferred prosecution agreements; and

- serious crime prevention orders.

6.4 What countries are currently subject to sanctions in your jurisdiction?

A full sanctions list of themes (relating to a particular issue), countries and individuals is available on the Gov.UK website. There are currently over 35 themes and countries and over 1,000 individuals on the UK sanctions list.

6.5 Are individuals or companies subject to sanctions in your jurisdiction?

The United Kingdom has a range of sanctions in place that impact sectors, themes, individuals and companies.

6.6 How are sanction decisions challenged in your jurisdiction? What does this process typically involve and how long does it take?

The Sanctions and Anti-Money Laundering Act 2018 (c 13) (‘Sanctions Act') provides guidance on how to request a review of a designation under the act.

Section 23 of the Sanctions Act enables a person that has been designated under a designation power contained in Sanctions Act regulations (‘designated person') to request variation or revocation of the designation. Section 25 of the Sanctions Act provides a right for persons subject to designation because they are named on a UN list to request that the United Kingdom use its best endeavours to secure their removal from the relevant UN list.

This process involves registration of the challenge and the provision of a variety of evidence to the authorities. The UK government will:

- issue guidance on the documentation needed;

- review the documentation; and notify

- the outcome and the reasons for it in writing ‘as soon as reasonably practicable' depending on the correct submission of documentation.

There is no fixed duration for such review and notification.

6.7 What strategies should be considered to ensure compliance with a sanction decision? What penalties are imposed for non-compliance?

Traders dealing with partners that are subject to UN Security Council or other sanctions might face difficulties in contractual and payment matters. As such, they should still be aware and cautious, and conduct sanctions screening for potential partners, their affiliates, beneficial owners and the extended supply chain – particularly in geographies known to have strong links to sanctioned countries. Attention should also be paid to ensure full compliance with the law on sanctions and anti-money laundering, including any reporting requirements.

7 Trends and predictions

7.1 How would you describe the current legal landscape and prevailing trends affecting international trade in your jurisdiction? Are any new developments anticipated in the next 12 months, including any proposed legislative reforms or the negotiation of new trade agreements?

As of 1 January 2021, the United Kingdom officially left the EU Customs Union, the Single Market and the value added tax area. As a result, many businesses may find dealing with the amended import and export procedures challenging. In preparation for departure, the United Kingdom actively sought to conclude new trading arrangements with the European Union, and to replace and expand free trade agreements with various countries around the world.

Pertaining to the COVID-19 pandemic, practical issues in dealing with the post-lockdown climate in different countries, understanding the rules across borders, margin pressures and shortages of containers and drivers are all concerns facing international businesses. Recruiting employees from overseas and dealing with issues such as quarantine are also issues that continue to hinder businesses in certain sectors, including food producers.

The impact of tariff changes and, more importantly, red tape caused by Brexit also weighs heavily on those running international businesses. In the short to medium term, there will be continued disruption in terms of supply chains and transportation links as outbreaks flare up and ‘local' lockdowns are put in place. This could impact on the supply of goods from and through those areas. Components that are produced in those areas not being shipped could result in problems across supply chains and manufacturing processes, increasing both costs and lead times. Many businesses are trying to reduce overdependence on China and Asia for raw materials and manufactured goods.

To cope with increasing red tape and supply chain disruptions, systems must be continually improved and upgraded. Free trade agreements (FTAs) will play a critical role in any recovery and how these progress will have a major impact on businesses.

In this context, the United Kingdom will continue to progress negotiations for ambitious new FTAs that benefit businesses and consumers in every part of the United Kingdom. The Department for International Trade is helping businesses to take full advantage of the UK FTA programme to export to new markets and access a greater range of products at competitive prices. To achieve this vision, it has the following steps in mind:

- opening negotiations on new trading arrangements with the Gulf Cooperation Council, Israel, India, the Comprehensive and Progressive Agreement for Trans-Pacific Partnership, the African Continental Free Trade Area, Canada, Turkey and Mexico;

- expanding the Export Support Service – while this currently focuses on questions businesses have about trading with Europe, it will be expanded to cover more global markets this year; and

- implementing the proposed Developing Countries Trading Scheme, which would apply to 70 qualifying countries and include improvements such as lower tariffs and simpler rules of origin requirements for countries exporting to the United Kingdom.

8 Tips and traps

8.1 What are your top tips for ensuring compliance with the regulatory framework for international trade and what potential sticking points would you highlight?

There are a number of reference points that traders can consult to ensure compliance with the regulatory framework for international trade in the United Kingdom.

The Gov.Uk portal provides checklists for both importing to and exporting from the United Kingdom. These include guidance on issues such as:

- economic operators registration and identification numbers;

- customs declarations;

- goods valuation;

- customs duties;

- licences and certificates for regulated goods;

- marking, labelling and marketing standards; and

- invoices and other documentation requirements.

Traders should also keep up to date with:

- the latest information on UK free trade agreements for any preferences; and

- notices from the authorities relating to:

-

- customs;

- sanctions;

- export controls;

- restricted persons;

- anti-dumping and countervailing duties and safeguard measures;

- subsidy and incentive programmes for domestic production; and

- geographical protections.

Businesses are generally encouraged to learn more about the issues relevant to their specific industry sector early in their plans to enter the UK market. They may also contact their country's relevant trade and commercial office for information and support. Traders are recommended to regularly check the relevant trade information sources for updated information on the relevant issues and seek advice from qualified professionals when dealing with specific situations.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.