- within Tax topic(s)

- in Europe

- within Tax topic(s)

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- with readers working within the Advertising & Public Relations, Banking & Credit and Insurance industries

- within Tax, Employment and HR and Corporate/Commercial Law topic(s)

Navigating Poland's VAT system can be daunting for international businesses, especially when it comes to recovering tax on eligible expenses. Fortunately, Poland provides a structured mechanism for VAT refunds not only for local entities but also for foreign companies engaging with Polish vendors and service providers.

This guide walks you through the key steps, eligibility rules, and practical considerations to help you secure your rightful tax refund.

Understanding Poland's VAT Reclaim Eligibility for Foreigners

Foreign entities - those without a permanent establishment or tax residency in Poland - can still reclaim VAT on specific expenses incurred within Poland or another EU Member State, provided they meet the statutory conditions.

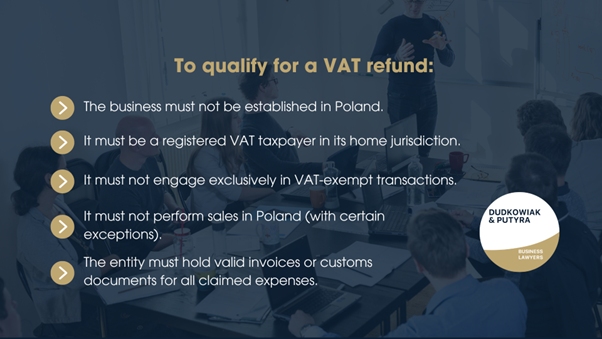

To qualify for a VAT refund:

- The business must not be established in Poland.

- It must be a registered VAT taxpayer in its home jurisdiction.

- It must not engage exclusively in VAT-exempt transactions.

- It must not perform sales in Poland (with certain exceptions).

- The entity must hold valid invoices or customs documents for all claimed expenses.

This process aligns with the EU Council Directive 2008/9/EC, governing VAT refunds to foreign companies within the EU and with the Directive 86/560/EEC applicable for entities established outside the EU (as a rule only for selected countries).

What Kind of Expenses Are Refundable?

A wide variety of business-related costs are eligible for VAT refunds under Polish and EU law, including:

| Category | Examples |

|---|---|

| Transport & Logistics | Fuel, vehicle rental, tolls, road charges |

| Business Travel | Taxis, public transport |

| Events | Entry fees to trade fairs, exhibitions |

| Office-Related | Equipment, repairs, office supplies |

Each item must be used for business purposes, and expenses must be substantiated with formal invoices issued in compliance with Polish VAT regulations.

How to File a VAT Refund Claim in Poland?

Foreign businesses located within the EU must file an application electronically through their own national tax authorities. This application is then transferred to the Polish tax office. Entrepreneurs from outside the EU file an application in regular paper form directly to the Polish tax authorities.

Key conditions:

- Submit the application by 30 September of the year following the tax year in which the expense was incurred.

- Include scanned copies of invoices and customs documents.

- Remember about additional documents if you are located outside the EU (e.g. tax status confirmation).

- Indicate Poland as the country from which the refund is being requested.

Polish authorities typically respond within 4 to 8 months, depending on the complexity and accuracy of the submission.

Tips for Faster Refunds in Poland

- Keep documentation immaculate - Ensure invoices include full supplier details, accurate VAT numbers, and descriptions of services or goods.

- Avoid grey areas - Certain expenses may be non-refundable.

- Use a local advisor - Appointing a VAT specialist or Polish legal counsel can significantly expedite the process and reduce the likelihood of rejections.

Beyond Poland: What About Cross-Border VAT Refunds?

Polish entities operating abroad can also apply for VAT refunds from other EU countries using the same mechanism.

Don't Leave VAT on the Table

For foreign companies doing business in Poland - whether occasionally or frequently - the VAT refund system offers a legitimate way to recover operational costs. By understanding the eligibility rules, documenting expenses properly, and leveraging professional support, businesses can reclaim thousands of euros annually.

For tailored support, reach out to legal professionals well-versed in cross-border VAT matters.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.