1. Income Tax On Companies

1.1. Income Tax Rate

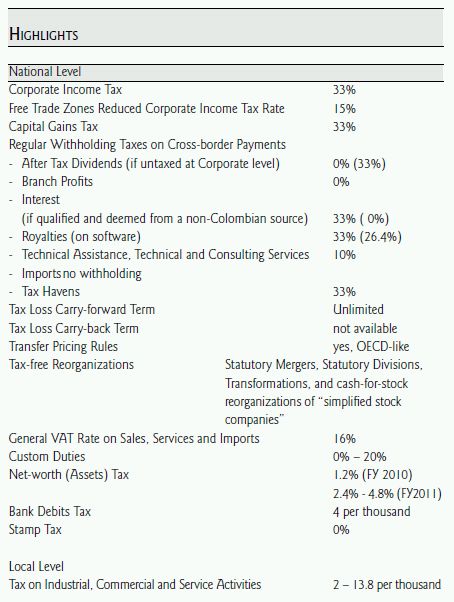

As of January 1st, 2008, the general statutory corporate income tax rate is 33 %.1

Unless otherwise provided, all Colombian and foreign entities subject to income tax in Colombia, including Colombian branches of foreign companies are subject to this 33 % rate.2 The reduced statutory corporate income tax rate applicable to entities that qualify as "industrial users" in Colombian "Free Trade Zones" is 15 %.3 Please bear in mind that there are statutory eligibility requirements in place for "industrial users4" wishing to benefit from the 15 % reduced income tax rate. As of 2010, "industrial users" wishing to benefit form this 15 % rate, must choose between using this benefit or the 30% FAID as Act 13 70-2009 eliminated the concurrance of these two benefits.

1.2. Taxable Base and Income Tax Assessment Process

The Taxable Base is multiplied by the applicable statutory corporate income tax rate and the result is the Income Tax Liability, from which applicable Tax Credits are subtracted to find the Income Tax Charge.

The Taxable Base of the Colombian corporate income tax is the result from subtracting the taxpayer's specifically Exempt Items of Income from the greater of (i) the Net Taxable Income ("NTI") and (ii) the Alternate Minimum Taxable Income. The NTI results from the sum of all revenues realized by the taxpayer, minus the sum of all specifically Excluded Items of Income, minus the sum of all costs and expenses allowed as Deductions. The Alternate Minimum Taxable Income computation is explained in §1.3. below.

The regular income tax assessment process can be illustrated as follows:

Gross Income (sum of all items of income, including short-term capital gains)

[–] Excluded Items of Income

[=] Gross Taxable Income

[–] Allowed Deductions

[=] NTI or Alternate Minimum Taxable Income (if greater)

[–] Tax Loss Carry-forward (if applicable)

[–] Exempt Items of Income

[=] Taxable Base

[*] 33 % Corporate Income Tax Rate (or 15% if applicable)

[=] Income Tax Liability

[–] Tax Credits

[=] Income Tax Charge

1.3. Alternate Minimum Taxable Income ("AMTI")

The taxpayer's AMTI is equal to the taxpayer's Net-worth (i.e., all assets net of all liabilities and other allowable exclusions, e.g., shares in Colombian corporations) as of December 31 st of the year immediately preceding the taxable year, multiplied by 3%.5

If the AMTI is greater than the NTI, the difference between these two items generates a carry-forward against the taxpayer's NTI, which can be within the following five (5) taxable years.6

1.4. Capital Gains

Short-term Capital Gains are deemed as a regular item of income subject to income tax. Long-term Capital Gains, i.e., gains realized on the sale or exchange of certain assets owned for at least two (2) years, are subject to the Capital Gains Tax.7 The taxable base of the Capital Gains Tax is the result of the amount realized, minus the taxpayer's adjusted tax basis on the asset, plus any recaptured depreciation, amortization or deductions, as applicable.8 Capital gains can be offset with capital losses only.9 The capital gains tax rate is 33%.10 Except for certain isolated cases,11 the taxpayer's capital gains tax is assessed, filed and paid with the taxpayer's regular yearly income tax assessment.12 Colombian tax law authorizes tax authorities to challenge through an audit the amount realized in the sale or exchange of assets and reported by the taxpayer, when they find evidence that they have breached certain statutory thresholds that use criteria such as the asset's fair market value, the greater of it's cadastral appraisal or the owner's self-appraisal in the case of real estate, and the "intrinsic" value in the case of stock or quotas.13 There are special rules to determine capital gains in the sale or exchange of intangibles depending on whether the intangible is formed or acquired.14

1.5. Income Tax Deductions

Unless otherwise provided by the statute, all costs and expenses incurred by the taxpayer are deductible, provided that they are related, proportional and necessary to the taxpayer's income producing activity.15 Costs or expenses related to specifically Excluded and/or Exempted Items of Income are not deductible.16 Certain costs and expenses may be subject to limitations, depending on the facts and circumstances of each case, e.g., related party charges and commissions,17 among others. Special limitations apply to the deduction of expenses incurred outside Colombia (see §1.18. below).18

1.6. Depreciation and Amortization

Tangible fixed assets' depreciation is deductible.19 The applicable depreciation term varies depending on the nature of the asset; twenty (20) years for real estate, ten (10) years for all other tangible fixed assets, except for motor vehicles and computers for which regulations establish a Five (5) year term.20 For tax purposes, regular methods used worldwide are commonly accepted in Colombia, e.g., straight-line method, declining balance method, etc.21 Unless specifically restricted, double and triple shift accelerated depreciation is also available and can be combined with the declining balance method when the asset needs to be depreciated in full in the first years of its useful life.22

Certain assets, including acquired intangibles, and certain costs and expenses deemed as necessary investments for the taxpayer's income producing activity that must be capitalized,23 can be amortized through a minimum five (5) year period using any generally accepted amortization method.24

1.7. Transfer Pricing

Colombia has OECD-like transfer pricing rules that are applicable to all transactions between a Colombian party and a foreign related party.25 A different set of rules applies to transactions between two Colombian related parties.26 Under these rules, the Colombian party exceeding certain statutory net assets or revenues thresholds must keep and file with the tax authorities supporting documentation, and prepare a transfer pricing study showing whether the corresponding prices or profit margins are arm's-length.27 Parties domiciled in tax havens are deemed as related parties.2829 The Colombian transfer-pricing regime has a catalogue of situations where two parties are deemed related. This catalogue is complex and its application requires a detailed case-by-case analysis.

Sale or exchange of stock or quotas in Colombian companies by foreign holders to a related party located abroad is subject to transfer pricing rules.30

1.8. Inflation Adjustments

The mandatory income tax inflation index adjustment system was revoked on 2006.31 Nevertheless, as of January 1st, 2007, income taxpayers can continue to use it to adjust the tax basis of fixed assets.32 Such adjustment is not mandatory and will not have effect in the taxpayer's Profits and Losses statement.

1.9. Tax Loss Carry-forward

As of January 1st, 2007 an evergreen tax loss carry-forward against the taxpayer's NTI is available.33 The tax loss must arise from an income producing activity commonly taxable under the regular income taxation rules.34 Should the tax loss lack such nexus, i.e., be related to a non-taxable or exempt income producing activity, the tax loss carry- forward would not be available.35 The credited amount cannot be greater than the taxpayer's NTI on the year the carry-forward is credited, i.e., a tax loss carry-forward cannot generate further tax loss.36 There is no carry-back possibility.

Tax losses realized by December 31st, 2006 can be carried forward subject to: (i) an eight (8) year expiration term, and (ii) a cap equal to 25% of the tax loss in the year the loss was realized.37

Tax loss generated from the 30% Fixed Assets Investments special deduction can be carried forward without any time limitation (see §1.11. below).

Except as provided for reorganizations, tax losses are not transferrable to share or quota holders, or to other taxpayers (see §1.10. below).38 In the case of tax-free mergers the above-mentioned general limitations continue to apply. Nonetheless, in this case part of the tax losses are transferable to the new or surviving entity.39 For tax-free spin offs a proportional part of the tax losses of the target entity are transferred to the resulting entity(ies).40 In order to qualify for the tax losses transfer under reorganization tax rules, the corporate purpose of the merging entities should be the same.41 For spin-offs the corporate purpose of the target entity and of the resulting entities should also be the same.42 The new, surviving or resulting entities will not be allowed to benefit from all of the tax losses accrued by the entities subject to the merger or to the spin-off.

Only that part proportionally corresponding to their participation in the net-worth of the new, surviving or resulting entities, should be deductible.43 The tax loss expiration term (when applicable) is not renewed by a reorganization event.44

Colombian tax law limits (or in some cases sets special conditions) for the assessment and deduction of tax losses other than those generated by the net operating losses. We list some of these cases:

a. loss generated by acts of god damaging taxpayer's assets;45

b. loss generated in the sale of fixed assets;46

c. loss generated in the sale of assets (fixed or current) between related parties, or a

corporation and its shareholders – not deductible;47

d. losses in the sale of stock – not deductible.48

1.10. Tax-Free Reorganizations

Tax-free treatment is available for statutory mergers, statutory divisions, corporate transformations,49 and cash-for-stock reorganizations of "simplified corporations." Although most tax attributes should survive in the head of the beneficiary corporation pursuant to a tax-free reorganization, due care should be given to the restriction on the use of tax losses (see §1.9. above). Except for the proportionality and the corporate purpose matching requirements for the transferability of tax losses, currently in Colombia there are no requirements of continuity of business or continuity of interest as a requirement to qualify for tax-free reorganization treatment.

1.11. 30 % Fixed Assets Investments Special Deduction

Subject to eligibility, the taxpayer can deduct 30% (Act 1370-2009 reduced the FAID benefit from 40% to the actual rate of 30%) of their investments in tangible fixed assets used in the taxpayer's income producing activity.50 The deduction is available for both purchased and manufactured (or built)51 assets and for both new and used (second-hand) assets.52 Leased assets can be eligible for this incentive, provided that the leasing terms incorporate an irrevocable purchase option that is exercised by the taxpayer.53 The taxpayer must take the deduction on the fiscal year of the investment. 54 The following rules apply:

(i) although dividends or profits distributed to share or quota holders are not taxable, provided that they have been subject to income tax at the company level, the 30% fixed assets deduction should not trigger taxable income for the share or quota holders;

(ii) fixed assets purchased from related parties are not eligible;55

(iii) assets subject to this benefit must be depreciated using the straight-line method;56

(iv) tax losses originated by this deduction can be carried-forward against the taxpayer's NTI without any time limitation (see §1.9. above).57

(v) free trade zone users can only benefit from the FAID when not applying the preferential income tax rate of 15%. Concurrence of both benefits is strictly prohibited as of 2010.

The deduction is computed on the cost basis of the asset, whether acquired, manufactured or built. The basis should include the VAT paid in the asset's acquisition but only if the VAT is capitalized in observance to general applicable tax law.58

Otherwise, the non-capitalized VAT should not increase the base to compute the deduction.59 If the non-capitalized VAT is creditable against VAT or income tax, its creditability is not prevented by the use of this deduction.

Should the asset purchase agreement be cancelled, rescinded, vacated or annulled, the deduction is recaptured in full and computed as net taxable income for the taxpayer in the fiscal year of the contract's rescission.60 The deduction is also recaptured in full on leased property, whenever the taxpayer fails to exercise the irrevocable

purchase option. In this event the lessor most report the lessee's omission to the Colombian Internal Revenue Service.61

This deduction is an additional tax benefit that should not prevent the taxpayer from benefiting from other statutory deductions on this type of investments, such as depreciation (only under straight-line method) or amortization. If the taxpayer stops using the property on her income producing activity prior to its depreciation

or amortization in full, the special deduction is recaptured in proportion to the remaining useful life (or amortization period) of the property.

1.12. Leasing Tax Treatment

Leased assets must be initially accounted for their value, both as an asset and a liability.62 The lease payments' portion allocated to principal decreases the liability while the portion allocated to interest is a deductible expense.63 Depreciation and amortization deductions are available, as applicable.64

In the case of M&E leasing agreements executed by "Medium Size Companies"65 where the lease term is thirty-six (36) months or more, or twenty-four (24 ) months or more in the case of motor vehicles and computers, or sixty (60) months or more in the case of real estate, the taxpayer cannot account an asset and a liability. Instead and provided that all the deductibility requirements are met, the full payment amount should be treated as a deduction.66 The same rule is temporally available for leasing agreements entered by December 31 st, 2011 in certain infrastructure projects, provided that the lease term is twelve (12 ) years or more, among other requirements.67

1.13. Certain Exempt Items of Income

Subject to eligibility and compliance by the taxpayer of the statutory requirements, income from the following activities is treated as an Exempt Item of Income:

(i) a fifteen (15) year exemption on income from power generation activities based on wind, biomass and agricultural waste technologies;68

(ii) as of January 1st, 2003,69 a fifteen (15) year exemption on income from fluvial transportation services using low draught boats;

(iii) a thirty (30) year exemption on income from hotel services rendered in newly built or refurbished facilities, provided that the facilities were built or refurbished within the fifteen (15) year term following January 1st, 2003;70

(iv) as of January 1st, 2003, a twenty (20) year exemption on income from ecotourism activities certified as such by the correspondent authority, available for twenty (20) years beginning on January 1st, 2003.71

(v) use of qualified new forestry plantations or investment in new sawmills for the use of said plantations.

1.14. Filing and Payment

The taxpayer must file the income tax return and pay the corresponding tax liability on the year immediately succeeding the fiscal year for which the return was prepared.

Every year tax authorities issue a filing and payment schedule with specific deadlines that vary depending on the last number of the taxpayer's Tax Identification Number.72 Usually, filing and payment dates are similar year after year. For FY2009, all entities including corporations must file their income tax return on April 2010.73 The taxpayer can pay the Income Tax Charge in two (2) 50% instalments. 74 The first instalment, on the filing date, and the second instalment on June 2010, observing the yearly payment schedule issued by the tax authorities. There are special filing and payment schedules issued by the tax authorities for certain corporations in the list of "grand income taxpayers." For FY2010 all "grand income taxpayers" must file their return on April 2010. "grand income taxpayers" benefit from a five (5) instalments payment facility. For FY2009 these instalments are due on February, April (upon filing), June, August and October 2010.

1.15. Non-payment and Lateness Penalties

Unpaid taxes are subject to daily interests75 at a rate equal to the highest legally accepted three (3) month rate certified by the Financial Regulatory Agency.76 Depending on the facts and circumstances of each case, other penalties apply for non-filing, late filing, or inaccurate filing, which may range from 5% up to 200% of the corresponding tax liability.77

1.16. Dividends Tax / Branch Profits Tax

As of January 1st, 2007, there is no remittance tax charge on dividends and branch profits distributed to non-resident alien entities or individuals.78 Dividends or profits generated by December 31 st, 2006, were subject to the former 7%

charge on dividends and branch profits. If such dividends or profits were reinvested in Colombia for a minimum five (5) year term, they were eligible for an exemption from this tax.79

Company profits are only taxed at the company's level. Nevertheless, if the earnings and profits of the company exceed the tax profits subject to income tax at the company level, the excess would be subject to income tax at the share or quota holder level.80 If the shareholder is a foreign resident, the applicable rate is 33%. In the case

of a Colombian branch of a foreign company, there should be no home office level taxation on the excess of the branch's earnings and profits over the tax profits subject to income tax in Colombia at the branch level.

1.17. Withholding Tax on Cross-border Payments

When Colombian sourced income is remitted abroad to a beneficiary that is a non-resident alien individual or entity, the payment should be subject to a withholding tax.

1.17.1. Dividends

If the corresponding profits were taxed at the corporate level then no withholding tax applies, otherwise a 33% withholding tax would be applicable.81

1.17.2. Royalties

Royalty payments are subject to a 33% withholding tax for income tax, with the exception of royalties on movies and software that are subject to an effective withholding tax rate of 19.8% and 26.4%, respectively .82

1.17.3. Technical Services, Technical Assistance and Consulting Services

Whether rendered in Colombia or abroad by non-residents, payments for technical services, technical assistance and consulting services are subject to 10% withholding tax.83

1.17.4. Other Services

If rendered from abroad and are not technical services or technical assistance or consulting services, then no withholding tax applies.84 If the services were rendered in Colombia, then a 33 % withholding tax applies, unless otherwise provided by special rules.

1.17.5. I nterest and Leasing Payments

Foreign debt interest payments and cross-border leasing payments are generally eligible to be deemed as income from a source outside Colombia.85 Therefore, not subject to withholding tax in Colombia.86 Interest and lease payments eligibility for this treatment should be carefully reviewed on a case-by-case basis. Should the interest and lease payments fail the eligibility test, they would be subject to a 33 % withholding tax. A reduced 2% withholding tax applies in some specific cases for M&E leasing payments in the construction industry, provided that certain requirements are met with.87

1.17.6. Capital Contributions Repatriation

For the foreign share or quota holders, reimbursements of capital contributions not corresponding to dividend or profit distributions are non-taxable items of income. Therefore no withholding tax should apply.

1.17.7. Tax Havens88

Payments directed to a tax haven beneficiary corresponding to items of income deemed from a Colombian source, are subject to a 33 % withholding tax. Otherwise the corresponding deduction will not be allowed.89 This higher withholding tax rate should not be applicable to interest and leasing payments corresponding to cross-border transactions duly registered with the Central Bank, provided that they meet the criteria to be deemed as income from a source outside Colombia (see §1.17.5. above).90

1.18. Additional Limitations on Costs and Expenses Incurred Abroad by Colombian Taxpayers

In addition to the regular deductibility requirements, costs and expenses incurred abroad are subject to additional limitations.

Costs and expenses incurred abroad are deductible only to the extent that such deductions do not exceed 15% of the taxpayer's Net Taxable Income assessed without taking into account these deductible items.91 This 15% limitation does

not apply whenever the payment abroad has been subjected to the corresponding statutory withholding tax, on certain commission payments, on interest and leasing payments that are deemed not from a Colombian source, and on payments on imported movable tangible property.92

Payments to a home office or parent company abroad are only deductible if they were subject to withholding tax in Colombia and meet the transfer pricing arm'slength criteria. There are other limitations on interest payments to a related party abroad, among others, which need to be analyzed on a case-by-case basis.

1.19. S tatutory Foreign Tax Credit ("FTC")

Provided compliance of the statutory requirements and subject to certain limitations, Colombian companies with operations outside Colombia are eligible for both a direct and an indirect statutory FTC for taxes levied by the source country on non-Colombian source income and dividends, respectively.93

1.20. Income Tax Treaties

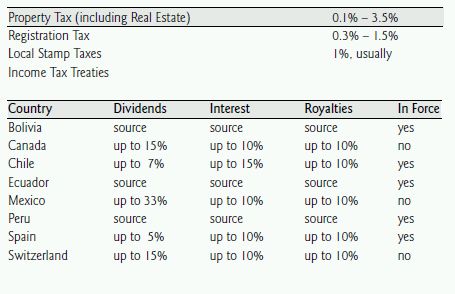

Colombia's belated development of a network of OECD-like treaties has lead to the conclusion of income tax treaties with Spain,94 Chile,95 Canada, Mexico and Switzerland.

Currently there are ongoing negotiations with Belgium, Czech Republic, Germany, South Korea, Netherlands, India, and the United States. The treaties with Spain and Chile are already enforceable. The treaties with Switzerland, Mexico and Canada are not yet enforceable because the ratification process has not yet concluded.

Colombia is a member of the Andean Pact. Therefore, it benefits from the Andean Pact tax Directive 578 to avoid double income taxation, enacted in 2004. With isolated exceptions, this tax Directive provides for exclusive source taxation among member countries96.

In addition, Colombia currently has limited scope income tax treaties to avoid double taxation on sea and air transportation activities with Argentina,97 Brazil,98 Chile, France (air)99, Germany,100 Italy,101 Panama(air),102 United States of America,103 and Venezuela.104

2. Value Added Tax ("VAT")

2.1. Tax Rates

VAT's general rate is 16%.105 There are reduced (10%)106 and increased rates for certain goods and services, e.g., motor vehicles rates range from 20% to 35%, depending on the vehicle type.107

2.2. Taxable Transactions

The sale and importation of movable tangible property, and services rendered in Colombia are subject to VAT.108 The sale of intangibles and seller's fixed assets is not subject to VAT.109 Certain public entities of the national and local territorial level are not subject to VAT.110

Consulting, advising and auditing services, rendered outside of Colombian to a Colombian party are subject to VAT. In these cases the VAT does not affect the foreign party as the Colombian party must cover and pay directly to the tax authorities 100% of the accrued VAT.111

Certain goods and services are exempted ("Zero-rated")112 or not taxable with VAT ("Excluded") goods.113 The lists of zero-rated and excluded goods are extensive and should be checked in detail on a case-by-case basis. In the case of Excluded goods and services, any VAT paid by the taxpayer to her goods and service suppliers has to be capitalized as part of the cost of the Excluded goods sold. In the case of Zerorated goods and services, any VAT paid by the taxpayer to her goods and service suppliers generates a VAT credit (See §2.4. below).114 In certain cases VAT credits from Zero-rated transactions may result in a refundable VAT balance.

2.3. Taxable Base

As a general rule, the taxable base is the price or value of the consideration paid for the goods or services, which should correspond to their fair market value.115 There are certain cases116 where certain items must be either included or excluded from the taxable base and/or cases with either mandatory or optional taxable bases, which should be analyzed on a case-by-case basis.

2.4. Creditable VAT

Unless otherwise provided, all VAT paid to suppliers of goods and services that constitute a cost or expense of the taxpayer's income producing activity, is creditable towards the VAT collected by the taxpayer from her clients.117

Unless otherwise allowed by law (See §2.5. below), VAT paid on the acquisition and importation of goods that become fixed assets for the buyer is neither creditable

against VAT nor income tax.118 This VAT should be capitalized increasing the taxpayer's cost basis of the fixed asset. There are certain limitations on the VAT credits available for zero-rated transactions.

2.5. Selected VAT Incentives

The following are some of the statutory VAT incentives available:

2.5.1. T emporary Importation of Heavy M&E

Temporary importation of "heavy119" M&E not produced in Colombia effectively used in a "basic industry120"in Colombia, should not be subject to import VAT.121

Although it is not clear, it is likely that this treatment does not apply to goods imported for construction sites.

2.5.2. Permanent Importation of Heavy M&E

Permanent importation of heavy M&E (whether or not produced in Colombia) is subject to VAT. But if the M&E's is going to be used in a "basic industry" and it's CIF value exceeds USD$500K, payment of the VAT can be deferred (40% upon importation, and 30% in each of the following 2 years).122 In addition, in these cases the VAT paid can be credited against the taxpayer's income tax in the taxable year in which the VAT was paid or in the subsequent taxable years if the VAT paid cannot be initially credited in full.123

2.5.3. Environmental Monitoring and Control Systems

Any domestic or imported equipments or devices to be used in the construction of control and monitoring systems required by environmental law and standards in any activity, are not subject to VAT.124 Access to this exemption requires certification of the environmental authority qualifying the specific equipment or devices acquired.125

2.6. Payment and Filing

VAT has a bimonthly taxable period.126 The VAT return must be filed and paid in full on the filing dates scheduled by the government for these purposes, which are usually after the first week immediately following the end of the corresponding bimonthly period.127

2.7. Andean Pact VAT Harmonization

In addition to Andean Pact Directive 578 to Avoid Double Income Taxation (see §1.20. above), Andean Pact Directive 599 establishes the framework for the near future harmonization of the VAT regimes in member countries.128

3. Net-worth Tax

From FY2007 through FY2010, taxpayers with a net-worth equal or greater than COP$ 3,000,000.00 are subject to a national level net-worth tax.129 Its taxable base is the taxpayers' net-worth as of January 1, 2007,130 i.e., assets minus liabilities, excluding stock held in Colombian corporations. The tax is computed and paid each of the four (4) taxable years on the same taxable base, using a 1.2% tax rate.131 Among others, Colombian companies and Colombian branches of foreign companies are subject to this tax.132

The 2010 tax reform act133 introduces a new "temporary" net-worth tax payable in installments from 2011 through 2014. This tax is almost identical to its predecessor 1.2% net-worth tax currently in force through fiscal year 2010.

Taxpayers subject to the newly adopted net-worth tax would have to assess the tax on their net-worth as of January 1st, 2011. If the taxpayer's net-worth as of January 1st, 2011 were $3,000,000,000 Colombian Pesos without exceeding $4,999,999,999.99 Colombian Pesos, the applicable rate would be 2.4%. If the taxpayer's net-worth exceeds $5,000,000,000 Colombian Pesos, the applicable rate would be 4.8%. If the taxpayer's net-worth does not exceed $2,999,999,999.99, the taxpayer would not be subject to the 2011 net-worth tax.

Although taxpayers subject to the 2011 net-worth tax would need to assess their net-worth tax liability on 2011 using their net-worth as of January 1st of that year, the tax would be payable in 8 installments. The first 2 installments would be payable on 2011 while the remaining 6 installments would be payable from 2012 through 2014, 2 installments each year on the dates that the Government indicates on the corresponding regulations.

In addition to a number of taxpayers that the 2010 tax reform act considers not subject to the new 2011 net-worth tax, even if their net-worth is within the taxable brackets, there are certain assets that the taxpayer can deduct from the 2011 net-worth taxable base.

4. Bank Debits Tax

This is a national level tax. Colombian banks (and other savings institutions) must withhold the tax at source.134 It applies on any funds deposited that are either withdrawn or transferred from checking or savings accounts.135 The taxable base is the amount withdrawn or transferred. The tax rate is 4 per thousand.136 There are very limited exemptions to this tax.137 It is an important tax to keep in mind when structuring a transactions' cash flow.

5. Local tax on industrial, commercial and service activities

This is a municipal (local) level tax applicable to all industrial commercial and service activities performed in the territory of a municipality. The taxable base is the sum of the taxpayer's gross revenue from the activity carried out in the relevant municipality. The tax rates vary from one municipality to the next and range from 2 to 10 per thousand138 (Bogota's rates go as high as 13,8 per thousand).139 This tax is usually paid and a return filed yearly, with the exception of some municipalities that have adopted a two (2) month taxable period, e.g., Bogota140,141. Incentives for this tax are created and regulated by each municipality. Therefore, the availability of incentives must be confirmed on a case-by-case basis.

6. Property Taxes

There are municipal (local) level taxes on real estate142 and vehicles. Each municipality adopts the applicable tax rates.143 Therefore, they vary from one municipality to the next. Real estate tax rates usually range between 1 per thousand and 33 per thousand144. Motor vehicles tax rates range between 1% and 3.5%. Unless otherwise specified, the taxable base in the case of real estate is the cadastral value of the property,145 and in the case of motor vehicles is their fair market value. Unless otherwise specified in the corresponding municipal ordinances, filing and payment is usually on a yearly basis.

Local tax incentives available, if any, are regulated by the relevant municipal ordinance applicable in the municipality in which the property is located or registered.

Therefore, the availability of incentives must be confirmed on a case-by-case basis.

7. Registration Tax

A taxpayer registering acts and documents with the cadastral registry or merchants' registry offices is subject to this tax.146 Depending on the type of act or document, the tax rate ranges from 0.5% to 1.5%147 (including registration rights) when the registration is with the cadastral registry office, and from 0.3% to 0.7%148 when the registration is with the merchants' registry office. Unless otherwise provided, the taxable base is the amount of the price or consideration reflected in the document. Very few documents subject to registration are exempt from this tax.149 Documents subject to registration tax are exempted from the national level stamp tax (see §5. above). If one of the parties to the document is a public entity, the taxable base is reduced to 50% of the regular taxable base.150

8. Local Stamp Taxes

Certain laws authorize departments151 to enact local stamp taxes to support investments in hospitals, universities and other public entities and activities.152 Such local stamp taxes are usually levied at a 1% rate on the gross income attached to the taxable event. Before engaging in activities, agreements or transactions with effects within the jurisdiction of any department in Colombia, the Taxpayer must confirm whether a local stamp tax is in place that could be triggered by such activity, agreement or transaction.

9. Royalties on Natural Resource s

Exploration Activities

Unless otherwise provided, all natural resources exploration activities are subject to the payment of royalties.153 This summary does not cover the royalty regime. Prior to engaging on any natural resources exploration activity in Colombia, you must seek qualified legal advice on the royalty regime applicable to the specific activity and jurisdiction.

10. Welfare Contributions

10.1. Retirement Contributions

The employee can elect between private or public pension funds.154 The contribution must be equal to at least 16% of the employee's wage;155 both employer and employees can make additional voluntary contributions. Contributions must be computed and paid to the pension funds monthly.156 The employer must cover 75%157 of the contribution, and the employee the remaining 25 %. The employer must withhold the employee's 25 %158 and deposit 100% of the monthly contribution in the pension fund.159

10.2. Health Contributions

The employee must be affiliated to a general Health Care Plan ("HCP").160 Contributions to the HCP must be equal to 12,5% of the employee's wage.161 Contributions must be computed and paid monthly. The employer must cover 2/3 of the contribution, 162 and the employee the remaining 1/3.163 The employer must withhold the employee's 1/3 and pay 100% of the monthly health contribution.164

10.3. Employment Risks Insurance System

The employee must be affiliated to an employment risk insurance system of her election.165 Contributions must be between 0.348% and 8,7% (depending on the activity) and are computed and paid monthly.166 The employer must cover and pay to the insurer 100% of the contribution.

10.4. Contributions to Child and Family Protection Services, Public Training System, and Compensation Funds

The employer must make these 3%,167 2%168 and 4%169 contributions, respectively, on behalf of the employee. The employer must cover 100% of these contributions. Filing and payment is done monthly.170

10.5. Unemployment Fund Contribution

During the employment relation, the employer must contribute an amount equal to one monthly wage per year to the employee's unemployment fund of choice.171 In addition, the employer must pay to the employee a 12 % yearly interest on the amount of that yearly contribution.172 Both the contribution and the interest must be paid on a yearly basis.

10.6. Incidence on Wages Deductibility

Payment of the above-mentioned welfare contributions is a requirement for deductibility of the corresponding wages paid by the employer .173

11. Customs Import s Regime

The following sections summarize some (not all) general aspects of the Colombian customs imports regime.

11.1. Imports Custom Duties

Unless Exempted, zero-rated or a different rate applies, importation of goods is subject to a 16% import VAT.174 In addition to import VAT, imports are also subject to custom duties ranging between 5% and 20%.175 Colombia has entered into Preferred Custom Duties Agreements with many countries,176 reducing the applicable custom duties for certain goods.

11.2. Taxable Base

Unless otherwise provided, custom duties are computed on the CIF value of the goods, while import VAT is computed on the CIF value plus the corresponding custom duties.177

11.3. Customs Valuation

Custom valuation rules in place in Colombia are those of the GATT (1994) valuation code, which are similar to the current WTO valuation rules. For valuation purposes, the Andean Pact valuation rules in Directives 378 and 379 apply. These rules are also similar to the first mentioned rules.178

11.4. Filing and Payment

An import return must be filed upon nationalizing the goods. As a general rule in the ordinary importation regime, custom duties and import VAT must be paid and an imports return filed within the first month following the arrival of the goods to Colombia. In certain cases the importer can request before custom authorities a one (1) month filing extension.179

11.5. Used M&E

Imported used M&E (and spare parts) require a previous import license that will be granted by the foreign trade authorities,180 only whenever the M&E are not produced locally or in any Andean Pact country. Importation of used spare parts is hardly authorized.181

11.6. Selected Custom Duties Imports Regimes Available

In addition to the regular imports regime, a variety of special customs regimes are available for M&E imports. The applicable duties and VAT vary depending on the specific regime.182

Both the regular and temporal imports regimes are available for M&E imports whether leased, on free bailment, or contributed in kind to a Colombian corporation or branch. Purchased M&E can only be imported into the country through the regular imports regime. The following is an overview of certain features of the regular and some temporal imports regimes available.

11.6.1. Regular Imports Regime

It applies to all goods that will remain permanently in Colombian territory without any use or jurisdictional restrictions. Upon nationalization, full payment of custom duties and import VAT is required.183 For foreign exchange purposes, these imports may be reimbursable or non-reimbursable. Non-reimbursable imports require a previously obtained imports license.184

11.6.2. Long-Term Temporary Imports Regime

It applies to M&E and spare parts listed by the applicable regulations as "Capital Goods." This regime is used whenever the goods are expected to remain in Colombia for a term of at least 10 months and no longer than 5 years.185 Under special circumstances, the Customs Administration has the authority to approve a longer term upon request.186 During this term, payment of custom duties and import VAT will be deferred, payable in equal instalments every six months.

It is important to keep in mind that computation of customs duties and import VAT must be performed upon the temporary nationalization of the goods and filing the return within the above-stated one (1) month period (See §12.4. above). If the Customs Administration authorizes a longer permanence period for the goods, payment of duties and VAT must be performed within the first 5-years of permanence.

In any event the importer must execute a compliance bond guaranteeing payment default or delays. For foreign exchange purposes, these imports may be reimbursable or non-reimbursable. Non-reimbursable imports require a previously obtained imports license. Upon finalization of the term, the importer can either export back or

nationalize the goods without paying any additional amounts for custom duties or import VAT.187

11.6.3. Long-Term Temporary Imports Regime for Leased Equipment

The rules of this regime are similar to the above-explained rules. Nevertheless, because for foreign exchange purposes lease payments are treated as foreign debt payments, the imports must be non-reimbursable imports. In addition, this regime allows the substitution of the goods initially imported and the corresponding spare parts (if any).188

11.6.4. S hort-Term Temporary Imports

This regime applies to specific goods that will be used for a certain activities taking no longer than six (6) months. The customs service can authorize a three (3) month extension.189 At the expiration of the authorized stay period, the goods must be exported back or the importer must apply for a long-term importation regime, otherwise the goods are forfeited and/or a 200% fine will be imposed.190 Although for control purposes an imports return must be filed within the above-stated one month period (see 12.4 above) assessing both customs duties and import VAT, payment of such duties and VAT is not required, provided that a guarantee for 150% of the VAT and customs duties amount is subscribed.191

11.6.5. VAT Incentives

The VAT incentives mentioned in §2.5. above are available for imported goods as well, provided compliance of certain requirements.

11.6.6. Free Trade Zones ("FTZ")

Colombia has an attractive FTZ regime192 that should be carefully explored by importers and other parties with business interest or permanent operations in the country.

In addition to the practical reasons and other benefits attached to FTZ, two of the most important benefits available for operations carried out from FTZ users (industrial and operators) are: (i) the entitlement to a reduced 15% income tax rate;193 and (ii) Zero-rated VAT treatment for goods purchased both within the FTZ from other "FTZ users" or outside of the FTZ.194

11.6.7. "Plan Vallejo" Special Imports Regime

Pursuant to complying with certain requirements, under "Plan Vallejo" raw materials, capital goods, spare parts, and other goods exclusively employed in the manufacturing of goods that are effectively exported out of Colombia, or that are employed in rendering services effectively connected with such manufacturing activity, can be temporarily imported into Colombia as zero-rated goods for both customs and import VAT purposes.195 Both agricultural activities196 and service activities197 could be eligible for "Plan Vallejo" benefits.

Footnotes

1 Tax Code, § 240.

2 Idem.

3 Tax Code § 240-1

4 Colombia Tax Service, Ruling 79604-2007, October 2, 2007.

5 Idem, § 188 and 189.

6 Idem, § 189.

7 Idem, § 300.

8 Idem, § 69 to 72.

9 Idem, § 311.

10 Idem, § 313.

11 These include the case of both short and long term capital gains realized on the sale or exchange of sock or quotas in

Colombian companies by a non-resident alien ("NRA"). In this case the NRA most file an advanced income tax return

reporting the transaction within the first month following the transaction. In this case, other Foreign Investment Control

requirements apply. Tax Code, § 326. Decree 1242-2003.

12 Tax Code, § 5 and 596.

13 Idem, § 90.

14 Idem, § 74 and 75.

15 Idem, § 107.

16 Idem, § 177-1.

17 Idem, § 124 and 124-1.

18 Idem, § 122.

19 Idem, § 128.

20 Decree 3019-1989.

21 Tax Code, § 134.

22 Idem, § 140.

23 These include expenses for the installation, organization and development or cost of acquisition or exploitation of mines

24 Tax Code, § 143.

25 Idem, § 260-1 to 260-11.

26 Tax Code, § 260-1.

27 Idem, § 260-4 and 260-8.

28 Idem, § 260-6.

29 The government must issue a tax havens list, which as of March, 2010 had not been issued.

30 Colombia Tax Service, Ruling 53175-2009, July 3, 2009.

31 Act 1111, 2006.

32 Tax Code, § 68.

33 Idem, § 147.

34 Idem.

35 Idem.

36 Idem.

37 Act 1111-2006, § 5 and Circular 9-2007.

38 Tax code § 68

39 Idem.

40 Idem.

41 Idem.

42 Idem.

43 Idem.

44 Idem.

45 Tax Code, § 148.

46 Idem, § 149.

47 Idem, § 151.

48 Idem, § 153.

49 Idem, § 14-1 and 14-2. Act 222-1995, § 3.

50 Tax Code, § 158-3.

51 Colombia Tax Service, Ruling 2376-2009, January 14, 2009.

52 Colombia Tax Service, Ruling 31270-2009, January 14, 2009. – Administrative Court Decision No. 15396, October 24,

2007.

53 Tax Code, § 158-3.

54 Decree 1766-2004, § 3.

55 Idem.

56 Idem.

57 Tax Code, § 147.

58 Decree 1766-2004, § 6.

59 Tax Code, § 258-2 and 485-2.

60 Decree 1766-2004, § 5.

61 Idem.

62 Tax Code, § 127-1.

63 Idem.

64 Idem.

65 i.e., with assets in an amount between approx. USD$1,200,000 and USD$7,200,000

66 Ibidem.

67 Act 223-1995, § 89.

68 Tax Code, § 207-2.

69 Decree 2755-2003, § 3.

70 Decree 2755-2003, § 4 and 6.

71 Decree 2755-2003, § 10.

72 Tax Code, § 579 and 800.

73 Decree 4680-2008.

74 Act 998-2005. Decree 4680-2008.

75 Tax Code, § 634.

76 Idem, § 635.

77 Tax Code, § 641 to 647.

78 The 7% remittance tax on dividends and branch profits distributed to non-resident alien entities or individuals was eliminated

by Act 1111, 2006

79 Tax Code, § 245.

80 Idem, § 48 y 49.

81 Tax Code, § 406.

82 Idem, § 408.

83 Idem.

84 Tax Code, § 418.

85 Tax Code, § 25.

86 Idem, § 418.

87 Tax Code, § 414.

88 The government must issue a tax havens list, which as of March 4, 2010 had not been issued.

89 Tax Code, § 124-2.

90 Idem.

91 Tax Code, § 122.

92 Idem.

93 Idem, § 254.

94 Congress approval, Act 1082-2006.

95 Congress approval, Act 1261-2008.

96 Currently, Bolivia, Colombia, Ecuador and Peru (Venezuela withdrew on April 22, 2006).

97 Act 15-1970.

98 Act 71-1993.

99 Act 6-1988.

100 Act 16-1970.

101 Act 14-1981.

102 Act 1265-2008.

103 Act 4-1988.

104 Act 16-1976.

105 Tax Code, § 468.

106 Tax Code, § 468-1 and 468-3.

107 Idem, § 471.

108 Idem, § 420.

109 Idem.

110 Act 21-1992, § 100. Act 30-1992, § 92.

111 Tax Code, § 437-2.

112 Idem, § 477 to 479 and § 481.

113 Idem, § 423, 423-1, 424, 424-2/5/6, 425, 427, 428 and 480.

114 Tax Code, § 489.

115 Idem, § 447 and 453.

116 Idem, § 448.

117 Idem, § 484.

118 Idem, § 491.

119 Qualified as such by the Ministry of Trade pursuant to a request filed by the importer.

120 i.e. mining, hydrocarbons, heavy chemistry, iron and steel industry, extracting metallurgy, electric generation and transmission,

obtaining purification and conduction of hydrogen oxygen.

121 Tax Code, § 428.

122 Idem, § 258-2.

123 Idem.

124 See note 167.

125 Decree 2532-2004, § 4.

126 Tax Code, § 600.

127 Decree 4680-2004, § 23.

128 Andean Pact Directive 599 of 2004.

129 Tax Code, § 292 and 293.

130 Idem, § 295.

131 Idem, § 296.

132 Tax Code, § 292.

133 Act 1370-2009

134 Idem, § 876.

135 Idem, § 871.

136 Idem, § 872.

137 Idem, § 879.

138 Act 14-1983, § 33.

139 Decree 352-2002, § 53.

140 Idem, § 36.

141 Technically Bogota is not a municipality, it is a different type of territorial entity but its tax regime structure shares many

of the characteristics of municipalities.

142 Bill of rights, § 317.

143 Act 44-1990, § 4.

144 Idem.

145 Idem, § 3.

146 Act 223-1995, § 226.

147 Idem, § 230.

148 Idem.

149 Decree 650-1996.

150 Idem.

151 A separate type of local territorial entity.

152 Bill of rights, § 300. Act 645-2001.

153 Bill of rights, § 360.

154 Act 100-1993, § 59.

155 Act 100-1993, § 20. Decree 4982-2007.

156 Decree 1406-1999, § 9.

157 Act 100-1993, § 20.

158 Idem.

159 Idem, § 22.

160 Idem, § 157 and 203.

161 Idem, § 204.

162 Idem.

163 Idem.

164 Idem, § 161. Decree 1406-1999, § 9.

165 Decree 1295-1994, § 4. Decreto 1772-1994, § 3.

166 Decree 1406-1999, § 9. Decreto 1772-1994, § 13.

167 Act 89-1989, § 1.

168 Act 21-1982, § 12.

169 Idem.

170 Act 21-1982, § 9 and 10. Act 89-1988, § 1.

171 Labour Code, § 249. Decree 663-1993, § 164.

172 Act 52-1975, § 1.

173 Tax Code, § 108. Act 7-1979, artcle 45.

174 Colombian Tax Code, §468.

175 Decree 4589-2006.

176 CAN, ALADI and Bilateral Agreements.

177 Colombian Tax Code, §459. Colombian Custom Code, §88.

178 Colombian Custom Code, §237; Resolution 4240-2000, §159.

179 Idem, §115.

180 Decree 3803-2006, §3.

181 Resolution 1512-2007.

182 Custom Code, §116.

183 Idem, §117.

184 Decree 3803-2006, §15.

185 Colombian Custom Code, §143.

186 Idem.

187 Idem, §150.

188 Idem, §153.

189 Idem, §144.

190 Idem, §§502 and 503.

191 Idem, §147.

192 Act 1004-2005; Colombian Custom Code, §392.

193 Colombian Tax Code, §240-1.

194 Colombia Custom Code, §394.

195 Resolution 1860-1999.

196 Decree 631-1985; Resolution 4240-2000.

197 Decree 2331-2001; Decree 2099-2008; Decree 2100-2008.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.