DIRECT TAXATION

RECENT CASE LAWS

Amount received for providing software-access to EY network firms not taxable as royalty

EY Global Services Limited (W.P.No. 11957 of 2016) and EYGBS (India) Private Limited (W.P.No. 12003 of 2016) (Delhi HC)

- The taxpayer, a UK-based company, is engaged in providing technology, other support services and software licenses to its member firms in countries all over the world. The taxpayer entered into an agreement with its Indian member firm (EYGBS), engaged in providing back-office support and data processing services, for 'right to benefit from the deliverables and/or services'.

- Both, the taxpayer and EYGBS moved applications before Authority of Advance Ruling (AAR) over taxability of services and software payments provided under the agreement. The AAR held that services provided under the agreement were not taxable as Fees for Technical Services (FTS). The consideration, however, received for software was taxable as royalty and would be liable to Tax Deducted at Source (TDS) under Section 195 of the Income Tax Act, 1961 (IT Act).

- Following this, the taxpayer and EYGBS filed a writ petition before the Delhi High Court (HC) and submitted that the case was covered by the Supreme Court (SC) ruling in Engineering Analysis Centre of Excellence Private Limited [Civil (Appeal) 8733-8734 of 2018 (SC)] (EAC). On the other hand, the Income Tax Department (ITD) submitted that, as per the agreement, a standard facility was created under a license from the third-party vendors which was used by all entities, where the owner of the computer program lawfully enabled the use of the confidential information contained therein. This makes the transaction taxable as royalty under India-UK DTAA.

- The Delhi HC followed the SC ruling in EAC and held that

payment received by the taxpayer for providing access to computer

software to its member firms in India does not amount to royalty

under the domestic law as well as India-UK DTAA on the following

grounds:

- For taxing the payment received by the taxpayer from EYGBS as royalty, it is essential to show a transfer of copyright in the software to do any of the acts mentioned in Section 14 of the Copyright Act, 1957 and a license conferring no proprietary interest on the licensee, does not entail parting with the copyright.

- Where the core of a transaction is to authorize the end-user to have access to and make use of the licensed software over which the licensee has no exclusive rights, no copyright is parted with and therefore, the payment received cannot be termed as 'royalty'.

- EYGBS merely received the right to use the software procured by the taxpayer from third-party vendors which cannot be taxed as royalty.

ELP Comments:

The Delhi High Court categorically observed that the scope of the Supreme Court judgement in EAC is not restricted to the four categories of facts discussed in the judgement and it goes beyond to cover cases where there is a 'transfer of a right to use the copyright in software' without there being a 'transfer of copyright in the software'.

Section 197 application to be decided in 2 weeks, on transaction covered by EAC

Alcatel Lucent International (W.P.No. 14075 of 2021) (Delhi HC)

- Taxpayer, a foreign company, preferred an application under Section 197 of the IT Act on August 30, 2021 for the grant of Nil deduction certificate regarding payments made for supply of hardware equipment embedded with software pertaining for the period from 1 October 2021 to 31 March 2022. However, there was an inordinate delay in disposing off the application by the jurisdictional Assessing Officer (AO).

- Aggrieved by the inaction on the part of the AO, the Taxpayer filed a writ petition before the Delhi HC for expeditious disposal of its application and made the following contentions:

- Failing to dispose of the application for more than three months is in direct contravention of the CBDT Instruction No. 01/2014 dated January 15, 2014 read with CBDT Citizen's Charter, 2014 which prescribes a time limit of one month to the jurisdictional AO for applications made under Section 197 of the Act.

- There was no valid reason for an inordinate delay since the transaction under the application was squarely covered in Taxpayer's favour by the coordinate bench ruling in Ericsson AB which was upheld by the Hon'ble Supreme Court in EAC.

- The transaction was also covered by the orders of different fora in THE Taxpayer's own case.

- Based on this, the AO should have disposed of the Taxpayer's application under Section 197 of IT Act by 30 September 2021. In view of the above, the Delhi HC directed the AO to dispose of the application under Section 197 preferred by the Taxpayer by passing a reasoned order within two weeks.

ELP Comments:

The Citizen's Charter lists down the service delivery standards i.e., the timelines for completion of key services provided by the Department. These timelines are required to be adhered to by department to avoid unnecessary delays and ensure expeditious disposal of applications by taxpayers.

Fees for 'using' IT Infrastructure taxable as Royalty; Transaction not covered by EAC ruling

Bekaert Industries Private Limited (ITA No. 1003/PUN/2017) (Pune ITAT)

- Taxpayer, a Company, paid IT support service fees to N.V. Bekaert SA, its Belgian associate enterprise (AE) for AY 2012-13. However, the AO disallowed the expenditure on account of failure to deduct TDS.

- On appeal, the Pune ITAT, noting the pricing mechanism, observed that the costs incurred by the AE in setting up and maintaining the IT Infrastructure facility had been allocated to group entities with a mark-up. Thus, the payment made by the taxpayer to its AE, being its share in the total costs, was for the use of the IT Infrastructure facility set up by the latter and not for availing any particular IT service from its AE.

- Further, the Pune ITAT held that the IT infrastructure set up by the AE was in the nature of equipment covered Explanation 2 to Section 9(1)(vi) (iva) and thus, it falls within the ambit of 'Royalty' under Section 9(1)(vi).

- As regards taxability under the DTAA, Pune ITAT referred to Article 12(3)(a) of India-Belgium DTAA and stated that there is no material difference in the definition of the term `Royalty' under Section 9(1)(vi) of the Act. The DTAA insofar as clause (iva) of Explanation 2 deals with payment of consideration for use or right to use of any industrial, commercial or scientific equipment.

- Thus, the Pune ITAT held that payment made by the taxpayer to its AE for using the IT Infrastructure facility set up by the AE falls within the ambit of royalty under Section 9(1)(vi). Also, under Article 12 of India-Belgium DTAA confirmed the disallowance under Section 40(a)(i) for default in deducting TDS on such transaction.

- Further, the Pune ITAT rejected the taxpayer's submission that since the department applied Karnataka HC ruling in Samsung Electronics Company Ltd. 345 ITR 494 (Kar.) overruled by SC in EAC, Pune ITAT could not view the transaction from a different angle. The ITAT observed that the SC ruling in EAC applies only on copyright royalty cases and not on industrial royalty cases. Thus, the transaction of availing access to the IT Infrastructure facility set up by its AE, is

ELP Comments:

For relying on the decision of SC in case of EAC, it is pertinent to take note of factors like the agreement language, nature of service/ license provided, the language used in the DTAA and the nature of royalty in question.

10% TDS on Coursera's receipts unreasonable, since transaction subjected to 2% EL; Directs for reasoned order as per Section 10(50)

Coursera INC (W.P.No. 46330-31 of 2021) (Delhi HC)

- Taxpayer, a company, is a US tax-resident and an e-platform operator, acting as an aggregator of educational institutions and providing access to various courses. The taxpayer filed an application under Section 197 of the IT Act before the AO for NIL deduction of TDS in respect of its receipts for FY 2021-22. The said application was rejected whereby the AO directed the customers of the Taxpayer to withhold tax @ 10% without giving reasons for arriving at such rate

- On the filing of the writ petition, the Delhi HC observed the

following regarding the Order passed by the AO under Section 197:

- The impugned order noted, "the receipts from Indian customers are not chargeable to tax as royalty/ FTS under the provisions of the Act read with India US tax treaty and since assessee has been suo moto paying equalization levy @ 2% on receipts from Indian customer...such receipts may be subjected to TDS under section 195 of the Act @ 4% keeping in the interest of Revenue",

- Further, there was no reasoning as to how the rate finally granted had been arrived at.

- The impugned order also did not take into account the impact of the amendment carried out in Section 10(50) by Finance Act, 2021 w.e.f. April 1, 2021 whereby the amounts taxable as royalty/fees for technical services under the Act read with Section 90/90A and the relevant DTAA would not be considered for the charge of Equalization Levy.

- Although the AO held that Taxpayer is not eligible for benefit under Article 12(5)(c) of the India-US DTAA, the order did not contain any reasoning or discussion on the applicability or otherwise of various sub-articles of the DTAA to the facts of the case.

- Based on the above observation, the Delhi HC, without delving into merits of the case, set aside the order under Section 197 directing TDS @ 10% on the taxpayer's receipts in India. It directed the AO to pass a de novo order excluding the receipts already subjected to Equalization Levy in the light of Section 10(50).

ELP Comments:

The newly inserted Section 10(50) of the IT Act excludes income chargeable to Equalisation Levy from the scope of total income. Subjecting an amount to TDS which has already been subjected to Equalisation Levy would result into double taxation. It is for this purpose that the Section 10(50) was inserted in the IT Act.

Educational cess held not deductible under Section 40(a)(ii)

Kanoria Chemicals & Industries Ltd (ITA No. 2184/Kol/2018) (Kolkata ITAT)

- Recently, the ITAT held that education cess is not deductible under Section 40(a)(ii) of the IT Act. The ITAT perused the provisions of the Finance Act, 2004 and Finance Act, 2011 and observed that it has been specifically provided that 'education cess' is an additional surcharge levied on the income-tax.

- As per the provisions of Section 40(a)(ii) of the IT Act, 'any rate or tax levied' on profits and gains of business or profession shall not be deducted in computing the income chargeable under the head profits and gains from business or profession.

- The taxpayer relied upon CBDT Circular No. 91/58/66-ITJ(19) dated May 18, 1967, wherein it has been interpreted that 'Cess' shall not be disallowable. Further, the taxpayer placed reliance on the decision of the Hon'ble Bombay HC in Sesa Goa Limited v. JCIT (2020) (117 taxmann.com 96) and decision of the Hon'ble Rajasthan HC in Chambal Fertilizers & Chemicals Ltd v. JCIT (ITA No. 52/2018) wherein the High Courts relying on the aforesaid CBDT circular allowed claim of deduction of education cess.

- The ITAT took note of the provisions of the Finance Act, 2004 and Finance Act, 2011 wherein education cess was mentioned as an additional surcharge to finance the Government's commitment to universalize quality basic education. The ITAT also took note of the decision of the Hon'ble SC of India in CIT v. K. Srinivasan (1972) (83 ITR 346) wherein it was held that surcharge and additional surcharge are part of the income-tax.

- Further, the ITAT remarked that the decision of the Hon'ble SC of India and the provisions of Finance Act, 2004 and Finance Act, 2011 were not brought to the knowledge of the two High Courts.

- In view of the above, since decision of the Hon'ble SC prevails over that of the High Courts, the ITAT respectfully followed the decision of the Hon'ble SC (supra) and held that education cess is not deductible under Section 40(a)(ii) of the IT Act.

ELP Comments:

The issue regarding deduction of education cess under Section 40(a)(ii) of the IT Act has been a subject matter of litigation over the years with various appellate authorities passing divergent rulings. The aforesaid decision of the ITAT has been contrary to the favourable decision in Sesa Goa Limited and Chambal Fertilizers & Chemicals Ltd (Supra). Further, it may be noted that a special leave petition has been filed before the Hon'ble SC in the case of Chambal Fertilizers & Chemicals Ltd (Supra) which is currently pending before the Hon'ble SC.

Legal fees paid to foreign attorney not chargeable to tax as FTS

Chander Mohan Lall (ITA No. 1869/Del/2019)

- The taxpayer had claimed deduction of payment to various persons/entities outside India towards legal/ professional fee and no tax was deducted on the same. The Tax Officer (TO) disallowed the said deduction under Section 40(a)(i) of the IT Act for non-deduction of tax at source.

- The ITAT observed that certain payments were made towards court and application fees which were in the nature of reimbursement made for official purpose and the same cannot come within the purview of either professional or technical services. Accordingly, the ITAT held that for such payments there was no obligation on the taxpayer to deduct tax at source.

- The ITAT took note of the nature of professional services rendered by the non-resident attorneys outside India and observed that the payments received by them cannot be treated as income received in India, or deemed to be received in India, or income which accrues or arises in India. Accordingly, the ITAT stated that the only category under which the payments can be chargeable to tax is income deemed to accrue or arise in India.

- On an examination of the various provisions of the IT Act, the ITAT observed that the domestic law provisions recognize legal/professional services and FTS as two distinct and separate categories. Therefore, payments made to non-resident attorneys cannot be regarded as FTS under Section 9(1)(vii) of the IT Act.

- Further, the ITAT observed that Section 40(a)(ia) encompasses both, FTS and fees for professional services, however, Section 40(a)(i) of the IT Act is applicable only in case of failure to deduct tax on payments made for FTS. In view of the same, the ITAT noted that payment of legal/professional fee to a non-resident does not accrue or arise in India or is not deemed to accrue or arise in India as per Section 5 and Section 9 of the IT Act.

- The ITAT relied on its coordinate bench ruling in NQA Quality Systems Registrar Ltd. v. DCIT (92 TTJ 946), wherein it was held that professional services are a category distinct from technical services and held that payments made to non-resident attorneys being not in the nature of FTS, there was no obligation on the taxpayer to deduct tax at source.

Proportionate tax credit under Section 90 of the IT Act on overseas income offered to tax in India allowed

Harish N. Salve (ITA No. 7356/Del./2018) (Delhi ITAT)

- Taxpayer, an individual, declared income of INR 93.40 crore for AY 2015-16. Taxpayer had also claimed credit under Section 90 amounting to INR 8.57 crore for taxes paid in UK. However, TO disallowed the said foreign tax credit. Further, CIT(A) dismissed taxpayer's appeal for allowing the foreign tax credit.

- Being aggrieved by the order of CIT(A), the taxpayer filed an appeal before ITAT. Before the ITAT, taxpayer submitted that the income was offered to tax in UK and tax was withheld on the same out of which INR 8.57 crore corresponded to income offered to tax in India. Further, as the entire amount withheld in UK was not available for set off in India, taxpayer claimed proportionate foreign tax credit as per Section 90 of the IT Act.

- ITAT observes that it is an undisputed fact that the overseas income earned by the taxpayer in UK had been offered to tax in India whereby the corresponding amount of income had already been offered to tax in India and accepted by the TO. The credit of the taxes paid on such income deserves to be allowed.

- Accordingly, ITAT restores the issue with a direction for TO to allow the credit of foreign taxes.

Difference between consideration and stamp duty value on invoking Section 50C of the IT Act, cannot be attributed to gift

Rajeev Suresh Ghai (ITA No. 6290/Mum/2019)

- Taxpayer, an individual, jointly owned a property (50%) along with his wife. Taxpayer sold the property to his relative i.e. his wife's brother for INR 59 lakhs, his share INR 29.50 lakhs. TO invoked provisions of Section 50C and held that stamp duty value (SDV) of the property amounting to INR 89.27 lakhs must be adopted as the sales consideration for calculating capital gains.

- On appeal before CIT(A), taxpayer contended that the difference between the sale consideration and SDV should be treated as gift to relative as per Explanation (e) to Section 56(2)(vii) of the IT Act. However, CIT(A) disregarded taxpayer's contention and referred the matter to Department Valuation Officer (DVO), who determined that value of the property at INR 70.54 lakhs resulting in the taxpayer's share at INR 35.27 lakhs. Further, CIT(A) also noted that no gift deed was made at the time of sale and also nowhere in the sale deed it was mentioned that the difference in the sale consideration and the SDV will be treated as gift.

- Aggrieved by the said order, taxpayer filed an appeal before ITAT. On perusal of Section 50C of the IT Act, ITAT notes that there is no scope for making any adjustment for the gift while determining the full value of consideration under the deeming provisions of Section 50C. Accordingly, ITAT dismissed taxpayer's appeal for applying Section 56(2)(vii) to the excess of stamp duty valuation.

NOTIFICATION/CIRCULARS

| S.No. | Reference | Particulars |

| 1. | Circular No. 20 of 2021 | CBDT vide Circular No. 20 of 2021 has issued guidelines on the scope of Section 194-O, Section 194Q and Section 206C of the IT Act. Among the many clarifications, the Circular clarifies that in case of purchase of goods which are not covered within the purview of GST, when tax is deducted at the time of credit of amount and the component of VAT/Sales tax/Excise duty/CST is indicated separately in the invoice, tax is to be deducted under Section 194Q on the amount credited without including such VAT/Excise duty/Sales tax/CST and in case the tax is deducted on payment, then tax is to be deducted on the whole amount as it will not be possible to identify the payment with VAT/Excise duty/Sales tax/CST component. |

| 2. | CBDT vide order dated December 16, 2021 | CBDT, vide Order dated December 16, 2021 has modified its earlier order (regarding extension from faceless assessments), and directed transfer of all cases, except the cases of International Taxation to the Central Charges where assessment proceedings are pending/initiated pursuant to survey u/s 133A or where survey is conducted in the course of the assessment proceedings. |

NEWS

- The European Union (EU) adopted a public Country-by-Country Reporting applicable to multinational companies and their subsidiaries whose revenue exceeds the CbCR threshold of EUR 750 million. Such entities/groups would be required to report certain information on activities, revenues, number of employees, tax paid etc., and the same would be accessible to the public free of charge in one of the official EU languages. It has also been provided that if a similar report on income tax information is prepared by the non-EU business and meets specified conditions, no reporting obligation will apply to EU subsidiaries and branches of non-EU companies.

- The Organization for Economic Co-operation and Development (OECD) published Pillar Two Model Rules for domestic implementation of 15% global minimum tax from 2023. These rules define the scope and set out the mechanism for the Global Anti-Base Erosion (GloBE) Rules under Pillar Two and will assist countries to bring the GloBE rules into domestic legislation in 2022 and provide for a coordinated system of interlocking rules.

RECENT CASE LAWS

Taxability of intercharge fee by issuing bank in pre-GST regime

Commissioner of GST and C. Ex. v. M/s. Citibank N.A. [TS-542-SC-2021-ST]

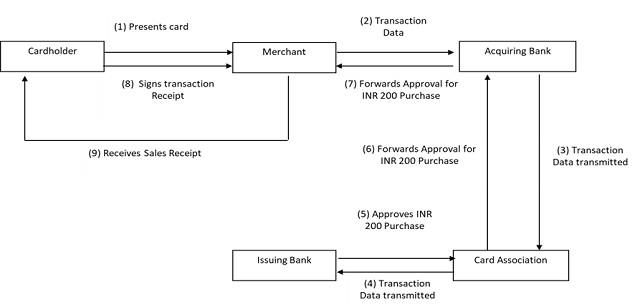

FACTS OF THE CASE

- The assessee is a bank and had received intercharge fees which

is a fee earned by credit card issuing banks while participating in

a credit card transaction. The manner in which a credit card

purchase transaction occurs is diagrammatically described

below:

- The parties enabling this transaction are:

- The issuing bank (IB) – Issues the credit card, thereby extends credit to the customer. Earns interchange fee in the process, which is part of the Merchant Discount Fee (MDF) deducted by the acquiring bank while paying the merchant.

- The acquiring bank (AB) – The merchant's bank, provides the point-of-sale machine (POS) enabling the merchant to acquire business and charges MDF, which includes the element of interchange fees.

- The Card Association/Network, such as Visa, Mastercard etc. which operates the digital system on which credit card settlement takes place.

- Card Holders - The card holder is the customer to whom the IB issues a credit card and who purchases goods at the merchant establishment using credit card.

- erchant Establishment - The merchant sells goods or services to card holders (buyers). The merchant is provided with POS machines by the AB to enable it to accept card payments, for a fee called MDF which is pre-agreed and deducted at the time of settlement of the transactions.

- The manner of settlement of card transactions and Service tax

charged thereon is illustrated as under:

- Card holder swipes card at POS for purchase of goods worth INR 200

- Card Association/Network initiates settlement process

- IB retains intercharge fee of INR 4 and transfers INR 196 to AB

- AB retains INR 6 as consideration for its services. AB pays Service tax (say at the rate of 14%) on total MDF of INR 10 (INR 6 + INR 4 retained by IB) and transfers balance INR 188.6 to Merchant establishment.

- AB pays Service tax of INR 1.4 to Government treasury

- Card holder pays Rs. 200 to IB

ISSUE

- The issue before the Hon'ble Supreme Court was whether the interchange fees earned by the IB is liable to be separately taxed as 'Credit card, debit card, charge card or other payment card service' (CCS) under Section 65(33a) read with Section 65(105)(zzzw) of the Finance Act, 1994 (Finance Act) for the period October 2007 to March 2015.

JUDGEMENT (POINTS OF CONSENT)

- Intercharge fee constitutes consideration for settling of card payments and would attract Service tax. The service falls within the scope of CCS under Section 65(33a)(iii) of the Finance Act during the period prior to 01.07.2012 and would constitute "service" under Section 65B(44) of the Finance Act thereafter.

- The reasoning in the Tribunal's order in ABN Amro's case was unsustainable.

- Interchange fees is not akin to interest on loan.

- Once tax is already paid on interchange fees by the AB, it cannot once again be collected from the IB since that would lead to double taxation.

JUDGEMENT (POINTS OF DISSENT)

| Issue | View of Hon'ble Justice Joseph | View of Hon'ble Justice Bhat |

| Unified/separate service | Interchange fee is consideration for an independent service of CCS provided by IB | Service provided by IB was a part of a single unified service of settling transactions provided by both AB and IB |

| Machinery provisions | IB is liable to discharge Service tax on intercharge fee and file return including the said fee | IB is not required to pay Service tax on intercharge fee as it is a part of single service provided by AB and IB |

ELP Comments:

- Thus, both judges have given dissenting views on the taxability of intercharge fees and the issue may be finally decided by a third member / larger bench of the Supreme Court.

- However, it is also equally important to note that both judges have held that double taxation must be avoided. Thus, Service tax would not be payable on interchange fees, provided it can be demonstrated with cogent evidence that AB have discharged Service tax on entire MDF, including interchange fees.

Time limit for filing appeal to be reckoned from date of communication

Meritas Hotels Pvt. Ltd. Vs. State of Maharashtra [TS-675-HC(BOM)-2021-GST]

FACTS OF THE CASE

- There was a delay on part of the Petitioner in filing Goods and Services Tax (GST) returns for the month of February 2019 on account of a financial crunch. The same was filed by the Petitioner on June 14, 2019. In the meanwhile, a notice dated March 26, 2019 was issued to the Petitioner for non-filing of return for February 2019.

- Thereafter, an assessment order dated 20.04.2019 was issued in Form GST ASMT-13 under Section 62 of the Central Goods and Services Tax Act, 2017 (CGST Act) for fixing the liability of tax amount along with applicable interest and penalty. The said order was not uploaded on GST portal but the scanned copy of the order was sent to the General Manager of the Petitioner Company vide email dated April 20, 2019. However, the General Manager failed to inform the management which became aware of the assessment order on July 1, 2019 after the bank account of the Petitioner Company was attached on July 1, 2019.

- Subsequently, the Petitioner obtained the certified true copy of the assessment order on November 6, 2019 and being aggrieved attempted to file an appeal manually on November 20, 2019. The said order was uploaded on the portal on January 8, 2020 and pursuant thereto, the Petitioner again made an attempt to file the appeal online on January 10, 2020 but the appeals were not entertained owing to delay in filing appeal. Hence the Writ Petition.

- The Petitioner inter alia argued that the period of three months for presenting appeal under Section 107 shall be computed from January 8, 2020 as prior thereto, the physical true copy of the assessment order was not served on the Petitioner nor the same was uploaded on the GSTN portal. Thus, refusal to accept and entertain the appeal on the ground of delay in filing thereof is unjustified.

ISSUE

- Whether the period of limitation for the purpose of filing an appeal under Section 107(1) of the said CGST Act would commence from the date when the impugned assessment order is uploaded on the GSTN portal or from the date of service upon the General Manager of the Petitioner Company vide email dated April 20, 2019.

JUDGEMENT

- The Hon'ble High Court inter alia held that in terms of Section 107 of the CGST Act, an appeal to the appellate authority has to be filed within three months from the date of communication of the impugned assessment order. In the present case, the order was communicated to General Manager vide email dated April 20, 2019 and the failure on the part of the General Manager to inform the Petitioner Company regarding receipt of the order would not have the effect of extending the period of limitation prescribed under Section 107(1) of the CGST Act.

- Further, referring to Rule 108 of the CGST Rules, the Hon'ble Court held that while Rule 108 prescribes that an appeal has to be filed electronically, it nowhere prescribes that the appeal is to be filed only after assessment order is uploaded on GSTN portal online.

- The Hon'ble High Court relying on various judgements including the case of Assistant Commissioner (CT) LTU, Kakinada Vs. Glaxo Smith Kline Consumer Health Care Limited 2020 SCC OnLine SC 440 inter alia held that as the Petitioner failed to avail of the remedy for filing of an appeal within the period prescribed under Section 107 of the CGST Act, the appeal was rightly not accepted and entertained by the appellate authority.

GST offences not grave enough to demand custodial interrogation

Tarun Jain vs. Directorate General of GST Intelligence DGGI [TS-645-HC(DEL)-2021-GST]

FACTS OF THE CASE

- The Petitioner is one of the directors in M/S Jetibai Grandsons Services India Pvt. Ltd. (Company). The Respondent alleged that the Company made most of its purchases from three firms which further received these goods from various firms, most of which have been found to be non-existent and had no inward supplies. The Respondent therefore alleged that the Company along with these three firms was involved in fraudulently availing and passing on ineligible/fake Input tax credit.

- Numerous summons were issued to the Petitioner. On apprehending arrest, the Petitioner filed an application for anticipatory bail before Court of Additional Sessions Judge, Patiala House Court, New Delhi which rejected the said application vide order dated 09.10.2021. Being aggrieved, the Petitioner approached the Hon'ble High Court.

JUDGEMENT

- The Hon'ble High Court noted that the maximum penalty imposable for committing offences under Section 132(1)(b) and (c) is imprisonment for a term which may extend to five years and with fine. Further, as per Section 132(5), the offences specified in clause (a) or (b) or (c) or (d) of Section 132(1) and punishable under Section 132(1)(i) are cognizable and non-bailable. The Hon'ble Court also stated that Section 138 of the CGST Act further dilutes the heinousness of offences under the CGST Act and makes every offence under the CGST Act compoundable except for certain circumstances specified under the proviso of Section 138.

- The Hon'ble Court observed that there is no embargo under the CGST Act restraining the Petitioner from seeking pre-arrest bail. The Court noted that economic offences are considered grave in nature and to deter persons from indulging in such offences, criminal sanctions such as arrest are imposed, however, the power to arrest shall be subject to necessary safeguards.

- The Court held that the offences under the CGST Act are not grave to an extent where the custody of the accused can be held to be sine qua non. It further held that custodial interrogation is neither warranted nor provided for by the statute and that detaining the Petitioner in Judicial Custody would serve no purpose rather would adversely impact the business of the Petitioner.

- Basis the above findings, the Hon'ble Court allowed the

anticipatory bail application filed under Section 438 of Code of

Criminal Procedure subject to satisfaction of stringent conditions

some of which are laid down hereunder:

- The Petitioner to furnish personal bond for INR 5 lacs with two solvent sureties

- He shall surrender his passport and under no circumstances leave India without prior permission of the Investigating Officer

- He shall cooperate in the investigation and appear when summoned;

- He shall not directly or indirectly make any inducement, threat, or promise to any person acquainted with the facts of the case;

- He shall provide his mobile number and keep it operational at all times;

- He shall drop a PIN on Google map to ensure that his location is available to the Investigating Officer;

- He shall commit no offence whatsoever during the period he is on bail.

Purchasing dealers can claim refund of excess CST collected on inter-state purchase of HSD

Tata Steel Ltd. & Anr. Vs. State of West Bengal [TS – 539-HC-2021 (CAL)-VAT]

FACTS OF THE CASE

- The Petitioners were purchasing HSD from IOCL situated in the State of West Bengal for use in its mining units situated in the State of Jharkhand at a concessional rate of tax under Section 8(3) of the Central Sales Tax Act, 1956 (CST Act) against issuance of "C" Form to IOCL.

- However, due to non-issuance of "C" Forms by State of Jharkhand, such concessional rate was denied by the State of West Bengal during the period July 1, 2017 to October 2018. Thus, during the said period, IOCL collected and deposited CST at full rate.

- Thereafter, the High Court of Jharkhand vide its interim Order dated May 17, 2018 further upheld by final order dated August 28, 2019 in the assessee's own case directed the State of Jharkhand to issue "C" Forms to the Petitioner. It further held that Petitioners would be entitled to claim refund of excess CST from sellers or from respective State Government. The Order dated August 28, 2019 was upheld by Hon'ble Supreme Court vide order dated September 13, 2021.

- Thereafter, the Petitioners obtained "C" Forms from the State of Jharkhand and submitted to IOCL for further submission with State of West Bengal, yet the State of West Bengal did not refund the excess CST so collected through IOCL.

- Being aggrieved, this Petition is filed by the Petitioners challenging the actions of State Government of West Bengal in refusing to refund the differential amount of CST collected through IOCL.

JUDGEMENT

- The Hon'ble Court inter alia held that since the Petitioners actually suffered and were subject to excess CST, the Petitioners are persons aggrieved and can challenge denial of refund of differential CST. They have locus standi to file a Writ Petition for refund of excess CST.

- The Court also remarked that "State cannot behave like an unfair private businessman and practice unjust enrichment by taking undue advantage of its own wrong in justification of its action of depriving the petitioners benefit of their statutory right to purchase HSD oil at concessional rate of tax".

- It was further held that in the absence of any specific prohibition under the statute, revenue should not get entangled in the cobweb of procedures and deprive the legitimate claim of the Petitioners.

- Accordingly, the Hon'ble Court directed the State of West Bengal to refund the amount of excess CST so collected along with interest at rate of 10% per annum to the Petitioners after inter alia verification of "C" Forms submitted by IOCL.

Denial of input tax credit is not justifiable if supplier appeared to be fake after completion of purchase transaction

LGW Industries Ltd & Ors. vs. Union of India & Ors. [TS-728-HC(CAL)-2021-GST]

FACTS OF THE CASE

- Various notices were issued to the assessee for denial of input tax credit along with a demand of interest and penalty on the purchases made from various suppliers. This was made on the grounds that such suppliers are not registered taxable persons (RTP) as the registration of such suppliers was cancelled with retrospective effect covering the transaction period in question.

- The assessee argued that the transactions in question were genuine and valid by relying upon (i) Government portal showed registrations of suppliers as valid and existing at the relevant time of transactions in question (ii) payments for all purchases in question were made through proper banking channels (iii) no cogent evidence to establish collusion between supplier and purchasers (iv) invoice-wise details of all the purchases in question were available on the GST portal in form GSTR-2A of the assessees.

- Accordingly, the assessee argued that they had undertaken due diligence in verifying the genuineness of the supplier at the relevant time and the assessee could not be faulted if they appeared to be fake later on.

JUDGEMENT

- The Hon'ble High Court remanded the matter to consider afresh and allow benefit of ITC to the assessee after considering the documents submitted by the assessee demonstrating that (a) payments on purchases in question were actually paid to the suppliers with GST (b) the transactions and purchases were made before the cancellation of registration of the suppliers (c) assessee had complied with statutory obligation of verification of identity of the suppliers and (d) all purchases are supported by valid documents.

Appeal involving limitation issue maintainable before High Court

Hindustan Petroleum Corporation Ltd. [ TS-577-HC-2021(BOM)-EXC

FACTS OF THE CASE

- The Respondent-assessee received non-duty paid Superior Kerosene Oil (SKO) from their refinery and cleared the same on payment of duty to Public Distribution System dealers and other Oil Marketing Companies. The Appellant – Revenue - issued a notice alleging that the Respondent – Assessee - paid Central Excise duty on a value lesser than that recovered by them from the other oil marketing companies in contravention of Section 4(1)(a) of the Central Excise Act 1944 (Excise Act). The Appellant demanded differential duty by invoking extended period of limitation

- On adjudication, the demand raised in the notice was upheld and being aggrieved the Respondent filed an appeal before Hon'ble CESTAT. CESTAT vide Order dated 31.10.2017 upheld the allegations on merits but set aside the demand on limitation. Being aggrieved, the Appellant- revenue filed an appeal before Hon'ble High Court. However, the Division Bench of High Court raised a question of maintainability of the appeal under Section 35G of the Excise Act and owing to conflicting views, referred the matter to the Larger bench.

JUDGEMENT

- The Court observed that the CESTAT Order, to the extent it confirmed demand of duty, interest and penalty on merits, has attained finality in as much as no appeal was filed by the Respondent- Assessee against such Order. Thus, only the issue of limitation is raised in the Central Excise appeal filed by the Appellant - Revenue.

- The Court observed that the presence of a question of law having a direct and/or proximate nexus to the determination of the applicable rate of duty or the value of the goods for the purposes of assessment of duty is a sine qua non for admission of the appeal before Supreme Court under Section 35L of the Excise Act. The Court opined that the issue of limitation - in this case - being purely question of fact or a mixed question of fact and law - disclosed in decision of the Tribunal- would thus not be a decision in rem but has to be in personal. Thus an appeal would not lie before Supreme Court.

- Hon'ble High Court also stated that the Tribunal set aside the demand under extended period purely based on findings of facts inter se and that such issue of limitation did not involve a question of general/public importance falling under Section 35L of the Excise Act.

- Hon'ble High held that the issue of limitation raised in this Central Excise Appeal has no direct or proximate relationship to the rate of duty and the value of goods for purposes of assessment and therefore, appeal is maintainable in the High Court as per Section 35G of the Excise Act.

Provider of back office services and IT & ITES services does not constitute "intermediary"

Macquarie Global Services Pvt. Ltd. [ TS-529-CESTAT-2021-ST ]

FACTS OF THE CASE

- The assessee had filed refund claim under Rule 5 of the CENVAT Credit Rules, 2004 (Credit Rules) for refund of unutilized credit used for providing back-office support services and IT and ITeS to its various overseas group entities.

- However, on noticing certain reimbursements claimed by the Appellant in its Transfer pricing documentation, the Department alleged that the functions performed by the Appellant related to facilitating the payment on behalf of associated entities. Thus, the Appellant constitutes "intermediary" under Rule 2(f) of the Place of Provision Rules, 2012 (POPS Rules). The Department also alleged that place of provision of such services falls in India as per Rule 9 of the POPS Rules and services so provided do not constitute export of services as per Rule 6A of the Service Tax Rules, 1994 (ST Rule). It rejected the refund claim.

- The assessee argued that they do not fall within the definition of "Intermediary Services" as laid down in the case of Orange Business Solutions Pvt. Ltd [2019 (27) GSTL 523 (T-Chand)] and Circular No 159/15/2021-GST dated September 20, 2021. The assessee also argued that the Department cannot reclassify the services in a refund claim filed by the assessee.

JUDGEMENT

- The Hon'ble Tribunal observed that the issue for consideration before both the authorities was validity of refund claims filed under Rule 5 of Credit Rules, and not whether the services provided by them were the "intermediary services". The original authority, however, misdirected himself, by considering the nature of the output services, to determine the eligibility of the refund claim.

- Relying on various judgements, the Hon'ble Tribunal stated that for a person to be said to be "intermediary", there should be two distinct services and three persons involved. The intermediary should be the person who is facilitating the provision between the other two persons. The Hon'ble Court held that while considering the issue on the ground of "intermediary services" both the authorities have at no stage identified the three persons, and have solely relied upon certain analysis in the transfer pricing document. Basis this, the Court held that the service provided by the Appellant do not qualify as a service under "Intermediary Services".

DRI officer is not "proper officer" for assessment of imported goods

Unik Traders [ TS-548-HC-2021(MAD)-CUST ]

FACTS OF THE CASE

- The assessee imported Areca Nuts from Mynamar and before commencement of assessment, the Assistant / Additional Commissioner of Customs (customs officers) collected test samples for testing. The assessee also executed a test bond of the value of consignments before customs officers. However, before the assessment could be completed by customs officers, DRI officers stalled the assessment and clearance of goods.

- The issue in the present case is whether the imported consignments of Areca nuts is to be classified under Chapter 0802 or under Sub Heading 2106 of the Customs Tariff Act,1975 (Tariff Act). Also, whether the DRI officers are "proper officers" as defined Section 2(34) of the Customs Act, 1972 (Customs Act).

JUDGEMENT

- Relying on Section 2(34) of the Customs Act read with Notification No.40/2012-Cus (N.T.) dated 02.05.2012, the Court held that the Deputy Commissioner or the Assistant Commissioner of Customs are designated as "proper officer" for various functions under the Customs Act including for the purpose of assessment of imported consignment and not DRI officers.

- The Court opined on the determination as to whether prohibition of imported goods can be carried only by a "Proper Officer" and cannot be usurped by DRI officers.

- The Court also stated that merely because DRI officers have powers to investigate by itself, will not mean that they can insist on a "hands off approach" by a competent proper officer who have been given the powers to assess Bill of Entry filed by an importer. If DRI officers felt the import was without proper license or of prohibited goods, the DRI officers could have informed the Customs officers which are designated proper officers to make a proper assessment.

- The Court held that the "proper officer" who has been given the task to assess the Bill of Entry - which involves both classification and valuation and determination as to whether the import of the goods is prohibited - should be allowed to pass appropriate Order under the Custom Act. Such proper officers can rely on the information which may be passed on by the DRI officers while assessing the goods. Accordingly, the High Court directed the Customs officers to complete assessment in a time bound manner.

ADVANCE RULING

Vouchers constitute goods and not actionable claims

In re: Premier Sales Promotion Pvt. Ltd. [TS-714-AAAR(KAR)-2021-GST]

FACTS OF THE CASE

- The assessee is engaged in the trading of vouchers having pre-defined face value to its merchants. The assessee supplies various types of vouchers such as 'gift vouchers', 'cashback vouchers' and 'open vouchers' redeemable at specified merchants for purchase of goods or services. The assessee purchases vouchers from entities authorized by RBI to issue vouchers on payment of consideration and sells the vouchers to its clients for a consideration.

- The Authority for Advance Ruling (AA) held that the trading of vouchers is a supply in terms of Section 7(1)(a) of the CGST Act and amounts to supply of goods and GST will be levied as per S.No. 453 of the Notification No. 1/2017 – CGST dated 28.06.2017.

- The assessee has assailed the Ruling before the Appellate Authority for Advance Ruling (AAAR) primarily on the ground that vouchers are consideration for purchase of goods and services and consideration cannot be held as "goods".

ADVANCE RULING

- The AAAR stated that the vouchers are a form of payment instruments recognized by RBI and in the instant case vouchers are bought and sold by the assessee on principal-to-principal basis and the assessee does not require RBI authorization for trading in these vouchers. The Authority observed that "money" is inter alia defined under Section 2(75) of the CGST Act to include a payment instrument used as consideration to settle an obligation. The Authority noted that "money" settles an obligation but the vouchers in the hands of the assessee does not settle any obligation but creates one. The settlement of the obligation occurs only at the time when ultimate beneficiary uses the voucher to purchase goods or services. Basis this, the Authority held that the vouchers in question do not constitute "money".

- The Authority thereafter held that vouchers in question are movable property as they have a monetary value and are capable of being transferred and thereby constitute "goods" under the CGST Act.

- The Authority also observed that actionable claims cover two types of claim (i) claim to an unsecured debt and (ii) beneficial interest in a movable property. The Authority opined that the vouchers are not claim to any debt and in present case, voucher is in possession of claimant at the time of claim and hence, cannot be considered as actionable claim.

In view of the above, the AAAR upheld the order passed by the Authority for Advance Ruling and dismissed the appeal filed by the assessee.

NOTIFICATION/CIRCULARS

| S.No. | Reference | Particulars |

| GST | ||

| 1. | Notification No. 18/2021-Central Tax (Rate) dated December 28, 2021 |

|

| 2. | Notification No. 19/2021-Central Tax (Rate) dated December 28, 2021 |

|

| 3. | Notification No. 20/2021-Central Tax (Rate) dated December 28, 2021 |

|

| 4. | Notification No. 2/2021-Compensation Cess (Rate) dated December 28, 2021 |

|

| 5. | Notification No. 39/2021-Central Tax dated December 21, 2021 |

|

| 6. | Notification No. 40/2021-Central Tax dated December 29, 2021 |

|

| 7. | Circular No. 167/23/2021-GST dated December 17, 2021 |

|

| 8. | Circular No. 164/24/2021-GST dated December 30, 2021 |

|

| 9. | Press Release dated 31.12.2021 |

|

| Customs | ||

| 1. | Notification No. 55 /2021-Customs dated December 29, 2021 | Amends the Customs Duty Exemption Notification – Notification No. 50/2017 – Customs dated June 30, 2017 in order to align the HSN mentioned therein with the new edition of HSN 2022. |

| 2. | Notification No. 56 /2021-Customs dated December 29, 2021 | Amends Notification No. 82/2017 – Customs dated October 27, 2017 which prescribes rate of customs duty on textile products, in order to align the HSN mentioned therein with the new edition of HSN 2022. |

| 3. | Notification No. 57 /2021-Customs dated December 29, 2021 | Amends the following notifications exempting

specified goods from customs duty in order to align the HSN

mentioned therein with the new edition of HSN 2022:

|

| 4. | Notification No. 58 /2021-Customs dated December 29, 2021 | Amends Notification No. 11/2018 – Customs dated February 2, 2018 which exempts certain goods from levy of Social Welfare Surcharge, in order to align the HSN mentioned therein with the new edition of HSN 2022. |

| 5. | Notification No. 59 /2021-Customs dated December 29, 2021 | Amends Notification No. 53/2017 – Customs dated June 30, 2017 which levies additional customs duty (SAD) on certain goods imported into India, in order to align the HSN mentioned therein with the new edition of HSN 2022. |

| 6. | Instructions F.No. 401/85/2021-Cus-III dated December 01, 2021 | Import of Sajji Khar/Pappad Khar does not require product approval under FSS Regulations, 2017 till standards are notified by Food Safety and Standards Authority of India. |

| 7. | Notification No. 68/2021-Customs (ADD) dated December 06, 2021 | Imposes ADD on imports of Certain Flat rolled Products of Aluminium from China. |

| 8. | Notification No. 69/2021-Customs (ADD) dated December 13, 2021 | Imposes ADD on imports of Axle for Trailers in CKD/SKD from China. |

| 9. | Notification No. 71/2021-Customs (ADD) dated December 17, 2021 | Imposes ADD on imports of Sodium Hydrosulphite from China and Korea RP. |

| 10. | Notification No. 73/2021-Customs (ADD) dated December 17, 2021 | Imposes ADD on imports of calcined gypsum powder from Iran, Oman, Saudi Arabia and UAE. |

| 11. | Notification No. 74/2021-Customs (ADD) dated December 21, 2021 | Imposes ADD on imports of Silicone Sealant from China. |

| 12. | Notification No. 75/2021-Customs (ADD) dated December 21, 2021 | Imposes ADD on imports of HFC R-32 from China |

| 13. | Notification No. 76/2021-Customs (ADD) dated December 21, 2021 | Imposes ADD on imports of Hydrofluorocarbon Blends (All blends other than 407 and 410 are excluded) from China. |

| 14. | Notification No. 77/2021-Customs (ADD) dated December 27, 2021 | Imposes ADD on imports of Décor Paper from China |

| 15. | Notification No. 78/2021-Customs (ADD) dated December 27, 2021 | Amends HSN provided in various notifications imposing anti-dumping duty to align them with HSN 2022. |

| Foreign Trade Policy | ||

| 1. | Notification No. 46/2015-2020 dated December 20, 2021 |

|

| 2. | Notification No. 47/2015-2020 dated December 20, 2021 |

|

| 3. | Notification No. 48/2015-2020 dated December 31, 2021 |

|

| 4. | Trade Notice No. 28/2021-22 dated December 31, 2021 |

|

| Central Excise | ||

| 1. | Notification No. 10/2021 dated December 29, 2021 |

|

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.