A detailed SOP for initiating scrutiny of GST returns for FY 2017-18 and FY 2018-19 vide Instruction No. 02/2022-GST dated 22 March 2022 has been issued by the Central Board of Indirect Tax and Customs (CBIC) to the officers of Central GST. This SOP is issued as an interim measure in order to ensure uniformity in the selection/ identification of returns for scrutiny, methodology of scrutiny of such returns and other related procedures. This SOP would be resorted until the time a Scrutiny Module for online scrutiny of returns is made available on the CBIC-GST application and would be applicable for the selection of GSTINs falling under center jurisdiction. We have summarized the SOP for easy understanding:

- SOP is based on the relevant statutory provisions, i.e.,

Section 61 of the CGST Act 2017 read with Rule 99 of the CGST Rules

2017, which provide the powers to the proper officers to scrutinize

the returns. Furthermore, the SOP also indicates that:

- The information could be made available for scrutiny from sources like the Directorate General of Analytics and Risk Management (DGARM), Advanced Analytics in Indirect Taxation (ADVAIT), GSTN, E-Way Bill Portal, etc.

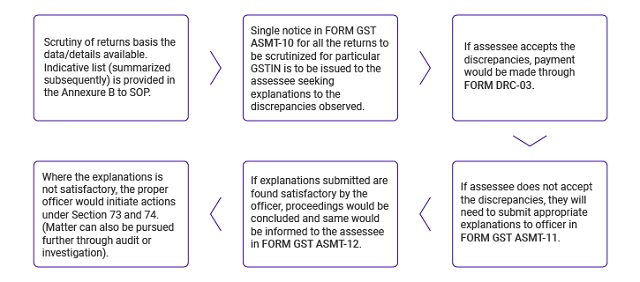

- On verification and detailed scrutiny, discrepancies shall be communicated to the taxpayer, if any, seeking explanations.

- The taxpayer will be granted an opportunity to be heard. Post this opportunity, if the liability is accepted and paid by the taxpayer or acceptable explanations are provided by the taxpayer- the proceedings shall be concluded.

- In case of non-compliance, appropriate actions shall be initiated in accordance with Section 65 or 66 or 67 and Section 73 or 74 of CGST Act 2017.

- As per the SOP, selection of GSTINs would be based on specific risk parameters and this activity has been assigned to DGARM and they shall then communicate such selection to the nodal officer of the concerned Commissionerate along with the relevant data and likely revenue implication pertaining to the returns to be scrutinized through the DDM portal.

- Superintendent of Central Tax is assigned the function as the 'proper officer' for the scrutiny shall vide Circular No. 3/3/2017 - GST dated 5 July 2017 who shall prepare a monthly scrutiny schedule with the approval of divisional Assistant/ Deputy Commissioner for the selected GSTIN.

- The GSTIN, which seems riskier based on the likely revenue implication indicated by the DGARM, may be prioritized. Such scrutiny schedule shall be shared with the Directorate General of Goods and Services Tax (DGGST) in the prescribed format. Scrutiny of the complete financial year for a minimum 3 GSTINs per month would have to be conducted by each proper officer.

- The process for carrying out the scrutiny would be as mentioned

below:

- Timelines for each step from communicating list by DGARM to the concluding of scrutiny has been prescribed in Paragraph 7 of the SOP, to ensure that necessary action to safeguard revenue may be taken up expeditiously. The proper officers are required to conclude the scrutiny within the timelines prescribed.

- A 'scrutiny register' shall be maintained by the proper officer in respect of the GSTINs allotted for scrutiny in Annexure C and each Commissionerate shall share the consolidated progress report of the scrutiny to DGGST by the 10th of the succeeding month, who in turn shall present to the board by 20th of the corresponding month.

- Any communication with the taxpayer for the purpose of scrutiny

shall be made with the use of DIN as per the guidelines mentioned

in Circular No. 122/41/2019-GST dated

5 November 2019.

Below is the summary of the indicative list of parameters for Scrutiny as carved out in Annexure B of SOP:

Sr. No. Source Parameter to be Scrutinized 1. Outward Tax Liability - Difference between the tax liability as per GSTR-1 vis-à-vis GSTR-3B

- Outward taxable value disclosed in GSTR-3B vis-à-vis amount reflected under TDS/TCS Table GSTR-2A.

- Tax liability disclosed in GSTR-3B vis-à-vis amount reflected in E-Way bill data

2. Tax Liability under RCM - RCM Liability paid to be verified with

- Corresponding credit availment

- With corresponding entries reflected in GSTR-2A

- Cash payment in GSTR-3B

3. Credit Availment and Reversal - Credit passed through ISD vis-à-vis credit reflected in GSTR- 2A.

- Amount of credit availed in GSTR-3B (All other ITC/ Import of goods) vis-à-vis amount reflected in relevant tables of GSTR-2A.

- Claim of credit in respect of supplies from taxpayers whose registrations have been canceled retrospectively shall be ineligible. The effective date of cancellation of registrations of the suppliers, if any, is made available in the relevant tables of GSTR-2A.

- Ineligible ITC availed in respect of invoices/debit notes issued by the suppliers who have not filed their GSTR-3B returns for the relevant tax period.

- Credit is not to be allowed if GSTR-3B of a tax period is filed after the last date of availment of ITC in respect of any invoice/debit note as per Section 16(4).

- Whether the assessee has made reversals of ITC in accordance with provisions of Rule 42 and Rule 43 of the CGST Rules, if applicable.

4. Interest and Late Fees - Whether the assesse has paid interest liability in terms of section 50 or late fee in terms of Section 47 in respect of returns/ statements.

|

Our Comments It is a welcome move from the CBIC to implement a uniform procedure and publish the SOPs in the public domain. This would act as an enabler for the assesse to initiate a review at their end before the formal scrutiny is undertaken. Furthermore, this move will also prevent the unnecessary harassment of the assessee from the department and make the verification process to be more fruitful. Generally, the States will follow the same Rules, however, we look up to having similar instructions to be made available to the State jurisdiction GSTIN on uniform grounds. As a way forward, we suggest the companies should carry on an internal review mechanism for all the parameters for the historic transactions, specific inclusion of reconciliations between the base documents and the returns filed, including the ancillary activities like E-way bill, TDS/TCS data etc. Furthermore, implementing a regular check and control on every transaction going forward would be beneficial for the companies. |

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]