Background

Impact investments are generally understood as investments made with the intent to generate impact (social and environmental). Impact investments may be made in any area where (a) there is a need for social upliftment; and (b) such upliftment matches with the investors' strategic goals.

Impact investments in India have been facilitated through different legal structures like Alternate Investment Funds ("AIFs") regulated by the Securities and Exchange Board of India; Non-Banking Financial Companies ("NBFCs") regulated by the Reserve Bank of India ("RBI"); foreign donations regulated by the Ministry of Home Affairs ("MHA"); and impact bonds ("IBs").

IBs, when backed by Government donations are identified as 'social impact bonds'; and when backed by private donations are identified as 'development impact bonds'. IBs gained popularity due to their potential to facilitate 'outcome-based funding'. This means that the donors are able to identify and fund projects to the extent it meets such donor's outcome assessment criteria/ metrics. IBs have also turned out to be a good source of profit generation for the private sector.

Concept of Impact Bonds

The very nature of IBs is nothing but an innovative financing mechanism in which governments/ donors enter into agreements with social service providers (which may be for-profit or non-profit organizations), investors and impact assessment agencies, to pay for the delivery of pre-defined outcomes. In general, IBs may be defined as "a contract with the Government/ donor, whereby it pays for better social outcomes in certain areas and passes on part of the savings achieved to the investors".

As per Forbes, the United States of America is the only country that has managed to introduce a central law on the subject, Social Impact Bond Act, 2014 which is proposed to enable the U.S. federal government allocate $300 million to social IBs. Even before this central law was enforced, various states in the country had already introduced laws at the state level to regulate and implement IBs.

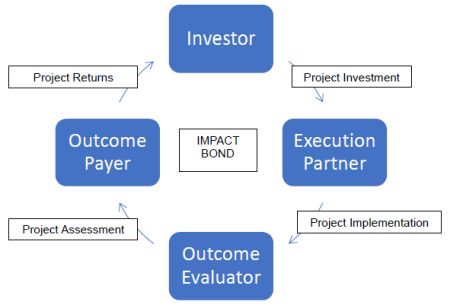

Working of Impact Bonds

IBs operate in a unique symphony between (a) an investor; (b) an outcome funder; (c) an execution partner; and (d) an outcome evaluator. Typically, the investor invests funds in an execution partner, which executes the project to achieve certain pre-determined outcomes, which are evaluated by the outcome evaluator. Based on the assessment provided by the outcome evaluator, the investor receives its principal investment amount + additional pre-agreed profits, from the outcome funder.

Initial Impact Bonds in India

India has been a witness to the first successful implementation of IBs through Educate Girls (an Indian NGO) in 2014. The objective of this IB was to reduce the gender gap in education in Rural India by getting girls into schools and promoting learning. UBS Optimus Foundation (the investor) provided an investment to Educate Girls (the execution partner). Children's Investment Fund Foundation (the outcome payer) agreed to pay (based on enrolment and learning outcomes) to UBS their initial investment plus a return on investment based on the performance of the program. ID Insight (the outcome evaluator) evaluated the program. In 2018, a review of this program showed that IBs resulted in a 52% return on investment because of high achievement of pre-defined targets.

In 2018, the British Asian Trust announced then world's largest IB for education to support three charities in India. This was finally launched with a coalition of partners including UBS Optimus Foundation, Tata Trusts, Michael & Susan Dell Foundation, Comic Relief, the Mittal Foundation, the UK Government's Department for International Development (DFID) and the BT (British Telecom), and committed contributions up to USD 11 million. According to some reports, these IBs have successfully been transforming future lives of Indian children.

Indian Legal Landscape and IBs

With multiple instances implementing IBs in India, it is pertinent to understand the legal landscape affecting various stakeholders involved in this process.

The IB Investor

The nature of transaction between (a) the IB investor and the IB execution partner; or (b) the outcome funder and the IB investor, depends on their ability to give and receive the IB investment/ fund. In case the IB investor is based in India, such ability is dictated by the nature of its legal embodiment under the Indian laws. For instance, conceptually, an IB investor may be an AIF, an NBFC, a non-profit foundation, a trust fund or an individual person. Depending on the nature of entity embodying an IB investor, relevant regulations will apply to the Indian IB investor.

In case the IB investor is a foreign entity, then any transaction involving them will be regulated by RBI through the Foreign Exchange Management Act (and the regulations thereunder) ("FEMA"); or MHA through the Foreign Contribution (Regulation) Act (and the rules thereunder) ("FCRA"), provided the other entity (i.e., the outcome funder or the IB execution partner) is an Indian resident. If the IB investor as well the other parties are based outside India, such relationship may not fall within the Indian jurisdiction at all.

The Outcome Funder

The outcome funder is generally a government body or a charity which seeks only outcomes in exchange for the funding of the IB investor. If it is a charity/ NGO based in India, then donations made by such NGOs will be regulated majorly by the FCRA and the (Indian) Income Tax Act ("ITA"). Indian NGOs are generally not allowed to donate to foreign entities.

In case the outcome funder happens to be a government body, such an IB may be called a 'social IB' and such donations will be regulated as per the ITA and applicable Government policies/ schemes. The outcome funder may also be an international organization like the UNDP. Such organizations are generally exempt from FCRA.

The Execution Partner

As stated above, the nature of transaction between the execution partner and the IB investor, shall depend on their ability to give and receive the IB investment/ fund. In case the execution partner is based in India, such ability will be dictated by the nature of legal embodiment of the execution partner, under the Indian laws. For instance, conceptually, an execution partner may be a for-profit (whose ability to receive is regulated by the Companies Act, 2013, FEMA and ITA) or a non-profit entity (whose ability to receive is regulated by the applicable law of incorporation, FCRA and ITA).

In case the execution partner is a foreign entity, then transaction with such an entity will be regulated by RBI through the Overseas Direct Investment Regulations and the Liberalized Remittance Scheme, in addition to other laws, as applicable, provided the IB investor is based in India.

The Outcome Evaluator

In this whole process of implementing an IB, the outcome evaluator operates as a service provider for the IB investor, or the outcome funder, or the execution partner, or a combination of such (depending on the contractual arrangements between the parties). Accordingly, transactions involving the outcome evaluator are mostly in the nature of service contracts, wherein income of the outcome evaluator is taxed as per the ITA. Service contracts typically do not fall under FDI and are exempt from FCRA.

In most of the existing examples, the execution partner is generally a non-profit based in India while the IB investor and the outcome funder are entities based outside India. Other possibilities and structures have certain regulatory challenges which may take time to resolve.

Are we there yet?

Recent recognition of zero coupon zero principal securities seems to encourage issue of IBs by non-profit social enterprises. However, apart from regulatory challenges, IBs are yet to overcome certain hurdles before they gain wide acceptance. Such hurdles include the overall cost of implementing the structure, the unnecessary complexity involving flow of funds, difficulty in arriving at a mutually agreeable impact metrics, and over-quantifying impact outcomes leading to loss of focus on qualitative outcomes.

At this point, there's no general opinion as to IBs being a "good" or a "bad" option for social financing. Investing through IBs has benefitted many (including beneficiaries, donors and investors). Implementation of projects through IBs is required to be evaluated on a case to cases basis, and should be subject to the cost benefit analysis in each instance.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.