As detailed in our other ESG briefings, with the aim of furthering sustainable finance and ESG integration, the European Commission (the "Commission") introduced a package of legislative measures in 2018 that includes three key Regulations: the Taxonomy Regulation, the Disclosures Regulation, and the Low Carbon and Positive Impacts Benchmarks Regulation. The underlying impact assessment to this legislative package also demonstrated that it was necessary to make clear that UCITS management companies (including self-managed UCITS) and AIFMs (together "Management Companies") should take sustainability risks and factors into account as part of their duties towards investors. Accordingly, Management Companies should be assessing not only all relevant financial risks on an ongoing basis, but also all relevant sustainability risks. In addition, their internal processes, systems and controls should also reflect these risks. Therefore, following the publication of its legislative package, the Commission requested ESMA to provide technical advice on integrating sustainability risks and factors into both the AIFMD and the UCITS Directive.

ESMA delivered its final report to the Commission in April 2019, recommending that its proposals should be implemented using a principles-based approach and having regard to the nature, scale and complexity of the relevant entity and its activities. Based on this technical advice, the Commission subsequently published on 8 June 2020 the draft texts of the delegated regulation and delegated directive to integrate sustainability risks and factors into the AIFMD and the UCITS legislative frameworks. The Commission conducted a short consultation on this draft legislation, which closed on 6 July 2020.

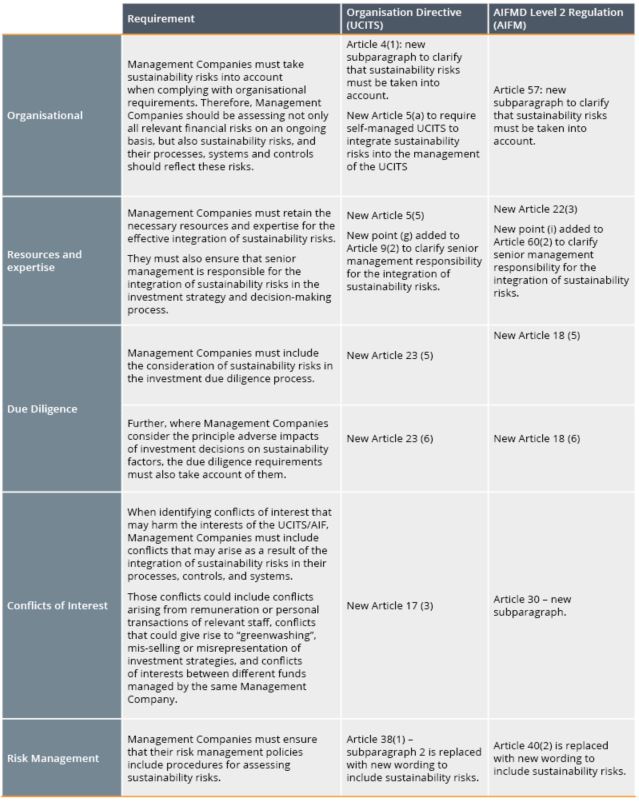

Once adopted, the delegated acts will amend the UCITS Organisation Directive and the AIFMD Level 2 Regulation, respectively, and will introduce requirements to integrate sustainability risks and factors in compliance with existing rules in three key areas: organisational requirements; operational requirements; and risk management.

The key requirements and corresponding legislative amendments are set out below:

Definitions

- "sustainability risk" and "sustainability factors" as defined according to the Disclosures Regulation.

- "sustainability risk" means

an environmental, social or governance event or condition that, if

it occurs, could cause an actual or a potential material negative

impact on the value

of the investment; - "sustainability factors" mean environmental, social and employee matters, respect for human rights, anti-corruption and anti-bribery matters.

Next Steps

The next steps are for the delegated acts to be formally adopted by the Commission and published in the Official Journal of the EU ("OJ"). The delegated acts will enter into force on the day following their publication in the OJ and will apply 12 months later. The delegated regulation amending the AIFMD Level 2 Regulation is directly effective, however the delegated directive amending the UCITS Organisation Directive will have to be transposed into national law.

Although the exact timing remains uncertain, it is likely that these measures will apply in late Q3 2020 or early Q4 2021. Management Companies should now be preparing to comply with the requirements by reviewing their:

- organisational requirements;

- senior management and board-level expertise;

- risk framework and risk management policies;

- due diligence policies; and

- conflicts of interest policies.

This article contains a general summary of developments and is not a complete or definitive statement of the law. Specific legal advice should be obtained where appropriate.