- within Immigration, Transport, Media, Telecoms, IT and Entertainment topic(s)

On 6 June 2017, the South African Revenue Service ("SARS") issued binding private ruling 274 ("BPR 274"). BPR 274 deals with a venture capital company ("VCC") investing in a company providing and expanding plants for the generation of solar electricity.

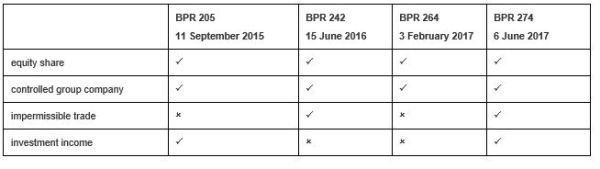

This brings the number of binding private rulings that SARS has issued in respect of venture capital companies to four. Below, we compare the rulings in this matter with prior rulings issued by SARS to determine whether there are any trends with regard to rulings issued by SARS in respect of venture capital companies.

Before dealing with these trends, we first set out the proposed transaction in BPR 274.

BPR 274 deals with two issues that have been a common feature in all the VCC-related rulings given thus far by SARS: equity share and controlled group company. The table below indicates that all four binding private rulings have considered the equity share and the controlled group company issue:

Controlled group company

The reason why many VCCs request a ruling from SARS on this issue, is that a VCC may not invest in a qualifying company if it is a controlled group company in relation to a group of companies. A controlled group company in relation to a group of companies, is where at least 70% of its shares are held by a controlling group company or by other controlled group companies within the group of companies.

The practical problem faced by VCCs occurs where they contribute 70% of the contributed tax capital to the qualifying company. If the qualifying company issues a commensurate amount of equity shares to the VCC, then the VCC becomes a controlled group company in relation to the qualifying company, as it will hold 70% of the equity shares in the qualifying company.

The mechanism that is used to overcome this problem, is for the qualifying company to issue different classes of shares. The VCC subscribes for a class of share with a high subscription price, for example, ZAR1 000 per share. The other investors subscribe for a class of share with a low subscription price, for example, ZAR10 per equity share.

As a result, the VCC contributes more of the contributed tax capital but acquires less of the equity shares. These rulings confirm that the test is the number of shares that the VCC holds in the qualifying company, not the VCC's economic interest (ie the value of those shares) in the qualifying company.

Equity share

The VCC that acquires higher-priced shares in the qualifying company would naturally want a preferential right to distributions from the qualifying company. This is why it is necessary that in all the VCC rulings issued by SARS, the applicants seek rulings that the shares are equity shares.

According to the Income Tax Act, 1962, an equity share is "any share in a company, excluding any share that, neither as respects dividends nor as respects returns of capital, carries any right to participate beyond a specified amount in a distribution."

It is only if there is a restriction placed on both returns of capital and dividends that a share will not qualify as an equity share and therefore, will not be a qualifying share under the VCC scheme.

What can be taken from the BPRs, is that an investor can contribute a disproportionate amount of share capital entitling the investor to a first distribution of profits or capital, in other words, the share is preferential in nature, yet it still remains an equity share.

Impermissible trade

A company cannot be classified as a qualifying company if it carries on an impermissible trade. Section 12J of the Income Tax Act lists a number of activities that are considered to be impermissible trades. The impermissible trade that BPR 274 deals with, is any trade carried on in respect of immovable property (other than a trade carried on as an hotel keeper).

BPR 274 deals with the business of conducting a solar facility at specific sites to its customer. The facilities provide for solar electricity. The difficulty with renewable energy facilities, is that they may be constructed in such a way that they accede to the land thereby, becoming immovable property. It was ruled that solar panels are movable assets, thus the qualifying company is not carrying on an impermissible trade.

Investment income

A VCC may not invest in a qualifying company that receives investment income that exceeds 20% of its gross income for a particular year of assessment. Investment income includes any income in the form of interest, dividends, foreign dividends, royalties, rental derived in respect of immovable property, annuities or income of a similar nature.

Since SARS ruled that the solar facilities are movable assets, it followed that the rental to be derived by the qualifying company is derived from movable property rather than immovable property. The investment income limitation is an important area that we feel will receive more attention particularly in light of the increase in the number of VCCs over the past three years.

For example, companies that license the use of intellectual property to others may be receiving royalty income that could result in them being ineligible to receive financing from venture capital companies if their royalty income exceeds the 20% investment income limitation.

Anuschka Wischnewski is a candidate attorney in ENSafrica's tax department.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]