- within Tax topic(s)

- in United States

- within Tax topic(s)

- in United States

As usual, like at the beginning of each year, Luxembourg VAT taxable persons received VAT account statements from the Luxembourg Treasury. For some of them, these statements show a negative amount which corresponds to a VAT credit towards the Luxembourg Treasury.

Such VAT credits are usually not refunded automatically within a short time frame and it is common to have to wait three to four years to get the reimbursement. Fortunately, the Luxembourg VAT law provides a mechanism to accelerate the VAT refund process and thereby optimise companies' cash flows.

In this Alert, we outline how businesses can enhance their cash flow by strengthening their VAT credit management practices.

- Which companies are usually in a VAT refundable position?

Any company with a full or partial VAT deduction right that incurs more input VAT on its expenses than output VAT on its turnover may be in a VAT refundable position. In the Private Equity, Fund Industry and Real Estate sectors, the following types of companies may be concerned:

- Financing companies with non EU borrowers their turnover and : these companies do not collect are often in a credit position Luxembourg due to the recoverable input VAT VAT on incurred on their overheads ;

- Property companies that hold and operate buildings located abroad, subject to foreign VAT on the rents;

- Companies registered under the simplified VAT regime (i.e. with no VAT deduction right) that have overpaid VAT. The "overpayments" may result from the payment of too large VAT advance payments made prior to the filing of the annual VAT return or from the receipt of a credit note related to a previous year where VAT was paid to the Treasury.

- Where can the VAT position of a company towards the VAT treasury be checked?

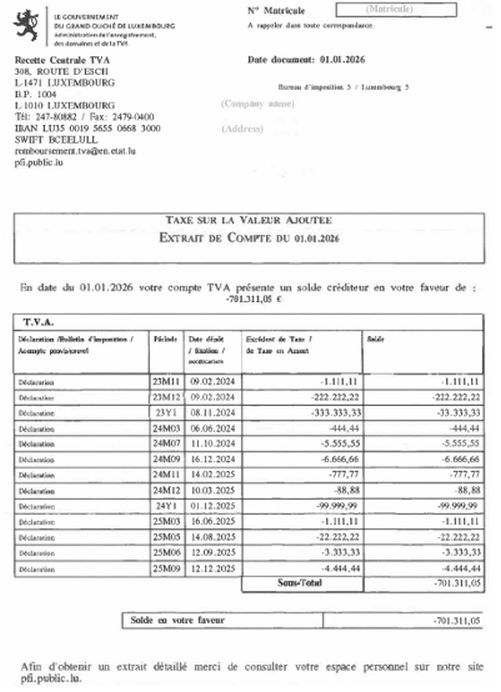

Every year in January, the Luxembourg Treasury sends VAT account statements ("Extraits de compte TVA") by postal mail to the registered address of most VAT-registered companies.

These documents indicate whether the taxable person is in a VAT credit position (negative amount) or a VAT payable position (positive amount) towards the Luxembourg Treasury.

If no recent VAT statement is available, it is still possible to download it on the eTVA portal.

VAT account statements are structured as follows:

- What happens if no action is taken after receiving the VAT account statement?

If a company is in a VAT receivable position, such VAT receivable is, in principle, carried forward and offset against subsequent VAT liabilities. VAT credit refunds are therefore neither immediate nor automatic.

The reimbursement of a VAT credit usually requires a (preliminary) review and assessment by the Luxembourg VAT authorities ("AEDT") of the annual VAT returns from which the credit originates. The AEDT is not subject to any specific deadline to perform this assessment, apart from the five-year statute of limitations.

In this context, the AEDT generally reviews an annual VAT return within three to four years after the filing of the return, before the prescription period expires. This delay has a negative cash-flow impact for companies in a VAT receivable position on an ongoing basis, as the corresponding VAT amount represents only a future receivable.

- What are the actions to be taken to speed up the refunds of the VAT credits?

The Luxembourg VAT law allows taxable persons to proactively request the refund of VAT credits. Once submitted, the AEDT has four months to notify its position on the VAT return(s) and thus to either approve or reject the related VAT refund request.

Following the filing of a refund request, questions from the AEDT can generally be expected regarding the nature and breakdown of the turnover, the expenses reported in the VAT returns, as well as the VAT deduction methodology used. It is quite logical to have the AEDT reviewing the positions taken in the VAT returns before proceeding to the reimbursement of the VAT credits. This means that taxable persons should anticipate receiving questions from the AEDT following the submission of the VAT refund request.

In almost all circumstances, similar questions would be raised by the AEDT in the case that no VAT refund was proactively requested. The main difference is related to the timing of these questions, usually received when the period of limitation is close.

- What are the advantages of filing VAT refund requests?

The submission of VAT refund requests and the receipt of the related VAT assessments from the AEDT following their review of the annual VAT returns offer several advantages:

- The reimbursement of the VAT credit

Once a VAT refund is granted, the company generally receives the cash in its bank account within a few weeks following the AEDT's decision. The VAT reimbursement also clears the VAT receivable and facilitates the preparation of the accounts as well as their review by auditors and management.

- Increased comfort regarding the content of the VAT returns

When the AEDT assesses annual VAT returns, the reviewed years are, in principle, considered as closed. Indeed, the AEDT's assessment confirms the amounts reported in the VAT returns and on the VAT deduction methodology used. If new facts or irregularities are discovered later, the AEDT may reopen an assessed year and initiate a new audit, although this situation is not frequent in practice.

- Increased comfort in case of due diligence

The assessment of annual VAT returns by the AEDT is particularly valuable in a due diligence context. It clearly demonstrates that the company has properly monitored its VAT affairs, which provides a significant level of comfort to a potential purchaser regarding the VAT returns filed and assessed by the AEDT.

Hence, this may facilitate negotiations in share deals, in particular regarding tax warranties in sale and purchase agreements.

- Smoother exchanges with the AEDT

If done systematically, regular VAT refund and assessment requests can facilitate communication with the AEDT and reduce the amount of information they request when assessing subsequent years. This allows the AEDT to develop a better understanding and monitoring of the development of the business.

- How to move on with a VAT refund request?

Requesting a VAT refund in Luxembourg is a straightforward process that requires companies to:

- Obtain a recent VAT account statement;

- Send a registered letter to the Recette Centrale requesting the refund of the VAT credit; Anticipate potential questions to be received from the VAT office in charge of the company;

- Consider implementing a recurring refund-request process for companies in an ongoing VAT receivable position. Such decision to request refunds is done on a company-by-company basis but could be contemplated as a group policy.

A 30-minute webinar during which we will briefly explain the VAT refund process and share practical insights and concrete examples will be scheduled on Thursday, 26 March 2026. Participants will then have the opportunity to request a dedicated meeting or Teams discussion to raise their questions and discuss any challenges they encounter in practice regarding VAT refund

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.