In this whitepaper, we explore how a redesign of Lifetime Mortgage (LTM) could enable insurers to continue to reap the benefits from these products and improve volumes in the high-rate environment.

Section 1: The story so far

1.1 LTMs – the story so far

In a so-called "hunt for yield", the UK Life Insurance sector's private asset allocation increased over the last decade. Lifetime Mortgages ("LTMs", or "Equity Release Mortgages"), once a niche investment class, now feature prominently in annuity providers' investment portfolios, with some providers' allocations exceeding 30%. LTMs provide a good match for annuity liabilities relative to vanilla public credit, not only due to the increased risk-adjusted spreads (and therefore Matching Adjustment ("MA")), but also because of their long-duration nature and potential capital efficiency.

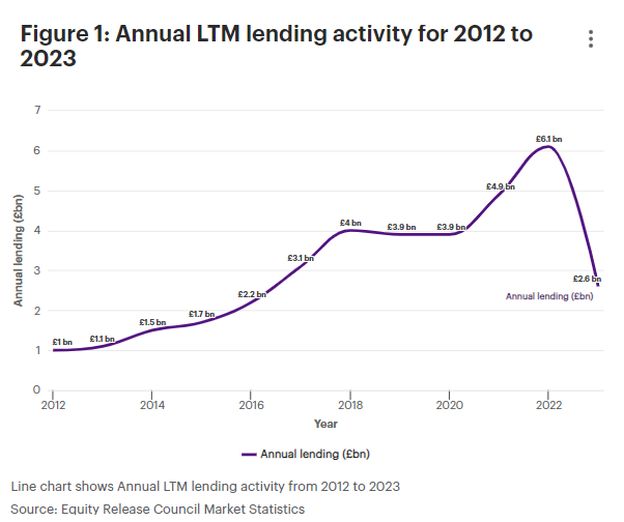

With an increasing number of retirees wanting to unlock equity from their homes, the LTM market has ballooned in size over the last decade. This was in part fuelled by low interest rates making these loans more attractive to borrowers. However, with rises in interest rates since the September 2022 "mini-budget", volumes in the LTM market have become far more subdued. Higher customer rates have dried up consumer demand at the lower end of the loan-to-value ("LTV") range, and higher rates have dried up supply at the higher end of the LTV range due to the increased Non-Negative Equity Guarantee ("NNEG") risk.

In this paper, we explore how a redesign of LTM products could enable insurers to continue to reap the benefits from LTMs and improve volumes in the high-rate environment.

Section 2: LTM Challenges and Potential Solutions

2.1 Current Market Challenges

Back-books

The regulatory treatment of LTMs on the Solvency II ("SII") balance sheet has become more onerous with the introduction of requirements such as the Effective Value Test ("EVT") in Supervisory Statement SS3/17. EVT-in-stress approaches are still being developed by firms despite a requirement for full compliance since 2019.

These additional regulatory hurdles have required insurers to develop bespoke capital modelling approaches that provide a better reflection of the underlying risks for LTMs. These changes have also necessitated enhancements to risk management frameworks and a rethink of the relative attractiveness of the asset class versus long-dated public credit and other private asset alternatives.

New originations

In addition to the regulatory hurdles noted earlier on back books, the current macroeconomic environment poses several challenges to insurance companies originating LTMs. The low LTM demand requires insurance companies to ask themselves a number of difficult questions, for example:

- Do you view that LTMs remain an attractive investment in a high

interest rate environment?

- And if not, will rates fall back,

- And if so, how quickly?

- And if not, will rates fall back,

- How do you balance risk and competitiveness?

- Which market segments can you out-compete in?

- Are assumptions becoming overly reliant on past data that may be out of date?

Before we explore a potential product re-design and other solutions to the current market challenges, we take a closer look at SII capital efficiency of LTMs between Q4 2021 and Q4 2023 and how these changes may be making more traditional product designs less attractive for insurers.

2.2 LTM Capital Efficiency challenges

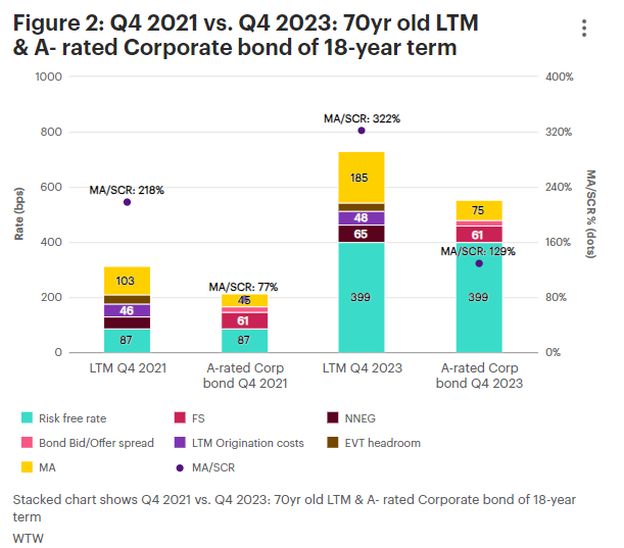

In Figure 2, we have summarised the LTM MA for the average LTM customer rates12 for Q421 and Q423. As shown below, LTMs achieved significantly better MA and capital efficiency relative to A-rated corporate bonds of a comparable tenor.3 While the capital efficiency and MA achievable has improved from Q421 to Q423 for LTMs, the attractiveness of public credit has improved and so the relative capital efficiency benefit of LTMs has declined.

Additional problems originators are facing is that the NNEG has increased on LTMs from the higher-interest roll-up rate. Insurers have been forced to reduce the LTVs they are prepared to offer to remain within risk appetite limits as a result, hampering volumes.

2.3 Potential Solutions

Understanding the value of different LTM market segments

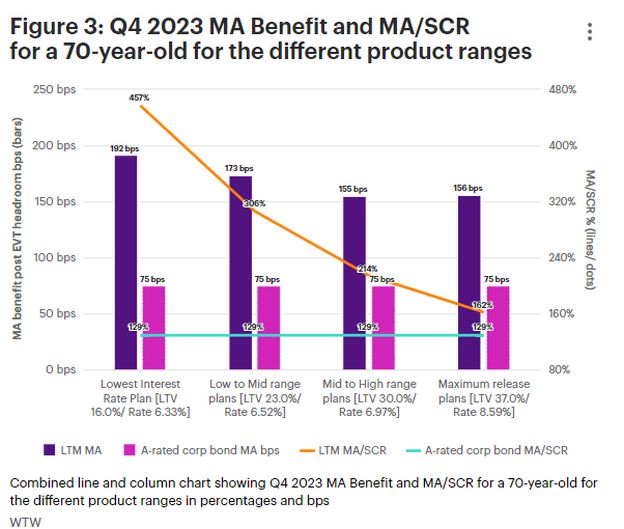

There is a balance to be struck in terms of MA and capital efficiency, and firms should consider this in their pricing. Overall, insurers should aim to identify which part of the market is most optimal for their balance sheet to price more competitively in those parts of the market but maintain coverage of the wide spectrum of the market for diversification benefits. Care should also be taken to ensure there is adequate spread compensation for the level of NNEG risk on the planned business mix. An end-to-end review of the pricing and regulatory capital management frameworks can achieve this.

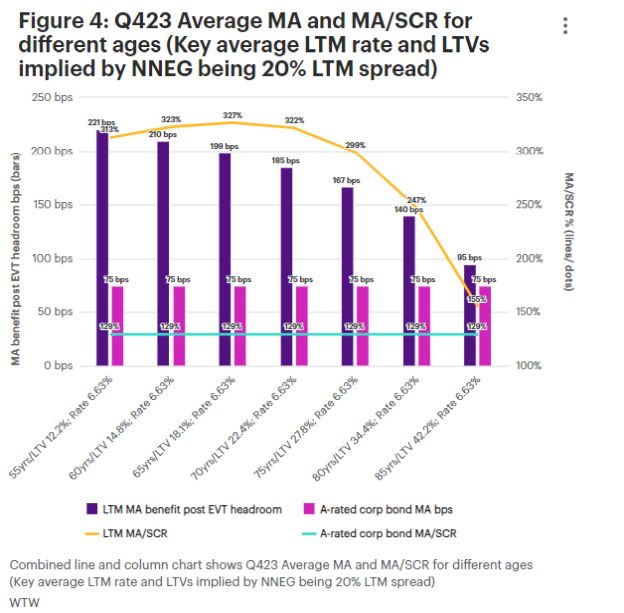

In Figure 4 below, we consider the capital efficiency at the Q4 2023 average LTM rate of 6.63% for different customer age groups. We maintained the LTM rate at 6.63% across the ages and varied the LTVs implied by the NNEG being 20% of spread for each age. This approach is consistent with WTW survey results, where we noted that most firms' pricing only vary LTVs offered for each age with the same rate charged across the ages.

From this analysis, we note the following observations, which may need to feed into pricing considerations by firms:

- Under the basis used in the analysis, MA/SCR capital efficiency rises slowly from age 55, reaches a peak at around the 65 year age, then drops with age, with marked drops in the capital efficiency at ages beyond 70 years.

- While higher ages would be expected to have lower NNEG risk due to lower durations, balance sheet efficiency drops markedly beyond 85-year-olds. This is due to the higher ages having lower durations and economic value, hence origination costs and EVT headroom consume a significant portion of the spread. Firms may need to reconsider their pricing bases for high ages, for example, by increasing rates to obtain higher MA relative to corporate bonds, more so with the current inverted risk-free rate curve.

While this analysis is high-level and not firm specific, with results varying between firms based on their own internal assumptions, it shows the power this kind of analysis can have on LTM pricing.

Product re-design

Reconsidering the LTM product design beyond traditional fixed-rate products could reduce NNEG risk and early repayment risk while offering a competitive differentiator to customers. It could also act as a unique selling point in the market and work toward countering the low LTM demand seen in recent times.

One such idea is to offer a customer rate that steps down based on terms set at the outset of the contract, which could create a capital light product range. Rate step downs will reduce the NNEG risk and may act as an incentive to the borrower to remain with the loan, as a step down in rate is an attractive loyalty feature for customers, thereby helping retain business, reducing Voluntary Early Redemptions ("VERs"). If priced effectively, such a product could take market share from existing high LTV ranges and even allow firms to fund higher LTV products.

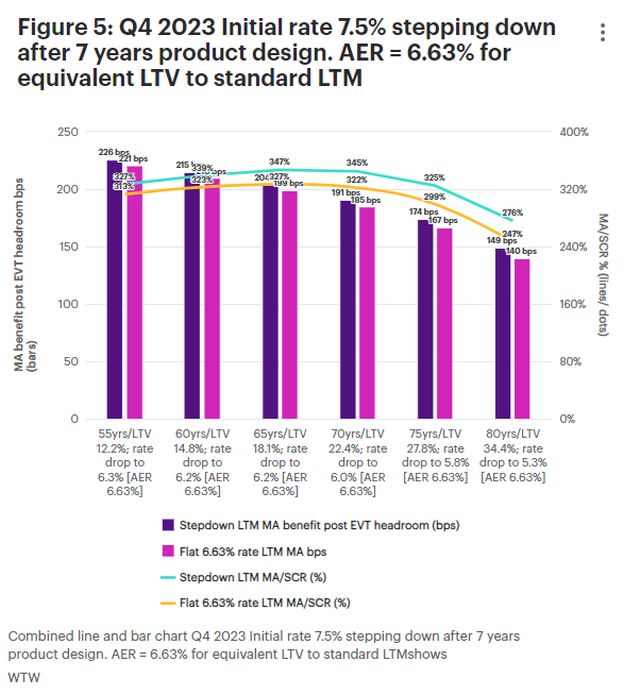

We have considered a specific rate step-down product design. For a 70-year-old, this product has a fixed-rate of 7.5% for the first 7 years, then it drops to a lower rate of 6.0% from the beginning of year 8 onwards, which works to maintain the annual equivalent rate ("AER") of 6.63% for the average product life expectancy, in line with the available rate at Q4 2023 assessed above. This product design makes the LTM more capital efficient than the standard product and may support demand for LTMs as it also allows higher LTVs.

The innovative design achieves better capital efficiency by earning LTM spread early in the term of the product, thereby reducing impact of VER experience. It should be noted that this is more pronounced with the current inverted risk-free rate term structure. The rate step down also reduces the buildup of NNEG, and hence lowers SCR for NNEG risk.

This is a simple product design that can be analysed and expanded upon, with the rates, timing of step down(s) and number of step down(s) assessed to optimise the balance sheet treatment of the asset.

In Figure 5 below, we see that the step-down design improves the capital efficiency and MA. This analysis has been performed with a step down after 7 years for all ages, but the term at which the step down occurs can be optimised for each age to make the product more capital efficient and more attractive to consumers.

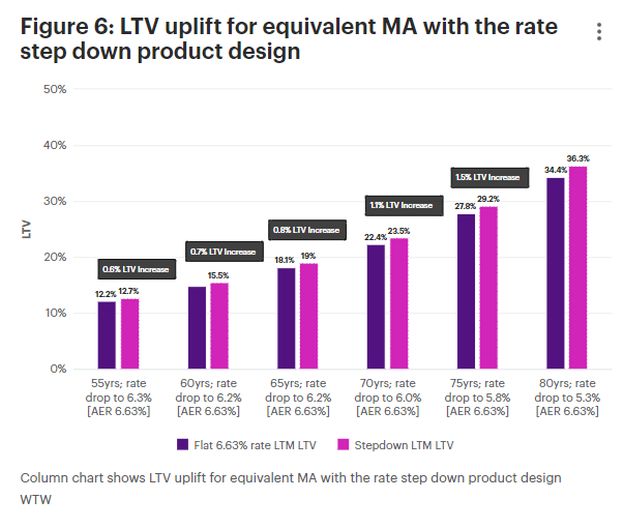

Figure 6 below compares the LTVs that could be offered for a standard fixed rate and step down product, targeted to achieve the same MA benefit. The rate step-down product design allows an LTV uplift as the spread is earned earlier in the term, reducing the impact of VER and reducing the build-up of NNEG as the rate is lower at the longer tenors. The term at which the step down occurs can also be optimised for each age to achieve better customer AER, better LTVs or a combination of both.

The need for an end-to-end LTM product review

Given the ever-changing market and different economic landscape from where LTM assumptions were initially set for most firms, a more comprehensive LTM product review may be required to fully understand and quantify the risks that LTMs expose to the balance sheet.

To be competitive, product design, pricing, securitisation and capital management processes need to be considered holistically. These processes should be considered from end to end, and not viewed in isolation, as changes to any part of the overall process can impact others. A more centralised ownership of the processes has been seen to be effective, with some firms having LTMs as a separate business line with a separate P&L and management team.

On assumptions, early repayment risk is particularly one of the key sources of risk and uncertainty. Due to different firms having different product mixes and product designs, early repayment experience of different portfolios may not be comparable. For most firms, there is no adequate volume of historical data to provide credible data to feed into assumptions setting. The recent change in the macroeconomic environment has also caused a volatile experience of early redemptions. The VER assumption therefore requires a higher degree of expert judgement to derive different sets of VER assumptions for different blocks of back-book business and for different profiles of new originations. Firms may wish to implement a dynamic prepayment model that varies with interest rates, LTVs and other variables expected to impact VER. Other assumptions may similarly require a comprehensive review.

On valuation approaches, there is still a wide variation in the industry on the NNEG valuation approaches, with some firms having an NNEG valuation approach which is more onerous than the PRA's EVT approach. Firms with stronger NNEG valuation approaches and/or more conservative matching adjustment structuring assumptions may struggle to price their LTMs competitively.

On structuring, firms may consider establishing a level of EVT headroom which is acceptable and within risk appetite then structuring teams target achieving this level of headroom. From recent surveys, we noted that structuring differences are the main differentiators of MA benefit and capital efficiency achieved, and well-targeted structures can result in better MA and capital efficiency outcomes relative to corporate bonds. A rethink of the note apportionment methodology should also be considered as part of the end-to-end review.

Section 3: Solvency UK considerations

Solvency UK is widening the MA asset eligibility criteria beyond the fixed cash flow requirement to allow a limited portion of highly predictable ("HP") cash flows, but this comes with new requirements such as Fundamental Spread ("FS") add-ons, additional cashflow matching tests and a 10% limit on the MA benefit obtained from HP assets. While Solvency UK brings about greater investment flexibility, it is unclear that this will lead to any material change for LTMs.

Creation of sub-investment grade mezzanine notes which carry the HP cash flows could be considered as a way to improve liquidity of the structure. While firms remain constrained by the EVT and therefore an increase in MA benefit is unlikely, if sub-investment grade mezzanine notes were added to the part of the MA portfolio which doesn't contribute to the MA benefit, this could improve liquidity. This is achieved by freeing up other assets held in this part of the MA portfolio whilst not reducing EVT headroom or contributing toward the 10% of MA limit for HP assets.

Using these HP mezzanine notes to back the stressed liabilities may also have the benefit of reducing overall capital requirements due to the MA offset of the SCR. This capital management action could reduce current capital requirements for the junior note by a significant amount and free up capital for release: consideration must however be given to how HP assets are generally modelled under stress.

While introducing HP mezzanine notes may be something firms consider, they will also need to factor in the additional associated requirements and restrictions. The operational burdens for implementing these changes should not be underestimated, and firms will need to make a decision as to whether this increased operational complexity and costs are worth any potential benefit. However, if firms are applying to include HP assets into their MAPs for other reasons and the set-up overheads have already been accounted for, then implementing a restructuring to include HP mezzanine notes may improve the overall balance sheet.

Consideration should also be given to the FS add-ons via the MA attestation process that will be required for assets held in the MA portfolio, including LTMs, going forward. However, the existence of the EVT is likely to negate the need for an FS add-on as this acts to cap the MA benefit attainable from LTMs and so in effect does the same job as any FS add-on that would be applied.

All these changes will need to be given due consideration by firms investing in LTMs and appropriate regulatory approvals will need to be sought.

Section 4: Concluding thoughts

Despite the reduction in the relative capital efficiency of LTMs compared to A-rated corporate bonds, LTMs still appear to be more capital efficient than A-rated corporate bonds. However, the current high interest rate environment is driving low LTVs and hence low business volumes seen for 2023 compared to the recent few years. For the low LTV end of the market, the current rates are unfavourably higher than previously which is also driving down demand for LTMs. With the same high-interest environment prevailing for the first quarter of 2024 and uncertainty on when rates may start reducing and by how much, firms can consider the following to enhance the MA benefit and capital efficiency of LTMs on the balance sheet:

- Consider innovative product re-designs such as the customer rate step down product analysed in this paper. For the same AER compared to the flat fixed rate product design, the rate step down achieves better capital efficiency and MA benefit. This rate step down product design may allow firms to offer higher LTVs for the same level of NNEG risk, offer lower AER or a carefully considered combination of both, making it a more competitive product offering.

- Understanding the value of different LTM market segments to identify optimal parts of the market to target and optimise risk versus return on pricing considerations for different parts of the market.

- Comprehensive reconsideration of the full LTM valuation chain from pricing bases, product re-design, valuation, structuring, and risk management enhancements may enable firms to price more competitively to shore up demand without losing capital efficiency. Similar exercises on back books will also optimise the efficiency of LTMs on the insurer balance sheet.

For further discussion on any thoughts and how WTW can provide support on LTMs, the authors and their contact details can be found in below.

Section 5: Appendices

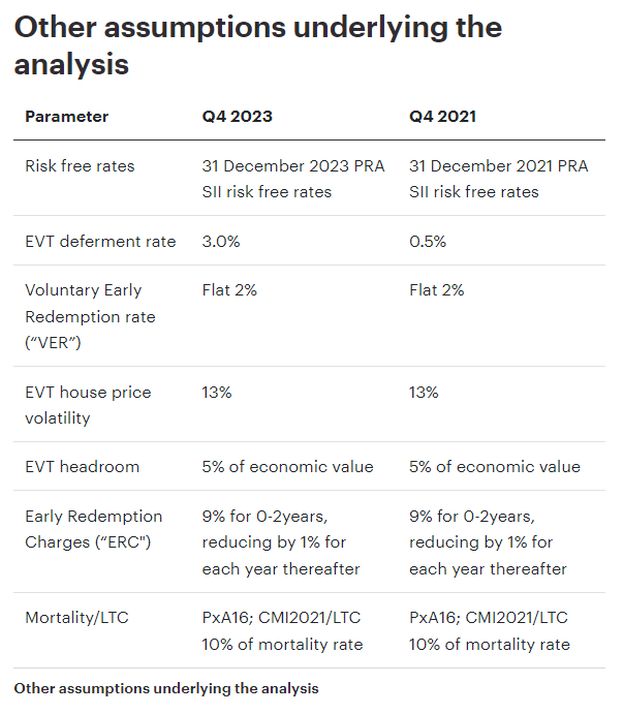

5.1 Assumptions underlying the analysis

MA approximation

The MA post EVT headroom has been approximated by modelling the LTM effective value as 95% of the economic value (i.e., EVT headroom of 5% of economic value) with the economic value modelled using the below assumptions.

- All model points have been run on a £200,000 LTM loan by grossing up the starting house value to the assumed LTV for each model point in the charts.

- LTVs for each age: the LTVs have been set such that the NNEG bps to full LTM spread ratio of 20% is maintained. The 20% assumption is based on analysis of the market average LTVs and rates for the average LTM customer age of 70.

- We have assumed an LTM origination cost of 7% of the LTM loan, and for comparison bonds, we have assumed trading costs of 20bps bid offer spread.

The other assumptions are noted in the tables below:

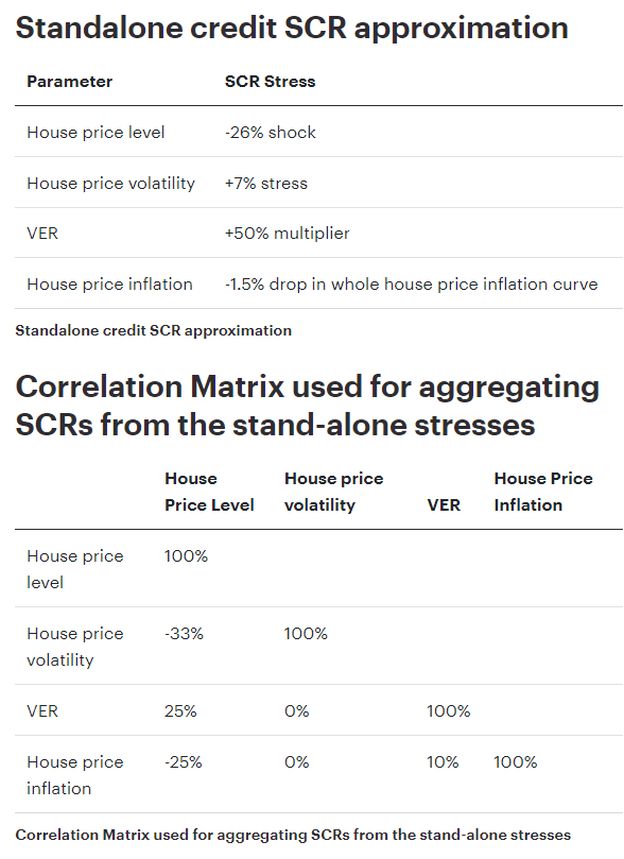

The standalone credit SCR has been approximated by applying the below stresses to the economic value. We have assumed an LTM SCR diversification factor of 60% (i.e., 40% reduction in stand-alone SCR) and a comparison bond SCR diversification factor of 90% (i.e., 10% reduction in stand-alone SCR).

Footnotes

1. Key partnerships market monitor reports average LTM rates.

2. Market monitor equity release performance in the UK.

3. For the underlying assumptions used to approximate the MA and SCR, please refer to Section 5.1 under appendices.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.